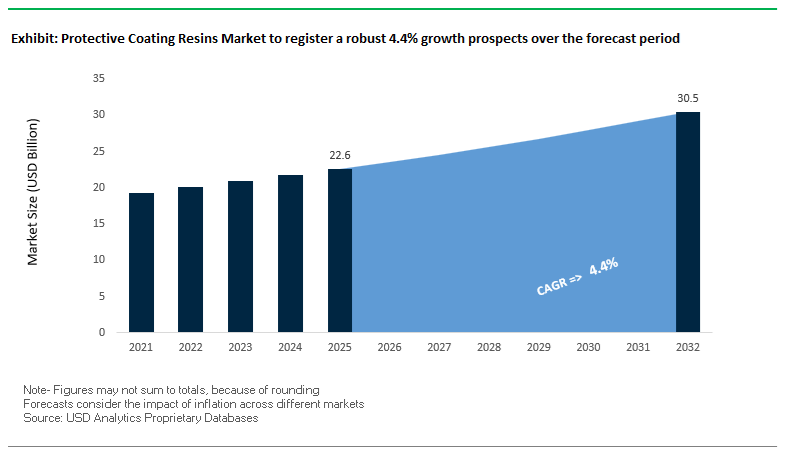

The global Protective Coating Resins Market was valued at $22.6 billion in 2025 and is projected to grow at a CAGR of 4.4% through 2032, reaching $30.6 billion by 2032. This growth is driven by rising demand across marine, energy, infrastructure, automotive, and industrial sectors, where resins form the core functional backbone of protective coating systems, delivering corrosion resistance, chemical durability, adhesion, and weatherability.

Protective coating resins—including epoxy, polyurethane, acrylic, alkyd, and silicone-based systems—are essential in enabling coatings to withstand extreme environmental conditions, such as offshore exposure, chemical processing environments, and high-temperature industrial operations. Their role is particularly critical in energy infrastructure, shipbuilding, wind turbines, and pipelines, where coating failure can result in significant operational and financial risks.

A key structural driver is the global expansion of energy and infrastructure projects, including offshore oil & gas, LNG terminals, renewable energy installations, and transportation networks. These applications require high-performance resin systems capable of maintaining long-term integrity under thermal cycling, UV exposure, and corrosive environments.

Sustainability is also reshaping the resin landscape. The market is witnessing a strong transition toward bio-based, recycled, and low-carbon resin systems, alongside innovations aimed at eliminating hazardous substances such as PFAS. This shift is driven by regulatory pressures, corporate decarbonization commitments, and the need for environmentally compliant high-performance materials.

Market Analysis: Bio-Based Resin Innovation, PFAS-Free Solutions, and Energy Efficiency Driving Market Evolution

Recent developments in the Protective Coating Resins Market highlight a convergence of sustainability-driven innovation, advanced material engineering, and strategic industry realignment. In March 2025, Westlake Epoxy launched the EpoVIVE portfolio, featuring sustainable epoxy and phenolic resins designed for high-performance applications in marine, aerospace, and wind energy sectors. This initiative emphasizes value-chain collaboration to reduce environmental impact without compromising durability.

Regulatory compliance is accelerating the shift toward safer chemistries. Evonik’s Protectosil ECO-TRETE® (March 2026) introduces a PFAS-free protective resin solution, addressing growing restrictions on fluorinated substances in architectural and infrastructure coatings. This development reflects a broader industry move toward responsible and compliant coating technologies.

Marine and energy applications continue to drive innovation. Hempel’s Hempaguard NB resin technology (March 2026) utilizes a silicone-based fouling-release system, contributing to improved vessel efficiency and reduced emissions. Supporting this trend, Jotun reported that its advanced resin systems helped avoid 11.8 million tonnes of CO₂ emissions in 2025, demonstrating the significant impact of resin performance on fuel efficiency and sustainability outcomes.

Collaborative initiatives are advancing low-carbon solutions. The AkzoNobel–Arkema–BASF partnership (September 2025) focuses on developing bio-based polyester resins for powder coatings, achieving up to 20% reduction in CO₂ intensity while maintaining performance standards. Additionally, Allnex’s introduction of rPET-based resins and bio-based polyurethane dispersions highlights the growing adoption of recycled and renewable feedstocks in protective coatings.

Innovation is also expanding into new functional applications. AkzoNobel’s solar-absorbing wall resin technology integrates protective coatings into energy-generating building systems, while its bio-based interior resin for KIA demonstrates the scalability of renewable materials across industrial applications.

Market dynamics are being influenced by supply-side adjustments. Olin Corporation’s strategic pivot (February 2026) toward higher-value protective coating applications reflects ongoing challenges in commodity epoxy markets, with companies increasingly focusing on specialty, performance-driven segments to maintain profitability.

The protective coating resins market is undergoing a significant transformation as waterborne epoxy resins evolve from compliance-driven alternatives into high-performance corrosion protection systems. Regulatory pressure from the U.S. Environmental Protection Agency NESHAP amendments and the European Chemicals Agency framework is accelerating the shift toward ultra-low VOC resin chemistries across North America and Europe.

Modern waterborne epoxy resins developed for 2026 applications demonstrate VOC levels in the range of 50–100 g/L, representing a 75% to 80% reduction compared to conventional solvent-borne epoxy systems that typically operate between 350 and 450 g/L. Despite this substantial reduction in emissions, performance metrics have reached parity with traditional formulations. These resins consistently achieve 2,000-hour salt spray resistance, making them suitable for demanding industrial environments including C4 and C5 atmospheric corrosivity categories.

Advancements in electrochemical performance are particularly notable. Electrochemical Impedance Spectroscopy testing indicates that next-generation waterborne epoxy resins deliver a reduction in corrosion current density exceeding 60% compared to early-stage waterborne technologies from the early 2020s. This improvement reflects enhanced barrier properties and reduced ionic permeability, enabling their deployment in aggressive marine and industrial exposure conditions.

Adhesion performance has also reached critical thresholds required for infrastructure and heavy-duty applications. Technical benchmarks for 2026 indicate pull-off adhesion strengths between 18 and 22 MPa on grit-blasted steel surfaces under ASTM D4541 testing conditions. This level of adhesion matches solvent-based bisphenol-A epoxy systems, removing one of the final barriers to widespread adoption of waterborne epoxy resins in protective coatings.

Decarbonization pressures across marine and infrastructure sectors are driving a shift toward low-embodied-carbon polyester resins. Regulatory frameworks such as maritime decarbonization mandates and carbon border mechanisms are transforming procurement criteria, making carbon footprint a critical parameter alongside performance in resin selection.

In the marine coatings sector, decarbonization is now directly impacting operational cost structures. Industry surveys conducted in 2026 indicate that more than 90% of maritime executives consider emissions reduction targets as a core financial factor. This is accelerating the adoption of polyester resins with verified production-phase carbon reductions of 20% to 30%, particularly in shipbuilding, offshore platforms, and marine maintenance coatings.

In parallel, infrastructure projects in North America are increasingly governed by “Buy Clean” procurement policies that require Environmental Product Declarations for coating materials. Polyester resins incorporating 15% to 25% recycled PET content are gaining preferential treatment, often receiving a 10% to 15% procurement advantage in publicly funded projects such as bridges, tunnels, and transportation networks. This is incentivizing resin manufacturers to integrate recycled feedstocks and optimize lifecycle emissions.

The convergence of regulatory mandates, procurement preferences, and carbon accounting frameworks is driving the emergence of traceable, low-carbon resin supply chains. Resin producers that can validate reduced embodied carbon through certified documentation are gaining a competitive edge in both domestic and export markets, particularly in regions with stringent environmental compliance requirements.

Market Opportunity: Graphene-Enhanced Epoxy Resins Unlocking Next-Generation Barrier Performance in Offshore Oil and Gas

The integration of functionalized graphene oxide into epoxy resin systems represents a high-impact innovation opportunity within the oil and gas coatings segment. As of 2026, graphene-enhanced epoxy resins have transitioned from laboratory-scale validation to real-world deployment in offshore environments, where extreme corrosion resistance is required.

Material science advancements demonstrate that incorporating approximately 0.4% reduced graphene oxide by weight can reduce coating porosity from 1.54% to 0.33%, effectively creating a highly impermeable barrier against corrosive species such as chloride ions and oxygen. This tortuous path mechanism significantly enhances the durability of protective coatings in high-salinity environments.

Field performance data from offshore platforms shows that graphene-modified epoxy coatings maintain an impedance modulus exceeding 10⁹ ohm-centimeter squared after 45 days of continuous immersion in brine solutions. This represents approximately double the functional lifespan compared to conventional zinc-rich epoxy primers, reducing maintenance frequency and associated operational downtime.

In addition to performance gains, graphene-enhanced resins enable coating weight optimization. Due to superior barrier efficiency, these systems allow for a 15% to 20% reduction in dry film thickness without compromising protection levels. This is particularly valuable in floating production storage and offloading units, where weight reduction directly impacts structural efficiency and fuel consumption.

Market Opportunity: Bio-Renewable Acrylic Resins from Lignin Creating Circular Economy Opportunities in Coatings

The development of bio-renewable acrylic resins derived from lignin is emerging as a strategic opportunity in regions with strong pulp and paper industries, particularly in Scandinavia and Canada. Lignin, a natural byproduct of wood processing, is increasingly being utilized as a feedstock for high-performance coating resins, aligning with circular economy and sustainability objectives.

Lignin-based acrylic resins offer inherent UV resistance advantages due to their aromatic polymer structure. Accelerated weathering tests conducted in 2026 indicate a 30% reduction in gloss loss over 3,000 hours of QUV-B exposure compared to conventional acrylic systems. This makes them highly suitable for exterior coatings applications where long-term aesthetic retention is critical.

Market dynamics in Northern Europe indicate that coatings formulated with more than 30% renewable carbon content, verified through ASTM D6866 testing, can command a price premium of approximately 12%. These materials also qualify for regional tax incentives linked to circular bioeconomy initiatives, enhancing their commercial attractiveness.

Supply chain developments are reinforcing this opportunity. Large-scale pulp mills in regions such as Ontario and Sweden are transitioning into integrated biorefineries, increasing lignin recovery yields by approximately 25% as of 2026. This provides a stable and cost-effective supply of bio-based precursors for resin manufacturers, supporting scalable production of sustainable protective coating resins and strengthening the linkage between forestry byproducts and advanced materials innovation.

Protective Coating Resins Market Share and Segmentation Insights: Spray Application Dominance and Direct Procurement Driving Industrial Demand

By Application Method: Spray Coating Leads with Versatility and On-Site Infrastructure Applicability

The spray coating segment dominated the protective coating resins market with a 58.6% share in 2025, driven by its unmatched versatility, uniform coverage, and efficiency across complex industrial applications. Advanced spray techniques such as airless spray, HVLP (high-volume low-pressure), and electrostatic spraying enable precise application of protective resins on tanks, pipelines, structural steel, bridges, and marine vessels, ensuring consistent film thickness and superior coating performance. A key advantage is the high transfer efficiency and reduced material wastage, which enhances cost-effectiveness in large-scale projects. Additionally, spray coating systems offer portable field application capabilities, allowing coatings to be applied directly on-site for infrastructure assets such as offshore platforms, storage tanks, and long-distance pipelines, where alternative methods like dipping or coil coating are impractical. This combination of application flexibility, operational efficiency, and scalability firmly establishes spray coating as the preferred method in the global protective coating resins market.

By Sales Channel: Direct Sales Channel Dominates with Custom Resin Development and Technical Collaboration

The direct sales segment accounted for a leading 47.8% share of the protective coating resins market in 2025, reflecting the growing need for customized resin formulations and close technical collaboration between suppliers and coating manufacturers. Large-scale buyers, including industrial coating producers and marine coating companies, work directly with resin manufacturers to develop formulations tailored for specific performance requirements such as corrosion resistance, curing speed, and weatherability in harsh environments. This direct engagement ensures faster innovation cycles and precise alignment with end-use applications. Furthermore, high-volume procurement enables buyers to secure competitive pricing, batch-to-batch consistency, and reliable supply chains, which are critical for large infrastructure and industrial projects. Direct relationships also provide on-site technical support and troubleshooting assistance, enhancing application performance and reducing operational risks. As demand rises for high-performance protective resins in oil & gas, marine, and infrastructure sectors, the direct sales channel continues to drive market growth and efficiency.

Competitive Landscape of the Protective Coating Resins Market

BASF Leads Market with Integrated Resin Production and Advanced Color Science

BASF SE remains the “Chemical Architect” of the protective coating resins market, leveraging its vertically integrated Verbund system to supply both raw materials and finished solutions. Its 2025–2026 “Driving the Proxy” innovation showcases advanced polyurethane resin systems with interference pigments that deliver multi-dimensional surface aesthetics for next-generation vehicles. The company has strengthened its supply chain through full-scale production at its Zhanjiang site, ensuring localized availability of isocyanates and polyols. Its RELIANCE® and RELEEST® series offer low-VOC epoxy resins with high chemical resistance, making them ideal for industrial and energy infrastructure applications.

Covestro Advances Circular Polyurethane Resins with Strong Sustainability Focus

Covestro AG is a leading innovator in the protective coating resins market, focusing on circular polymer solutions and sustainability. The company reported €12.9 billion in sales and is investing heavily in mass-balanced polyurethane resins that reduce Scope 3 emissions by up to 40%. Its INSQIN® waterborne PU technology enables high-performance coatings with low VOC emissions, particularly for automotive interiors. Covestro also leads in infrastructure applications with Platilon® TPU films used in trenchless pipe repair systems, enhancing durability while minimizing environmental impact.

allnex Drives Green Chemistry with Recycled and Non-Isocyanate Resin Technologies

allnex is a key player in the protective coating resins market, specializing in sustainable and high-performance resin solutions. Its CRYLCOAT® OCEAN polyester resin incorporates up to 25% recycled PET, supporting circular economy initiatives in industrial coatings. In 2026, the company introduced the ACURE® AQ platform, a waterborne non-isocyanate 2K system that offers rapid curing and improved safety compared to traditional urethanes. allnex is also advancing ultra-low VOC technologies through its SETAQUA® range, reinforcing its leadership in eco-friendly resin innovation.

Evonik Strengthens Specialty Resin Market with Crosslinker and Additive Integration

Evonik Industries AG plays a critical role in the protective coating resins market, focusing on high-value specialty chemicals and crosslinker technologies. The company is targeting strong EBITDA growth while shifting toward high-margin specialty resins. Its crosslinkers and oil additives are essential for high-performance plastics, membranes, and 3D printing applications, which are increasingly integrated into protective coatings. Evonik’s strong presence in the renewable energy sector, including wind turbine and solar applications, highlights its leadership in durable and sustainable resin solutions.

Dow Expands Resin Applications with Advanced Silicone and Acrylic Technologies

Dow Inc. leverages its materials science expertise to drive innovation in the protective coating resins market. Its DOWSIL™ and ACUDYNE™ technologies are being adapted to create breathable, water-repellent, and humidity-resistant coatings for both industrial and consumer applications. Dow is focusing on scalable solutions for the Asia-Pacific infrastructure market, aligning with the region’s rapid growth. Its strong presence in silicone and acrylic resin platforms positions it as a key supplier for high-performance and sustainable coatings.

Huntsman Leads High-Durability Resin Development for Aerospace and EV Applications

Huntsman Corporation is a leader in high-performance polyurethane resins, particularly for aerospace, defense, and electric vehicle applications. In 2026, the company partnered with advanced research groups to develop resins for anti-ballistic armor, offering exceptional thermal stability and structural integrity. Huntsman is also a major supplier of polyurethane systems for EV batteries, enhancing safety and performance under extreme conditions. Its alignment with global decarbonization initiatives and focus on energy-efficient building materials reinforce its position in next-generation protective resin technologies.

China Protective Coating Resins Market: High-Volume Transformation and Waterborne Shift

China leads the global protective coating resins market, transitioning rapidly from conventional solvent-based systems to high-value, environmentally compliant formulations. Under the 2025–2026 “Green Industry” initiative, strict VOC limits are pushing manufacturers toward waterborne epoxy resins and polyurethane dispersions (PUDs), accelerating the solvent-to-water (S2W) shift.

Technological advancements include ultra-low temperature curing resins (80–100°C), significantly reducing energy consumption in industrial coating processes. China is also dominating the EV sector with flame-retardant, high-dielectric epoxy resins used in battery packs. Strategic investments, such as Wanhua Chemical’s expansion in isocyanate production, are strengthening supply chains for high-performance polyurethane coatings. Additionally, innovations like graphene-embedded anticorrosive resins and silicone-modified acrylics for UHV grids are enhancing durability and performance across infrastructure and marine applications.

India Protective Coating Resins Market: Infrastructure Growth and Renewable Energy Expansion

India is emerging as a high-growth market in the protective coating resins industry, driven by infrastructure development and manufacturing localization. Government initiatives such as the PM Gati Shakti Master Plan are increasing demand for epoxy-zinc phosphate resins in large-scale infrastructure projects.

The renewable energy sector is also fueling growth, with rising demand for vinyl ester resins in offshore wind turbine blade protection. Investments by domestic leaders like Asian Paints and Berger are expanding production capacity for acrylic and polyester resins. Technological innovation includes the use of nanocoating additives for self-cleaning and antimicrobial properties, while regulatory pressure from the CPCB is accelerating the transition to waterborne systems. Additionally, the automotive sector is adopting advanced polyester resins to improve finish quality and durability.

United States Protective Coating Resins Market: PFAS-Free Innovation and Reshoring Momentum

The U.S. protective coating resins market is defined by regulatory transformation, infrastructure investment, and reshoring of manufacturing. The enforcement of PFAS-free mandates (2025–2026) is driving a complete redesign of fluoropolymer-based resins, pushing innovation toward safer alternatives.

Infrastructure investments under the Bipartisan Infrastructure Law are boosting demand for moisture-cured urethane (MCU) resins in bridge and transportation projects. The market is also seeing strong growth in UV-curable resins, enabling fast processing with minimal energy consumption. Sustainability trends are driving the adoption of bio-attributed resins, particularly in aerospace and automotive sectors. Additionally, investments in battery manufacturing are increasing demand for specialized coating resins used in lithium-ion battery production, reinforcing the U.S. position in advanced materials innovation.

Germany Protective Coating Resins Market: Bio-Based Innovation and Industry 4.0 Integration

Germany is at the forefront of sustainable and high-performance resin technologies, emphasizing bio-based materials and advanced manufacturing integration. Innovations include the development of bio-based epoxy resins derived from lignin and cashew nut shell liquid (CNSL), achieving high renewable content while maintaining performance.

The country is also advancing self-healing resin systems using micro-encapsulation, improving durability in industrial applications. Government support for green steel initiatives is driving demand for low-carbon resin systems, while compliance with EU REACH regulations is encouraging the development of biodegradable coatings. Digitalization through AI-driven resin batching is reducing waste and improving efficiency, positioning Germany as a leader in precision and sustainable coating technologies.

South Korea Protective Coating Resins Market: Maritime Leadership and Electronics Innovation

South Korea remains a global leader in marine-grade and electronics-focused coating resins, supported by strong shipbuilding and semiconductor industries. The country is standardizing the use of zinc silicate and antifouling resins in LNG carrier construction, ensuring durability and environmental compliance.

In electronics, South Korea dominates the use of EMI/RFI shielding resins for 5G devices and advanced consumer electronics. Investments in high-solids polyurethane resin production are strengthening export capabilities, while innovations in fouling-release silicone-hydrogel resins are improving marine performance without harmful biocides. Regulatory updates under K-REACH are also driving improvements in chemical safety and transparency.

Vietnam Protective Coating Resins Market: Manufacturing Expansion and Clean Production

Vietnam is rapidly emerging as a key player in the protective coating resins market, driven by foreign investment and industrial expansion. The influx of global OEMs is increasing demand for ESD resins used in electronics manufacturing, while government regulations are promoting the adoption of waterborne acrylic resins to reduce VOC emissions.

Record levels of foreign direct investment are supporting the development of industrial parks that require marine-grade protective resins for structural steel. Innovations in UV-LED curing technologies are enabling faster production cycles, particularly in furniture manufacturing. Additionally, urban housing demand is driving the use of elastomeric acrylic resins for waterproofing applications, strengthening Vietnam’s role as a manufacturing hub.

Brazil Protective Coating Resins Market: Agribusiness Demand and Industrial Applications

Brazil’s protective coating resins market is closely linked to its leadership in agriculture, mining, and offshore oil production. High demand exists for abrasion-resistant epoxy-novolac resins used in mining equipment and grain storage systems.

Government initiatives such as the Nova Indústria Brasil (NIB) plan are supporting investments in energy-efficient resin technologies, while environmental regulations are encouraging the shift to water-based systems. Innovations include ZAM-compatible resins for agricultural machinery, significantly improving corrosion resistance and lifespan. Additionally, demand from offshore oil and gas projects is driving the use of fusion-bonded epoxy (FBE) resins for deepwater pipelines, reinforcing Brazil’s position in heavy-duty industrial applications.

Protective Coating Resins Market Report Scope

Protective Coating Resins Market

Parameter

Details

Market Size (2025)

$22.6 Billion

Market Size (2032)

$30.6 Billion

Market Growth Rate

4.4%

Segments

By Resin (Epoxy, Polyurethane, Acrylic, Alkyd, Vinyl Ester and Vinyl, Polyester, Fluoropolymer, Polysiloxane, Bio-based), By Technology (Solvent-borne, Water-borne, Powder-based, 100% Solids, Radiation-Cured), By Substrate Compatibility (Metals, Concrete and Masonry, Plastics and Composites, Wood), By End-Use Industry (Infrastructure and Construction, Oil and Gas, Power Generation, Marine, Industrial Machinery and Equipment, Automotive and Transportation, Mining and Metal Processing, Aerospace and Defense), By Application Method (Spray Coating, Brush and Roller, Dipping and Electrocoating, Coil Coating), By Functional Property (Anti-Corrosion, Chemical and Acid Resistance, Thermal and Fire Resistance, Abrasion and Impact Resistance, UV and Weathering Resistance), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Professional Contractor Supply Channels)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

BASF SE, Covestro AG, Arkema S.A., allnex GmbH, Dow Chemical Company, Hexion Inc., Huntsman Corporation, DIC Corporation, Evonik Industries AG, Solvay S.A., Aditya Birla Chemicals, Daikin Industries, Ltd., Synthomer plc, Shin-Etsu Chemical Co., Ltd., Olin Corporation

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Protective Coating Resins Market Segmentation

By Resin

Epoxy

Polyurethane

Acrylic

Alkyd

Vinyl Ester and Vinyl

Polyester

Fluoropolymer

Polysiloxane

Bio-based

By Technology

Solvent-borne

Water-borne

Powder-based

100% Solids

Radiation-Cured

By Substrate Compatibility

Metals

Concrete and Masonry

Plastics and Composites

Wood

By End-Use Industry

Infrastructure and Construction

Oil and Gas

Power Generation

Marine

Industrial Machinery and Equipment

Automotive and Transportation

Mining and Metal Processing

Aerospace and Defense

By Application Method

Spray Coating

Brush and Roller

Dipping and Electrocoating

Coil Coating

By Functional Property

Anti-Corrosion

Chemical and Acid Resistance

Thermal and Fire Resistance

Abrasion and Impact Resistance

UV and Weathering Resistance

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Professional Contractor Supply Channels

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Protective Coating Resins Industry

BASF SE

Covestro AG

Arkema S.A.

Allnex GMBH

Dow Chemical Company

Hexion Inc.

Huntsman Corporation

DIC Corporation

Evonik Industries AG

Solvay S.A.

Aditya Birla Chemicals

Daikin Industries, Ltd.

Synthomer PLC

Shin-Etsu Chemical Co., Ltd.

Olin Corporation

*- List not Exhaustive

Table of Contents: Protective Coating Resins Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Protective Coating Resins Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Protective Coating Resins Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Dynamics and Growth Drivers

2.4. Regulatory and Sustainability Landscape

2.5. Strategic Industry Developments and Future Outlook

3. Innovations Reshaping the Protective Coating Resins Market

3.1. Trend: Ultra-Low VOC Waterborne Epoxy Resins Advancing High-Performance Corrosion Protection Standards

3.2. Trend: Low-Carbon Polyester Resin Supply Chains Reshaping Marine and Infrastructure Coatings

3.3. Opportunity: Graphene-Enhanced Epoxy Resins Unlocking Next-Generation Barrier Performance in Offshore Oil and Gas

3.4. Opportunity: Bio-Renewable Acrylic Resins from Lignin Creating Circular Economy Opportunities in Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Capacity Expansion and Regional Growth

5. Market Share and Segmentation Insights: Protective Coating Resins Market

5.1. By Resin

5.1.1. Epoxy

5.1.2. Polyurethane

5.1.3. Acrylic

5.1.4. Alkyd

5.1.5. Vinyl Ester and Vinyl

5.1.6. Polyester

5.1.7. Fluoropolymer

5.1.8. Polysiloxane

5.1.9. Bio-based

5.2. By Technology

5.2.1. Solvent-borne

5.2.2. Water-borne

5.2.3. Powder-based

5.2.4. 100% Solids

5.2.5. Radiation-Cured

5.3. By Substrate Compatibility

5.3.1. Metals

5.3.2. Concrete and Masonry

5.3.3. Plastics and Composites

5.3.4. Wood

5.4. By End-Use Industry

5.4.1. Infrastructure and Construction

5.4.2. Oil and Gas

5.4.3. Power Generation

5.4.4. Marine

5.4.5. Industrial Machinery and Equipment

5.4.6. Automotive and Transportation

5.4.7. Mining and Metal Processing

5.4.8. Aerospace and Defense

5.5. By Application Method

5.5.1. Spray Coating

5.5.2. Brush and Roller

5.5.3. Dipping and Electrocoating

5.5.4. Coil Coating

5.6. By Functional Property

5.6.1. Anti-Corrosion

5.6.2. Chemical and Acid Resistance

5.6.3. Thermal and Fire Resistance

5.6.4. Abrasion and Impact Resistance

5.6.5. UV and Weathering Resistance

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Chemical Distributors

5.7.3. Professional Contractor Supply Channels

6. Country Analysis and Outlook of Protective Coating Resins Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. Africa

7. Protective Coating Resins Market Size Outlook by Region (2025–2034)

7.1. North America Protective Coating Resins Market Size Outlook to 2034

7.1.1. By Resin

7.1.2. By Technology

7.1.3. By Substrate Compatibility

7.1.4. By End-Use Industry

7.1.5. By Application Method

7.1.6. By Functional Property

7.1.7. By Sales Channel

7.2. Europe Protective Coating Resins Market Size Outlook to 2034

7.2.1. By Resin

7.2.2. By Technology

7.2.3. By Substrate Compatibility

7.2.4. By End-Use Industry

7.2.5. By Application Method

7.2.6. By Functional Property

7.2.7. By Sales Channel

7.3. Asia Pacific Protective Coating Resins Market Size Outlook to 2034

7.3.1. By Resin

7.3.2. By Technology

7.3.3. By Substrate Compatibility

7.3.4. By End-Use Industry

7.3.5. By Application Method

7.3.6. By Functional Property

7.3.7. By Sales Channel

7.4. South America Protective Coating Resins Market Size Outlook to 2034

7.4.1. By Resin

7.4.2. By Technology

7.4.3. By Substrate Compatibility

7.4.4. By End-Use Industry

7.4.5. By Application Method

7.4.6. By Functional Property

7.4.7. By Sales Channel

7.5. Middle East and Africa Protective Coating Resins Market Size Outlook to 2034

7.5.1. By Resin

7.5.2. By Technology

7.5.3. By Substrate Compatibility

7.5.4. By End-Use Industry

7.5.5. By Application Method

7.5.6. By Functional Property

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Protective Coating Resins Market

8.1. BASF SE

8.2. Covestro AG

8.3. Arkema S.A.

8.4. allnex GmbH

8.5. Dow Chemical Company

8.6. Hexion Inc.

8.7. Huntsman Corporation

8.8. DIC Corporation

8.9. Evonik Industries AG

8.10. Solvay S.A.

8.11. Aditya Birla Chemicals

8.12. Daikin Industries, Ltd.

8.13. Synthomer plc

8.14. Shin-Etsu Chemical Co., Ltd.

8.15. Olin Corporation

9. Methodology

9.1. Research Scope

9.2. Research Methodology

9.3. Market Sizing and Forecasting Model

9.4. Data Validation and Triangulation

9.5. Assumptions and Limitations

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Protective Coating Resins Market Segmentation

By Resin

Epoxy

Polyurethane

Acrylic

Alkyd

Vinyl Ester and Vinyl

Polyester

Fluoropolymer

Polysiloxane

Bio-based

By Technology

Solvent-borne

Water-borne

Powder-based

100% Solids

Radiation-Cured

By Substrate Compatibility

Metals

Concrete and Masonry

Plastics and Composites

Wood

By End-Use Industry

Infrastructure and Construction

Oil and Gas

Power Generation

Marine

Industrial Machinery and Equipment

Automotive and Transportation

Mining and Metal Processing

Aerospace and Defense

By Application Method

Spray Coating

Brush and Roller

Dipping and Electrocoating

Coil Coating

By Functional Property

Anti-Corrosion

Chemical and Acid Resistance

Thermal and Fire Resistance

Abrasion and Impact Resistance

UV and Weathering Resistance

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Professional Contractor Supply Channels

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global Protective Coating Resins Market was valued at USD 22.6 billion in 2025 and is projected to reach USD 30.6 billion by 2032, expanding at a CAGR of 4.4%. Growth is being supported by rising investments in infrastructure, offshore energy, marine coatings, transportation networks, and industrial corrosion protection solutions. Increasing adoption of sustainable and PFAS-free resin systems is also accelerating long-term industry development.

Waterborne epoxy resins are emerging as a major technological advancement due to ultra-low VOC emissions and high corrosion resistance performance. Modern formulations introduced for 2026 applications deliver 75% to 80% lower VOC levels while achieving 2,000-hour salt spray resistance suitable for harsh industrial and marine environments. Regulatory pressure from the EPA and European Chemicals Agency is further accelerating the transition toward sustainable coating technologies across North America and Europe.

Major companies shaping the competitive landscape include BASF SE, Covestro AG, Arkema S.A., allnex GMBH, Dow Chemical Company, Huntsman Corporation, and Evonik Industries AG. These companies are investing in bio-based polyester resins, waterborne polyurethane technologies, PFAS-free coatings, graphene-enhanced epoxy systems, and recycled PET-based resin innovations to strengthen sustainability and performance capabilities.

Spray coating remained the dominant application method with a 58.6% market share in 2025 due to its efficiency in coating pipelines, offshore platforms, tanks, bridges, and industrial structures. Infrastructure, marine, oil & gas, renewable energy, industrial machinery, and automotive sectors are generating strong demand for advanced anti-corrosion and weather-resistant resin systems. Growth in offshore wind projects, LNG terminals, and transportation infrastructure is further boosting adoption globally.

Key future opportunities are centered around graphene-enhanced epoxy coatings, lignin-derived bio-renewable acrylic resins, and low-carbon polyester resin supply chains. Graphene-modified epoxy systems are improving offshore corrosion resistance and reducing coating thickness requirements, while lignin-based acrylic resins are gaining attention for superior UV resistance and circular economy benefits. Increasing procurement requirements for low-carbon and recycled-content coatings across Europe and North America are expected to create new revenue opportunities for sustainable resin manufacturers.