Specialty Biocides Market Valuation 2025–2034: $8.7 Billion to $18.9 Billion at 9% CAGR Driven by Chlorine-Free Disinfection and Sustainable Preservatives

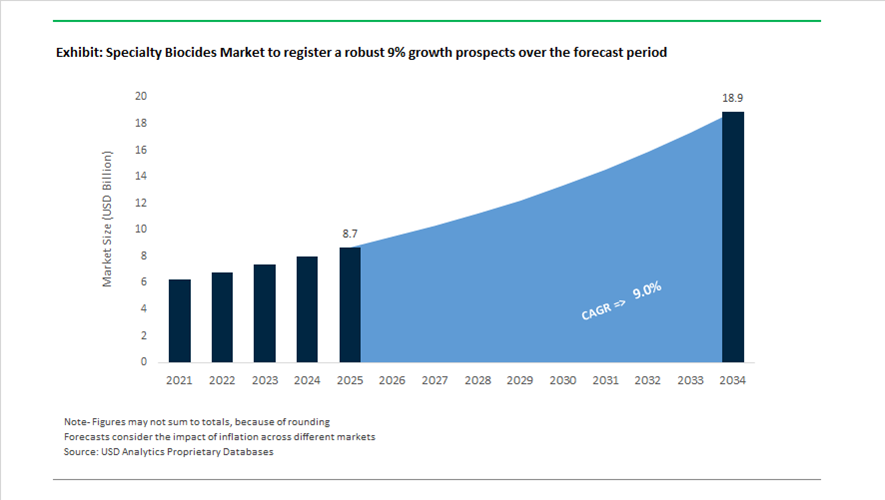

The global specialty biocides market is valued at $8.7 billion in 2025 and is projected to reach $18.9 billion by 2034, expanding at a strong CAGR of 9%. Growth is driven by increasing demand for antimicrobial additives, oxidizing biocides, preservatives, peracetic acid (PAA), performic acid (PFA), isothiazolinones, and multifunctional microbial control agents across water treatment, paints and coatings, construction materials, healthcare, personal care, and food processing. Regulatory tightening in the EU and North America, particularly restrictions on chlorine-based disinfectants and hazardous preservatives, is accelerating the transition toward chlorine-free, low-toxicity, and rapidly biodegradable biocidal chemistries. Sustainability-driven procurement, EPA registration requirements, and advanced formulation technologies are reshaping product development and market positioning.

In June 2024, LANXESS expanded capacity for sustainable preservative lines at its Krefeld-Uerdingen site in Germany, targeting environmentally optimized microbial control for food and coatings applications. In August 2024, Ecolab launched an enzyme-based Clean-in-Place system for protein processing facilities, reducing dependency on chlorine disinfectants while improving environmental safety in meat and poultry operations. In September 2024, BASF entered Brazil’s biocide market with advanced solutions tailored to construction and healthcare sectors. In October 2024, BASF introduced eco-resilient Irgaguard preservative formulations designed for coatings and packaging requiring lower environmental impact. During 2024–2025, Arxada modernized three large-scale U.S. production sites following its acquisition of Enviro Tech Chemical Services, scaling output of peracetic acid as a sustainable chlorine alternative.

Product innovation and regulatory approvals accelerated in 2025. In February 2025, Arxada launched Polyboost™, a multifunctional additive designed to enhance biocide performance in paints and coatings, enabling reduced active dosages without compromising long-term protection. In March 2025, LANXESS introduced Preventol® OX, a chlorine-free oxidizing biocide presented at the European Coatings Show, aligned with strict EU disinfection standards. In May 2025, Kemira secured U.S. EPA registration for FennoSurf 600, the active foundation of KemConnect™ DEX, a performic acid-based antimicrobial solution that decomposes rapidly and supports automated, data-driven water treatment systems. In January 2025, Arxada reported a doubling of patent filings in 2024 focused on sustainable microbial control technologies following integration of Troy Corporation.

Strategic portfolio realignment reinforced specialization in 2025. On April 1, 2025, LANXESS completed the divestiture of its Urethane Systems business to UBE Corporation, finalizing its transition into a pure-play specialty chemicals and consumer protection company centered on disinfectants and preservatives. In October 2024, Sudarshan Chemical Industries acquired the Heubach Group, integrating specialty pigment technologies that require advanced biocide-stabilized formulations in coatings and industrial materials.

Key Trends and High-Value Opportunities in the Specialty Biocides Market

Regulatory Substitution Pressure Under the ECHA Exclusion Framework

The specialty biocides market is undergoing enforced structural change as regulators move from risk management toward outright exclusion of high-concern active substances. The enforcement posture of European Chemicals Agency under the Biocidal Products Regulation is no longer gradual or negotiable. It is compelling manufacturers to redesign portfolios, reformulate products, or exit regulated end markets altogether.

A defining inflection point is the Zinc Pyrithione substitution process. From late 2024 through 2025, ECHA advanced a formal consultation covering Product Types 6, 7, 9, and 21, concluding that Zinc Pyrithione meets Article 5(1) exclusion criteria. Unless proven essential to mitigate a serious and uncontrollable danger, its use in paints, coatings, and textiles faces restriction or phase-out. This has triggered an accelerated pivot toward non-metal, non-leaching biocide systems and functional alternatives that can meet durability and aesthetics requirements without regulatory exposure.

Parallel pressure is evident in the isothiazolinone class. Tightened sensitization labeling under H317 for MIT and CIT has forced producers to rethink not only active selection but lifecycle exposure. In response, LANXESS introduced Klarix XIT at the 2025 European Coatings Show. This de-activation technology allows biocides to perform during manufacturing and storage before being chemically neutralized in the final formulation. The result is compliance with consumer-facing labeling expectations while preserving production-level microbial control, a shift that illustrates how regulatory pressure is now driving innovation rather than incremental substitution.

Non-Discretionary Biocide Demand in Water-Based and Low-VOC Systems

Sustainability policy is structurally increasing biocide intensity across multiple end-use segments. As solvent-based systems decline, water-based formulations have become the default across architectural coatings, metalworking fluids, and industrial additives. This transition inherently raises microbial risk, creating a permanent baseline demand for advanced preservation chemistries rather than a cyclical or discretionary one.

The EU VOC Solvents Emissions Directive has reduced allowable VOC levels by more than 60% versus 2010 benchmarks, pushing water-based paints to represent over 70% of architectural coatings consumption by 2025. These systems are intrinsically more susceptible to bacterial and fungal growth, resulting in a 40% to 60% higher preservative requirement per liter compared to solvent-based predecessors. As a result, biocides are no longer optional formulation components but critical performance enablers.

To address this challenge without escalating hazard labeling, innovation is shifting toward multifunctional stabilization systems. Arxada launched Polyboost in early 2025, a technology that stabilizes pH and viscosity while allowing lower preservative dosages. This approach enables extended in-can shelf life and microbial control while helping manufacturers avoid restrictive sensitization labels. Such solutions reflect a broader market trend where preservation performance, regulatory compliance, and brand perception must be optimized simultaneously.

Bio-Targeted and Biocide-Free Antifouling for Net-Zero Shipping

Maritime regulation is creating one of the most attractive white spaces in the specialty biocides market. As global shipping aligns with decarbonization targets, regulators are moving beyond bans on tributyltin and Cybutryne toward restrictions on copper-based antifouling systems. The 2025 Net-Zero framework issued by International Maritime Organization directly links hull efficiency to carbon intensity metrics. Biofouling-related drag can increase fuel consumption by up to 40%, turning antifouling performance into a decarbonization lever rather than a maintenance consideration.

This shift is accelerating adoption of controlled-elution and biocide-free technologies. Nippon Paint Marine expanded its FASTAR portfolio using hydrophilic nanodomain technology that reduces biocide release by up to 50% while delivering measurable fuel efficiency gains. Its AQUATERRAS system represents the first fully biocide-free self-polishing coating, offering compliance in sensitive coastal and aquaculture zones. These systems command premium pricing because they align fuel savings, regulatory compliance, and biodiversity protection, transforming antifouling from a cost center into a strategic efficiency investment.

Performance-Integrated Preservation for Green Building Materials

Decarbonization in construction is creating a structurally new demand category for specialty biocides. As builders adopt wood-plastic composites, bio-based insulation, and low-carbon concretes, material susceptibility to mold, algae, and microbial degradation is rising. This is driving demand for performance-integrated preservatives that function as structural enablers rather than add-on chemicals.

The growth of bio-based WPCs illustrates this shift. In 2025, Trex Company partnered with NatureWorks to launch next-generation composites using recycled PLA and wood fibers. These materials require fungicides capable of surviving extrusion temperatures above 180°C while maintaining long-term UV and fungal resistance. This has created a niche for high-durability, thermally stable biocides engineered specifically for polymer processing environments.

A similar pattern is emerging in low-carbon cement and concrete systems. The use of organic grinding aids and admixtures increases microbial risk during storage and circulation. To address this, Arxada’s Enviro Tech unit introduced on-site peracetic acid generation technology in October 2025. This low-odor, reduced-corrosivity solution supports large-scale water and material preservation while aligning with green construction mandates. Collectively, these developments position functional biocides as essential components of sustainable building systems, anchoring long-term demand growth in the specialty biocides market.

Specialty Biocides Market Share and Segmentation Insights

Quaternary Ammonium Compounds Lead the Specialty Biocides Market with Broad-Spectrum Antimicrobial Performance

Quaternary ammonium compounds accounted for 28.40% of the specialty biocides market in 2025, making them the leading product category across multiple antimicrobial applications. Compounds such as benzalkonium chloride and didecyl dimethyl ammonium chloride provide strong broad-spectrum antimicrobial activity, surface compatibility, and long-lasting residual protection, supporting their use in water treatment systems, paints and coatings, personal care formulations, and industrial sanitation products. Their surfactant properties also enhance cleaning and surface wetting performance in many formulations. A key 2025 industry development is the increasing focus on biocide reformulation to improve environmental compatibility, where manufacturers are developing more readily biodegradable quaternary ammonium compounds while maintaining the established cost-performance advantages and regulatory acceptance that sustain their widespread use.

Water Treatment Sector Drives Global Demand for Specialty Biocides

Water treatment represents the largest application segment in the specialty biocides market, accounting for 32.80% of global demand in 2025 due to the need for microbial control in industrial and municipal water systems. Biocides are widely used in cooling towers, wastewater treatment plants, municipal water systems, and industrial water circuits to prevent biofilm formation, bacterial growth, and microbiologically influenced corrosion. Effective microbial control ensures operational efficiency and protects infrastructure from biological fouling. A major 2025 industry driver is the increasing emphasis on Legionella risk management in water systems, particularly in cooling towers, healthcare facilities, and large commercial buildings. This has led to stricter water monitoring programs and specialized biocide treatment protocols designed to control Legionella bacteria and improve public health protection.

Specialty Biocides Market Competitive Landscape

The global specialty biocides market in 2026 is shaped by regulatory-driven green chemistry adoption, micro-encapsulation innovation, and chlorine-free antimicrobial solutions. Leading players are focusing on sustainable biocide formulations, integrated hygiene platforms, and advanced microbial control technologies across water treatment, coatings, agriculture, and industrial applications.

LANXESS Strengthens Low-Biocide Formulations and Integrated Hygiene Solutions Through CDP Concept and Klarix Innovation

LANXESS AG is reinforcing its leadership in specialty biocides following the integration of IFF’s Microbial Control business, expanding its portfolio across material protection and hygiene applications. Its Klarix XIT innovation enables low-biocide or biocide-free coatings by breaking down CIT/MIT residues post-production, addressing strict EU regulatory requirements. The company’s CDP (Control–Detect–Prevent) framework integrates Preventol OX, a chlorine-free disinfectant positioned as a sustainable alternative to DBNPA. Under its FORWARD! program, LANXESS achieved €150 million in savings and is targeting an additional €100 million by 2028. Its strong IP portfolio spans animal biosecurity, industrial water treatment, and wood preservation. The company’s focus on integrated microbial management strengthens its competitive position in regulated markets.

Arxada Advances Micro-Encapsulation and Multifunctional Biocide Additives with LEAP Platform and Polyboost™ Innovation

Arxada AG is driving innovation in specialty biocides through its LEAP platform, with Polyboost™ enabling reduced preservative usage by enhancing formulation stability and performance. Its TIME micro-encapsulation technology, used in products like Polyphase® 862CR, minimizes active ingredient leaching while extending durability in coatings. The EPA registration of PeraGuard® AH strengthens its presence in agricultural biosecurity, particularly in combating avian influenza risks. Arxada’s sustainability credentials are reinforced by Social Seal Certification at its Salto site. The company’s focus on multifunctional additives and controlled-release biocides aligns with regulatory and environmental demands. Its advanced encapsulation technologies enhance efficiency and compliance across applications.

Solenis Expands Global Biocide and Water Treatment Capabilities Through NCH Acquisition and Innovation-Driven Sustainability Model

Solenis LLC is scaling its position in specialty biocides through the acquisition of NCH Corporation, significantly expanding its footprint in industrial water treatment and hygiene solutions. With 74% of revenue linked to sustainability-driven solutions, the company is aligning its portfolio with circular economy principles. The establishment of a Global Research Center in Delaware supports development of next-generation antimicrobial and water stewardship technologies. Integration of ClearPointSM biofilm detection and Oxivir™ disinfectants enables advanced microbial control across global operations. Solenis’ unified operational platform accelerates deployment of innovative biocide solutions. Its strong focus on sustainability and digital integration enhances its market leadership.

BASF Optimizes Biocide Portfolio Through Strategic Divestments and Focus on Integrated Agricultural and Antimicrobial Solutions

BASF SE is refining its specialty biocides strategy by divesting non-core assets such as its Aseptrol® chlorine dioxide business to focus on high-growth agricultural and industrial applications. Its Agricultural Solutions segment is advancing products like Ridivex herbicide, supporting integrated crop protection strategies. The company is scaling biomass balance polyether polyols production, enabling sustainable antimicrobial-ready materials for coatings and automotive applications. BASF’s Verbund integration ensures cost-efficient production of biocide intermediates, providing a competitive advantage during supply chain disruptions. Its focus on sustainable feedstocks aligns with global decarbonization goals. The company’s strategic portfolio optimization strengthens its position in specialty chemical markets.

Nouryon Advances Green Biocide Formulations and Bio-Based Additives for Industrial and Consumer Applications

Nouryon Chemicals is strengthening its position in specialty biocides through the development of bio-based and biodegradable additives that enhance antimicrobial performance. Its launch of fully biobased carboxymethylcellulose supports detergent formulations that maintain hygiene while reducing environmental impact. The company is focusing on green biocides using natural-derived raw materials and low-solvent systems to meet eco-label standards. Its Arquad® product line remains widely used in oilfield and industrial water treatment for microbial control. Strategic partnerships with IMCD expand distribution of antimicrobial solutions in textiles and leather across EMEA. Nouryon’s emphasis on sustainable chemistry and functional additives enhances its competitiveness in evolving regulatory environments.

United States Specialty Biocides Market Driven by Capacity Localization and PFAS Elimination

The United States specialty biocides industry is undergoing a decisive restructuring anchored in domestic capacity expansion and regulatory-driven reformulation. In March 2024, LANXESS expanded its North American footprint through the acquisition of a major U.S.-based biocide manufacturing facility, integrating the asset into its Material Protection Products division. This move strengthens local supply for wood preservation, construction materials, and hygiene applications at a time when U.S. customers are prioritizing domestic sourcing to mitigate regulatory and logistics risk. Parallel to capacity expansion, the market is adapting rapidly to the 2024–2025 EPA rulings on per- and polyfluoroalkyl substances. U.S. formulators have re-engineered surfactant and carrier systems to eliminate PFAS while preserving dispersion stability in aqueous coatings, industrial cleaners, and antimicrobial paints.

Portfolio consolidation and carbon accounting are further reshaping competition. In June 2025, Solenis entered into a definitive agreement to acquire NCH Corporation, creating a combined hygiene and water treatment platform with strong penetration in middle-market industrial and light water segments. Sustainability-linked innovation is also accelerating. Dow Personal Care introduced its Decarbia reduced-carbon platform at Suppliers’ Day 2025, pairing low-carbon silicone systems with specialty biocidal preservatives verified to deliver a 50% lower carbon footprint. In pulp and paper, restricted antimicrobials are being replaced with oxidative biocides that perform more effectively in recycled fiber loops, reflecting both EPA pressure and operational efficiency goals.

Germany Specialty Biocides Market Defined by Chlorine-Free Alternatives and Regulatory Simplification

Germany’s specialty biocides market is positioned at the intersection of regulatory rigor and formulation innovation. At the European Coatings Show 2025, LANXESS launched Preventol OX, a chlorine-free oxidizing biocide designed as a technical alternative to highly regulated DBNPA for industrial process water and equipment sterilization. This launch reflects the broader German shift toward oxidant-based systems that meet tightening environmental thresholds while maintaining efficacy. An even more structural change emerged with the debut of Klarix XIT in 2025, a non-biocidal additive that allows manufacturers to use CIT and MIT during wet-phase processing and fully neutralize them before final product formation, resulting in biocide-free end products for sensitive applications.

Policy dialogue is reinforcing these innovations. In July 2025, the European Commission convened a high-level Implementation Dialogue on the Biocidal Products Regulation, initiating a simplification package intended to reduce approval timelines for innovative, lower-impact actives. Sustainability signaling has become commercialized. LANXESS has transitioned its preservative portfolio under the Scopeblue label, certifying either a minimum of 50% sustainable raw materials or a 50% lower carbon footprint compared with conventional benchmarks. These developments position Germany as a lead market for compliant, low-toxicity biocide systems in coatings, construction chemicals, and industrial water treatment.

China Specialty Biocides Market Anchored by Verbund Integration and Food-Contact Standards

China’s specialty biocides industry is scaling through integrated production platforms and stricter national safety standards. In November 2025, BASF SE commenced production at the core of its Zhanjiang Verbund site, a multibillion-euro investment that includes downstream intermediates critical for advanced industrial biocides supplied to the Asia-Pacific coatings market. This integration improves cost efficiency, quality control, and supply reliability for performance preservatives used in architectural and industrial coatings.

Capacity expansion is complemented by formulation upgrades. Clariant completed an 80 million CHF expansion at its Daya Bay facility in late 2025, increasing output of specialty surfactants and ingredients engineered to reduce VOC emissions in biocide-stabilized home care formulations. Regulatory enforcement is reshaping product specifications. The late-2025 implementation of GB 4806.16-2025 has forced a transition to high-purity antimicrobials in food packaging, eliminating trace heavy metals from preservative systems used in food-contact plastics. In parallel, BASF commissioned a Controlled Free Radical Polymerization dispersant line in Nanjing to enhance stability and performance of biocidal pigments, reinforcing China’s role as a technology-forward manufacturing hub.

India Specialty Biocides Market Expanded by Bio-Innovation and Infrastructure Spending

India’s specialty biocides market is expanding through a dual pathway of bio-based innovation and infrastructure-driven demand. The BioE3 Policy approved in August 2024 introduced capital subsidies for bio-foundries, catalyzing domestic production of nature-inspired biocides derived from agricultural waste. These bio-based actives are increasingly targeted at crop protection and integrated pest management, aligning with India’s sustainability and rural value-add objectives.

Conventional demand is also rising sharply. Large-scale investments under the Jal Jeevan Mission and wastewater treatment upgrades in 2025 have driven increased consumption of halogenated biocides and quaternary ammonium compounds for municipal water disinfection. On the supply side, Indian manufacturers are moving up the value chain. Firms such as Anupam Rasayan reported a strategic shift in late 2025 toward acting as contract development and manufacturing partners for multinational biocide originators, focusing on complex, patent-protected active ingredients. This transition is positioning India as a high-end synthesis base rather than a commodity supplier.

Comparative Snapshot: Country-Level Specialty Biocides Dynamics

Specialty Biocides Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Hygiene, wood protection, paper

|

PFAS-free reformulation, domestic capacity

|

Localized supply and portfolio consolidation

|

|

Germany

|

Industrial water, coatings

|

Chlorine-free oxidants, neutralized biocides

|

Regulation-led innovation

|

|

China

|

Coatings, home care, packaging

|

Verbund integration, high-purity standards

|

Scaled, technology-integrated output

|

|

India

|

Water infrastructure, agriculture

|

Bio-based actives, CDMO synthesis

|

Value-chain upgrading

|

Specialty Biocides Market Report Scope

Specialty Biocides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.7 Billion

|

|

Market Size (2034)

|

$18.9 Billion

|

|

Market Growth Rate

|

9%

|

|

Segments

|

By Product Type (Halogen Compounds, Metallic Compounds, Organosulfur Compounds, Quaternary Ammonium Compounds, Phenolic Biocides, Organic Acid Biocides, Nitrogen-Based Biocides), By Application (Water Treatment, Paints & Coatings, Wood Preservation, Food & Beverage, Personal Care & Cosmetics, Oil & Gas, Pulp & Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LANXESS AG, Arxada AG, BASF SE, Dow Inc., Veolia Group, Solenis, Ecolab Inc., Nouryon, Clariant AG, Kemira Oyj, Lubrizol Corporation, Albemarle Corporation, Evonik Industries AG, Buckman Laboratories International, Neogen Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Biocides Market Segmentation

By Product Type

- Halogen Compounds

- Metallic Compounds

- Organosulfur Compounds

- Quaternary Ammonium Compounds

- Phenolic Biocides

- Organic Acid Biocides

- Nitrogen-Based Biocides

By Application

- Water Treatment

- Paints & Coatings

- Wood Preservation

- Food & Beverage

- Personal Care & Cosmetics

- Oil & Gas

- Pulp & Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Biocides Industry

- LANXESS AG

- Arxada AG

- BASF SE

- Dow Inc.

- Veolia Group

- Solenis

- Ecolab Inc.

- Nouryon

- Clariant AG

- Kemira Oyj

- Lubrizol Corporation

- Albemarle Corporation

- Evonik Industries AG

- Buckman Laboratories International

- Neogen Corporation

*- List not Exhaustive