Low-Observable Technologies and Defense Modernization Driving Niche Growth

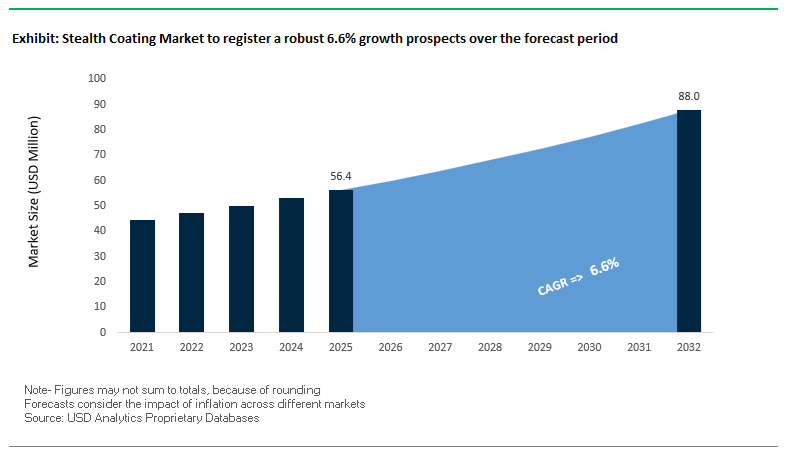

The global Stealth Coating Market represents a highly specialized segment within advanced aerospace and defense materials, driven by the need for low-observable (LO) technologies that reduce radar, infrared (IR), and electromagnetic signatures. The market was valued at $56.4 million in 2025 and is projected to reach $88.2 million by 2032, growing at a CAGR of 6.6% during 2025–2032. While relatively small in absolute value, the market is strategically critical, with demand closely tied to military modernization programs, next-generation aircraft development, and advanced surveillance evasion technologies.

A core growth driver is the increasing investment in fifth- and sixth-generation fighter aircraft, stealth bombers, and advanced naval systems, where coatings play a central role in reducing detectability. Stealth coatings are engineered using radar-absorbing materials (RAM), conductive polymers, and specialized nanostructures, enabling platforms to evade detection across multiple spectrums. These coatings are not only critical for aircraft exteriors but are also increasingly applied to radar systems, sensors, and electronic warfare components, expanding their application scope.

Another structural trend is the shift toward durable, low-maintenance stealth coatings. Historically, stealth materials required frequent maintenance due to environmental degradation. However, modern formulations are being developed to withstand extreme temperatures, corrosion, and operational stress, significantly reducing lifecycle costs and improving mission readiness. This evolution is particularly important for naval and amphibious platforms operating in high-salinity maritime environments.

The market is also influenced by regulatory and environmental considerations, with manufacturers focusing on low-VOC, chrome-free, and environmentally compliant formulations for defense applications. Additionally, the integration of multi-functional coatings that combine stealth properties with anti-corrosion, anti-icing, and drag-reduction capabilities is emerging as a key innovation trend, enhancing overall platform performance.

Market Analysis: Next-Generation Aircraft Programs, Automated Application Systems, and Multi-Spectrum Stealth Innovation Driving Market Evolution

The stealth coating market is being shaped by defense program advancements, precision manufacturing technologies, and multi-functional material innovation, reflecting the increasing complexity of modern military platforms. In January 2026, Northrop Grumman confirmed that the B-21 Raider has entered low-rate initial production, highlighting advancements in its next-generation stealth coating systems. These coatings are designed to be more durable and easier to maintain than previous generations, addressing long-standing operational challenges associated with stealth material upkeep.

Similarly, Lockheed Martin’s May 2025 initiative to integrate sixth-generation stealth coatings into the F-35 Lightning II demonstrates the ongoing evolution of low-observable technologies, enhancing both radar and infrared evasion capabilities. This reflects a broader trend of technology transfer from next-generation defense programs into existing platforms, accelerating capability upgrades.

Product innovation is also advancing at the national defense level. Kansai Paint’s December 2025/January 2026 launch of a specialized stealth coating for the Japan Self-Defense Force highlights the growing demand for region-specific formulations optimized for unique operational environments, such as high-corrosion maritime conditions.

Precision in application is becoming increasingly critical. Mankiewicz’s December 2025 launch of an automated stealth coating R&D and training center focuses on robotic application technologies capable of controlling coating thickness at the micron level, which is essential for maintaining consistent radar-absorbing performance.

Sustainability and compliance are also influencing innovation. PPG’s October 2025 development of low-VOC, chrome-free stealth coatings demonstrates the industry’s shift toward environmentally compliant defense materials without compromising radar-absorption performance.

Beyond aircraft, stealth coatings are expanding into naval and sensor applications. Nippon Paint Marine’s November 2025 low-friction stealth hybrid coating for amphibious aircraft combines reduced radar cross-section with improved hydrodynamics, while Murata Manufacturing’s functional sensor coatings provide protection against icing and lightning without affecting stealth performance.

Defense infrastructure is also integrating stealth technologies. Northrop Grumman’s G/ATOR radar modification program (2024–ongoing) incorporates advanced stealth materials to reduce detectability of radar systems themselves, highlighting the broadening application scope beyond vehicles to electronic systems.

Additionally, Hempel’s “Accelerate to Win” strategy (January 2026) signals the entry of traditional coatings manufacturers into the defense segment, focusing on infrared suppression and long-term corrosion resistance, further diversifying the competitive landscape.

Market Trend: B-21 Raider Program Driving Integrated “Smart RAM” with Reduced Maintenance and Coupled Signature Control

The transition of the B-21 Raider into low-rate initial production in 2026 is redefining the design philosophy of radar-absorbing materials within stealth coating systems. Unlike legacy platforms such as the B-2 Spirit, which relied heavily on labor-intensive external applications, the B-21 incorporates “Smart RAM” directly into composite airframe structures during manufacturing. This integration reduces reliance on post-application coatings and significantly enhances durability. The program’s specification mandates a 90% reduction in coating-related maintenance, targeting a “fly-through” capability where the aircraft maintains its low-observable signature for at least 50 consecutive sorties without requiring repair or recalibration. Additionally, the coupling of radar and infrared stealth characteristics is becoming a central requirement, with RAM systems engineered to achieve emissivity values below 0.1 at operational temperatures. This ensures that reductions in radar cross-section are not offset by increased infrared detectability, aligning with multi-spectrum survivability requirements. As stealth platforms evolve toward integrated material architectures, the emphasis is shifting from surface-applied coatings to embedded multifunctional systems that deliver consistent performance across extended mission cycles.

Market Trend: NGJ-LB Electronic Warfare Pods Require Frequency-Selective and Corrosion-Resistant RAM Systems

The integration of Next Generation Jammer Low-Band pods on carrier-based aircraft is creating new technical demands for stealth coatings, particularly in the domain of electronic warfare. These pods require radar-absorbing materials that not only reduce detectability but also maintain high transparency to internally generated jamming frequencies. To meet these requirements, advanced coatings are incorporating frequency-selective surface layers that allow near-total transmission of operational signals while attenuating hostile radar frequencies by up to 25 decibels in key bands. This dual-functionality represents a significant advancement over conventional passive RAM systems. At the same time, the naval operating environment introduces additional durability challenges, including exposure to salt spray, high humidity, and mechanical vibration. Coatings deployed on these pods must withstand 2,000 hours of accelerated cyclic corrosion testing without delamination or surface degradation, ensuring both aerodynamic integrity and stealth performance. These requirements are driving innovation in multi-layer coating architectures that combine electromagnetic functionality with robust environmental resistance, positioning electronic warfare platforms as a key growth segment in the stealth coatings market.

Market Opportunity: Ambient-Cure Field-Repairable RAM Enables Operational Flexibility and Reduced Maintenance Downtime

One of the most significant operational constraints for current stealth aircraft fleets is the dependency on controlled environments for radar-absorbing material repair and curing. Emerging ambient-cure RAM technologies are addressing this limitation by enabling rapid, field-level repairs without the need for specialized infrastructure. Advanced formulations introduced in 2026 can achieve approximately 90% mechanical cure within four hours at ambient temperatures between 20°C and 30°C, a substantial improvement over traditional systems that require 24 to 48 hours under controlled thermal conditions. These materials also demonstrate high intercoat adhesion strength exceeding 800 psi, even when applied in humidity levels up to 75%, ensuring reliable performance in diverse operational environments. The ability to perform repairs at forward operating bases significantly enhances aircraft availability and mission readiness. Furthermore, transitioning to ambient-cure systems is projected to reduce the logistical footprint associated with low-observable maintenance by approximately 30%, eliminating the need for heavy curing equipment and controlled enclosures. As defense forces prioritize rapid deployment and operational resilience, field-repairable RAM systems represent a critical advancement in stealth coating technology.

Market Opportunity: Radar-Transparent Protective Coatings Enable Next-Generation Conformal Antenna Integration

The increasing adoption of conformal antenna systems embedded within aircraft structures is creating a specialized demand for radar-transparent protective coatings that combine electromagnetic transparency with mechanical durability. These coatings must maintain precise dielectric properties, with dielectric constants below 3.0 and loss tangents under 0.005 across a wide frequency range of 2 to 18 GHz, ensuring minimal signal distortion and efficient beam steering. At the same time, they must provide protection against environmental and mechanical stresses encountered during high-speed flight. Recent advancements in nano-filled polymer coatings have significantly improved erosion resistance, with systems capable of withstanding over 60 minutes of simulated rain erosion at near-sonic speeds before performance degradation occurs. Additionally, these coatings reduce cross-polarization interference by approximately 15 decibels, enhancing signal fidelity for advanced communication and sensor fusion systems. This capability is particularly relevant for next-generation fighter programs, where integrated sensing and communication architectures are central to operational effectiveness. As aerospace platforms evolve toward greater system integration, radar-transparent coatings are emerging as a critical enabling technology within the stealth coatings industry.

Stealth Coating Market Share and Segmentation Insights: Polyurethane-Based RAM Systems and Defense Sector Dominance

By Resin Type: Polyurethane Stealth Coatings Lead with Flexibility and Field Repair Capability

The polyurethane segment dominated the stealth coating market with a 33.6% share in 2025, driven by its critical role as a flexible and durable matrix for radar absorbing materials (RAM). Polyurethane binders are widely used to host advanced magnetic and dielectric fillers such as carbonyl iron, ferrites, and carbon nanotubes, which are essential for reducing radar cross-section (RCS) in low-observable platforms. A key advantage of polyurethane-based stealth coatings is their excellent mechanical flexibility, toughness, and weather resistance, enabling consistent performance under harsh operational conditions. Additionally, these coatings offer superior field repairability, as they can be spray-applied and maintained at depot level, unlike ceramic or polyimide-based systems that require high-temperature curing and specialized facilities. This combination of ease of application, durability, and cost-effective maintenance makes polyurethane the preferred resin type for modern stealth coating systems, reinforcing its leadership in the global stealth coatings market.

By End-User: Defense and Military Segment Dominates with High Demand from Low-Observable Platforms

The defense and military segment accounted for a dominant 66.9% share of the stealth coating market in 2025, reflecting the strategic importance of low-observable technologies in modern warfare. Advanced military platforms such as F-35, F-22, B-21 bombers, and next-generation stealth aircraft rely heavily on radar absorbing coatings for airframes, inlet ducts, and control surfaces to minimize detectability. These coatings are critical for enhancing stealth capabilities, survivability, and mission effectiveness in high-threat environments. Furthermore, stealth coatings require frequent inspection, maintenance, and repair cycles—typically every 50 to 200 flight hours—due to exposure to erosion, rain impact, and thermal stress, creating a strong recurring demand. Defense contractors and military agencies invest heavily in high-performance stealth coating systems and maintenance programs, ensuring continuous innovation and supply. This sustained demand from defense applications solidifies the military sector as the primary driver of growth in the global stealth coatings market.

Competitive Landscape of the Stealth Coatings Market

PPG Leads Market with Advanced Polymer-Based and Infrared-Suppressing Coatings

PPG Industries, Inc. is a key technological catalyst in the stealth coatings market, leveraging its expertise in aerospace and specialty coatings. The company is advancing radiation-curable coatings for rapid deployment of infrared-suppressing finishes, particularly for military assets. Following strategic divestments, PPG has redirected investments toward high-margin aerospace coatings, achieving strong profitability. Its capabilities in conductive and anti-static coatings enable protection against electromagnetic interference, making it a critical supplier for modern stealth platforms.

AkzoNobel Strengthens Market Position with AI-Driven Maintenance and Aerospace Expansion

AkzoNobel N.V. is a major player in the stealth coatings market, focusing on lifecycle management and precision application. Its Iris CMX drone-based inspection tool enables real-time measurement of coating thickness and condition, ensuring optimal performance for radar evasion. The company is expanding its aerospace presence with a new coatings hub in Dubai, supporting regional defense demand. Its Aerofleet Coatings Management system integrates flight data, UV exposure, and predictive analytics, reducing maintenance costs and improving operational readiness.

Northrop Grumman Dominates Strategic Defense with Multi-Spectral Stealth Coatings

Northrop Grumman Corporation is the “stealth architect” of the industry, leading through its advanced defense programs. Its B-21 Raider bomber utilizes next-generation multi-spectral stealth coatings designed to counter advanced radar systems. The company has optimized production processes, significantly reducing costs while maintaining performance. Its focus on modular stealth coating architectures allows rapid updates to counter evolving detection technologies, reinforcing its dominance in strategic defense applications.

Lockheed Martin Leads Aerospace Segment with Integrated Stealth Coating Systems

Lockheed Martin Corporation holds a dominant position in the stealth coatings market, particularly in fighter aircraft production. With a record delivery of 191 F-35 jets, the company integrates advanced stealth coatings directly into manufacturing processes. Its development of coordinated stealth coatings for manned and unmanned systems ensures full-spectrum invisibility across mission platforms. Partnerships with technology firms enable AI-driven maintenance and faster detection of coating degradation, enhancing operational efficiency.

Hentzen Coatings Specializes in Tactical and Low-Signature Military Applications

Hentzen Coatings, Inc. is a specialist leader in the stealth coatings market, focusing on tactical military applications. Its Low Solar Absorbance (LSA) CARC coatings reduce thermal signatures in desert environments, making them ideal for ground vehicles. The company also provides rapid-response repair kits for stealth coatings, improving field maintenance efficiency. Its expertise in epoxy-based systems ensures durability and chemical resistance in extreme combat conditions.

Surrey NanoSystems Leads Nanocomposite Segment with Ultra-Low Reflectance Coatings

Surrey NanoSystems is a pioneer in nanocomposite stealth coatings, particularly through its Vantablack® technology. This coating absorbs 99.965% of visible light, making it the darkest material available for optical and aerospace applications. Its sprayable versions enable application on complex geometries such as drones and satellite components. The company’s expertise in carbon nanotube (CNT) arrays allows superior absorption across visible and infrared spectrums, positioning it at the forefront of next-generation stealth technologies.

United States Leading Next-Generation Stealth Coatings with Autonomous and Self-Diagnostic Technologies

The United States remains the global leader in the stealth coatings market, driven by advanced defense programs and rapid innovation in next-generation aerospace technologies. The shift toward high-throughput, robotic-applied stealth coatings is enabling scalable production for drone swarms and next-generation combat aircraft.

Technological advancements include the development of self-diagnostic stealth coatings with embedded fiber-optic sensors, capable of detecting real-time degradation in radar-absorbing properties. Government-backed initiatives such as the Next-Generation Air Dominance (NGAD) program are supporting the development of adaptive “morphing skin” coatings that can dynamically alter absorption frequencies during flight. Product innovations such as ceramic-matrix composite radar-absorbent materials (RAM) capable of withstanding extreme temperatures above 2,000°C are critical for hypersonic applications. Additionally, large-scale deployment of polyimide-based stealth coatings across advanced fighter platforms highlights the U.S. leadership in high-performance, multi-domain stealth technologies.

China Scaling Mass Production of Radar-Absorbent Coatings for Air and Naval Platforms

China is rapidly advancing in the stealth coatings industry, transitioning from R&D to large-scale manufacturing of radar-absorbent materials (RAM). The focus is on improving operational efficiency by reducing maintenance requirements for stealth aircraft and naval fleets.

Technological innovations include the development of graphene-enhanced stealth primers offering improved adhesion and durability in high-humidity environments, as well as plasma-magnetic coatings for signature suppression in space-based assets. Large-scale investments in nanomaterial production are strengthening domestic capabilities, while new standards are driving the adoption of broadband radar-absorbing coatings capable of countering advanced detection systems. Applications extend to naval vessels, with anisotropic stealth coatings significantly reducing radar cross-sections in modern destroyers, reinforcing China’s position in multi-domain stealth capabilities.

India Advancing Indigenous Stealth Coatings for Defense Self-Reliance

India is emerging as a key player in the stealth coatings market, driven by its focus on defense self-reliance under national initiatives. The development of multi-spectral stealth coatings capable of reducing both radar and infrared signatures is a major breakthrough for next-generation combat aircraft.

Government programs such as iDEX (Innovations for Defence Excellence) are encouraging startups to develop lightweight radar-absorbing materials, particularly for drones and advanced weapon systems. Technological advancements include conductive polymer-based coatings that significantly reduce weight compared to traditional materials, improving performance in high-altitude environments. Infrastructure investments in testing facilities and updated defense procurement policies are further supporting domestic innovation. Key applications include stealth coatings for submarines and naval vessels, highlighting India’s growing capabilities across air and maritime defense sectors.

South Korea Driving Commercial-Scale Stealth Coatings for Aerospace and Defense Exports

South Korea is positioning itself as a global exporter of cost-effective stealth coating technologies, leveraging its expertise in advanced materials and manufacturing. The integration of UV-curable stealth coatings in fighter aircraft production is significantly reducing curing times and improving manufacturing efficiency.

Investments in advanced materials such as frequency-selective surfaces (FSS) are enabling coatings that selectively absorb hostile radar signals while allowing friendly communication signals to pass through. Product innovations such as stealth repair films (“Stealth-Wrap”) are improving operational readiness by enabling rapid field maintenance. South Korea is also expanding applications into terrestrial defense systems, with radar-absorbing coatings for armored vehicles becoming a key growth segment. Regulatory frameworks are ensuring strict control over advanced formulations, reinforcing the country’s competitive edge in global defense markets.

France Leading European Innovation in Multispectral and Environmentally Compliant Stealth Coatings

France is at the forefront of European innovation in the stealth coatings market, focusing on multispectral signature management for advanced defense platforms. Technological advancements include the development of nanostructured smart coatings capable of dynamically adjusting thermal emissivity, enabling better camouflage across different environments.

Sustainability is also a major focus, with the introduction of waterborne stealth coatings that meet stringent EU environmental regulations while maintaining high corrosion resistance in marine applications. Strategic investments in metamaterial-based coatings are enhancing performance against ultra-wideband radar systems. Applications such as infrared-suppressive coatings for helicopters highlight the importance of stealth technologies in modern defense systems. Government policies mandating increased investment in signature management technologies are further accelerating innovation in this segment.

Australia Emerging as a Strategic Stealth Coatings Hub for Indo-Pacific Defense Operations

Australia is evolving into a key regional hub in the stealth coatings market, particularly for maintenance, repair, and overhaul (MRO) operations. The establishment of advanced facilities for stealth coating application and repair is supporting regional fleets of advanced fighter aircraft.

Technological advancements include the development of robotic inspection and repair systems, enabling efficient maintenance of stealth coatings without requiring full system shutdowns. Government investments are supporting the localization of radar-absorbent material production, strengthening supply chain resilience. Applications extend to naval and underwater systems, with the use of acoustic stealth coatings for autonomous underwater vehicles. Strategic collaborations under international defense agreements are further enhancing Australia’s role in the global stealth coatings ecosystem.

Stealth Coating Market Report Scope

Stealth Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$56.4 Million

|

|

Market Size (2032)

|

$88.2 Million

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Polyimide, Thermoplastics, Ceramic-based), By Material Composition (Iron-Ball Paint, Carbon-based Materials, Ferrite-based, Nanocomposites, Polymer Matrix Composites), By Technology (Radar Absorbing Materials, Radar Absorbing Structural, Infrared, Visual, Acoustic Stealth, Plasma Stealth), By Substrate (Metals, Composites, Ceramics, Polymers), By Application (Aerospace, Naval Vessels, Ground Defense Systems, Missiles and Munitions, Electronic Devices, Luxury Automotive), By End-User (Defense and Military, Aerospace and Aviation OEMs, Automotive Manufacturers, Consumer Electronics), By Form (Liquid Coatings, Films and Sheets, Spray, Powder Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lockheed Martin Corporation, Northrop Grumman Corporation, BAE Systems plc, RTX Corporation, PPG Industries, Inc., Akzo Nobel N.V., The Boeing Company, BASF SE, Intermat Defense, Hentzen Coatings, Inc., HyperStealth Biotechnology Corp., CFI Solutions, Surrey NanoSystems, Micromag, Stealth Veils Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stealth Coating Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Polyimide

- Thermoplastics

- Ceramic-based

By Material Composition

- Iron-Ball Paint

- Carbon-based Materials

- Ferrite-based

- Nanocomposites

- Polymer Matrix Composites

By Technology

- Radar Absorbing Materials

- Radar Absorbing Structural

- Infrared

- Visual

- Acoustic Stealth

- Plasma Stealth

By Substrate

- Metals

- Composites

- Ceramics

- Polymers

By Application

- Aerospace

- Naval Vessels

- Ground Defense Systems

- Missiles and Munitions

- Electronic Devices

- Luxury Automotive

By End-User

- Defense and Military

- Aerospace and Aviation OEMs

- Automotive Manufacturers

- Consumer Electronics

By Form

- Liquid Coatings

- Films and Sheets

- Spray

- Powder Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Stealth Coating Industry

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- RTX Corporation

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Boeing Company

- BASF SE

- Intermat Defense

- Hentzen Coatings, Inc.

- HyperStealth Biotechnology Corp.

- CFI Solutions

- Surrey NanoSystems

- Micromag

- Stealth Veils Inc.

*- List not Exhaustive