Military Aerospace Coatings Market Size, CARC Technologies, and Defense Aviation Coating Demand Outlook

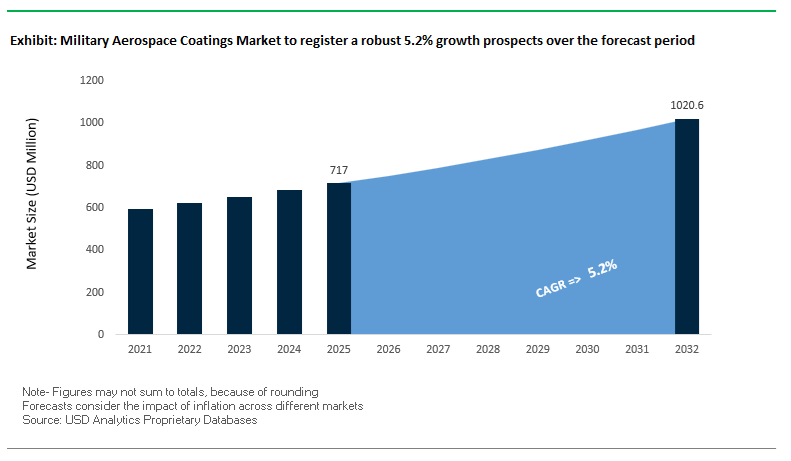

The global military aerospace coatings market was valued at $717 million in 2025 and is projected to reach $1,022.4 million by 2032, growing at a CAGR of 5.2%. Market growth is driven by increasing demand for chemical agent resistant coatings (CARC), radar-absorbent coatings, high-performance aerospace coatings, and advanced military-grade surface treatments across fighter aircraft, transport planes, UAVs, and defense infrastructure. These coatings are critical for ensuring corrosion protection, stealth capability, chemical resistance, and operational durability in extreme environments.

A key growth driver is the modernization of military aircraft fleets and defense aviation systems, where coatings play a vital role in enhancing stealth characteristics, infrared (IR) signature management, and survivability in hostile environments. Advanced coatings are engineered to meet stringent MIL-PRF specifications, offering low observability, resistance to chemical warfare agents, and high thermal stability. Additionally, the increasing focus on maintenance, repair, and overhaul (MRO) efficiency is driving demand for coatings that enable faster application, reduced downtime, and extended service intervals.

The market is also benefiting from advancements in nanocoatings, lightweight coating systems, and multifunctional materials, which improve fuel efficiency, reduce aircraft weight, and enhance structural integrity. Growing defense budgets, particularly in Asia-Pacific and North America, are further accelerating the adoption of next-generation aerospace coatings. Sustainability considerations, including low-VOC formulations and waste reduction during application, are also gaining importance in military procurement strategies.

Market Analysis: MRO Optimization, Stealth Coating Innovation, and Defense Sector Expansion Driving Market Evolution

The military aerospace coatings industry is evolving through technological innovation, digitalization, and strategic investments in defense-focused coating solutions. In January 2026, AkzoNobel announced a €50 million upgrade to its Waukegan aerospace facility, enhancing capabilities with high-speed dissolvers and a Rapid Service Unit. This development is aimed at accelerating color development and turnaround times for military MRO operations, addressing the need for faster aircraft servicing cycles.

Regulatory approvals and regional expansion are strengthening global supply chains. AkzoNobel’s January 2026 extended CAAC approval in China enables localized support for military-derivative airframes in the Asian market, aligning with the region’s increasing investment in indigenous defense manufacturing. Similarly, Nippon Paint’s November 2025 strategic pivot toward defense and non-residential sectors reflects growing demand for locally sourced aerospace coatings in Japan and Southeast Asia.

Training and digitalization are becoming critical for ensuring application precision. In October 2025, AkzoNobel launched AS7489-certified training modules, focusing on precise film thickness control, which is essential for maintaining weight efficiency and stealth performance. This is complemented by the company’s Virtual Reality (VR) paint training initiative, reported in July 2025, which allows defense contractors to simulate coating application processes, reducing material waste and improving workforce readiness.

Product compliance and performance standards are also advancing. Hentzen Coatings confirmed that its CARC and MIL-PRF-85285 compliant coatings meet updated infrared reflectance and decontamination standards, ensuring compatibility with next-generation military systems. Additionally, DuPont’s Tedlar® PVF coatings, launched in December 2023, are increasingly being specified for military transport and MEDEVAC aircraft, offering exceptional durability and chemical resistance for interior applications.

Strategic leadership and corporate focus are shaping long-term innovation. PPG Industries’ January 2024 appointment of a dedicated aerospace coatings leader underscores its commitment to advancing coatings for modernized military strike systems, including next-generation aircraft platforms.

Broader defense strategies are also influencing coating demand. Hempel A/S, through its March 2025 “Accelerate to Win” strategy, is prioritizing high-end specialty coatings for military infrastructure and support airframes, reflecting the expanding scope of coatings beyond aircraft to include defense facilities and ground equipment.

Market Trend: Next-Generation “Tough-Coat” RAM Systems Enhancing Stealth Durability and Fleet Readiness

The military aerospace coatings industry is undergoing a critical evolution in Radar-Absorbent Material (RAM) technologies, particularly for 5th-generation stealth platforms such as advanced multirole fighters. Historically, the operational limitation of stealth aircraft has been the high maintenance-man-hour per flight hour ratio associated with fragile RAM coatings. As of 2026, the transition to “tough-coat” RAM formulations are significantly improving durability, reducing maintenance burden, and enhancing mission readiness.

Modern RAM coatings deployed on upgraded stealth platforms have achieved approximately 30% reduction in specialized maintenance hours compared to earlier-generation coatings. This improvement directly supports defense objectives to increase mission-capable rates, which have historically remained constrained due to maintenance-intensive stealth surfaces. Enhanced coating robustness is enabling more efficient sustainment cycles and reducing downtime between missions.

Durability improvements are equally significant. Next-generation RAM systems maintain signal attenuation performance for up to 400 flight hours in high-speed, high-friction operational environments, effectively doubling the service interval compared to previous 200-hour benchmarks. This extended lifecycle reduces the frequency of costly re-skinning operations and improves overall aircraft availability. In parallel, the growing operational footprint of stealth fleets, which surpassed 1.3 million cumulative flight hours by early 2026, is accelerating demand for scalable and repeatable coating processes.

Automation is emerging as a key enabler in this transition. Robotic spray-application systems are increasingly being adopted to ensure precise coating thickness and uniformity, reducing human-induced variability by 15% to 20%. This level of process control is essential for maintaining consistent radar signature performance across fleets, positioning automated RAM application as a standard in next-generation aerospace manufacturing and maintenance operations.

Market Trend: High-Solids CARC Systems Advancing Field Repairability and Operational Agility

Chemical Agent Resistant Coatings (CARC) are evolving to meet the operational demands of modern military platforms, particularly in forward-deployed environments. The adoption of high-solids CARC formulations under updated military specifications is enabling rapid field repair, improved environmental compliance, and enhanced durability across ground and air support assets.

New-generation high-solids polyurethane CARC systems achieve volume solids levels of 51% to 54% while maintaining VOC content at or below 180 g/L. This balance between solids loading and emissions compliance is critical as military operations increasingly align with global environmental regulations. These coatings provide robust protection against chemical agents while minimizing environmental impact during application.

Drying performance is a key operational advantage. Advanced CARC formulations reach dry-to-touch states within 5 to 30 minutes and achieve full hardness in approximately three hours. This rapid curing capability allows for same-shift repair and redeployment of equipment, significantly improving operational readiness compared to legacy systems that require up to 24 hours for full cure. This is particularly valuable in high-tempo operational environments where asset availability is critical.

Mechanical durability is also enhanced, with high-solids CARC coatings demonstrating approximately 40% higher abrasion resistance compared to waterborne alternatives. This performance is essential for assets operating in harsh conditions such as desert environments, where sand abrasion and particulate exposure can rapidly degrade conventional coatings. These advancements are positioning high-solids CARC systems as a critical component of modern military maintenance strategies, supporting both performance and logistical efficiency.

Market Opportunity: PFAS Elimination Mandates Driving Development of Next-Generation Fluorine-Free Aerospace Coatings

The global regulatory push to eliminate perfluoroalkyl and polyfluoroalkyl substances is creating a transformative opportunity in the military aerospace coatings sector. Under evolving U.S. Department of Defense mandates, including requirements tied to fiscal year 2026 authorization frameworks, new coating formulations must be free of PFAS to qualify for inclusion in approved military specifications.

This shift represents a fundamental challenge for coating manufacturers, as fluoropolymer resins have historically been central to achieving the chemical resistance, weatherability, and low surface energy required in aerospace applications. The transition to PFAS-free systems is therefore driving significant research and development investment, with industry spending exceeding hundreds of millions of dollars to develop alternative chemistries.

Emerging solutions include silicon-alkyd hybrids and advanced acrylic-urethane systems engineered to replicate the performance characteristics of fluoropolymers without the environmental persistence associated with PFAS. At the same time, regulatory reporting requirements under environmental frameworks are increasing transparency and compliance obligations, further accelerating the transition toward sustainable coating technologies. This “clean-sheet” reformulation requirement is expected to reshape the competitive landscape, favoring suppliers with advanced material science capabilities and regulatory-ready product portfolios.

Market Opportunity: Sixth-Generation Fighter Programs Creating Demand for Multi-Spectral Low-Observable Coating Technologies

The development of sixth-generation fighter platforms under international programs is creating a high-value opportunity segment for advanced low-observable coating systems. Collaborative initiatives such as next-generation combat aircraft programs are emphasizing sovereign capability, requiring participating nations to develop and maintain domestic expertise in stealth coating technologies.

This shift toward localized capability is driving demand for regionally developed RAM systems, reducing reliance on proprietary technologies controlled by external suppliers. Governments are allocating substantial funding to establish domestic manufacturing and maintenance ecosystems for low-observable coatings, creating long-term service and supply contracts with significant economic value.

Technical requirements for next-generation platforms are also expanding beyond traditional radar stealth. Coating systems are now expected to provide multi-spectral masking, including infrared and visual signature management. This is driving the integration of advanced material systems, including metamaterial additives capable of manipulating thermal emissivity and optical properties. Such coatings must maintain performance across a broader electromagnetic spectrum while withstanding extreme operational conditions.

The convergence of sovereign defense strategies, advanced material science, and multi-domain stealth requirements is positioning next-generation aerospace coatings as a critical innovation frontier. Suppliers capable of delivering integrated, multi-functional coating systems are expected to play a central role in the evolution of future combat aircraft platforms.

Military Aerospace Coatings Market Share and Segmentation Insights

Fixed-Wing Aircraft Account for 52% Share Driven by Fleet Size and Advanced Coating Needs

The military aerospace coatings market by aircraft type is dominated by fixed-wing aircraft, holding 52% of the global market share in 2025, driven by their extensive fleet size and high coating consumption per unit. Platforms such as fighter jets (F-35, F-16, F-18), bombers (B-52, B-21), and transport aircraft (C-17, C-130) require advanced coating systems for radar-absorbent materials (RAM), corrosion protection, and leading-edge erosion resistance. A major growth driver is the increasing adoption of stealth technology, where specialized coatings are engineered to deliver controlled reflectivity, infrared signature suppression, and radar absorption. These high-performance coatings are among the most technologically sophisticated and high-value segments in the coatings industry. As defense modernization programs accelerate globally, the demand for next-generation military aircraft coatings continues to strengthen the dominance of fixed-wing platforms.

Maintenance, Repair, and Overhaul Holds 58% Share Due to Continuous Aircraft Servicing Cycles

In the military aerospace coatings market by end-user, maintenance, repair, and overhaul (MRO) leads with a 58% market share in 2025, reflecting the ongoing need for aircraft refinishing and coating maintenance. Military aircraft require repainting every 3 to 7 years due to harsh operational conditions, including UV exposure, extreme temperatures, and mission-induced wear, as well as the need to maintain stealth and radar signature performance. This creates a steady, recurring demand for aerospace-grade coatings, stripping solutions, and surface treatments, independent of new aircraft production cycles. Additionally, depot-level refinishing operations—often conducted at specialized military facilities or contracted MRO providers—involve coating removal (via chemical or laser stripping) and precise reapplication of advanced coating systems tailored to each airframe. This continuous lifecycle demand firmly establishes MRO as the dominant revenue segment in the global military aerospace coatings market.

Competitive Landscape in the Military Aerospace Coatings Market

PPG leads military aerospace coatings with LO technology and global MRO integration

PPG Industries stands as the dominant player in the military aerospace coatings market, driven by its leadership in low-observable coatings and high-durability solutions. In Q1 2026, the company reported $3.9 billion in net sales, supported by strong demand from major defense programs such as the F-35 Lightning II and B-21 Raider. PPG is pioneering electro-conductive and anti-static coatings designed for composite airframes, essential for mitigating electromagnetic interference in advanced electronic warfare systems. Its Total Service Solutions platform integrates coating application with digital inventory management, strengthening its global MRO footprint across the U.S. and Europe. The company’s reaffirmed EPS guidance reflects confidence in scaling chrome-free primer technologies.

AkzoNobel expands regional aerospace coatings capabilities with low-VOC compliance focus

AkzoNobel is strengthening its position in military aerospace coatings through regional expansion and environmentally compliant product development. The company is set to open its Dubai Aerospace Coatings Hub in 2026, enabling localized production of Aerodur 3001 and Eclipse coatings for Middle Eastern defense fleets. It has also secured extended approvals from the Civil Aviation Administration of China, reinforcing its presence in the Asia-Pacific defense market. AkzoNobel’s Aerobase system reduces aircraft weight by up to 20%, improving fuel efficiency and operational performance. The company’s focus on REACH-compliant and low-VOC coatings aligns with stringent NATO environmental standards, positioning it as a key supplier for sustainable military aviation solutions.

Sherwin-Williams dominates defense coatings with MIL-SPEC solutions and digital visualization tools

The Sherwin-Williams Company maintains a strong position in the North American military aerospace coatings market, particularly in fixed-wing and rotary aircraft segments. Its Jet Glo Express™ and Military Mil-Spec coatings are widely specified for aircraft such as the C-130 and CH-47, delivering high durability and performance under demanding conditions. The company’s Aerospace Color Visualizer enables defense OEMs to simulate camouflage and infrared-reflective patterns using digital twin technology, enhancing design precision. With an extensive network of over 4,800 locations, Sherwin-Williams provides localized technical support to contractors and suppliers. Its SKYscapes® technology further enhances coating efficiency with single-stage, high-gloss finishes.

Hentzen advances chrome-free primers and CARC technologies for military compliance

Hentzen Coatings is a specialized innovator in military aerospace coatings, particularly in chemical agent resistant coatings (CARC) and advanced primer technologies. The company is developing next-generation chrome-free primers that aim to match the corrosion protection performance of traditional hexavalent chromium systems while eliminating environmental toxicity. Hentzen was the first to achieve compliance with MIL-PRF-23377 standards using chrome-free formulations, marking a significant milestone in sustainable aerospace coatings. Its automated production of 2K aerosol and touch-up kits ensures rapid delivery for field maintenance operations. The company also provides specialized coatings for engine components and landing gear, including heat-reflective and anti-galling solutions for high-stress environments.

Indestructible Paint specializes in high-temperature aerospace coatings for engine systems

Indestructible Paint Ltd is a niche leader in high-performance coatings for aero-engines and critical mechanical systems. In 2026, the company secured its largest-ever order from a U.S. aerospace customer, expanding its presence in both defense and emerging space applications. Its coatings are engineered to withstand temperatures up to 1,000°C while resisting hydraulic fluids, de-icing chemicals, and turbine fuels. The company received recognition from the UK Institute of Materials Finishing for its development of chromium-free anticorrosive primers. Indestructible Paint is also advancing low-friction turbine coatings aimed at improving fuel efficiency in next-generation combat aircraft, reinforcing its role in high-performance propulsion systems.

Mankiewicz leads cockpit and composite interface coatings for next-generation aircraft

Mankiewicz Gebr. & Co. is a specialized provider of coatings for aircraft interiors and composite-metal interfaces, particularly within European defense programs. The company is recognized for its expertise in preventing galvanic corrosion between carbon-fiber structures and aluminum components, a critical challenge in modern aircraft design. Its soft-touch cockpit coatings enhance pilot ergonomics while meeting stringent fire, smoke, and toxicity (FST) standards. Mankiewicz also focuses on maintenance-ready coatings that reduce turntimes in MRO operations. With a strategic expansion into Asia-Pacific, the company is positioning itself to capture growth opportunities driven by regional military fleet modernization initiatives.

United States Military Aerospace Coatings Market: Smart Coatings and Next-Generation Air Dominance Driving Innovation

The United States leads the military aerospace coatings market, driven by advanced defense programs such as Next Generation Air Dominance (NGAD) and the rapid evolution of multi-functional smart coating technologies. The commercialization of sensor-integrated coatings capable of detecting structural fatigue and chemical leaks in real time is transforming maintenance strategies for advanced aircraft platforms such as the F-35 and B-21 bombers. These innovations are significantly improving operational safety and lifecycle management.

Regulatory shifts, including the phase-out of hexavalent chromium and PFAS-based coatings, are accelerating the adoption of magnesium-rich and lithium-based corrosion protection systems. Infrastructure investments in robotic spray application systems, particularly at facilities like Hill Air Force Base, are enabling micron-level precision for radar-absorbing material (RAM) coatings. The development of UV-curable ultra-low-energy coatings is reducing curing times dramatically, supporting rapid maintenance operations. Additionally, specialized applications such as infrared suppression coatings for rotary-wing aircraft are enhancing survivability in combat scenarios. Expansion by major players like PPG and Sherwin-Williams is further strengthening the U.S. position in high-performance aerospace coatings.

China Military Aerospace Coatings Market: Stealth Technology and Graphene Integration Accelerating Growth

China’s military aerospace coatings market is rapidly advancing, supported by its focus on stealth technology, indigenous material development, and next-generation aircraft programs. The country is scaling the production of graphene-enhanced anti-corrosion coatings, which provide superior durability for carrier-based aircraft operating in harsh marine environments.

Technological advancements include the development of broadband radar-absorbing coatings, designed to minimize radar cross-section across multiple frequency bands, enhancing stealth capabilities. Government initiatives under the 14th Five-Year Plan are driving a high level of indigenization in aerospace coating materials, reducing reliance on imported specialty chemicals. Investments in specialized infrastructure, such as the Stealth Coating Center of Excellence in Chengdu, are supporting rapid coating application and maintenance for both manned and unmanned aerial systems. The adoption of high-solid polyurethane coatings is further improving UV resistance and durability in high-altitude missions, while regulatory frameworks are promoting low-VOC coating solutions for sustainable defense manufacturing.

India Military Aerospace Coatings Market: Indigenization and Defense Manufacturing Expansion

India is emerging as a strategic hub in the military aerospace coatings market, driven by its push for self-reliance under the “Aatmanirbharta” initiative. The development of indigenous radar-absorbing coatings, successfully tested for the LCA Tejas Mk1A program, marks a significant milestone in domestic aerospace innovation.

Infrastructure expansion, including robotic painting facilities by Hindustan Aeronautics Limited (HAL), is enhancing production efficiency and coating precision for military aircraft upgrades. Government policies under the Defense Acquisition Procedure (DAP) are incentivizing the use of locally manufactured, environmentally compliant coatings. The market is also seeing innovation in moisture-resistant and anti-fungal coatings, tailored for naval aircraft operating in tropical coastal environments. Significant investments in stealth technology for the Advanced Medium Combat Aircraft (AMCA) program and the development of heat-resistant coatings for missile systems are further strengthening India’s capabilities in high-performance aerospace coatings.

Russia Military Aerospace Coatings Market: Extreme-Environment and Hypersonic Coating Expertise

Russia continues to maintain a strong position in the military aerospace coatings market, particularly in applications requiring extreme thermal resistance and high-speed performance. The development of radio-transparent coatings for aircraft nose cones enables effective radar transmission while maintaining stealth characteristics, a critical requirement for modern fighter jets such as the Su-57.

Technological advancements include refractory ceramic coatings designed for hypersonic missiles, capable of withstanding temperatures exceeding 2,000°C. These coatings are essential for next-generation defense systems such as the Zircon and Kinzhal missile platforms. The market also focuses on specialized applications such as anti-icing coatings for Arctic operations, supporting long-range bombers in extreme environments. Investments in vacuum-deposition technologies are enabling the application of ultra-thin metallic coatings for enhanced performance. Russia’s expansion into export-oriented stealth coating solutions further highlights its role in the global defense coatings landscape.

France Military Aerospace Coatings Market: Adaptive Camouflage and European Defense Integration

France is a leading player in the European military aerospace coatings market, driven by its focus on defense sovereignty and advanced coating technologies. Innovations in adaptive camouflage coatings, used in Rafale F5 aircraft, are enabling dynamic changes in emissivity to improve stealth performance under varying environmental conditions.

The development of biocide-free antimicrobial coatings for cockpit interiors reflects a growing emphasis on crew safety and operational health. Infrastructure investments, including advanced testing facilities at Dassault Aviation’s Istres center, are supporting the development of next-generation coatings for stealth unmanned systems. France is also advancing low-friction coatings for engine components, improving fuel efficiency and reducing thermal signatures. Government initiatives under the Military Programming Law (LPM) are strengthening domestic supply chains, while early adoption of chrome-free coating technologies is setting new environmental benchmarks in military aviation.

Israel Military Aerospace Coatings Market: Combat-Tested Innovation and Rapid Field Repair Technologies

Israel’s military aerospace coatings market is uniquely driven by real-world combat data and rapid innovation cycles, making it a leader in operationally validated coating technologies. The development of field-repairable radar-absorbing material (RAM) kits allows maintenance crews to perform quick repairs in forward operating environments, significantly reducing downtime for advanced aircraft such as the F-35I “Adir”.

Continuous feedback from active deployments is driving improvements in stealth coating durability and performance, providing valuable insights for global aerospace programs. Israel is also advancing multi-spectral camouflage coatings for UAVs, enabling evasion across visual, thermal, and radar detection systems. Infrastructure expansion by Israel Aerospace Industries (IAI) is supporting large-scale production of advanced aerospace components with specialized coatings. Strategic agreements with the United States allow for customized electronic warfare coating applications, reinforcing Israel’s position as a leader in next-generation aerospace surface technologies.

Military Aerospace Coatings Market Report Scope

Military Aerospace Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$717 Million

|

|

Market Size (2032)

|

$1022.4 Million

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Resin Type (Polyurethane, Epoxy, Acrylic, Fluoropolymers, Silicones, Specialty Resins), By Technology (Solvent-borne, Water-borne, Powder Coatings, Radiation-Cured), By Aircraft Type (Fixed Wing, Rotary Wing, Unmanned Aerial Vehicles, Spacecraft and Missiles), By Application Area (Exterior Coatings, Interior Coatings), By End-User (Original Equipment Manufacturer, Maintenance, Repair, and Overhaul), By Substrate (Aluminum Alloys, Composites, Titanium and Steel Alloys, Magnesium Alloys)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Hentzen Coatings, Inc., Axalta Coating Systems Ltd., BASF SE, Mankiewicz Gebr. and Co., Henkel AG and Co. KGaA, Socomore, IHI Ionbond AG, Saint-Gobain S.A., Jotun A/S, Zircotec Ltd., BryCoat Inc., Indestructible Paint Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Military Aerospace Coatings Market Segmentation

By Resin Type

- Polyurethane

- Epoxy

- Acrylic

- Fluoropolymers

- Silicones

- Specialty Resins

By Technology

- Solvent-borne

- Water-borne

- Powder Coatings

- Radiation-Cured

By Aircraft Type

- Fixed Wing

- Rotary Wing

- Unmanned Aerial Vehicles

- Spacecraft and Missiles

By Application Area

- Exterior Coatings

- Interior Coatings

By End-User

- Original Equipment Manufacturer

- Maintenance, Repair, and Overhaul

By Substrate

- Aluminum Alloys

- Composites

- Titanium and Steel Alloys

- Magnesium Alloys

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Military Aerospace Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Hentzen Coatings, Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Mankiewicz Gebr. & Co.

- Henkel AG & Co. KGaA

- Socomore

- IHI Ionbond AG

- Saint-Gobain S.A.

- Jotun A/S

- Zircotec Ltd.

- BryCoat Inc.

- Indestructible Paint Ltd.

*- List not Exhaustive