Water Clarifiers Market Overview

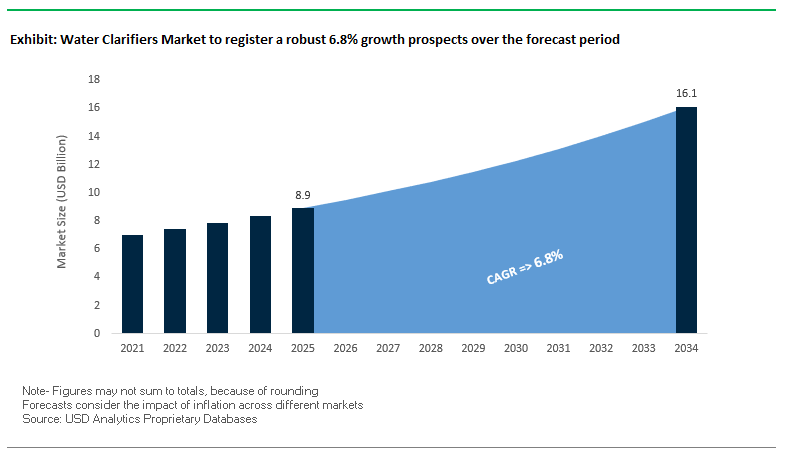

The global water clarifiers market is projected to grow from $8.9 billion in 2025 to $16.1 billion by 2034, at a CAGR of 6.8%. Water clarifiers are essential components in municipal and industrial water treatment systems, playing a critical role in the removal of suspended solids and other impurities. They ensure compliance with public health standards and environmental discharge regulations and are increasingly pivotal for industries that require high-quality process water.

Industrial sectors such as food and beverage, pulp and paper, and petrochemicals depend on clarifiers to protect equipment, maintain process efficiency, and ensure product quality. Meanwhile, rising global water stress has highlighted the need for treated water for reuse and surface water processing, further boosting the market. Regulatory frameworks, such as India’s Water Purification System Rules 2023, are accelerating adoption of advanced clarification technologies across emerging markets.

Key Insights for Industry Stakeholders:

- Municipal and Industrial Necessity: Foundational in both drinking water and wastewater treatment for suspended solids removal.

- Industrial Process Optimization: Ensures process water quality and safeguards equipment in manufacturing industries.

- Water Scarcity Mitigation: Critical for making treated wastewater safe for reuse and surface water processing.

- Regulatory Compliance: Growing regulations worldwide are driving demand for effective clarification solutions.

- Integration with Advanced Systems: Increasing adoption of digital and automated water treatment enhances clarifier performance and monitoring.

Market Analysis: Recent Developments in Water Clarifiers

The water clarifiers market has seen significant strategic and technological advancements between 2024 and 2025. In August 2025, a water treatment plant improvement project in Columbia, Missouri, involved rehabilitation and replacement of clarifiers to enhance treatment capacity to 32 million gallons per day. In the same month, Grundfos acquired Newterra, expanding its modular and scalable water treatment solutions that rely on robust clarification systems.

July 2025 marked the opening of one of the largest PFAS treatment plants in Delaware, U.S., by Veolia, highlighting the continued reliance on primary clarification in advanced water treatment processes. Kemira announced a €20 million investment in July 2025 to expand Aluminum Chloro Hydrate (ACH) production in Tarragona, Spain, reflecting the growing demand for high-performance coagulants essential for clarification. Similarly, AECOM and Aquatech in June 2025 fast-tracked the deployment of DE-FLUORO™ PFAS destruction technology, emphasizing the critical role of pre-treatment and clarification in handling complex water contaminants.

Further strategic moves include AqueoUS Vets’ FoamPro system in May 2025, utilizing robust pre-treatment including clarification, and the Kurita America–Avista Technologies merger in April 2025, enhancing industrial and municipal water treatment capabilities. In December 2024, Xylem Inc. acquired Idrica, strengthening its digital portfolio for optimized clarifier performance, demonstrating the growing trend of integrating AI and data analytics into water treatment operations.

Key Trends Shaping the Water Clarifiers Market

Push for Next-Generation, Eco-Friendly Coagulants

The water clarifiers market is seeing a major shift toward eco-friendly and bio-based coagulants. Academic studies highlight the use of natural coagulants derived from plant-based materials as effective alternatives to traditional inorganic salts like aluminum sulfate or ferric chloride. These bio-coagulants not only enhance the removal of heavy metals and suspended solids but also significantly reduce sludge generation, lowering disposal costs and environmental impact. Additionally, the development of more stable and efficient polymer coagulants improves floc formation even under fluctuating pH conditions, resulting in denser, more easily settleable flocs and reducing the need for secondary treatments.

Integration of IoT and Digital Monitoring for Real-Time Optimization

IoT and digital monitoring systems are increasingly being integrated into clarifier tanks to continuously track water turbidity, suspended solids, and pH levels. Real-time data allows operators to adjust chemical dosing and flow rates instantly, optimizing clarification efficiency and ensuring compliance with stringent discharge regulations. Industry announcements have highlighted new platforms enabling remote clarifier operation and predictive maintenance, which reduce operational costs and prevent unplanned downtime. The use of smart sensors and predictive analytics is particularly transformative in large municipal and industrial operations, providing high-value operational insights.

Government and Public-Private Partnerships Driving Water Security

Government initiatives and public-private partnerships (PPPs) are accelerating the adoption of high-performance clarifiers. For example, India’s “Jal Sanchay Jan Bhagidari” initiative promotes rainwater harvesting and efficient water management, creating demand for robust clarification systems. Similarly, hybrid annuity-based PPP projects in Indian cities leverage private sector expertise to build modern wastewater treatment infrastructure, with performance-based operations monitored using advanced systems. Such programs highlight the role of clarifiers in ensuring water security, compliance, and sustainability across public and private sectors.

Emerging Opportunities in the Water Clarifiers Market

The water clarifiers market presents opportunities for companies offering next-generation coagulants, compact and high-efficiency clarifier designs, and IoT-enabled monitoring solutions. Industrial and municipal sectors alike are seeking solutions that reduce operational costs, optimize chemical usage, and meet regulatory discharge standards. Compact designs such as lamella clarifiers, along with solids contact systems, provide space-saving and high-performance solutions for industries with variable flows or constrained footprints. Companies that combine eco-friendly coagulants with smart clarifier technologies are well-positioned to capture growth in both traditional municipal projects and high-value industrial water treatment applications.

Market Share Analysis of Water Clarifiers Market

Market Share by Clarifier Type: Circular Clarifiers Lead, Lamella Growing Rapidly

Circular clarifiers (44.1%) dominate the market due to their robust design, ease of operation, and efficient sludge collection, making them the preferred choice for large-scale municipal plants. Solids contact clarifiers (26.9%) combine mixing, flocculation, and sedimentation in one unit, enhancing efficiency in industrial applications with highly variable flow and load. Inclined plate (lamella) clarifiers (22.5%) are experiencing rapid adoption in space-constrained industrial plants due to their compact footprint and high effective settling area. Rectangular clarifiers (11.8%) remain stable in large municipal projects where modular layouts reduce construction costs. The trend indicates a shift toward compact, efficient designs while maintaining a base for conventional circular units.

Market Share by Application & End-User: Municipal Dominates, Industrial Shows High Growth

Municipal water treatment (58%) represents the largest application and end-user segment, driven by the continuous demand for potable water and municipal wastewater treatment, stringent regulations, and aging infrastructure upgrades. Industrial water treatment (44.1%) is a high-growth segment, encompassing power generation, chemicals, oil & gas, food & beverage, pulp & paper, and mining industries. Industrial adoption is motivated by regulatory compliance, water reuse initiatives, and the need for high-quality process water to protect downstream equipment. Municipal projects prioritize longevity, reliability, and operational simplicity, while industrial projects focus on flexible operation, footprint efficiency, and cost-effectiveness. This dual dynamic illustrates how clarifiers serve both large-scale municipal infrastructure and specialized industrial applications, offering diverse opportunities for manufacturers.

Competitive Landscape of Water Clarifiers Market

The water clarifiers market is dominated by leading global players focusing on technological innovation, sustainable solutions, and integrated water treatment services. Companies differentiate through proprietary chemicals, advanced equipment, digital monitoring, and strategic acquisitions to enhance municipal and industrial water treatment capabilities.

Ecolab Inc. delivers science-based clarifier solutions for industrial efficiency

Ecolab, through its Nalco Water division, combines chemical expertise with digital monitoring to provide high-performance coagulants and flocculants for industrial water clarification. The company integrates on-site service and smart monitoring systems, optimizing water and energy use, enhancing operational efficiency, and supporting sustainability objectives.

SUEZ S.A. leads with integrated water clarification and digital solutions

SUEZ provides advanced clarification technologies, including decanting and settling systems, integrated with its AQUADVANCED® digital suite for plant optimization. Strategic projects in desalination and wastewater treatment worldwide highlight its commitment to large-scale infrastructure and digital water management, ensuring resilient operations under changing climate conditions.

Kurita Water Industries Ltd. innovates industrial water clarification

Kurita offers a range of high-performance coagulants and flocculants, alongside membrane treatment solutions, to enhance water clarification efficiency. The April 2025 merger with Avista Technologies strengthens its capabilities in pre-clarification and industrial process support, allowing the company to provide comprehensive, sustainable water treatment solutions.

Kemira Oyj expands coagulant production to meet rising demand

Kemira specializes in sustainable water treatment chemicals, including coagulants and polymers essential for effective clarification and sludge management. Its €20 million investment in Tarragona, Spain, in July 2025 reflects the growing market need for high-performance water treatment chemicals in municipal and industrial applications.

Veolia Water Technologies integrates advanced clarifiers with emerging contaminant solutions

Veolia provides high-rate clarifiers and lamella settlers as part of integrated treatment systems. The June 2025 partnership with AECOM for PFAS destruction demonstrates its expertise in handling complex contaminants using robust pre-treatment solutions. Veolia leverages its Hubgrade platform to optimize system performance through AI and analytics, offering innovative and sustainable water treatment solutions.

BASF SE focuses on chemical innovation for water clarification

BASF delivers a comprehensive portfolio of coagulants and flocculants, including Magnafloc® and Hydrosmart® brands, enhancing sedimentation and separation processes. Its PuriCycle™ portfolio, introduced in 2024, reflects the company’s commitment to sustainable water treatment solutions, integrating circular economy principles while maintaining high-performance industrial and municipal clarifiers.

U.S. EPA Regulations and Infrastructure Investments Driving Water Clarifiers Market Growth

The United States water clarifiers market is experiencing robust growth as regulatory compliance and infrastructure funding converge to accelerate adoption. The U.S. Environmental Protection Agency (EPA) has tightened drinking water standards, including enforceable limits for six PFAS compounds, which necessitate advanced clarification processes across municipal and industrial facilities. This regulatory environment has significantly increased the need for high-performance clarifiers in water treatment plants. Federal investments under the Bipartisan Infrastructure Law (BIL), including more than $2 billion earmarked for emerging contaminants like PFAS, are modernizing aging infrastructure and supporting widespread adoption of clarifiers nationwide. Corporate innovation is also reshaping the market landscape Hawkins’ April 2025 acquisition of WaterSurplus strengthens its environmental remediation portfolio, while Aquatech International’s recognition as Water Technology Company of the Year underscores the U.S. leadership in industrial water purification. Key applications span from municipal water utilities to wastewater management in industries such as oil & gas, food & beverage, and chemicals, making the U.S. a central hub for clarifier adoption.

China’s “Water Ten Plan” and Multi-Billion Investments Powering Clarifiers Demand

China is emerging as one of the most dynamic markets for water clarifiers, propelled by government initiatives and unprecedented infrastructure spending. The "Water Ten Plan" and "War on Pollution" have expanded the national monitoring network from 972 sections in 2015 to 3,646 during the 14th Five-Year Plan, driving transparent reporting and stricter compliance with water quality standards. This push toward environmental accountability has created vast opportunities for clarifier deployment. Between 2017 and 2022, the Ministry of Finance reported RMB673.31 billion in water pollution control investments, while urban drainage pipeline density reached 12.67 km/km² and wastewater treatment rates soared to 98.69% by 2023. These figures highlight the enormous scale of China’s infrastructure transformation. Clarifiers are in high demand to address urban water contamination, agricultural runoff, and industrial effluents, particularly from the refining and petrochemical sectors. With rapid urbanization fueling water scarcity and pollution concerns, clarifier systems are becoming a cornerstone of China’s water security strategy.

India’s Jal Jeevan Mission and Industrial Growth Creating High Demand for Clarifiers

India’s water clarifiers market is rapidly expanding due to government programs and large-scale infrastructure investments. The flagship Jal Jeevan Mission aims to provide safe drinking water to all rural households, necessitating the construction of hundreds of new treatment plants equipped with clarifiers. Parallelly, the National Mission for Clean Ganga sanctioned 39 new projects worth ₹2,056 crore in 2024, specifically targeting sewage treatment and river clean-up. Data from Q4 FY 2024–25 further reveals 442 water infrastructure projects with an estimated cost of ₹44,777 crore, including 283 for water supply systems and 53 for Sewerage Treatment Plants (STPs), both heavy users of clarifier systems. Foreign partnerships are also shaping the market Veolia’s September 2023 joint venture with an Indian water treatment company strengthens local clarifier manufacturing and distribution. Rising industrial demand from sectors such as food & beverage and pharmaceuticals, coupled with the government’s river rejuvenation and urban sanitation push, cements India’s position as a fast-growing clarifiers market in Asia.

Germany’s EU Directives and Technological Innovation Strengthening Clarifiers Adoption

Germany is at the forefront of Europe’s water clarifiers market, driven by strict EU regulations and pioneering technological advancements. The revised EU Urban Wastewater Treatment Directive, effective from January 2025, requires stricter monitoring and removal of pollutants, compelling municipalities and industries to adopt advanced clarifier systems. German research institutions and companies are spearheading solutions for eliminating micro-pollutants such as pharmaceuticals and PFAS, reinforcing the role of clarifiers in meeting emerging environmental standards. The market is heavily influenced by strong public demand for clean water and sustainability, ensuring that clarifiers remain integral to wastewater treatment upgrades across both industrial and municipal applications. By blending regulatory compliance with technological leadership, Germany continues to serve as a model for innovation-driven water treatment strategies in Europe.

UK’s AMP 8 Regulations and Digital Integration Accelerating Clarifiers Market Growth

The United Kingdom water clarifiers market is being transformed by regulatory requirements and the adoption of digital technologies. Under the Asset Management Period (AMP) 8, water utilities are mandated to upgrade infrastructure to mitigate environmental risks and safeguard water quality, significantly driving the uptake of advanced clarifiers. Complementing this regulatory framework, Siemens introduced Water Quality Analytics as a Service (WQAaaS) in 2024, providing real-time monitoring and performance optimization for clarifiers. This integration of digital analytics with traditional treatment technologies enhances efficiency and reliability. Market demand is further propelled by the urgent need to replace aging infrastructure and improve resilience across municipal utilities. With sustainability and modernization at the core of the UK’s water management strategy, clarifiers are positioned as a critical technology in ensuring future-ready water systems.

Japan’s Industrial Water Treatment Focus and Corporate Leadership in Clarifiers

Japan’s water clarifiers market is being shaped by industrial requirements and strong corporate participation. The country faces mounting challenges from aging infrastructure and water scarcity, which are driving investments in advanced treatment technologies. Japanese firms, particularly Kurita Water Industries, play a leading role in developing innovative clarifier systems that address both municipal and industrial water treatment needs. With rising emphasis on water reuse and recycling, clarifiers are becoming central to Japan’s sustainability agenda. The combination of stringent industrial standards, corporate innovation, and a national focus on environmental resilience positions Japan as a key innovator in the global clarifiers market.

Summary of Country-Level Water Clarifiers Market Dynamics

Water Clarifiers Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Clarifier Technology Focus

|

Strategic Market Role

|

|

United States

|

PFAS regulation and funding timing

|

Advanced primary clarifiers with IoT

|

Compliance-led, service-oriented market

|

|

China

|

Water conservation and petrochemical growth

|

High-efficiency central-drive clarifiers

|

Industrial reuse scale driver

|

|

Saudi Arabia

|

100% reuse mandate

|

GRP clarifiers and AI-packaged STPs

|

Arid-region circularity leader

|

|

India

|

Rural water access and ZLD enforcement

|

Lamella settlers and high-purity units

|

Broad-based growth across segments

|

Water Clarifiers Market Report Scope

Water Clarifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.9 Billion

|

|

Market Size (2034)

|

$16.1 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Design Type (Circular Clarifiers, Rectangular Clarifiers, Lamella Clarifiers, Solids-Contact Clarifiers), By Material (Carbon Steel, Stainless Steel, Fiber-Reinforced Plastic, Concrete), By Product Type (Flocculants, Inorganic Coagulants, Organic Coagulants, pH Stabilizers and Specialty Additives), By Application (Municipal Wastewater Treatment, Industrial Wastewater Treatment, Potable Water Treatment, Power Generation Cooling Systems)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Evoqua Water Technologies (A Xylem Brand), SUEZ, Ecolab Inc., Kurita Water Industries Ltd., Xylem Inc., DuPont de Nemours, Inc., SNF Floerger, Kemira Oyj, The Dow Chemical Company, BASF SE, Hach (A Danaher Company), Aquatech International, WesTech Engineering, Inc., Thermax Limited, Others

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Clarifiers Market Segmentation

By Type

- Circular Clarifiers

- Rectangular Clarifiers

- Solids Contact Clarifiers

- Inclined Plate (Lamella) Clarifiers

By Application

- Municipal Water Treatment

- Industrial Water Treatment

- Chemical & Petrochemical

- Mining & Metallurgy

- Food & Beverage

- Pulp & Paper

- Textiles

- Power Generation

- Pharmaceutical

By End-User

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Clarifiers Industry include-

- Veolia

- Evoqua Water Technologies (A Xylem Brand)

- SUEZ

- Ecolab Inc.

- Kurita Water Industries Ltd.

- Xylem Inc.

- DuPont de Nemours, Inc.

- SNF Floerger

- Kemira Oyj

- The Dow Chemical Company

- BASF SE

- Hach (A Danaher Company)

- Aquatech International

- WesTech Engineering, Inc.

- Thermax Limited

*- List not Exhaustive

Research Coverage

The Water Clarifiers Market study from USDAnalytics delivers a decision-ready view of demand drivers, technology shifts, and purchasing patterns across municipal and industrial treatment trains. Building on operator interviews and plant audits, this report investigates how clarifier type, chemistry programs, and digital controls reshape lifecycle cost and compliance outcomes; it catalogs breakthroughs in lamella/high-rate designs, polymer/coagulant innovation, and AI-enabled monitoring; our competitive analysis reviews capacity additions, M&A, and specification wins; and it highlights how evolving effluent limits, water-reuse targets, and PFAS pre-treatment needs are influencing capex and opex choices. With clear sizing, growth trajectories through 2034, and field-tested best practices, this report is an essential resource for utility leaders, EPCs, plant managers, and suppliers aligning clarification strategy with resilience, sustainability, and budget discipline. Scope Includes-

- Segmentation: By type (circular, rectangular, solids contact, inclined plate/lamella), application (municipal water, industrial water chemicals & petrochemicals, mining & metallurgy, food & beverage, pulp & paper, textiles, power, pharmaceutical), and end-user (municipal, industrial).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; Evoqua Water Technologies (a Xylem brand); SUEZ; Ecolab Inc.; Kurita Water Industries Ltd.; Xylem Inc.; DuPont de Nemours, Inc.; SNF Floerger; Kemira Oyj; The Dow Chemical Company; BASF SE; Hach (a Danaher company); Aquatech International; WesTech Engineering, Inc.; Thermax Limited

Methodology

USDAnalytics triangulates market size using a bottom-up plant census (installed clarifiers by type, diameter/plate area, duty, and chemical program) reconciled with a top-down spend model from public capex, utility tariffs, EPC awards, and supplier revenues. Primary research covers utility operators, industrial water managers, and OEMs to capture loading variability, sludge yields, polymer/ACH dose, energy draw, and maintenance cycles. Bench/PFR data and vendor FAT/SAT records inform removal-efficiency and surface-overflow-rate curves; these feed a Monte-Carlo forecast linking build-rates, reuse mandates, PFAS/pollutant rules, and coagulant pricing to unit demand and ASPs by region. All outputs pass multi-step QA (bill-of-materials checks, import/export harmonization, and variance analysis versus prior vintages) to ensure traceable, audit-ready numbers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.