Marine Deck Coatings Market Size, Non-Slip Safety Systems, and High-Traffic Deck Protection Outlook

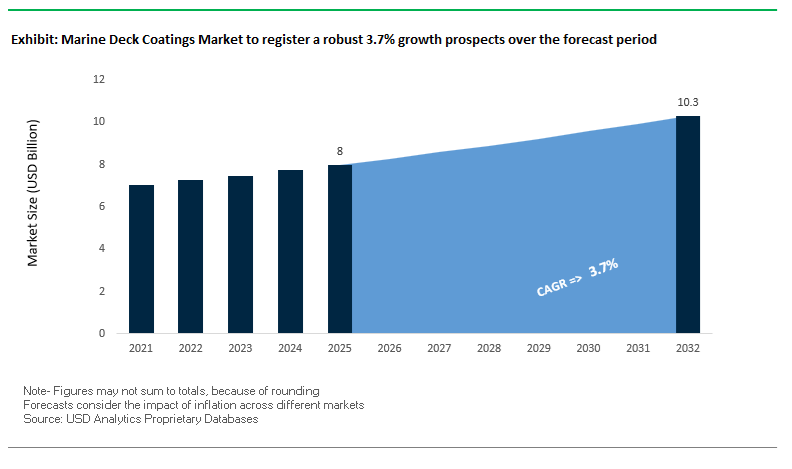

The global marine deck coatings market was valued at $8 billion in 2025 and is projected to reach $10.3 billion by 2032, growing at a CAGR of 3.7%. Market expansion is driven by rising demand for non-slip deck coatings, polyurethane deck coatings, epoxy deck systems, and UV-resistant marine coatings across commercial vessels, naval fleets, offshore platforms, cruise ships, and leisure marine segments. These coatings are critical for ensuring crew safety, corrosion protection, and durability in high-traffic and harsh marine environments exposed to saltwater, UV radiation, and mechanical wear.

A key growth driver is the increasing emphasis on safety compliance and slip resistance, particularly in helidecks, passenger decks, and offshore access platforms, where accidents due to wet or contaminated surfaces pose significant risks. Advanced high-friction coatings and rapid-cure deck systems are gaining traction as they allow faster turnaround during docking while maintaining high-performance safety standards. Additionally, the expansion of cruise tourism, offshore wind installations, and LNG infrastructure is driving demand for specialized deck coatings that combine aesthetic appeal with functional performance.

Sustainability is also shaping market evolution. The shift toward low-VOC coatings, bio-based resins, and environmentally friendly formulations is accelerating as regulatory pressures increase and operators seek to reduce environmental impact. Innovations in ceramic coatings, hydrophobic surfaces, and advanced polyurethane systems are enhancing resistance to UV degradation, staining, and corrosion, extending the lifecycle of marine deck surfaces. Regionally, Asia-Pacific dominates due to strong shipbuilding activity, while Europe leads in offshore wind and sustainable marine coating innovations.

Market Analysis: Contract Wins, Sustainable Deck Coatings, and Advanced Application Technologies Driving Market Evolution

The marine deck coatings industry is evolving through project-driven demand, sustainability innovation, and advanced coating technologies. In March 2026, AkzoNobel secured a contract to supply Interdeck non-slip coatings for next-generation ferries, emphasizing rapid curing and high durability for high-traffic commuter decks. This highlights the growing importance of fast-application deck systems that reduce docking time while maintaining safety performance.

Strategic growth and portfolio expansion are shaping competitive positioning. Hempel A/S reported €750 million in marine sales in 2025 and launched its “Accelerate to Win” strategy, which prioritizes expanding its topsides and deck coatings portfolio, particularly for superyachts and cruise vessels where both aesthetic quality and performance are critical. Additionally, Hempel’s October 2025 contract for North Sea offshore wind foundations includes the application of high-friction Hempadur deck coatings for helidecks and technician platforms, reinforcing the role of deck coatings in safety-critical offshore infrastructure.

Sustainability and material innovation are gaining prominence. In July 2025, AkzoNobel introduced a bio-based resin deck coating, replacing traditional petroleum-derived components with plant-based alternatives such as rapeseed and pine-derived resins, while maintaining UV stability and durability. Similarly, PPG Industries reported that 41% of its 2024 sales were derived from sustainably advantaged solutions, with strong demand for SIGMADUR™ polyurethane deck coatings featuring ultra-low VOC formulations for passenger vessels.

Product innovation is also expanding into niche and high-value segments. IGL Coatings’ January 2026 Ecocoat Marine “Wave 2” series introduces ceramic-based coatings designed for wood and composite decks, offering enhanced hydrophobic properties and UV resistance to prevent saltwater staining. This builds on its May 2024 launch of specialized coatings for luxury deck materials such as leather and fabric, reflecting growing demand in the premium leisure marine segment.

Operational expansion and manufacturing investments are supporting market growth. Sherwin-Williams’ November 2025 $300 million facility expansion includes dedicated production lines for SeaGuard® and Macropoxy® deck systems, targeting increased demand from U.S. Navy and Coast Guard maintenance programs. Meanwhile, PPG Industries’ March 2025 expansion of its Yantai facility in China adds significant capacity for epoxy and polyurethane deck coatings, supporting the rapidly growing Asia-Pacific newbuild market, particularly for LNG carriers.

Advancements in application technology are further improving efficiency and sustainability. PPG’s November 2024 deployment of electrostatic spray technology for marine decks achieved a 35% reduction in paint waste and overspray, while delivering more uniform coating coverage on complex deck geometries.

Market Trend: Rapid-Cure Polyurethane Deck Coatings Transforming Cruise Ship Maintenance Cycles and Passenger Operations

The marine deck coatings industry is witnessing a decisive transition within the cruise segment toward rapid-cure polyurethane (PU) systems, replacing conventional epoxy-based coatings. This shift is primarily driven by the need to maintain uninterrupted passenger operations while conducting routine deck maintenance. Cruise operators are increasingly prioritizing coating technologies that enable overnight application and immediate usability, minimizing disruption to onboard services and revenue-generating activities.

Rapid-cure PU coatings deliver significant improvements in turnaround efficiency. These systems achieve walk-on hardness within 2 to 4 hours at standard ambient conditions, compared to 12 to 24 hours for traditional marine epoxies. This performance enables maintenance teams to complete deck refurbishment during nighttime windows, ensuring full passenger access by the following day. Such operational continuity is critical in the cruise industry, where downtime directly impacts customer experience and onboard revenue streams.

Environmental compliance is another major factor driving adoption. Modern aliphatic polyurethane formulations maintain VOC levels below 150 g/L, aligning with stringent emission standards enforced in key maritime regions, including the European Union and California. This compliance is increasingly necessary for vessels operating across regulated international ports. In addition to curing speed and environmental performance, PU coatings provide superior mechanical flexibility, with elongation-at-break values exceeding 50% to 100%. This elasticity allows coatings to accommodate structural flexing in large vessels, reducing the risk of cracking and premature failure. In contrast, rigid epoxy systems exhibit failure rates of 15% to 20% within the first three years under dynamic load conditions. These combined advantages position rapid-cure polyurethane coatings as the preferred solution for high-utilization passenger vessels.

Market Trend: Ceramic-Based Non-Skid Coatings Enhancing Naval Flight Deck Durability and Thermal Resistance

Naval applications are driving a parallel innovation trajectory in marine deck coatings, particularly through the adoption of ceramic non-skid systems for flight decks. Traditional epoxy-aggregate non-skid coatings are being replaced by ceramic-metal thermal spray (CMTS) and ceramic-reinforced resin systems, driven by the need for enhanced durability, reduced weight, and extreme thermal resistance under advanced aircraft operations.

Weight reduction is a critical performance parameter for naval vessels. Ceramic-based non-skid systems can be applied at significantly lower thicknesses compared to conventional coatings, resulting in weight savings of 20 to 30 metric tons on large amphibious assault ships. This reduction directly improves vessel stability by lowering the vertical center of gravity, which is essential for operational safety and maneuverability.

Lifecycle performance improvements are equally significant. While traditional non-skid coatings typically require replacement every 12 to 18 months due to wear and loss of friction, ceramic-reinforced systems demonstrate service lives of 5 to 8 years. This extended durability reduces maintenance frequency and lifecycle costs by approximately 40%, making them highly attractive for long-duration naval deployments.

Thermal resistance is a defining advantage of ceramic systems. These coatings maintain structural integrity at temperatures exceeding 400°C, enabling them to withstand the extreme thermal loads generated by short takeoff and vertical landing aircraft such as the F-35B. Conventional epoxy coatings often fail under such conditions, exhibiting rapid charring and delamination. The superior thermal and mechanical performance of ceramic non-skid systems is positioning them as a standard specification in next-generation naval fleet modernization programs.

Market Opportunity: IMO Polar Code Expansion Driving Demand for Ice-Resistant and Low-Temperature Marine Deck Coatings

The expansion of the International Maritime Organization’s Polar Code in 2026 to include non-SOLAS vessels is creating a new demand segment for specialized marine deck coatings designed for Arctic and sub-Arctic operations. This regulatory update extends compliance requirements to fishing vessels over 24 meters and yachts exceeding 300 gross tons, triggering a widespread upgrade cycle for deck safety systems.

One of the primary functional requirements emerging from this regulation is ice adhesion mitigation. Advanced low-adhesion deck coatings are capable of reducing the bond strength of sea ice by up to 70%, significantly improving crew safety and vessel stability. Ice accumulation on decks can add substantial top-weight, potentially reaching hundreds of tons, which increases the risk of stability loss in extreme conditions. Coatings that minimize ice buildup are therefore becoming essential for vessels operating in polar environments.

Application capability in extreme climates is another critical factor. There is a growing demand for coatings that can be applied and cured at temperatures as low as −10°C, enabling maintenance activities in remote regions where heated facilities are unavailable. This is particularly relevant for the more than 3,500 vessels operating in or near Arctic waters, many of which lack access to specialized infrastructure. These requirements are driving innovation in low-temperature curing chemistries and expanding opportunities for manufacturers offering cold-climate coating solutions tailored to polar operations.

Marine Deck Coatings Market Share and Segmentation Insights

Exposed Weather Deck Coatings Capture 35% Share Driven by Harsh Marine Exposure and Non-Skid Demand

The marine deck coatings market by deck location is dominated by exposed weather decks, accounting for 35% of the global market share in 2025, due to their constant exposure to extreme marine conditions. These decks endure UV radiation, saltwater corrosion, heavy foot traffic, and mechanical wear, making non-skid epoxy coatings and polyurethane deck coatings essential for both safety and longevity. Slip-resistant properties are critical for crew operations, especially under wet conditions, while corrosion protection ensures structural integrity across vessel types. Additionally, weather decks are highly visible and frequently accessed areas, increasing the demand for aesthetic finishes, color retention, and long-lasting durability. This combination of safety compliance, operational performance, and visual standards drives the adoption of premium marine deck coating systems, reinforcing exposed weather decks as the leading segment.

Maintenance and Repair Segment Holds 64% Share Due to Frequent Recoating Cycles and Safety Regulations

In the marine deck coatings market by end-use industry, maintenance and repair dominate with a 64% market share in 2025, reflecting the high wear and tear experienced by deck surfaces. Unlike hull coatings, deck coatings require more frequent recoating cycles—typically every 2 to 4 years—due to constant exposure to cargo handling, equipment movement, and crew activity. This leads to accelerated abrasion, cracking, and coating degradation, necessitating regular maintenance. Furthermore, maritime safety regulations mandate the use of slip-resistant, non-skid coatings in operational areas, with inspections often requiring immediate remediation if standards are not met. These regulatory pressures, combined with operational wear, ensure consistent demand for marine maintenance coatings, anti-slip deck systems, and corrosion-resistant surface solutions, positioning maintenance and repair as the dominant and most recurring revenue segment.

Competitive Landscape in the Marine Deck Coatings Market

AkzoNobel advances high-performance marine deck systems with AI-driven customization

AkzoNobel, through its International® brand, remains a dominant force in marine deck coatings, offering integrated systems that combine industrial durability with aesthetic precision. The company reported €10.16 billion in revenue in 2025, supported by a 47% reduction in Scope 1 and 2 emissions compared to its 2018 baseline. Its Intershield® 300HS high-solids epoxy is engineered for helicopter landing decks and cargo walkways, delivering superior abrasion resistance and corrosion protection. AkzoNobel has also integrated AI-driven color matching following its 2026 “Rhythm of Blues” launch, enabling customized cruise ship deck finishes with enhanced UV stability. Its focus on bio-attributed resins, developed with BASF, aligns with circular economy goals for large-scale marine recoating projects.

Hempel strengthens marine deck coatings with reinforced durability and fire protection integration

Hempel A/S is a performance-driven leader in marine deck coatings, achieving an adjusted EBITDA margin of 18.2% on €2.165 billion revenue in 2026, with marine segment growth reaching €750 million. Its Hempadur Multi-Strength 350 coating incorporates reinforced glass flakes, providing exceptional impact resistance for bulk carrier weather decks. The company has also advanced integration between deck and hull systems through Hempaguard NB applications for Maersk vessels, enhancing overall vessel efficiency. Hempel’s expertise in passive fire protection (PFP) makes its deck coatings a preferred choice for offshore oil and gas platforms, where safety and durability are critical. Its solutions combine slip resistance, fire safety, and long-term corrosion protection in demanding marine environments.

Jotun leads smart deck coating innovation with predictive maintenance technologies

Jotun is at the forefront of innovation in marine deck coatings, particularly in the Asia-Pacific region, which accounts for over 50.5% of global shipbuilding demand. The company has introduced Smart Deck Coatings embedded with micro-sensor technology that detects early-stage corrosion and surface degradation. Its Jotafloor and Hardtop series are widely recognized for UV-resistant polyurethane performance, maintaining color integrity in harsh marine conditions. Jotun has extended its HullSkater platform logic to deck maintenance, enabling predictive maintenance scheduling that can reduce long-term repair costs by approximately 20%. With strong OEM presence, Jotun coatings are extensively used in LNG-powered and hybrid vessels launched between 2025 and 2026.

PPG enhances marine deck coatings with AI-driven formulation and thermal management solutions

PPG Industries leverages its aerospace-grade coating expertise to deliver lightweight, high-performance marine deck coatings. The company reported $15.9 billion in net sales in 2025, with continued growth in its Protective and Marine Coatings segment. PPG has introduced AI-designed coatings that reduce development cycles and material waste, particularly for cruise ships and luxury yachts. Its solar-reflective deck coatings reduce surface temperatures of exposed steel, lowering thermal stress on cargo stored below deck. Additionally, the adaptation of MoonWalk® automated mixing technology ensures consistent color and texture across large-scale marine applications. These innovations position PPG as a key player in performance-driven and energy-efficient deck coating systems.

Sherwin-Williams dominates non-skid marine deck coatings for naval and offshore applications

Sherwin-Williams leads the North American marine deck coatings market, particularly in naval and offshore sectors requiring MIL-SPEC compliance. The company is benefiting from a projected 4.4% CAGR between 2026 and 2030, driven by U.S. naval expansion and offshore wind projects. Its advanced epoxy-based non-skid coatings provide superior grip even under oil or seawater exposure, making them essential for aircraft carriers and emergency vessels. In 2026, Sherwin-Williams introduced UV-curable deck coatings that enable same-day repair and return-to-service, significantly reducing operational downtime. Its extensive logistics network across the U.S. and Europe supports rapid deployment and on-site technical services for complex marine infrastructure projects.

Nippon Paint advances marine deck coatings with hydrogel and self-cleaning technologies

Nippon Paint Marine is advancing marine deck coating technology through its focus on hydrogel surfaces and antimicrobial performance. In its 2026 strategy update, the company allocated 59% of its R&D investment toward sustainability and elimination of PFAS and MCCP chemicals. It has developed self-cleaning deck coatings using photocatalytic technology, enabling decomposition of organic contaminants and reducing maintenance requirements. Nippon Paint is expanding production capacity in China and India under its NIPSEA Group to meet growing demand for low-VOC marine coatings. Its integration of antifungal additives directly into coating systems supports hygiene-critical applications such as hospital ships and luxury cruise vessels in the post-pandemic environment.

China’s Green Ferry Policy Accelerating Adoption of High-Performance, Low-VOC Deck Coatings

China’s Ministry of Transport is implementing stringent environmental and safety standards under its “Green Water” initiative, creating substantial opportunities for advanced marine deck coatings in the domestic passenger vessel segment. The policy focuses on improving safety performance and reducing environmental impact across coastal and inland ferry operations, particularly in high-density regions such as the Pearl River Delta and Yangtze River basin.

A key regulatory requirement is the enforcement of enhanced slip resistance standards. All new coastal ferries must now utilize deck coatings with a Pendulum Test Value exceeding 50 under wet conditions. This mandate is driving a shift away from smooth-finish coatings toward textured polyurethane systems that provide high friction without compromising durability or cleanability. As passenger safety becomes a regulatory priority, demand for advanced non-skid coatings is expected to increase significantly.

VOC emission limits are also being tightened, with new standards capping VOC content at 250 g/L for topside coatings. This regulation affects approximately 12,000 domestic vessels, creating a large-scale replacement market for compliant coating systems. Water-based and high-solids formulations are gaining traction as operators seek to meet regulatory thresholds while maintaining performance characteristics.

The combination of safety mandates, environmental compliance, and fleet modernization is positioning China as a major growth hub for marine deck coatings. Suppliers capable of delivering low-VOC, high-durability, and slip-resistant coating systems are expected to benefit from sustained demand driven by regulatory enforcement and infrastructure investment across the country’s inland and coastal waterways.

South Korea Marine Deck Coatings Market: LNG Vessel Innovation and Smart Shipbuilding Excellence

South Korea leads the marine deck coatings market, driven by its global dominance in LNG carriers, ammonia-ready vessels, and advanced shipbuilding technologies. The country is at the forefront of developing cryogenic-resistant deck coatings, specifically engineered to withstand extreme thermal shocks during LNG bunkering operations. These coatings are essential for ensuring structural integrity and operational safety in high-value maritime assets.

Technological innovation is evident in the commercialization of nano-composite non-skid deck coatings, which enhance safety by increasing the coefficient of friction while reducing overall coating weight. The adoption of ultra-durable epoxy systems for autonomous vessel fleets such as the “K-Smart” series reflects the industry’s focus on long-life, low-maintenance solutions. Infrastructure investments, including KCC Corporation’s smart-compounding facility in Ulsan, are strengthening production capabilities for high-performance deck coatings. Supported by the Green Shipbuilding Initiative 2030 and strict environmental regulations, South Korea continues to lead in bio-based, low-VOC marine coating technologies.

China Marine Deck Coatings Market: High-Volume Production and Naval Expansion Driving Demand

China dominates the marine deck coatings market in terms of volume, supported by its expansive merchant fleet and growing naval capabilities. The country is rapidly adopting graphene-enhanced deck coatings, offering superior anti-corrosion performance and durability, particularly for high-stress applications such as helidecks and cargo decks.

Technological advancements include the widespread use of waterborne polyurethane (WPU) topcoats, providing high UV resistance while significantly reducing VOC emissions. Infrastructure investments in major ship-repair hubs like Zhoushan are introducing automated robotic coating systems, improving efficiency and application consistency. China’s naval expansion is also driving demand for specialized flight deck coatings, designed to withstand high heat from jet operations. Regulatory frameworks such as GB/T 38597-2020 updates are enforcing strict limits on hazardous substances, accelerating the transition toward environmentally sustainable marine coating solutions.

Norway Marine Deck Coatings Market: Offshore Wind Applications and Zero-Emission Innovation

Norway’s marine deck coatings market is shaped by its leadership in offshore wind energy and zero-emission maritime operations. The development of biocide-free silicone-based deck coatings is improving safety by preventing slime buildup, which is critical for offshore service vessels operating in harsh North Sea conditions.

Innovations such as self-healing deck coatings with micro-encapsulated resins are enhancing durability by automatically repairing micro-cracks, even in sub-zero temperatures. Government support through initiatives like the NOx Fund is encouraging the adoption of UV-cured deck coatings, which eliminate the need for energy-intensive curing processes. Norway is also integrating digital twin technologies and satellite monitoring systems to track coating performance in real time, optimizing maintenance cycles. These advancements are particularly important for service operation vessels (SOVs) used in offshore wind farms, where safety and durability are paramount.

United States Marine Deck Coatings Market: Defense Modernization and PFAS-Free Coating Transition

The United States marine deck coatings market is driven by defense modernization programs and regulatory-driven innovation, particularly focusing on the elimination of harmful chemicals. Updates to the Toxic Substances Control Act (TSCA) are accelerating the phase-out of PFAS-containing additives, pushing manufacturers toward PFAS-free silicone-based deck coatings.

Product innovations include infrared-reflective “cool deck” coatings, which reduce internal vessel temperatures and improve crew comfort. The market is also benefiting from investments under the Infrastructure Investment and Jobs Act (IIJA), supporting the refurbishment of aging ferry decks and maritime infrastructure. Low-temperature, moisture-tolerant coatings are being widely adopted in military fleet maintenance, particularly for the U.S. Navy and Military Sealift Command operations. The expansion of specialized R&D centers is further accelerating the development of rapid-cure, high-performance deck coatings for challenging marine environments.

Japan Marine Deck Coatings Market: Precision Engineering and Long-Life Coating Systems

Japan’s marine deck coatings market is defined by precision engineering, advanced material science, and long-life coating technologies. The development of hybrid inorganic-organic coatings combines the flexibility of polymers with the hardness of ceramics, delivering extended service life and superior durability.

Japanese manufacturers are pioneering in-water deck repair technologies, enabling maintenance without dry docking and reducing operational downtime. The adoption of visible-light photocatalytic coatings is enhancing cleanliness by breaking down organic contaminants on deck surfaces. These innovations are particularly relevant in applications such as pure car and truck carriers (PCC/PCTC), where non-marking, high-performance coatings are essential. Government support under the Blue-Growth Strategy is further driving innovation in anti-static and autonomous vessel coating technologies, reinforcing Japan’s leadership in advanced marine coatings.

Singapore Marine Deck Coatings Market: Global MRO Hub and Rapid-Return Coating Technologies

Singapore has established itself as the global hub for marine maintenance, repair, and overhaul (MRO), making it a key market for advanced deck coating technologies. The country’s shipyards are experiencing increased dry-docking activity, driven by regulatory compliance and the need for fuel-efficient, low-emission coating systems.

Technological advancements include the implementation of underwater drone inspections, enabling real-time monitoring of coating performance without operational disruptions. Regulatory initiatives such as the Green Port Programme 2026 are incentivizing the adoption of zero-VOC deck coatings, offering significant cost benefits to shipowners. The demand for abrasion-resistant coatings is particularly strong in tanker and VLCC segments, where decks are subjected to heavy mechanical stress. Innovations in bio-renewable deck sealants and low-odor coatings are further enhancing performance in Singapore’s high-temperature, high-humidity environment, reinforcing its position as a leading global retrofit hub.

Marine Deck Coatings Market Report Scope

Marine Deck Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8 Billion

|

|

Market Size (2032)

|

$10.3 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Chemistry (Epoxy, Polyurethane, Polyaspartic and Polyurea, Acrylic, Alkyd Enamels, Vinyl Ester, Methyl Methacrylate), By Technology (Solvent-borne Coatings, Water-borne Coatings, Solvent-free, UV-Curable Coatings), By Deck Location (Exposed Weather Decks, Helidecks, Internal Decks, Cargo Decks, Bridge and Topside Decks, Tank Tops and Bilges), By Functional Property (Anti-Slip, Anti-Corrosive Primers, UV-Resistant Topcoats, Chemical and Fuel Resistant Coatings, Heat-Reflective, Impact and Abrasion Resistant), By End-Use Industry (Newbuild, Maintenance and Repair)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., The Sherwin-Williams Company, Chugoku Marine Paints, Ltd., Nippon Paint Marine Coatings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, RPM International Inc., BASF SE, Axalta Coating Systems Ltd., Sika AG, Beckers Group, SunRui Marine Environment Engineering Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Deck Coatings Market Segmentation

By Chemistry

- Epoxy

- Polyurethane

- Polyaspartic and Polyurea

- Acrylic

- Alkyd Enamels

- Vinyl Ester

- Methyl Methacrylate

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Solvent-free

- UV-Curable Coatings

By Deck Location

- Exposed Weather Decks

- Helidecks

- Internal Decks

- Cargo Decks

- Bridge and Topside Decks

- Tank Tops and Bilges

By Functional Property

- Anti-Slip

- Anti-Corrosive Primers

- UV-Resistant Topcoats

- Chemical and Fuel Resistant Coatings

- Heat-Reflective

- Impact and Abrasion Resistant

By End-Use Industry

- Newbuild

- Maintenance and Repair

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Marine Deck Coatings Industry

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Chugoku Marine Paints, Ltd.

- Nippon Paint Marine Coatings Co., Ltd.

- Kansai Paint Co., Ltd.

- KCC Corporation

- RPM International Inc.

- BASF SE

- Axalta Coating Systems Ltd.

- Sika AG

- Beckers Group

- SunRui Marine Environment Engineering Co., Ltd.

*- List not Exhaustive