MRO Protective Coatings Market Size, Asset Lifecycle Extension, and High-Performance Maintenance Coatings Outlook

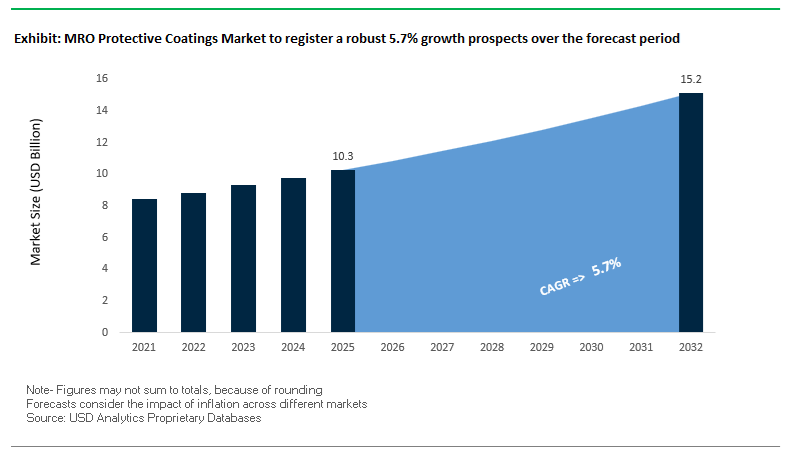

The global MRO (Maintenance, Repair, and Overhaul) protective coatings market was valued at $10.3 billion in 2025 and is projected to reach $15.2 billion by 2032, expanding at a CAGR of 5.7%. Growth is driven by rising demand for protective coatings for maintenance, corrosion-resistant coatings, industrial MRO coatings, aerospace maintenance coatings, and infrastructure refurbishment solutions across energy, marine, aviation, infrastructure, and industrial facilities. These coatings are essential for extending asset lifespan, minimizing downtime, and reducing total cost of ownership in aging infrastructure and high-value equipment.

A primary growth driver is the increasing global focus on asset lifecycle management and predictive maintenance, particularly in critical infrastructure such as bridges, offshore platforms, wind turbines, and aircraft fleets. MRO coatings are designed to provide corrosion resistance, chemical protection, thermal stability, and mechanical durability, enabling operators to maintain performance in harsh environments classified as C5VH and CX corrosion zones. Additionally, the rapid expansion of renewable energy infrastructure and aerospace MRO activities is further accelerating demand for specialized coating systems.

The market is also benefiting from advancements in digital maintenance technologies, smart coatings, and high-performance formulations, which support real-time monitoring, faster application, and reduced maintenance cycles. Sustainability trends, including the adoption of low-VOC coatings, high-solids systems, and energy-efficient application methods, are influencing product development. Regionally, North America and Europe lead in advanced MRO technologies, while the Middle East and Asia-Pacific are emerging as high-growth regions due to expanding aviation and energy infrastructure.

Market Analysis: MRO Consolidation, Aerospace Expansion, and Digital Maintenance Solutions Driving Market Evolution

The MRO protective coatings industry is undergoing structural transformation driven by industry consolidation, infrastructure expansion, and digital innovation in maintenance practices. A major development occurred in February 2026, when AkzoNobel and Axalta announced a merger of equals, creating a dominant player in the MRO coatings segment by combining AkzoNobel’s International® protective coatings with Axalta’s high-performance refinish and industrial maintenance portfolio. This consolidation is expected to significantly influence global supply chains and specification standards in the MRO sector.

Strategic investments in aerospace MRO infrastructure are accelerating market growth. In January 2026, AkzoNobel announced the launch of a Dubai Aerospace Coatings Hub, designed to provide localized coating solutions and color blending services for regional airlines, significantly reducing turnaround times. Similarly, PPG Industries’ $380 million aerospace coatings facility in North Carolina, announced in October 2025, is focused on meeting rising demand for commercial and military aircraft maintenance coatings, highlighting the rapid expansion of the aviation MRO segment.

Product innovation is targeting emerging maintenance challenges in energy and infrastructure. In November 2025, Jotun introduced specialized Energy Storage System (ESS) coatings, engineered for extreme corrosion environments while providing electrical insulation for battery storage systems. Sherwin-Williams further expanded its MRO portfolio in May 2025 with Repacor SW-1000 and Sher-Bar TEC, designed for offshore wind turbine maintenance and infrastructure rehabilitation, addressing the growing need for coatings that support renewable energy asset longevity.

Advanced applications in regulated environments are also gaining traction. Sherwin-Williams showcased pharmaceutical cleanroom coatings at INTERPHEX 2025, engineered to withstand aggressive sterilization processes while maintaining non-porous, contamination-resistant surfaces, reflecting increasing demand for high-performance coatings in healthcare and life sciences facilities.

Strategic repositioning and financial performance indicate strong market momentum. RPM International reported record Q3 FY2026 sales of $1.61 billion, with its Performance Coatings Group achieving 8.4% growth, driven by demand for engineered MRO solutions. Additionally, AkzoNobel’s September 2025 divestment of its decorative business in India allows a sharper focus on high-margin industrial and MRO coatings, reinforcing the strategic importance of this segment.

Digitalization is emerging as a key differentiator in MRO services. Hempel A/S, through its “Accelerate to Win” strategy launched in March 2025, is integrating AI-driven corrosion monitoring and predictive maintenance tools, enabling asset owners to optimize maintenance schedules and reduce unexpected failures. Complementing this trend, PPG Industries’ January 2024 leadership initiative focuses on modernizing and digitizing its global aerospace MRO supply chain, improving service efficiency and responsiveness.

Market Trend: High-Solids and Single-Coat Systems Reducing Turnaround Time in Commercial Aviation MRO

The commercial aviation MRO coatings segment is undergoing a significant process transformation as operators adopt high-solids and single-coat coating systems to compress turnaround time (TAT) and improve operational efficiency. Traditional multi-coat systems are increasingly being replaced by advanced basecoat/clearcoat hybrids or enhanced single-coat technologies that reduce application complexity while maintaining performance standards.

Field data from late 2025 indicates that next-generation single-coat systems can reduce total coating application time by 30% to 40% at MRO facilities. This reduction is critical in an industry where aircraft downtime directly impacts airline revenue and fleet utilization. Faster coating cycles enable MRO providers to increase throughput without expanding physical infrastructure, improving overall service capacity.

Weight reduction is an additional performance driver. Modern high-solids coatings achieve approximately 36% lower dry-film weight compared to legacy systems. For single-aisle aircraft, this reduction contributes to measurable fuel savings and lower carbon emissions over the aircraft’s operational lifecycle. As airlines intensify their focus on sustainability and cost efficiency, coating weight is becoming a strategic parameter in maintenance planning.

Application performance has also improved significantly. Advanced formulations exhibit up to 40% better sag resistance, allowing technicians to achieve uniform coverage and required hiding power in a single pass. This reduces rework, enhances finish consistency across mixed fleets, and minimizes labor intensity. These combined advantages are positioning high-solids and single-coat systems as the preferred solution for next-generation commercial aircraft maintenance operations.

Market Trend: Ultra-High Solids Primers Enhancing Throughput and Compliance in Military MRO Operations

Military aviation MRO facilities are increasingly adopting ultra-high solids (UHS) primer systems to address maintenance backlogs and improve depot efficiency. Coatings with solids content in the range of 90% to 95% by volume are enabling faster application cycles while maintaining stringent performance requirements for corrosion protection and durability.

The use of UHS primers is directly improving hangar throughput. Military depots report a 15% to 20% increase in processing capacity due to reduced flash-off times and fewer application passes required to achieve specified dry film thickness. This is particularly important in large-scale maintenance operations where coating application has historically been a bottleneck.

Environmental compliance is another critical factor driving adoption. UHS coatings typically emit less than 250 g/L of VOCs, allowing military facilities to operate within tightening regional air quality regulations. This represents a significant improvement over legacy solvent-based system, which often exceed 350 g/L, and reduces the need for additional emission control infrastructure.

Despite their high viscosity, modern UHS primers deliver robust corrosion protection. Laboratory testing conducted in 2025 demonstrates performance exceeding 2,000 hours in salt spray exposure, with strong adhesion characteristics on direct-to-metal applications. This ensures long-term protection for advanced airframes, including next-generation platforms operating in demanding environments. The convergence of efficiency, compliance, and performance is driving widespread adoption of UHS technologies in military MRO operations.

The modernization of next-generation aircraft carriers is creating a specialized opportunity segment within the MRO coatings market. Advanced carrier platforms incorporate high-intensity operational systems that place unprecedented demands on coating performance, particularly in-flight deck and hangar environments.

Flight deck coatings are required to withstand significantly higher thermal and mechanical stress due to increased sortie rates and advanced launch and recovery systems. New coating specifications demand enhanced resistance to heat, friction, and impact, ensuring durability under continuous operational cycles. This creates demand for high-performance, thermally stable coatings capable of maintaining integrity under extreme conditions.

In addition to deck applications, there is growing interest in “smart” anti-corrosion coatings for internal structures such as hangar bays. These coatings are designed to provide early detection of corrosion through visual indicators or self-healing mechanisms, reducing the need for intensive inspection and maintenance. Adoption of such technologies is projected to reduce corrosion-related maintenance hours by approximately 12% per deployment cycle, improving operational efficiency and lifecycle cost management.

The scale and longevity of carrier programs ensure sustained demand for advanced coatings, positioning this segment as a high-value niche for suppliers capable of delivering specialized, high-durability solutions.

Market Opportunity: EU Rail Maintenance Directive Creating Standardized Demand for High-Durability MRO Coatings

The implementation of a unified rail maintenance directive across Europe is creating a significant opportunity for MRO protective coatings in the rail sector. The directive establishes standardized requirements for durability, fire safety, and corrosion resistance, effectively harmonizing coating specifications across the region.

Under the new framework, coatings used in rail maintenance must comply with EN 45545-2 fire safety standards and ISO 12944 corrosion protection requirements. This standardization eliminates regional variability and creates a consolidated market for compliant coating systems, estimated to exceed €500 million in value. Suppliers offering certified, pan-European solutions are well positioned to capture this demand.

Ease of maintenance is a central focus of the directive, driving demand for coatings with enhanced cleanability and resistance to repeated chemical exposure. Rail operators now require coatings that can withstand at least 25 aggressive cleaning cycles without degradation of gloss or color. This requirement is accelerating the adoption of advanced polysiloxane topcoats, which offer superior chemical resistance and long-term aesthetic retention.

These regulatory changes are transforming the rail MRO coatings landscape, shifting demand toward high-performance, standardized solutions that support operational efficiency and long-term asset durability across European rail networks.

MRO Protective Coatings Market Share and Segmentation Insights

Field-Applied Coatings Hold 48.4% Share Driven by In-Situ Corrosion Protection for Critical Infrastructure

The MRO protective coatings market by form is led by field-applied coatings, accounting for 48.4% of the global market share in 2025, due to their essential role in on-site maintenance and repair of large-scale assets. Infrastructure such as pipelines, bridges, storage tanks, offshore platforms, and wind turbines cannot be relocated to controlled environments, making brush, roller, and plural-component spray-applied coatings indispensable for in-situ applications. These coatings—primarily high-solids epoxies, polyurea, and corrosion-resistant systems—are engineered for fast curing, enabling assets to return to operation within hours and minimizing costly downtime. As industries prioritize asset integrity management, corrosion protection, and operational continuity, field-applied coatings remain the backbone of the global industrial MRO coatings market.

Contract Service Providers Capture 52.3% Share Through Safety Compliance and Condition-Based Maintenance Programs

In the MRO protective coatings market by sales channel, professional contract service providers dominate with a 52.3% market share in 2025, driven by the complexity and safety requirements of industrial coating applications. MRO projects demand rigorous surface preparation standards (SSPC-SP10/NACE No. 2 abrasive blasting), along with strict adherence to environmental and hazardous material handling regulations, making certified contractors the preferred choice for asset owners. These providers offer end-to-end services, including coating application, containment systems, and compliance management, reducing operational risk. Additionally, they play a critical role in condition-based maintenance programs, conducting inspections such as dry film thickness (DFT), adhesion testing, and corrosion assessment to optimize recoat cycles. This creates recurring revenue streams and long-term service contracts, reinforcing their leadership in the global MRO protective coatings market.

Competitive Landscape in the MRO Protective Coatings Market

AkzoNobel leads digital MRO coatings with predictive maintenance and surface-tolerant technologies

AkzoNobel, through its International® brand, remains a strategic leader in MRO protective coatings, particularly in marine and energy sectors. In 2026, the company expanded its Intershield® and Interzone® portfolios with surface-tolerant epoxy coatings capable of application on St 2/St 3 substrates, reducing the need for abrasive blasting during maintenance. Its Intertrac® HullMS digital platform enables predictive analytics for corrosion and fouling, allowing asset owners to shift from reactive to proactive maintenance strategies. AkzoNobel also enhanced its Interchar® intumescent coatings to reduce return-to-service time by up to 25%, minimizing operational downtime. With a 47% reduction in carbon emissions across its MRO production facilities, the company continues to align performance with sustainability objectives.

PPG strengthens infrastructure and aerospace MRO coatings with energy-efficient and corrosion-resistant systems

PPG Industries holds a strong position in infrastructure and aerospace MRO coatings, leveraging advanced chemistry and global distribution capabilities. Its Desothane® HS topcoats are widely used in aircraft maintenance, offering superior UV resistance and long-term color retention for aging fleets. Following the acquisition of Ozark Materials in 2026, PPG expanded its presence in bridge and rail maintenance, integrating specialized adhesion technologies into its portfolio. The company also introduced a low-bake clearcoat system that reduces CO₂ emissions by 16 kg per maintenance cycle. Its SIGMASHIELD™ coatings address corrosion under insulation (CUI), a major challenge in petrochemical facilities, reinforcing PPG’s leadership in high-performance industrial maintenance solutions.

Sherwin-Williams dominates North American MRO coatings with digital asset management and high-build systems

The Sherwin-Williams Company leads the North American MRO protective coatings market, with a projected 38.2% share driven by its extensive distribution network and digital tools. Its Macropoxy® 646 series remains an industry benchmark for surface-tolerant primers, offering high-build application and rapid recoat times. The company is transitioning toward high-solids and waterborne coatings to meet the 2026 VOC cap of 250 g/L under EPA and REACH regulations. Its Sher-Loram™ platform integrates Bluetooth-enabled dry-film thickness monitoring, enabling real-time tracking of coating condition across large infrastructure assets. Through its “Success by Design” platform, Sherwin-Williams provides automated coating specifications for municipal and industrial MRO applications.

Jotun advances smart MRO coatings with corrosion-detection technologies and robotic cleaning systems

Jotun is a key innovator in offshore and energy MRO coatings, particularly in regions such as the North Sea and Asia-Pacific. In 2026, the company introduced Smart Barrier coatings that use micro-sensor technologies or color-change indicators to detect early-stage corrosion, reducing inspection costs by up to 30%. Its Jotamastic 90 epoxy system is widely used for maintenance applications, offering flexibility across a wide temperature range and strong chemical resistance. Jotun has also expanded its presence in major MRO hubs such as Dubai and Singapore, targeting refurbishment of LNG carriers and offshore platforms. The introduction of the HullSkater robotic cleaning system further supports proactive maintenance by preventing biofouling before major recoating is required.

Hempel drives long-cycle MRO coatings with sustainability-linked performance solutions

Hempel A/S is positioned as an efficiency-focused leader in the MRO coatings market, particularly in marine and wind energy applications. Its Hempaguard® Ultima system enables extended service intervals of up to 10 years, effectively doubling traditional maintenance cycles for large vessels and reducing total lifecycle costs. The company reported an adjusted EBITDA margin of 18.2% in 2026, supported by strong demand for coatings that improve Carbon Intensity Indicator (CII) performance. Hempel is also a leader in offshore wind MRO coatings, providing solutions for turbine foundations exposed to extreme mechanical and environmental stress. Its EcoVadis Gold rating enhances its appeal to ESG-focused clients, positioning it as a preferred partner for sustainable infrastructure maintenance projects.

United States MRO Protective Coatings Market: Infrastructure Lifecycle Extension and PFAS-Free Innovation

The United States leads the MRO protective coatings market, driven by large-scale infrastructure renewal and a strong transition toward PFAS-free, environmentally compliant coating technologies. The $1.2 trillion Bipartisan Infrastructure Law is fueling demand for high-build epoxy mastic coatings, particularly in bridge repair and replacement programs, where coatings must perform effectively even on marginally prepared surfaces. This “life-extension” strategy is central to maintaining aging infrastructure while minimizing downtime and cost.

Regulatory pressure from the EPA and Department of Defense (DoD) is accelerating the phase-out of PFAS-based chemistries, pushing the adoption of non-fluorinated, low-friction protective coatings in aerospace MRO. Technological advancements include sensor-integrated smart coatings, which provide real-time data on corrosion rates and coating integrity, enabling predictive maintenance. Innovations such as ambient-cure, high-solid polyurethane systems are allowing rapid field repairs without external heating, especially in pipeline maintenance across the Gulf Coast. Strategic R&D investments by companies like PPG are further advancing self-healing coatings for defense applications, reinforcing the U.S. leadership in high-performance MRO coatings.

India MRO Protective Coatings Market: Naval Modernization and Infrastructure-Driven Growth

India is emerging as a strategic hub for MRO protective coatings, supported by rapid industrialization and government initiatives under “Aatmanirbhar Bharat”. Significant investments in the maritime sector, including the development of the Karwar Naval Hub, are driving demand for underwater-curing epoxy coatings for hull maintenance and naval asset protection. The modernization of India’s naval and industrial MRO ecosystem is positioning the country as a key player in Asia.

Infrastructure expansion across railways and energy sectors is also fueling growth. The adoption of robotic ultra-high pressure (UHP) water jetting combined with automated coating systems is improving efficiency in maintaining high-speed rail networks such as the Vande Bharat fleet. Innovations such as polyaspartic coatings for rapid-return-to-service applications are reducing downtime in critical infrastructure projects. Additionally, the expansion of offshore wind energy in coastal regions is increasing demand for C5-M rated anti-corrosion coatings, capable of withstanding harsh marine environments.

China MRO Protective Coatings Market: Smart Manufacturing and High-Speed Rail Maintenance Leadership

China’s MRO protective coatings market is evolving through industrial modernization and smart manufacturing integration, with a strong emphasis on low-VOC and environmentally sustainable coating systems. Government mandates under the “Blue Sky” Industrial Update (2026) require that a significant portion of infrastructure repair projects use waterborne or powder-based coatings, accelerating the shift toward eco-friendly technologies.

Technological advancements include the adoption of graphene-enhanced anti-corrosion coatings, particularly in power grid infrastructure, reducing maintenance frequency and extending asset life. The integration of AI-driven spray booth systems is enabling precise coating application with micron-level accuracy, especially in aerospace MRO operations. China’s leadership in high-speed rail infrastructure, including 600 km/h Maglev systems, is driving demand for coatings with extreme weather resistance and low friction properties. Investments in green MRO facilities and smart surface treatment zones are further strengthening China’s position in advanced protective coating technologies.

Germany leads the European MRO protective coatings market, driven by its commitment to sustainability, circular economy principles, and advanced coating technologies. The commercialization of bio-based epoxy resins, derived from renewable sources such as cashew nutshell liquid, is significantly reducing the carbon footprint of industrial maintenance coatings.

Government initiatives such as the Building Refurbishment Grant program are promoting the use of thermal-insulating and heat-reflective coatings, supporting energy efficiency targets for 2030. Technological advancements include the adoption of laser ablation surface preparation combined with solvent-free polyaspartic coatings, improving coating adhesion and durability. Germany is also investing in specialized coatings for hydrogen infrastructure, addressing challenges such as hydrogen embrittlement in pipelines. Strict compliance with REACH 2026 regulations is further driving the adoption of environmentally safe coating systems across marine and industrial MRO applications.

South Korea MRO Protective Coatings Market: Smart Shipbuilding and Advanced Urban Maintenance

South Korea is leveraging its expertise in shipbuilding and advanced materials engineering to become a key player in the MRO protective coatings market. The development of AI-optimized smart antifouling coatings is enabling dynamic adjustment of biocide release based on environmental conditions, enhancing performance for marine vessels operating in diverse climates.

Infrastructure investments are also driving growth, particularly through smart bridge maintenance programs, where advanced coatings extend asset lifespan and reduce maintenance costs. Innovations such as super-durable metallic powder coatings are being used for façade repairs in urban environments, eliminating color-matching challenges associated with traditional liquid coatings. Expansion of R&D facilities, including KCC Corporation’s Advanced Materials Center, is supporting the development of moisture-cure polyurethane coatings for emergency repairs in marine and industrial sectors. South Korea’s focus on cleanroom-grade coatings for semiconductor facilities further highlights its role in high-tech MRO applications.

Brazil MRO Protective Coatings Market: Mining, Offshore Energy, and Sustainable Maintenance Solutions

Brazil is emerging as a regional leader in MRO protective coatings, driven by strong demand from mining, offshore oil & gas, and agricultural infrastructure sectors. The use of abrasion-resistant ceramic-epoxy coatings in mining equipment is critical for maintaining performance in harsh operating conditions, particularly for iron ore transport systems.

Significant investments by global companies such as AkzoNobel are expanding production of high-solid, low-VOC coatings for offshore applications. Technological advancements such as cold-spray repair techniques are enabling safe and efficient maintenance of offshore platforms without the risks associated with high-temperature processes. Government initiatives like the BNDES Green Credit program are encouraging the adoption of waterborne coating technologies, aligning with sustainability goals. Additionally, the expansion of agro-industrial corridors is driving demand for chemical-resistant coatings in fertilizer storage and grain processing facilities, reinforcing Brazil’s position in the global MRO coatings market.

MRO Protective Coatings Market Report Scope

MRO Protective Coatings Market

Parameter

Details

Market Size (2025)

$10.3 Billion

Market Size (2032)

$15.2 Billion

Market Growth Rate

5.7%

Segments

By Chemistry (Epoxy, Polyurethane, Acrylic, Alkyd, Polyaspartic and Polyurea, Zinc-Rich Coatings, Fluoropolymers), By Product Technology (Solvent-borne, Water-borne, Powder Coatings, Aerosol-based Repair Coatings), By Function (Corrosion Resistance, Abrasion and Wear Resistance, Chemical and Asset Protection, Intumescent and Fire Protection, Low Friction, Thermal Barrier, Tank Linings and Internal Pipe Coatings), By End-Use Industry (Marine, Infrastructure and Construction, Industrial Plants and Manufacturing, Power Generation, Aerospace and Defense), By Form (Field-Applied Coatings, Shop-Applied, Touch-up Kits and Specialty Applicators), By Substrate (Metals, Concrete and Masonry, Composites and Plastics), By Sales Channel (Direct Sales, Specialty Industrial MRO Distributors, Professional Contract Service Providers)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun A/S, Hempel A/S, RPM International Inc., Sika AG, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Belzona International Ltd., Henkel AG and Co. KGaA, Chugoku Marine Paints, Ltd., BASF SE, Weilburger Coatings GmbH

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

MRO Protective Coatings Market Segmentation

By Chemistry

Epoxy

Polyurethane

Acrylic

Alkyd

Polyaspartic and Polyurea

Zinc-Rich Coatings

Fluoropolymers

By Product Technology

Solvent-borne

Water-borne

Powder Coatings

Aerosol-based Repair Coatings

By Function

Corrosion Resistance

Abrasion and Wear Resistance

Chemical and Asset Protection

Intumescent and Fire Protection

Low Friction

Thermal Barrier

Tank Linings and Internal Pipe Coatings

By End-Use Industry

Marine

Infrastructure and Construction

Industrial Plants and Manufacturing

Power Generation

Aerospace and Defense

By Form

Field-Applied Coatings

Shop-Applied

Touch-up Kits and Specialty Applicators

By Substrate

Metals

Concrete and Masonry

Composites and Plastics

By Sales Channel

Direct Sales

Specialty Industrial MRO Distributors

Professional Contract Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in MRO Protective Coatings Industry

The Sherwin-Williams Company

PPG Industries, Inc.

Akzo Nobel N.V.

Jotun A/S

Hempel A/S

RPM International Inc.

Sika AG

Axalta Coating Systems Ltd.

Kansai Paint Co., Ltd.

Nippon Paint Holdings Co., Ltd.

Belzona International Ltd.

Henkel AG & Co. KGaA

Chugoku Marine Paints, Ltd.

BASF SE

Weilburger Coatings GmbH

*- List not Exhaustive

Table of Contents: MRO Protective Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. MRO Protective Coatings Market Landscape and Outlook (2025–2034)

2.1. Introduction to the MRO Protective Coatings Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the MRO Protective Coatings Market

3.1. Trend: High-Solids and Single-Coat Systems Reducing Turnaround Time in Commercial Aviation MRO

3.2. Trend: Ultra-High Solids Primers Enhancing Throughput and Compliance in Military MRO Operations

3.3. Opportunity: Ford-Class Aircraft Carrier Modernization Driving Demand for High-Performance Marine-Aviation Coatings

3.4. Opportunity: EU Rail Maintenance Directive Creating Standardized Demand for High-Durability MRO Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Product Innovation

4.3. Sustainability and ESG Strategies

4.4. Capacity Expansion and Geographic Expansion

5. Market Share and Segmentation Insights: MRO Protective Coatings Market

5.1. By Chemistry

5.1.1. Epoxy

5.1.2. Polyurethane

5.1.3. Acrylic

5.1.4. Alkyd

5.1.5. Polyaspartic and Polyurea

5.1.6. Zinc-Rich Coatings

5.1.7. Fluoropolymers

5.2. By Product Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder Coatings

5.2.4. Aerosol-based Repair Coatings

5.3. By Function

5.3.1. Corrosion Resistance

5.3.2. Abrasion and Wear Resistance

5.3.3. Chemical and Asset Protection

5.3.4. Intumescent and Fire Protection

5.3.5. Low Friction

5.3.6. Thermal Barrier

5.3.7. Tank Linings and Internal Pipe Coatings

5.4. By End-Use Industry

5.4.1. Marine

5.4.2. Infrastructure and Construction

5.4.3. Industrial Plants and Manufacturing

5.4.4. Power Generation

5.4.5. Aerospace and Defense

5.5. By Form

5.5.1. Field-Applied Coatings

5.5.2. Shop-Applied

5.5.3. Touch-up Kits and Specialty Applicators

5.6. By Substrate

5.6.1. Metals

5.6.2. Concrete and Masonry

5.6.3. Composites and Plastics

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Industrial MRO Distributors

5.7.3. Professional Contract Service Providers

6. Country Analysis and Outlook of MRO Protective Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. UAE

6.20. Middle East and Africa

7. MRO Protective Coatings Market Size Outlook by Region (2025–2034)

7.1. North America MRO Protective Coatings Market Size Outlook to 2034

7.1.1. By Chemistry

7.1.2. By Product Technology

7.1.3. By Function

7.1.4. By End-Use Industry

7.1.5. By Form

7.1.6. By Substrate

7.1.7. By Sales Channel

7.2. Europe MRO Protective Coatings Market Size Outlook to 2034

7.2.1. By Chemistry

7.2.2. By Product Technology

7.2.3. By Function

7.2.4. By End-Use Industry

7.2.5. By Form

7.2.6. By Substrate

7.2.7. By Sales Channel

7.3. Asia Pacific MRO Protective Coatings Market Size Outlook to 2034

7.3.1. By Chemistry

7.3.2. By Product Technology

7.3.3. By Function

7.3.4. By End-Use Industry

7.3.5. By Form

7.3.6. By Substrate

7.3.7. By Sales Channel

7.4. South and Central America MRO Protective Coatings Market Size Outlook to 2034

7.4.1. By Chemistry

7.4.2. By Product Technology

7.4.3. By Function

7.4.4. By End-Use Industry

7.4.5. By Form

7.4.6. By Substrate

7.4.7. By Sales Channel

7.5. Middle East and Africa MRO Protective Coatings Market Size Outlook to 2034

7.5.1. By Chemistry

7.5.2. By Product Technology

7.5.3. By Function

7.5.4. By End-Use Industry

7.5.5. By Form

7.5.6. By Substrate

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the MRO Protective Coatings Market

8.1. The Sherwin-Williams Company

8.2. PPG Industries, Inc.

8.3. Akzo Nobel N.V.

8.4. Jotun A/S

8.5. Hempel A/S

8.6. RPM International Inc.

8.7. Sika AG

8.8. Axalta Coating Systems Ltd.

8.9. Kansai Paint Co., Ltd.

8.10. Nippon Paint Holdings Co., Ltd.

8.11. Belzona International Ltd.

8.12. Henkel AG and Co. KGaA

8.13. Chugoku Marine Paints, Ltd.

8.14. BASF SE

8.15. Weilburger Coatings GmbH

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

MRO Protective Coatings Market Segmentation

By Chemistry

Epoxy

Polyurethane

Acrylic

Alkyd

Polyaspartic and Polyurea

Zinc-Rich Coatings

Fluoropolymers

By Product Technology

Solvent-borne

Water-borne

Powder Coatings

Aerosol-based Repair Coatings

By Function

Corrosion Resistance

Abrasion and Wear Resistance

Chemical and Asset Protection

Intumescent and Fire Protection

Low Friction

Thermal Barrier

Tank Linings and Internal Pipe Coatings

By End-Use Industry

Marine

Infrastructure and Construction

Industrial Plants and Manufacturing

Power Generation

Aerospace and Defense

By Form

Field-Applied Coatings

Shop-Applied

Touch-up Kits and Specialty Applicators

By Substrate

Metals

Concrete and Masonry

Composites and Plastics

By Sales Channel

Direct Sales

Specialty Industrial MRO Distributors

Professional Contract Service Providers

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global MRO protective coatings market was valued at $10.3 billion in 2025 and is projected to reach $15.2 billion by 2032, expanding at a CAGR of 5.7%. Market growth is being driven by increasing demand for corrosion-resistant maintenance coatings, aerospace MRO coatings, offshore protective systems, infrastructure rehabilitation coatings, and industrial asset lifecycle extension technologies across aviation, marine, energy, transportation, and manufacturing sectors.

Advanced high-solids and single-coat protective systems are significantly reducing aircraft maintenance turnaround time by 30% to 40% while improving operational efficiency and lowering lifecycle emissions. Ultra-high solids (UHS) primers with VOC levels below 250 g/L are enabling faster application cycles, fewer coating passes, and improved hangar throughput in military depots. These systems also provide strong corrosion resistance exceeding 2,000 hours of salt spray exposure, making them critical for next-generation aviation maintenance programs.

The integration of AI-driven corrosion monitoring, sensor-enabled coatings, and predictive maintenance platforms is transforming asset management strategies across industrial infrastructure. Smart coatings with embedded micro-sensors and visual corrosion indicators allow operators to detect coating degradation in real time, optimize maintenance schedules, reduce inspection costs, and minimize unplanned downtime. These technologies are increasingly being deployed in offshore platforms, bridges, pipelines, aircraft fleets, and renewable energy infrastructure.

North America and Europe lead in advanced aerospace MRO technologies, predictive maintenance integration, and sustainable coating innovation, while Asia-Pacific and the Middle East are emerging as major growth regions due to expanding aviation hubs, offshore energy projects, and infrastructure modernization programs. Strong demand is also emerging from offshore wind farms, naval modernization, rail maintenance, hydrogen infrastructure, and industrial refurbishment projects requiring long-term corrosion protection and rapid return-to-service coatings.

Major companies operating in the MRO protective coatings industry include The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun A/S, Hempel A/S, RPM International Inc., Sika AG, and Axalta Coating Systems Ltd.. These companies are investing heavily in predictive maintenance platforms, smart corrosion monitoring technologies, high-solids coating systems, aerospace MRO infrastructure, low-VOC formulations, and digital asset management solutions to strengthen their global market positions.