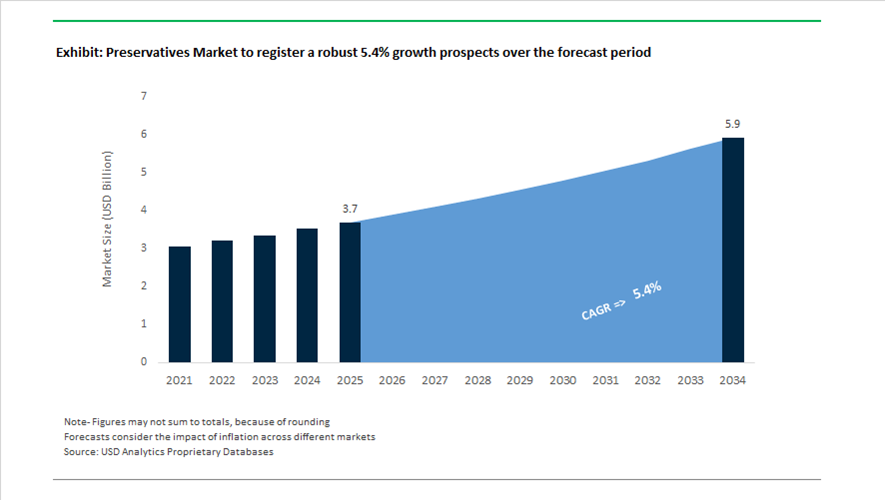

Preservatives Market Valued at $3.7 Billion in 2025, Projected to Reach $5.9 Billion by 2034 at 5.4% CAGR

The global preservatives market is valued at $3.7 billion in 2025 and is projected to reach $5.9 billion by 2034, expanding at a CAGR of 5.4%. Growth is being driven by rising demand for natural food preservatives, antimicrobial additives, cosmetic preservation systems, clean-label mold inhibitors, multifunctional formulation stabilizers, and bio-based preservation ingredients across food and beverage, personal care, home care, paints and coatings, and industrial applications. Regulatory tightening in Europe and North America, combined with consumer demand for paraben-free and naturally derived alternatives, is accelerating reformulation across multiple end-use industries.

Strategic portfolio repositioning intensified in 2024. In January 2024, Kobo Products introduced PreservEssence, a 100% natural preservative line targeting clean-label and organic cosmetics. In March 2024, Symrise formed Vizag Care Ingredients, a joint venture with India’s Virchow Group in Visakhapatnam, establishing its first chemical production base outside Europe and North America to serve Asia-Pacific demand for multifunctional actives and preservation ingredients. During the same month, Dow and SABIC announced a collaboration to develop bio-based preservatives for cosmetics, utilizing renewable feedstocks to reduce environmental impact compared to petrochemical-derived stabilizers. In late 2024, Kerry Group completed the divestiture of its Dairy Ireland business, finalizing its transition into a pure-play B2B nutrition and taste company and redirecting capital toward Niacet’s antimicrobial and food preservation technologies.

Innovation momentum accelerated in 2025. In February 2025, Arxada launched Polyboost™, a multifunctional additive for paints and coatings designed to enhance formulation stability while enabling lower preservative loading levels, reducing the need for hazardous H317 labeling. In March 2025, Clariant introduced Nipaguard® SCE Vita, a 100% natural preservation blend combining renewable sorbitan caprylate and naturally derived benzoic acid to deliver broad-spectrum microbial protection without reliance on controversial synthetic alternatives. In April 2025, Corbion unveiled Verdad Essence WH100, a cultured wheat-based mold inhibitor that enables bakery manufacturers to replace calcium propionate while maintaining shelf life through fermentation-derived antimicrobial action. That same month, BASF received European Commission approval for Myrtec MX, a natural-based preservation system reinforcing its expansion in the bio-derived cosmetics segment.

Corporate consolidation and operational restructuring are reshaping competitive dynamics. In May 2025, Clariant completed the acquisition of Huntsman Corporation’s specialty ingredients business, significantly expanding its global preservation solutions portfolio in home and personal care markets. Throughout 2024 and 2025, Lanxess implemented its “Forward!” action plan, achieving over €150 million in cost reductions while strengthening its Consumer Protection segment, which includes antimicrobial and preservative product lines. In late 2025, BASF advanced its “Winning Ways” strategy, announcing investment in a Ludwigshafen production facility utilizing 3D-printed X3D catalyst technology scheduled for 2026 startup. This technology improves process efficiency in manufacturing food-grade and industrial preservatives, lowering energy intensity and production costs.

The preservatives market is increasingly characterized by bio-based antimicrobial systems, fermentation-derived mold inhibitors, multifunctional preservative-reducing additives, renewable cosmetic stabilizers, clean-label bakery preservation, catalyst-driven process optimization, and Asia-Pacific capacity localization. Portfolio rationalization, regulatory approvals for natural ingredients, and sustainability-driven reformulation are reinforcing long-term demand across food, personal care, coatings, and industrial chemical sectors.

Strategic Trends and High-Value Opportunities Reshaping the Preservatives Market

Accelerated Reformulation Toward Clean Label and Natural Preservative Systems

The preservatives market is undergoing a structural reset as clean label expectations move from brand differentiation to market access criteria. Retailer-led ingredient blacklists, heightened scrutiny of Ultra-Processed Foods, and evolving regulatory expectations are forcing global food and beverage manufacturers to re-engineer preservation strategies at a portfolio level. Traditional synthetics such as potassium sorbate and sodium benzoate are increasingly being replaced with nature-identical and plant-derived alternatives that support short, recognizable ingredient lists while delivering reliable microbial control.

Fermentation-derived preservatives have moved firmly into the mainstream. According to strategic disclosures from Corbion, the company significantly expanded vinegar fermentation and lactic acid derivative capacity to address accelerating demand for label-friendly mold inhibition solutions. By late 2025, an estimated 38% of global packaged food preservative applications had transitioned to natural sources such as cultured dextrose, rosemary extract, and vinegar-based systems, representing a sharp increase over the prior three-year period. This shift is particularly pronounced in bakery, ready meals, and chilled foods, where clean label compliance is now a prerequisite for premium shelf placement.

At the same time, artisanal and zero-additive positioning is influencing mainstream brand strategies. In March 2025, Olli Salumeria launched a preservative-free salami line using traditional curing and process controls to eliminate chemical additives entirely. While such approaches are not scalable across all categories, they reinforce a broader consumer mindset. By 2025, roughly 42% of global consumers defined clean label explicitly by the presence of natural ingredients, pushing multinational brands such as Heinz and General Mills to prioritize familiar, kitchen-cupboard preservation solutions without compromising food safety or shelf life.

Strategic Scaling of Multifunctional Blends and Hurdle Technology

As manufacturers move away from single-molecule preservatives, the market is shifting toward multifunctional blends designed around hurdle technology. These systems combine organic acids, fermentation metabolites, and plant extracts to reduce the minimum inhibitory concentration required for microbial control, closing the efficacy gap historically associated with natural preservatives. The commercial logic is clear: better performance at lower dosages, minimal sensory impact, and a cleaner label declaration.

Investment patterns reflect this evolution. In May 2025, Galactic commissioned a €5 million spray-drying facility in China to scale production of its Galimax preservative powders. These blends are engineered for meat, poultry, and ready-meal applications, delivering improved solubility, flavor neutrality, and combined antimicrobial functionality. For processors, this translates into shorter ingredient lists and reduced formulation complexity without sacrificing shelf stability.

Digital tools are further accelerating adoption. Kerry Group has deployed AI-driven predictive modeling platforms that simulate the combined effects of pH, water activity, and natural antimicrobials in real time. Internal data indicates that extending shelf life by approximately 20% through optimized hurdle systems can materially reduce food waste. This aligns closely with consumer behavior trends, as over 90% of shoppers now report actively seeking ways to minimize household food waste, reinforcing the commercial value of advanced preservation design.

High-Value Preservation Systems for Plant-Based Meat and Dairy Alternatives

Plant-based meat and dairy alternatives represent one of the most technically demanding and fastest-growing opportunities within the preservatives market. Unlike animal proteins, plant-based matrices lack inherent antimicrobial hurdles and often exhibit unique spoilage pathways driven by soy- and pea-derived substrates. As category volumes scale, shelf-life instability has emerged as a critical bottleneck for manufacturers and retailers alike.

Research published in September 2025 by the Center for Food Safety at the University of Georgia highlighted that plant proteins follow distinct microbial trajectories post-thaw, increasing susceptibility to pathogens such as Listeria. This has created strong demand for precision preservation systems tailored specifically to plant-based formulations. In response, Kerry Group, leveraging capabilities from its Niacet acquisition, has accelerated development of organic acid and vinegar-based solutions engineered to target plant-specific spoilage organisms while maintaining vegan and clean label credentials.

Parallel growth is occurring upstream in fermentation chemicals. With the global fermentation market exceeding $111 billion in 2024, producers are increasingly focused on high-purity organic acids such as citric and lactic acid for plant-based applications. Precision fermentation enables consistent antimicrobial performance while supporting natural and vegan labeling, allowing plant-based products to achieve shelf lives comparable to conventional meat without resorting to synthetic preservatives.

Green Chemistry Expansion in Cosmetics and Personal Care Preservation

Beyond food, cosmetics and personal care are emerging as structurally attractive growth segments for advanced preservatives. Regulatory pressure in the EU and China, combined with consumer aversion to parabens and formaldehyde donors, is driving rapid adoption of eco-certified, skin-compatible preservation systems that perform across a wide pH range.

Innovation is centered on multifunctional blends. In October 2025, LANXESS launched Neolone PH Max, combining phenoxyethanol with sunflower-oil-derived pelargonic acid. This formulation enhances antimicrobial efficacy while staying within EU SCCS concentration limits and delivering antioxidant benefits, making it a practical drop-in solution for sustainable skincare and haircare products.

Sustainability credentials are becoming equally decisive. LANXESS also expanded its Purox S Scopeblue portfolio during 2024 and 2025, offering nature-identical sodium benzoate produced using renewable raw materials. With ISCC PLUS certification and an estimated 50% lower carbon footprint versus conventional benzoates, these solutions directly support Ecocert and COSMOS compliance. For premium cosmetic brands, such attributes are increasingly mandatory rather than optional, positioning green chemistry preservatives as a core enabler of future product launches.

Preservatives Market Share and Segmentation Insights

Synthetic Preservatives Lead Global Preservation Systems in Food, Cosmetics, and Pharmaceutical Products

Synthetic preservatives accounted for 52.80% of the Preservatives Market by type in 2025, supported by their proven antimicrobial efficacy, formulation stability, and cost efficiency across high-volume consumer product industries. Compounds such as parabens, benzoates, sorbates, propionates, and phenoxyethanol are widely used to inhibit microbial growth and extend product shelf life in processed foods, beverages, personal care products, and pharmaceutical formulations. Their established regulatory approvals and extensive safety data support continued use in large-scale commercial production. In 2025, clean label pressure is influencing preservative formulation strategies, prompting manufacturers to explore natural preservation systems while maintaining synthetic preservatives in applications where natural alternatives cannot provide equivalent stability, performance, or economic viability.

Food and Beverage Industry Drives Preservative Demand Across Global Processed Food Supply Chains

Food and beverage applications represented 52.80% of the Preservatives Market by end-use industry in 2025, reflecting the extensive need for microbial stability and shelf life management in packaged foods and beverages distributed through complex global supply chains. Preservatives are essential for preventing spoilage, maintaining product quality, and ensuring food safety across categories including baked goods, dairy products, beverages, sauces, and ready-to-eat foods. The scale of global food manufacturing continues to drive substantial demand for antimicrobial and antioxidant preservation systems. In 2025, clean label food preservation technologies are gaining industry focus, with manufacturers adopting fermentation-derived preservatives, cultured sugar systems, vinegar extracts, and botanical antioxidants to reduce synthetic additive usage while maintaining food safety and shelf stability.

Preservatives Market Competitive Landscape

The global preservatives market in 2026 is defined by clean-label antimicrobials, fermentation-derived preservatives, and portfolio optimization toward bioscience-driven solutions. Leading players are divesting commodity businesses while investing in natural preservation technologies, predictive modeling, and circular bio-based ingredients to meet evolving food safety, personal care, and regulatory demands.

BASF Strengthens High-Purity Preservatives Through Verbund Integration and Strategic Divestments

BASF is reinforcing its position in the preservatives market through its “Winning Ways” strategy, focusing on high-value nutrition and care segments. The company reported €6.6 billion EBITDA in 2025 and expects earnings growth in 2026 supported by the Zhanjiang Verbund site expansion. Its €1.7 billion cost-reduction program and divestiture of the decorative paints business enable reinvestment into high-purity industrial preservatives. BASF’s integrated Verbund production model ensures supply chain efficiency and low-carbon intermediates for home and personal care applications. The company targets CO2 emissions of 17.2–18.2 million metric tons in 2026, aligning with sustainability goals. Strong shareholder returns of €12 billion planned between 2025–2028 reflect confidence in its preservative portfolio resilience.

Kerry Drives Clean-Label Antimicrobial Leadership Through Niacet Acquisition and Predictive Food Safety Models

Kerry is positioning itself as a leader in food preservation technology through its $1 billion Niacet acquisition and advanced bioscience capabilities. The establishment of a BSL-2 laboratory enables high-precision testing against pathogens like Listeria and Salmonella, strengthening food safety solutions. Its predictive modeling tools optimize preservative dosage, reducing chemical load while maintaining efficacy. Kerry’s integration of IsoAge Technologies and Biosecur Lab expands its natural preservative portfolio, focusing on citrus extracts and bioflavonoids. The company is leading food waste reduction initiatives using fermentation-based antimicrobials in emerging markets. This strategy aligns with growing demand for clean-label, sustainable preservation systems.

Corbion Advances Fermentation-Based Preservation with Strong EBITDA Growth and Algae Innovation

Corbion is emerging as a pure-play leader in natural preservatives, transitioning fully toward fermentation-based solutions under its BRIGHT 2030 strategy. The company reported 26.7% organic EBITDA growth in 2025, supported by its focus on lactic acid and vinegar-based preservatives. Its strategic exit from emulsifiers and review of PLA operations reflect a commitment to high-margin bio-based ingredients. Corbion is expanding algae-derived stabilizers into human nutrition and pet food markets, enhancing functionality and sustainability. With targeted annual growth of 3%–6% and an EBITDA margin goal of ~18% by 2028, the company is strengthening its leadership in clean-label preservation. Its innovation pipeline is centered on bio-circular and fermentation-driven technologies.

IFF Refocuses on High-Margin Bioscience Preservatives Through Portfolio Reset and Debt Reduction

IFF is executing a major portfolio transformation, divesting lower-margin food ingredient businesses to prioritize its Health & Biosciences division. This segment delivered 26% margins and 20% operating profit growth in Q4 2025, driven by strong demand for enzymes and microbial preservation systems. The company is advancing the sale of its Food Ingredients and soy-based businesses, sharpening its focus on high-value bioscience applications. With $2.9 billion in debt reduction, IFF has improved its leverage ratio to 2.6x, enabling reinvestment into innovation. Its 2026 sales guidance of $10.5–$10.8 billion reflects steady growth supported by preservation and flavor integration trends. IFF’s strategy emphasizes advanced cultures and clean-label preservation technologies.

LANXESS Stabilizes Preservatives Segment with Cost Optimization and Focus on Consumer Protection

LANXESS is strengthening its preservatives business through its resilient Consumer Protection segment, which delivered improved EBITDA margins of 15.4% in 2025 despite declining group revenues. The company’s “FORWARD!” program achieved €150 million in savings, with additional €100 million targeted by 2028 to enhance operational efficiency. The divestiture of its Urethane Systems business reduced financial liabilities by 15%, enabling a sharper focus on antimicrobials and material protection solutions. LANXESS is maintaining stability in its preservatives portfolio amid geopolitical volatility and fluctuating demand. The company expects a recovery in H2 2026, with EBITDA projected between €450–€550 million. Its focus remains on industrial preservatives and regulatory-compliant antimicrobial systems.

ADM Expands Fermentation-Driven Preservation with Cost Efficiency and Nutrition Integration

ADM is advancing its preservatives portfolio through its Nutrition & Care segment, focusing on fermentation-based and clean-label solutions. The company’s 2026 EPS guidance of $3.60–$4.25 reflects stable growth supported by its nutrition-driven strategy. ADM’s Global Culinary Trends highlight fermentation and pickling as key drivers of natural preservation demand. Its cost-efficiency program aims to deliver $500–$750 million in savings, improving manufacturing and operational performance. The launch of Nutripiscis Oxygen demonstrates its ability to integrate preservation technologies into aquafeed and animal health. ADM’s vertically integrated supply chain ensures consistent quality and scalability for global food preservation solutions.

United States: Labeling Reform and Digitized Compliance Reshape Preservative Portfolios

The United States preservatives market is undergoing a structural reconfiguration driven by nutrition labeling reform, ingredient bans, and digitally enabled food safety compliance. The FDA’s finalized “Healthy” claim criteria in January 2025 materially altered formulation economics by penalizing sodium-heavy preservation systems. As a result, manufacturers accelerated substitution toward low-sodium and potassium-based preservatives, most notably potassium sorbate, across beverages, bakery, and ready meals to retain front-of-pack eligibility. Reformulation pressure intensified with the January 15, 2025 revocation of FD&C Red No. 3 in ingestible products, prompting widespread pairing of natural colorants with tocopherol-based antioxidants to preserve oxidative stability and shelf life without synthetic dyes.

Industrial and technology-driven preservation is expanding in parallel. In March 2025, BASF committed new capital to expand aminic antioxidant capacity across its North American network, targeting lubricant and industrial preservative demand with completion slated for 2026. The USDA supported multiple 2025 grants for precision fermentation platforms, including startups such as EdiMembre, developing edible, preservative-infused membranes that extend protein shelf life without conventional additives. Compliance timelines are catalyzing digitalization. As the January 2026 deadline for FSMA Section 204 approaches, manufacturers are embedding smart sensors to monitor preservative efficacy in real time across the cold chain, integrating safety, traceability, and shelf-life optimization into a single compliance framework.

European Union: Concentration Limits, Circularity, and Digital Product Passports

The European Union preservatives landscape is increasingly defined by restrictive concentration limits, circular economy integration, and mandatory digital disclosure. Regulation (EU) 2025/1090 under REACH Annex XVII introduced new restrictions on specific solvents and preservatives in consumer articles, imposing 0.3% concentration caps effective December 23, 2026. These thresholds are accelerating the replacement of legacy chemistries with lower-toxicity alternatives across coatings, personal care, and household products. Concurrently, European producers are scaling low-VOC dispersion lines. In October 2025, multiple chemical leaders inaugurated production for EU Ecolabel-compliant systems that rely on advanced preservative packages optimized for indoor air quality.

Circularity requirements are tightening preservative selection for plastics. Commission Regulation (EU) 2025/351 established new rules for preservatives used in recycled plastics intended for food contact, mandating non-migration beyond 10 ppb. This has increased demand for stabilizers compatible with degraded polymer matrices. In August 2025, BASF expanded its VALERAS® sustainability platform to include preservatives and additives engineered for recycled polymers. Transparency is becoming non-negotiable. By early 2026, Digital Product Passport requirements are pushing preservative manufacturers to provide batch-level life cycle assessment data, reshaping procurement toward suppliers with auditable environmental and safety credentials.

India: Domestic KSM Localization and Botanical Preservation for Exports

India’s preservatives industry is transitioning from import dependence to domestic depth, supported by policy incentives and export-driven formulation shifts. In December 2025, the Department of Pharmaceuticals extended application windows for the Production Linked Incentive scheme, explicitly targeting domestic manufacturing of key starting materials for preservatives and drug stabilizers. This follows progress under Atmanirbhar Bharat initiatives, which by September 2025 localized production of 26 critical chemical intermediates previously fully imported, including paraben-free preservation systems for food and personal care.

Export compliance is driving botanical preservation. The Food Safety and Standards Authority of India launched the Zero-Residual program in 2025, encouraging spice, seafood, and ready-to-eat exporters to adopt botanical extracts such as rosemary and neem-derived acids. This shift aligns Indian exports with residue-sensitive markets while preserving antimicrobial efficacy. Industrial scale remains robust. The Gujarat PCPIR recorded ₹1.76 lakh crore in realized investments by March 2025, with a significant share allocated to high-purity food-grade sulfites and preservatives, reinforcing India’s role as a compliant, cost-competitive supply base.

China: Equipment Renewal, Standard Proliferation, and AI-Led Scale

China’s preservatives sector is moving decisively toward high-end manufacturing standards and technology-enabled scale. In September 2025, the Ministry of Industry and Information Technology rolled out a 2025–2026 action plan emphasizing equipment renewal across preservative synthesis, targeting consistency, purity, and energy efficiency aligned with global benchmarks. Standardization is accelerating. An April 2025 roadmap outlined the development of 1,800 industry standards, including new technical bodies dedicated to bio-preservatives and nanotechnology-based antimicrobials, signaling long-term regulatory depth for emerging chemistries.

As Made in China 2025 reaches its milestone, leading firms are embedding AI at scale. Companies such as Shandong Minde transitioned to AI-driven saponification processes in 2025 for potassium-based preservatives, improving yield control and batch uniformity. These advances are supporting China’s dual objective of domestic supply stability and competitive exports in food, feed, and industrial preservation, with technology differentiation increasingly central to market positioning.

Türkiye: Regional Capacity Build-Out and Low-Carbon Production

Türkiye is strengthening its role as a regional preservatives hub serving the Middle East and Northwest Africa through capacity expansion and low-carbon operations. In late 2025, BASF commissioned a major new preservatives and dispersions line in Dilovası, significantly increasing regional availability and shortening supply chains for neighboring markets. This investment enhances resilience for customers facing longer lead times from Western Europe.

Sustainability credentials are emerging as a competitive advantage. As of October 2025, the Dilovası site operates entirely on green electricity under a mass balance approach, setting a benchmark for low-emissions chemical production in the region. This positioning supports customers seeking to reduce Scope 3 emissions while maintaining access to industrial-scale preservative supply.

Comparative Overview of Country-Level Dynamics in the Preservatives Industry

Preservatives Market County Level Snapshot

|

Region

|

Primary 2025–2026 Drivers

|

Structural Impact on Preservatives

|

|

United States

|

Healthy labeling, dye bans, FSMA digitization

|

Shift to low-sodium systems and smart preservation

|

|

European Union

|

REACH limits, circular plastics, DPP

|

Safer chemistries with auditable life cycle data

|

|

India

|

PLI incentives, export residue controls

|

Localized KSMs and botanical preservation growth

|

|

China

|

Equipment renewal, standard expansion, AI

|

High-end, technology-led scale and consistency

|

|

Türkiye

|

Regional capacity, green electricity

|

Resilient supply with low-carbon production

|

Preservatives Market Report Scope

Preservatives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Synthetic Preservatives, Natural & Bio-Derived Preservatives, Inorganic Preservatives), By Function (Antimicrobials, Antioxidants, Chelating Agents, Enzyme Inhibitors), By Form (Liquid Solutions, Solid & Granular, Encapsulated Systems), By End-Use Industry (Food & Beverage, Pharmaceuticals, Cosmetics & Personal Care, Industrial & Coatings, Feed & Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Lanxess AG, Archer Daniels Midland Company, Kerry Group, Corbion NV, Nouryon, Eastman Chemical Company, International Flavors & Fragrances Inc., Jungbunzlauer Suisse AG, Kemin Industries Inc., DuPont de Nemours Inc., Cargill Incorporated, Celanese Corporation, Galactic SA, Aditya Birla Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Preservatives Market Segmentation

By Type

- Synthetic Preservatives

- Natural & Bio-Derived Preservatives

- Inorganic Preservatives

By Function

By Form

- Liquid Solutions

- Solid & Granular

- Encapsulated Systems

By End-Use Industry

- Food & Beverage

- Pharmaceuticals

- Cosmetics & Personal Care

- Industrial & Coatings

- Feed & Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Preservatives Industry

- BASF SE

- Lanxess AG

- Archer Daniels Midland Company

- Kerry Group

- Corbion NV

- Nouryon

- Eastman Chemical Company

- International Flavors & Fragrances Inc.

- Jungbunzlauer Suisse AG

- Kemin Industries Inc.

- DuPont de Nemours Inc.

- Cargill Incorporated

- Celanese Corporation

- Galactic SA

- Aditya Birla Chemicals

*- List not Exhaustive