OEM Coatings Market Size, Automotive OEM Finishes, and Industrial Coating Technologies Outlook

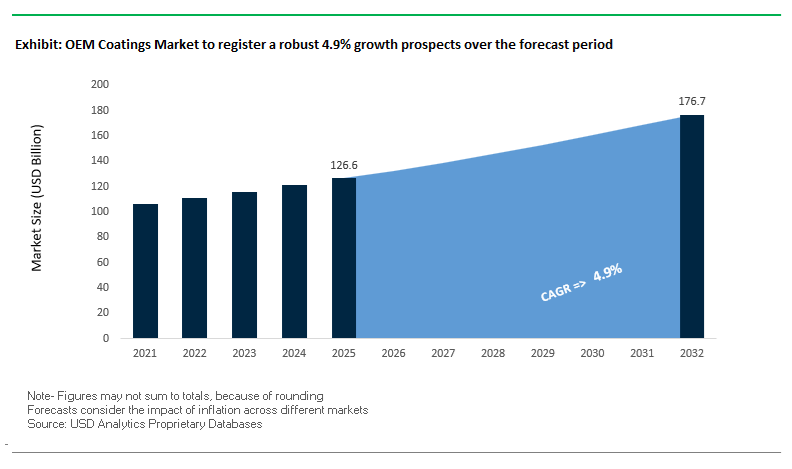

The global OEM coatings market was valued at $126.6 billion in 2025 and is projected to reach $177 billion by 2032, expanding at a CAGR of 4.9%. Growth is anchored in sustained demand for automotive OEM coatings, industrial OEM coatings, electrocoat (e-coat) systems, powder coatings, and high-performance liquid coatings across automotive manufacturing, heavy equipment, appliances, rail, and general industrial sectors. These coatings are integral to corrosion protection, surface aesthetics, durability, and regulatory compliance in high-throughput manufacturing environments.

A central demand driver is the evolution of automotive OEM coating technologies, particularly with the shift toward electric vehicles (EVs), lightweight materials, and multi-substrate manufacturing. OEM coatings are increasingly engineered for enhanced adhesion on aluminum and composites, improved scratch resistance, and reduced curing temperatures to align with energy efficiency mandates. Additionally, manufacturers are prioritizing process efficiency, cost optimization, and sustainability, leading to increased adoption of low-VOC coatings, waterborne systems, and energy-efficient curing technologies.

The market is also shaped by the integration of digital manufacturing, automation, and advanced application technologies, including wet-on-wet (WoW) processes, robotic coating systems, and smart quality monitoring tools. Aesthetic differentiation is becoming a competitive factor, with OEMs investing in advanced color technologies, special effect pigments, and premium finishes to enhance product appeal. Regionally, Asia-Pacific dominates due to large-scale automotive and industrial production, while Europe and North America lead in innovation, sustainability, and advanced coating technologies.

Market Analysis: Wet-on-Wet Efficiency Gains, and OEM Profitability Strategies Driving Market Evolution

The OEM coatings industry is undergoing structural transformation driven by major consolidation, process innovation, and strategic profitability optimization. The most significant development occurred in February 2026, when AkzoNobel and Axalta formally initiated a merger of equals, creating a dominant global entity combining AkzoNobel’s industrial coatings expertise with Axalta’s leadership in automotive OEM coatings. This merger is expected to reshape global supply chains, pricing strategies, and R&D priorities across the OEM coatings landscape.

Financial performance across leading players indicates a shift toward margin-focused growth strategies. AkzoNobel’s February 2026 results showed a 27% increase in operating profit despite flat volumes, driven by a “price-over-volume” approach and €980 million in cost reductions. Similarly, Axalta reported record 2025 earnings with a 22% Adjusted EBITDA margin, supported by favorable price-mix dynamics in its Mobility Coatings segment. Sherwin-Williams also reported 2025 net sales of $23.57 billion, with growth supported by the integration of its Suvinil acquisition, strengthening its OEM presence in emerging markets.

Technological innovation is significantly improving manufacturing efficiency. PPG Industries’ April 2025 expansion of wet-on-wet (WoW) coating technology allows multiple layers to be applied without intermediate curing, delivering up to 50% productivity gains and 20% energy savings in OEM production lines. Additionally, PPG’s focus on electrocoat and digital innovation, highlighted for the ECOAT 2026 Conference, underscores the importance of automation and process optimization in next-generation OEM facilities.

Product innovation and design trends are also shaping market dynamics. BASF Coatings’ October 2025 “DRIVING THE PROXY” color collection introduces advanced liquid-metal effects and multi-color pigments, reflecting the growing importance of aesthetic differentiation in automotive OEM coatings. These innovations are aligned with OEM requirements for durable, visually distinctive finishes that enhance brand identity.

Strategic regional and portfolio expansions continue to drive competitive positioning. Nippon Paint’s 2024–2026 strategy focuses on becoming a leading player in Southeast Asia by delivering localized OEM coating solutions, while Kansai Helios’ May 2024 acquisition of Weilburger Coatings expands its footprint in industrial, railway, and appliance OEM segments. Leadership changes, such as Kansai Nerolac’s February 2025 transition, reflect ongoing efforts to strengthen regional market strategies and industrial synergies, particularly in high-growth markets like India.

Market Trend: Ultra-Low VOC Waterborne Automotive Coatings Enabling Zero-Solvent Paint Shops and Energy-Efficient OEM Manufacturing

The OEM coatings industry is undergoing a structural shift as automotive manufacturers accelerate the adoption of ultra-low VOC waterborne coatings to meet tightening global air quality regulations and internal decarbonization targets. Modern automotive paint shops are increasingly designed around a zero-solvent philosophy, replacing conventional solvent-borne basecoats with advanced waterborne systems that deliver both environmental compliance and process efficiency.

Waterborne automotive coatings are achieving VOC levels as low as 20 to 50 g/L, representing a reduction of nearly 90% compared to legacy solvent-based systems, which typically range between 400 and 600 g/L. This dramatic decrease in emissions is enabling OEMs to comply with stringent regulatory frameworks across Europe, Asia-Pacific, and North America while improving workplace safety and reducing hazardous air pollutant exposure within manufacturing facilities.

Process innovation is further enhancing the value proposition of waterborne systems. The implementation of compact “3-wet” coating processes allows OEMs to apply primer, basecoat, and clearcoat layers sequentially without intermediate curing stages. This eliminates the need for primer surfacer flash-off ovens, reducing total energy consumption by approximately 15% to 25% and shrinking paint shop footprints by up to 30%. These efficiency gains are particularly critical in new vehicle assembly plants, where capital expenditure and operational optimization are closely linked.

Global adoption trends reflect this transition. As of 2026, more than 75% of newly commissioned vehicle assembly lines in Europe and the Asia-Pacific region specify waterborne basecoat technologies as the primary coating method. This widespread implementation underscores the role of ultra-low VOC coatings as a foundational technology in next-generation automotive manufacturing.

Market Trend: Single-Coat Powder Coatings Replacing Multi-Layer Liquid Systems in Industrial OEM Applications

General industrial OEM sectors, including agriculture, construction equipment, and electronics manufacturing, are rapidly transitioning toward single-coat powder coating systems as a replacement for traditional multi-layer liquid coating processes. This shift is driven by the need for improved durability, higher material efficiency, and lower carbon emissions in large-scale manufacturing operations.

Modern single-coat powder coatings are delivering corrosion protection performance that matches or exceeds traditional two-coat liquid systems. Advanced formulations consistently achieve 1,000 to 2,000 hours of Neutral Salt Spray resistance under ASTM B117 testing conditions, providing robust protection against environmental exposure while simplifying the coating process. This level of performance allows manufacturers to eliminate primer layers, reducing process complexity and cycle time.

Material utilization efficiency is a major advantage of powder coatings. These systems achieve utilization rates of 95% to 98% through effective overspray reclamation, significantly outperforming liquid spray processes, which typically lose 30% to 50% of material due to overspray and solvent evaporation. This efficiency translates directly into cost savings and reduced waste generation, supporting both economic and sustainability objectives.

Carbon footprint reduction is another critical driver. By eliminating solvent flash-off stages and reducing curing requirements, single-coat powder coating lines can lower total CO₂ emissions by approximately 40% compared to solvent-based liquid systems. As industrial OEMs align with global decarbonization targets, powder coatings are emerging as a key technology for achieving low-emission, high-efficiency manufacturing.

Market Opportunity: US DOE Industrial Decarbonization Funding Accelerating Adoption of Low-Temperature and Electrified Coating Technologies

The United States Department of Energy’s Industrial Decarbonization Program is creating a significant opportunity for OEM coatings manufacturers to modernize production infrastructure through federal funding and incentives. Coating processes, particularly curing operations, are among the most energy-intensive stages in manufacturing, making them a primary focus for emissions reduction initiatives.

Through the Industrial Demonstrations Program, more than $6.3 billion has been allocated to support first-of-a-kind technology deployments, including the electrification of coating processes. OEMs are increasingly leveraging this funding to transition from gas-fired curing ovens to electric infrared and ultraviolet curing systems, which offer substantial reductions in energy consumption and greenhouse gas emissions.

The DOE’s Industrial Heat Shot initiative further reinforces this opportunity by targeting an 85% reduction in emissions from industrial heating processes by 2035. This creates a clear pathway for OEMs to adopt low-temperature curing coatings and advanced application technologies that align with decarbonization goals. Suppliers offering coatings compatible with these emerging curing technologies are well positioned to benefit from increased demand as manufacturers invest in sustainable production systems.

Market Opportunity: China GB 30981.2-2025 Standard Driving Mandatory Transition to Low-VOC and Heavy-Metal-Free OEM Coatings

China’s implementation of GB 30981.2-2025 is reshaping the OEM coatings market by establishing strict limits on VOC emissions and hazardous substances in industrial coatings. Effective from early 2026, this regulation mandates compliance across all vehicle manufacturing operations, creating a large-scale transition toward environmentally compliant coating technologies.

The standard introduces stringent VOC thresholds, particularly for water-based primers, where “Green Product” classification requires VOC levels below 200 g/L. This effectively eliminates the use of water-reducible hybrid coatings that rely on significant solvent content, pushing manufacturers toward fully waterborne systems. In addition to VOC limits, the regulation imposes strict caps on heavy metals, including a maximum lead content of 90 mg/kg, raising the bar for material safety and environmental performance.

The scale of China’s automotive industry amplifies the impact of these regulations. With annual vehicle production exceeding 26 million units, the enforcement of GB 30981.2-2025 is driving a comprehensive supply chain transformation affecting OEMs, Tier 1 suppliers, and coating manufacturers. Companies that can deliver compliant, high-performance coatings are positioned to capture significant market share as the industry transitions toward low-VOC, sustainable coating solutions in one of the world’s largest manufacturing hubs.

OEM Coatings Market Share and Segmentation Insights

Basecoat Segment Holds 32.6% Share Driven by Color Effects and High Film Build Demand

The OEM coatings market by coating layer is led by the basecoat segment, accounting for 32.6% of the global market share in 2025, due to its critical role in delivering color, visual effects, and aesthetic differentiation. Basecoats are responsible for metallic flake alignment, pearlescent finishes, matte effects, and color depth, making them the most formulation-intensive layer in automotive coatings, appliance coatings, and industrial OEM finishing. Additionally, basecoats are applied at higher film thicknesses (15–25 microns) compared to primers, driving greater material consumption across high-volume automotive assembly lines. As OEMs increasingly focus on premium finishes, customization, and brand differentiation, demand for advanced basecoat technologies continues to rise. This reinforces the segment’s leadership within the global OEM coatings market, supported by both aesthetic value and volume-driven demand dynamics.

Automated Spraying Captures 58.1% Share Driven by Robotic Efficiency and Superior Finish Quality

In the OEM coatings market by application method, automated spraying dominates with a 58.1% market share in 2025, reflecting its widespread adoption in automotive manufacturing, heavy equipment, and industrial coating lines. Advanced robotic spray systems, including bell applicators and reciprocators, deliver high transfer efficiency, uniform atomization, and consistent film thickness, even on complex 3D geometries. This ensures superior surface finish quality while minimizing overspray and defects. Furthermore, automated spray lines are increasingly integrated with Industry 4.0 technologies, such as real-time viscosity control, flow monitoring, and AI-driven defect detection, significantly reducing paint waste and rework rates. These capabilities enhance operational efficiency and sustainability, making automated spraying the preferred method for large-scale OEM production. As manufacturers prioritize precision coating, cost optimization, and digital transformation, automated spraying continues to lead the global OEM coatings market.

Competitive Landscape of the OEM Coatings Market

AkzoNobel Strengthens OEM Leadership Through Axalta Merger and Nanolayer Innovation

AkzoNobel N.V., strengthened by its merger with Axalta, is emerging as a global powerhouse in the OEM coatings market, with combined revenues exceeding $15.2 billion. In Q1 2026, the company reported a 7% rise in adjusted EBITDA to €345 million, achieving a 14.5% margin through price optimization and industrial efficiency strategies. Its Interpon Futura 2026–2029 Collection leverages nanolayer coating technology to deliver anodized aluminum aesthetics with superior weather resistance for automotive and architectural OEM applications. Additionally, AkzoNobel’s strategic divestment in India has optimized its financial structure, while its sustainability roadmap targets a 50% carbon reduction by 2030, reinforcing its leadership in eco-friendly OEM coatings.

PPG Industries Accelerates Growth with Low-Bake Technologies and Aerospace Coating Dominance

PPG Industries, Inc. continues to lead the industrial OEM coatings sector through its “Safety & Speed” strategy, targeting high-growth segments like aerospace MRO and EV battery protection. In 2026, the company exceeded financial expectations, driven by strong growth in its Aerospace and Protective & Marine divisions. A major innovation includes its low-bake automotive clearcoat system, which cures at 80°C—significantly reducing energy consumption and CO2 emissions. The acquisition of Ozark Materials further enhances its infrastructure coatings portfolio. With 12 consecutive quarters of volume growth in protective coatings, PPG maintains a dominant position in heavy-duty and high-performance OEM coating applications.

Sherwin-Williams Expands OEM Market Share with Integrated Supply Chain and Digital Tools

The Sherwin-Williams Company is a dominant player in the North American OEM coatings market, leveraging its robust supply chain and customer-centric “Last-Mile” delivery model. The company forecasts strong 2026 financial performance, with adjusted EPS between $11.50 and $11.90 despite macroeconomic challenges. Its Performance Coatings Group achieved a 19.0% margin, driven by strategic acquisitions like Suvinil. Sherwin-Williams is targeting architectural and industrial metal segment through its “Success by Design” digital platform, enabling efficient specification for suppliers. Additionally, its DesignHouse facility supports rapid development of custom functional coatings for industrial and appliance OEMs, strengthening its innovation leadership.

BASF Leads OEM Innovation with Advanced Color Science and Sustainable Mobility Coatings

BASF SE’s Coatings Division is a global leader in automotive OEM coatings, known for its expertise in molecular-level color innovation and sustainability. In 2026, the company introduced its “Driving the Proxy” color trends, featuring advanced interference pigment technologies for enhanced visual depth. BASF’s CathoGuard® 800 electrocoat is specifically designed for EV components, offering tin-free, corrosion-resistant protection for complex geometries. The company is also partnering with Chinese EV startups to develop waterborne coating systems that reduce capital expenditure by 15%. With its ChemCycling initiative, BASF integrates recycled feedstocks into production, reinforcing its position in sustainable OEM coating solutions.

Kansai Paint Drives APAC Expansion with Lightweight and High-Efficiency OEM Coatings

Kansai Paint Co., Ltd. is a key player in the Asia-Pacific OEM coatings market, focusing on lightweight and high-efficiency solutions for automotive and industrial sectors. In 2026, the company achieved a breakthrough with high-solid, low-viscosity coating technology, enabling premium “Class A” finishes at just 10 μm thickness—reducing material usage and vehicle weight. Kansai maintains a strong presence in Japan and is expanding aggressively in India to capitalize on high automotive growth rates. Its sustainability-driven approach includes eliminating hazardous materials like lead and chromium. Additionally, its joint venture in Europe supports the production of anti-corrosion coatings for renewable energy OEM applications, strengthening its global footprint.

China OEM Coatings Market: NEV Ecosystem and Smart Factory Integration Driving Global Leadership

China dominates the global OEM coatings market, driven by its leadership in New Energy Vehicles (NEVs) and rapid adoption of smart manufacturing technologies. The implementation of integrated paint-shop systems, where primer, basecoat, and clearcoat are applied in compressed cycles, is reducing energy consumption by 15–20%, significantly improving production efficiency.

Technological innovation includes radar-transparent coatings for EVs, ensuring seamless functioning of ADAS sensors through metallic finishes—critical for brands like BYD and NIO. Government mandates under the 2026 Green Manufacturing Standard require that at least 40% of vehicle production use waterborne or powder coatings, accelerating sustainability. Investments in graphene-enhanced cathodic electrocoats (E-coats) are enhancing corrosion resistance, particularly for electric truck chassis. Additionally, AI-driven facilities like Nippon Paint’s Smart Color Center in Shanghai are enabling real-time color matching in high-speed production lines. Key applications also include intumescent fire-protective coatings for EV battery systems, reinforcing China’s dominance in both volume and advanced innovation.

United States OEM Coatings Market: Smart Coatings and PFAS-Free Compliance Reshaping Industry

The United States OEM coatings market is defined by a “compliance-first” approach, driven by strict environmental regulations and high-value applications in automotive and aerospace sectors. The EPA’s updated TSCA regulations (2026) have triggered a shift away from PFAS-based coatings toward silicone-modified and acrylic alternatives, reshaping formulation strategies.

Technological advancements include self-healing smart clearcoats, which repair micro-scratches from environmental exposure, improving durability and vehicle aesthetics. The adoption of UV-LED curing technologies is reducing energy consumption in paint shops by up to 30%, aligning with carbon reduction goals. Innovations such as infrared-reflective coatings are improving EV efficiency by reducing cabin heat load. The market is also benefiting from growth in the commercial space sector, requiring coatings capable of withstanding extreme thermal cycles. Strategic expansions by companies like Axalta in waterborne coatings are supporting the rise of the U.S. “Battery Belt.”

Germany OEM Coatings Market: Circular Economy and Precision Finishing Leadership

Germany leads the European OEM coatings market through its focus on precision engineering, sustainability, and circular manufacturing systems. Innovations in 100% bio-based polyurethane resins, derived from non-food biomass, are enabling high-performance coatings while reducing environmental impact—critical for luxury automotive brands.

Technological advancements include digital twin color modeling, allowing virtual visualization of complex finishes, reducing physical sampling by up to 70%. The adoption of overspray recycling technologies, such as Dürr’s EcoDryScrubber, is eliminating water and chemicals from paint booth operations. Germany is also pioneering chrome-free pretreatment systems, aligning with EU regulatory standards. Key applications include coatings for hydrogen storage systems, addressing challenges such as hydrogen embrittlement. Partnerships like BASF’s closed-loop recycling initiatives are further reinforcing sustainability leadership.

India OEM Coatings Market: Manufacturing Expansion and Localization Driving High Growth

India is emerging as a high-growth OEM coatings market, fueled by large-scale investments under the PLI Scheme 2.0 and rapid expansion in automotive and rail manufacturing. The government’s push has catalyzed investments exceeding ₹25,000 crore, strengthening domestic coating supply chains.

The market is witnessing a major shift from solvent-based systems to waterborne basecoats, particularly in two-wheelers and passenger vehicles, driven by Bharat Stage VI (Phase 2) emission norms. Infrastructure development, including the Vande Bharat high-speed rail network and metro systems, is driving demand for advanced anti-corrosive coatings. Investments in R&D centers, such as Mitsui Chemicals’ facility in Gurugram, are enhancing localized innovation. Additionally, stricter BIS standards requiring long-term durability (up to 10 years gloss retention) are improving product quality across public transport applications.

Japan OEM Coatings Market: Ultra-Functional Coatings and Robotics Integration

Japan’s OEM coatings market is characterized by ultra-functional materials, precision engineering, and robotics integration. The adoption of “wet-on-wet” coating technologies is reducing production cycles by eliminating intermediate baking steps, significantly improving efficiency.

Innovations such as photocatalytic coatings enable self-cleaning vehicle surfaces by breaking down pollutants under sunlight. Japan is also advancing radar-absorbing coatings for autonomous systems, including delivery robots and drones. High-end applications in medical and robotic equipment are driving demand for antimicrobial metallic coatings with premium finishes. Government incentives for net-zero manufacturing facilities are encouraging the adoption of low-temperature curing systems, further enhancing sustainability.

South Korea OEM Coatings Market: Electronics Integration and Energy Storage Innovation

South Korea is leveraging its leadership in electronics and EV battery manufacturing to drive innovation in OEM coatings. The development of high-dielectric coatings for EV motor housings is enabling improved electrical insulation and thermal management, critical for next-generation vehicle performance.

Technological advancements include nano-glass flake “fine-sparkle” clearcoats, delivering premium aesthetics in consumer electronics and automotive applications. The market is also benefiting from innovations in coatings for foldable OLED displays, which require durability under repeated mechanical stress. Government initiatives such as the K-Battery Strategy are supporting the development of solvent-free coating systems, while investments in automated E-coat lines are improving efficiency and reducing material waste. Expansion of R&D facilities, including KCC Corporation’s centers, is further strengthening South Korea’s position in advanced OEM coating technologies.

OEM Coatings Market Report Scope

OEM Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$126.6 Billion

|

|

Market Size (2032)

|

$177 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Cured), By Resin Type (Acrylic, Epoxy, Polyurethane, Alkyd, Polyester, Vinyl and Fluoropolymers), By End-Use Industry (Automotive and Transportation, Consumer Goods and Appliances, Furniture, Heavy Equipment and Industrial Machinery, Aerospace and Defense, Electrical Insulation and Components), By Coating Layer (Electrocoat, Primer, Basecoat, Clearcoat), By Application Method (Automated Spraying, Dipping, Roll and Coil Coating, Flow and Curtain Coating)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun A/S, KCC Corporation, RPM International Inc., Hempel A/S, Asian Paints Limited, Beckers Group, Tiger Coatings GmbH and Co. KG, Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

OEM Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Cured

By Resin Type

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- Polyester

- Vinyl and Fluoropolymers

By End-Use Industry

- Automotive and Transportation

- Consumer Goods and Appliances

- Furniture

- Heavy Equipment and Industrial Machinery

- Aerospace and Defense

- Electrical Insulation and Components

By Coating Layer

- Electrocoat

- Primer

- Basecoat

- Clearcoat

By Application Method

- Automated Spraying

- Dipping

- Roll and Coil Coating

- Flow and Curtain Coating

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in OEM Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun A/S

- KCC Corporation

- RPM International Inc.

- Hempel A/S

- Asian Paints Limited

- Beckers Group

- Tiger Coatings GmbH & Co. KG

- Sika AG

*- List not Exhaustive