Marine Coatings Market Size, Fuel-Efficient Coating Technologies, and Sustainable Shipping Outlook

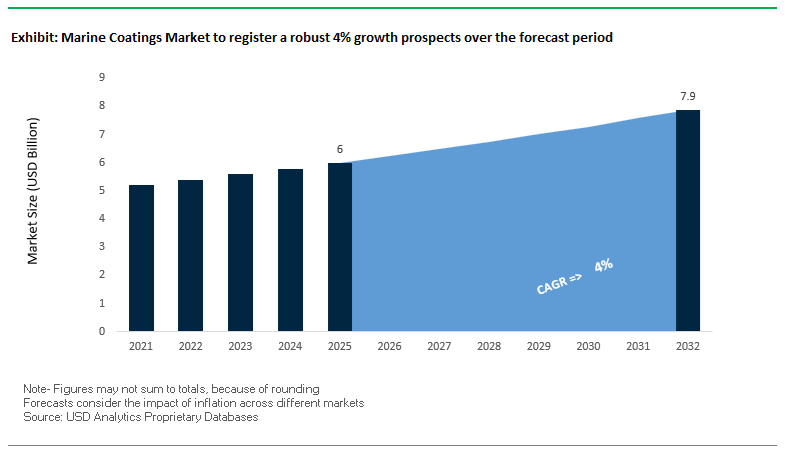

The global marine coatings market was valued at $6 billion in 2025 and is projected to reach $7.9 billion by 2032, growing at a CAGR of 4%. Market growth is being driven by increasing demand for antifouling coatings, protective marine coatings, foul-release coatings, and high-performance hull coatings across commercial shipping, naval vessels, offshore platforms, and LNG carriers. As the maritime industry faces mounting pressure to reduce emissions and improve operational efficiency, marine coatings are evolving into critical enablers of fuel savings, corrosion protection, and regulatory compliance.

A key growth driver is the rising adoption of fuel-efficient and low-friction coating systems, which significantly reduce hydrodynamic drag and fuel consumption. With regulatory frameworks such as the EU Emissions Trading System (ETS) and IMO carbon intensity regulations, shipowners are increasingly investing in advanced coating technologies that contribute to measurable emissions reductions. Additionally, the expansion of electric and hybrid propulsion vessels is driving demand for coatings optimized for ultra-smooth surfaces and energy-efficient performance.

The market is also benefiting from growth in global shipbuilding, LNG carrier expansion, and offshore energy infrastructure, where coatings play a vital role in protecting assets from harsh marine environments, corrosion, and extreme temperatures. Innovations in biomimetic coatings, silicone-based systems, and electrostatic application technologies are further enhancing performance and sustainability. Regionally, Asia-Pacific dominates due to strong shipbuilding activity, while Europe leads in regulatory-driven innovation and sustainable marine coating adoption.

Market Analysis: Decarbonization Technologies, Strategic Expansion, and Advanced Coating Systems Driving Market Evolution

The marine coatings industry is undergoing significant transformation driven by decarbonization goals, advanced coating technologies, and strategic repositioning among leading players. In March 2026, AkzoNobel secured a major contract to supply its full marine coating suite for next-generation ferries, emphasizing ultra-smooth primers and topcoats designed to complement electric and hybrid propulsion systems. This reflects the increasing integration of coatings into energy-efficient vessel design strategies.

Strategic growth and financial performance highlight strong market momentum. Hempel A/S reported €750 million in marine sales for 2025, achieving 9.8% organic growth, and launched its “Accelerate to Win” strategy, prioritizing marine maintenance and newbuild segments in Asia. Similarly, PPG Industries reported record financial performance in 2025, with its Protective and Marine Coatings division identified as a key growth driver due to strong demand for technology-advantaged, fuel-saving coatings.

Sustainability validation is becoming a core differentiator. In February 2026, Jotun released a DNV-verified report confirming that vessels coated with its solutions achieved 11.8 million tonnes of avoided CO₂ emissions in 2025, highlighting the tangible environmental impact of advanced marine coatings and hull performance systems. Complementing this, Nippon Paint’s February 2026 strategy update outlines a shift toward increasing its marine and industrial coatings portfolio, targeting high-end shipbuilding and non-residential applications.

Technological innovation is accelerating performance improvements. Nippon Paint Marine’s July 2025 launch of HydroSmoothXT, a biomimetic antifouling coating, delivers up to 8% drag reduction, directly supporting compliance with EU ETS regulations. AkzoNobel’s December 2025 partnership with Winning Shipping further reinforces this trend through the deployment of Intersleek 1100SR and Intercept 8500 LPP coatings in large-scale drydocking projects, emphasizing low-friction, slime-release technologies.

Advancements in safety and specialized applications are also shaping the market. AkzoNobel’s Chartek 1709 certification milestone in September 2025—the first system approved for jet fire protection in marine cryogenic spill scenarios—addresses critical safety requirements in the rapidly expanding LNG carrier market. Meanwhile, PPG Industries’ global expansion of electrostatic coating application technology in April 2025 enhances coating uniformity and reduces VOC emissions by up to 35%, improving both environmental performance and operational efficiency.

Integrated service solutions are gaining traction as well. Jotun’s Hull Skating Solutions (HSS), which combines robotic hull cleaning with advanced coatings, reached its 100th commercial installation in January 2025, underscoring the shift toward continuous hull performance management systems.

Market Trend: Silicone-Based Foul-Release Coatings Accelerating Compliance with IMO CII and Biofouling Regulations

The marine coatings industry is undergoing a decisive transition toward silicone-based foul-release coatings (FRCs), driven by decarbonization mandates and evolving biofouling compliance frameworks under the International Maritime Organization’s Carbon Intensity Indicator (CII) and the revised 2025 Biofouling Guidelines. Unlike conventional self-polishing copolymer (SPC) systems that rely on controlled biocide release, silicone FRCs utilize ultra-low surface energy to prevent permanent organism adhesion, enabling passive fouling control without environmental discharge.

From an operational efficiency standpoint, these coatings deliver measurable hydrodynamic benefits. Field data from 2025 indicates that silicone-based systems reduce hull-induced drag by 8% to 12%, directly translating into equivalent reductions in fuel consumption and CO₂ emissions. This performance improvement is particularly critical for vessel operators targeting compliance with tightening carbon intensity benchmarks and fuel efficiency targets across global shipping routes.

Lifecycle performance is also a major differentiator. Advanced silicone FRC systems now support extended dry-docking intervals of 90 to 120 months, significantly surpassing the conventional 60-month maintenance cycle associated with copper-based coatings. This extension allows shipowners to reduce the frequency of dry-docking events, optimize fleet utilization, and lower total maintenance costs. Adoption trends reflect this shift, with industry surveys indicating that nearly 50% of shipowners have already updated their biofouling management strategies to align with IMO requirements. Within this cohort, there is a clear preference for biocide-free silicone technologies, particularly for vessels operating at high utilization rates exceeding 75% time at sea, where continuous movement enhances foul-release performance.

Market Trend: Ultra-High-Build Epoxy Coatings Transforming VLCC Cargo Tank Maintenance Efficiency

In parallel with hull coating innovations, the marine coatings market is seeing strong adoption of ultra-high-build (UHB) epoxy coatings in Very Large Crude Carrier (VLCC) cargo tanks. This shift is driven by the need to reduce maintenance downtime, improve operational flexibility between crude grades, and streamline shipyard processes during scheduled dry-docking.

UHB epoxy coatings enable single-coat application at dry film thickness levels of 500 to 600 microns, eliminating the need for multiple coating layers traditionally required in phenolic epoxy systems. This capability significantly accelerates application timelines, reducing coating process duration by approximately 35% to 45%. The elimination of intermediate curing stages further enhances productivity within shipyard environments, where time efficiency directly impacts operational costs.

Performance data from 2025 dry-docking cycles highlights the tangible benefits of this transition. VLCCs utilizing UHB epoxy tank linings achieved a reduction of approximately four days in total shipyard turnaround time compared to vessels coated with conventional systems. This reduction is highly significant in the context of large tanker operations, where daily charter rates and operational downtime represent substantial financial exposure. In addition to speed, UHB coatings improve tank cleanability, enabling faster turnaround between cargo types and reducing contamination risks. These advantages are positioning ultra-high-build epoxy systems as a preferred solution for next-generation tanker maintenance strategies.

Market Opportunity: DDG(X) Naval Program Creating Demand for Long-Life, Lightweight Marine Coating Systems

The United States Navy’s DDG(X) next-generation destroyer program is emerging as a high-value opportunity segment within the marine coatings market, particularly for advanced protective systems designed to meet stringent durability, weight, and performance requirements. With procurement expected to begin in the early 2030s, coating specifications are already being defined to support extended service life and enhanced operational capabilities.

A key requirement is the development of coating systems capable of withstanding 15 to 20 years of topside exposure without requiring full substrate recoating. This represents a significant increase from the current 10-year maintenance cycle observed in existing destroyer classes. Achieving this level of durability necessitates advancements in corrosion-resistant epoxy primers, UV-stable topcoats, and multi-functional barrier systems that can endure prolonged exposure to aggressive marine environments.

Weight optimization is another critical parameter influencing coating development. Next-generation coating systems are being engineered to reduce total coating weight by approximately 15%, contributing to overall vessel efficiency and supporting the integration of high-demand electrical systems such as Integrated Power Systems (IPS). Additionally, coatings designed for acoustic stealth and reduced radar signature are gaining importance, requiring precise control over surface smoothness and material composition. This convergence of durability, weight reduction, and stealth functionality is creating a specialized niche for high-performance marine coatings in defense applications.

Marine Coatings Market Share and Segmentation Insights

Cargo Ship Coatings Account for 42% Share Driven by Massive Shipping Volume and Fuel Efficiency Gains

The marine coatings market by application is led by cargo ships, holding 42% of the global market share in 2025, primarily due to their dominance in international trade logistics. Container ships, bulk carriers, and oil tankers collectively represent over 80% of global shipping tonnage, requiring extensive use of antifouling coatings, anticorrosive marine coatings, ballast tank coatings, and cargo hold linings for both new builds and maintenance cycles. High-performance solutions such as silicone foul-release coatings and self-polishing copolymer (SPC) systems are increasingly adopted to reduce hydrodynamic drag. Even a 1–2% improvement in fuel efficiency can generate millions in annual savings for fleet operators, making advanced coatings a critical operational investment. This strong link between global trade expansion, fuel cost optimization, and coating performance firmly establishes cargo ships as the largest application segment.

Maintenance and Repair Holds 62% Share Supported by Dry Dock Cycles and Aging Fleet

In the marine coatings market by end-use, maintenance and repair dominate with a 62% market share in 2025, reflecting the recurring nature of vessel upkeep and regulatory compliance requirements. Commercial ships typically undergo dry docking every five years (approximately 60 months), during which full hull recoating, antifouling application, and topside maintenance are performed. This scheduled maintenance cycle ensures consistent demand for marine protective coatings, corrosion-resistant systems, and ballast tank coatings regardless of fluctuations in new shipbuilding activity. Additionally, the aging global fleet—often exceeding 20 years for tankers and bulk carriers— requires more frequent coating interventions to address corrosion, wear, and compliance with standards such as IMO PSPC (Performance Standard for Protective Coatings). This combination of mandatory maintenance cycles and fleet aging solidifies maintenance and repair as the dominant and most stable revenue-generating segment.

Competitive Landscape in the Marine Coatings Market

AkzoNobel strengthens digital marine coatings leadership with sustainability-driven innovations

AkzoNobel, through its International® brand, remains the global benchmark in marine coatings, combining sustainability with digital hull monitoring technologies. The company is progressing toward a strategic merger with Axalta, expected to close in late 2026, creating a global coatings leader with an EBITDA margin exceeding 16%. In Q1 2026, AkzoNobel reported €345 million in adjusted EBITDA with a margin of 14.5%, supported by portfolio optimization and divestments in India and Pakistan. Its Intersleek® series, a pioneer in biocide-free fouling release coatings, can reduce fuel consumption and CO₂ emissions by up to 9%. The Intertrac® HullMS platform further enhances performance by enabling real-time CII compliance tracking through big data analytics.

Jotun leads marine coatings innovation with robotic hull cleaning and SPC technology

Jotun dominates the marine coatings market, particularly in newbuilding and drydocking segments, with strong exposure to the Asia-Pacific region, which accounts for over 50.5% of global shipbuilding orders. The company is a leader in self-polishing antifouling (SPC) coatings, with its SeaQuantum series utilizing advanced silyl acrylate chemistry to deliver ultra-low friction performance. Jotun’s HullSkater technology represents a major innovation, enabling robotic hull grooming to prevent biofilm formation and maintain optimal vessel efficiency. Through its Hull Performance Solutions (HPS), the company integrates coatings, sensors, and ISO 19030-based performance guarantees. With a projected CAGR of 5.58% through 2034, Jotun is expanding its presence in offshore and energy infrastructure segments.

Hempel drives marine coating efficiency with low-emission and high-performance systems

Hempel A/S is emerging as a performance leader in marine coatings, delivering strong financial results through a focus on efficiency and sustainability. The company launched its “Accelerate to Win” strategy in 2026, reinforcing its commercial focus and operational excellence. Hempel achieved an adjusted EBITDA margin of 18.2%, alongside a 9.8% organic growth in its Marine segment, reaching €750 million. Its Hempaguard® coatings have enabled customers to reduce 35.9 million tonnes of CO₂ emissions, demonstrating the economic and environmental value of premium fouling release systems. The company is also on track to achieve a 90% reduction in Scope 1 and 2 emissions by late 2026, strengthening its position as a preferred partner for green shipping initiatives.

PPG enhances marine coatings performance with silicone technologies and regional expansion

PPG Industries is leveraging its advanced R&D capabilities to deliver high-performance marine coatings with aerospace-grade durability. Its SIGMAGLIDE® 1290 is a 100% silicone fouling release coating featuring surface regeneration technology, maintaining ultra-smooth finishes over extended service periods. In Q1 2026, PPG reported a 7% increase in net sales, with its Protective and Marine Coatings segment achieving its 12th consecutive quarter of volume growth. The company has expanded its presence in Asia-Pacific through a new manufacturing and R&D hub in Tianjin, China, aligning with the region’s dominance in shipbuilding. PPG has also introduced low-VOC, high-build primers that reduce coating cycles, lowering labor costs and emissions during drydocking operations.

Nippon Paint Marine advances hydrogel coatings for ultra-low friction vessel performance

Nippon Paint Marine is a technological leader in advanced antifouling coatings, particularly in North Asia’s shipbuilding hub. In 2026, the company introduced FASTAR, a next-generation hydrogel-based coating that reduces drag by trapping a water layer on the hull surface, preventing organism attachment. Nippon Paint is also expanding its global footprint through strategic M&A and asset consolidation, transitioning into a broader coatings platform with a market capitalization exceeding ¥2.3 trillion. The company leads in biocide-free coatings for leisure boats and cruise ships, where environmental regulations are most stringent. Its strategic focus on waterborne resin technologies and ROIC-driven acquisitions positions it for long-term growth in sustainable marine coatings.

Chugoku Marine Paints strengthens marine coatings specialization with polymer technology expertise

Chugoku Marine Paints (CMP) is a specialized player with a strong focus on marine coatings, which account for 87.9% of its total sales. This singular focus enables CMP to deliver highly specialized solutions for maritime asset protection. In 2026, the company revised its full-year outlook upward, citing strong performance in Europe and the United States, which now contribute 23.4% of total sales. Its SEAFLO NEO series utilizes advanced cross-linking polymer technology to provide long-lasting antifouling performance and improved fuel efficiency. CMP’s expertise in container coatings and industrial marine applications further strengthens its integrated vessel protection portfolio, positioning it as a key player in high-performance marine coating systems.

India’s Green Port Mandates Driving Demand for Cleaning-Resistant, Low-Friction Hull Coatings

India’s maritime regulatory framework is evolving rapidly, creating new growth opportunities for advanced marine coatings. The Ministry of Ports, Shipping and Waterways is implementing stricter biofouling management protocols as part of its “Green Port” initiative, with a focus on preventing the spread of Invasive Aquatic Species and improving port efficiency.

A key regulatory development is the introduction of mandatory biofouling inspections for foreign-flagged vessels calling at major Indian ports starting in 2026. This requirement is significantly increasing demand for coatings capable of withstanding frequent in-water cleaning operations using remotely operated vehicles. Coatings designed for high cleaning durability are gaining traction, as they maintain thickness and performance even after repeated mechanical cleaning cycles. Industry data indicates a 22% increase in demand for such “cleaning-hardy” coating systems as shipowners adapt to compliance requirements.

Operational implications are equally significant. Vessels classified as high-risk for biofouling face potential berthing delays and financial surcharges, directly impacting turnaround times and port efficiency. This is incentivizing operators to invest in premium low-friction coatings that minimize fouling accumulation and facilitate rapid inspection clearance. The combination of regulatory enforcement, operational penalties, and environmental priorities is positioning India as a key emerging market for advanced marine coatings, particularly those offering durability, compliance, and hydrodynamic performance advantages.

South Korea Marine Coatings Market: Smart Shipbuilding and High-Performance Coating Innovation Hub

South Korea leads the global marine coatings market, driven by its dominance in LNG carriers, ammonia-ready vessels, and advanced shipbuilding technologies. The country is pioneering AI-driven smart coating application systems, particularly in Ulsan shipyards, where real-time environmental sensors optimize parameters such as spray viscosity and humidity. This ensures ultra-thin, uniform coating layers, enhancing durability and performance in harsh marine environments.

The commercialization of nano-structured hydrogel coatings, such as the Lo-Frick series, is significantly reducing frictional resistance and improving fuel efficiency for modern “Eco-Class” fleets. Infrastructure investments, including the expansion of Smart Surface Treatment Centers at HD Hyundai Heavy Industries, are boosting capacity for high-performance epoxy and polyurethane coatings. Government initiatives like the “K-Shipbuilding Strategy 2030” are further accelerating innovation in bio-inspired, low-friction coatings, while strict enforcement of environmental regulations is driving the transition toward waterborne and high-solid marine coatings.

China Marine Coatings Market: Graphene-Enhanced Protection and Sustainable Maritime Transition

China dominates the marine coatings market in terms of volume, supported by large-scale shipbuilding, offshore energy expansion, and strong government-backed sustainability initiatives. The country is transitioning from conventional coatings to graphene-enhanced marine coatings, offering significantly improved corrosion resistance and durability in saline environments.

Government mandates under the 14th Five-Year Plan are driving a shift toward low-VOC and electrostatic coating technologies, reducing emissions in shipyard operations. Investments in specialized facilities, such as Nippon Paint’s marine coating plant in Tianjin, are strengthening domestic production of copper-free antifouling coatings. China’s rapid growth in the offshore wind energy sector is also boosting demand for advanced “splash-zone” coatings capable of withstanding extreme environmental exposure. Additionally, regulatory updates are limiting the use of harmful biocides, accelerating the adoption of biocide-free foul-release systems and reinforcing China’s role as a leader in sustainable marine coatings innovation.

Norway Marine Coatings Market: Digital Hull Performance and Zero-Emission Marine Solutions

Norway is at the forefront of zero-emission marine coatings and digital hull performance technologies, redefining how coatings contribute to vessel efficiency and sustainability. Innovations such as robotic hull skaters are enabling proactive maintenance by cleaning hull surfaces without damaging coatings, significantly extending dry-docking intervals and reducing fuel consumption.

The country is leading the adoption of biocide-free silicone-based foul-release systems, which rely on surface physics rather than chemical toxicity to prevent marine growth. Government policies, including the “100% Emission-Free Public Tender Rule”, are accelerating the transition away from solvent-based coatings in public vessels. Norway’s integration of real-time hull performance monitoring systems with satellite data is enabling predictive maintenance and optimized vessel operations. These advancements are particularly critical for vessels operating in Arctic and environmentally sensitive regions, where strict environmental compliance is mandatory.

United States Marine Coatings Market: Defense Modernization and PFAS-Free Coating Transition

The United States marine coatings market is evolving through defense modernization programs and regulatory-driven innovation, particularly focusing on the elimination of harmful chemicals. Updates to the Toxic Substances Control Act (TSCA) are accelerating the phase-out of PFAS-containing additives, pushing manufacturers toward environmentally safe, high-performance coating formulations.

The U.S. Navy is increasingly adopting ultra-low friction coatings for submarine fleets, enhancing operational efficiency, fuel endurance, and acoustic stealth. Product innovations such as photodegradable biocides are reducing environmental impact while maintaining coating effectiveness. The adoption of electrostatic coating technologies in shipyards is improving application efficiency and reducing material waste. Additionally, infrastructure investments are supporting the refurbishment of bridges, lock-and-dam systems, and marine assets, driving demand for moisture-tolerant and rapid-application coatings. Expansion of R&D facilities by companies like Sherwin-Williams is further strengthening innovation in marine-grade coating technologies.

Singapore Marine Coatings Market: Global MRO Hub and Rapid-Return Coating Technologies

Singapore has established itself as a global hub for marine maintenance, repair, and overhaul (MRO), making it a key center for advanced marine coating applications and retrofit solutions. The country’s shipyards are experiencing strong growth in dry-docking activity, driven by compliance upgrades and the need for fuel-efficient coating systems.

Technological advancements include the adoption of underwater drone inspections, enabling real-time evaluation of coating integrity without disrupting vessel operations. Regulatory initiatives such as the Green Ship Programme are incentivizing the use of eco-friendly, high-performance coatings through port fee rebates. Singapore is also witnessing increased demand for coatings designed for high-impact environments, particularly in tanker and VLCC operations. Innovations in low-odor, solvent-free marine coatings are supporting rapid application in the region’s challenging climatic conditions, reinforcing Singapore’s role as a leading global retrofit hub.

Japan Marine Coatings Market: Nanotechnology and Long-Life Coating Systems for Advanced Marine Applications

Japan’s marine coatings market is characterized by advanced nanotechnology, precision engineering, and long-life coating systems, ensuring superior performance in demanding maritime environments. The development of nano-composite coatings with super-hydrophobic properties is enhancing resistance to fouling and mechanical wear, even under extreme operational conditions.

Innovations such as photocatalytic marine coatings are enabling self-cleaning surfaces that reduce maintenance requirements and environmental impact. Japan is also leading in the development of in-water application technologies, allowing for repairs without dry docking, significantly improving operational efficiency. Government initiatives under the “Blue-Growth Strategy” are supporting R&D for coatings used in autonomous vessels and advanced maritime systems. With strict regulatory compliance under the Chemical Substances Control Law (CSCL), Japan continues to push the adoption of sustainable, low-emission coating technologies, strengthening its position as a global innovator in marine coatings.

Marine Coatings Market Report Scope

Marine Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6 Billion

|

|

Market Size (2032)

|

$7.9 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Product Type (Anti-Fouling Coatings, Anti-Corrosion Coatings, Foul Release Coatings, Specialty Coatings), By Resin Type (Epoxy, Alkyd, Polyurethane, Acrylic, Fluoropolymer, Vinyl Ester, Bio-based Resins), By Technology (Solvent-borne Coatings, Water-borne Coatings, Radiation-Cured, Powder Coatings), By Application (Cargo Ships, Passenger Ships, Leisure Boats, Naval Vessels, Offshore Vessels, Offshore Structures), By End-Use (New Build, Maintenance and Repair), By Application Method (Airless Spraying, Conventional Spraying, Brush and Roller, Plural Component Spraying)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., Chugoku Marine Paints, Ltd., Nippon Paint Marine Coatings Co., Ltd., The Sherwin-Williams Company, Kansai Paint Co., Ltd., KCC Corporation, Axalta Coating Systems Ltd., BASF SE, RPM International Inc., Mapei S.p.A., Boero YachtCoatings, Advanced Polymer Coatings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Coatings Market Segmentation

By Product Type

- Self-Polishing Copolymer

- Ablative

- Hard Anti-Fouling

- Epoxy Coatings

- Polyurethane Coatings

- Zinc-Rich Primers

- Anti-Slip

- Potable Water Tank Linings

- Chemical and Cargo Tank Coatings

- Heat-Resistant

By Resin Type

- Epoxy

- Alkyd

- Polyurethane

- Acrylic

- Fluoropolymer

- Vinyl Ester

- Bio-based Resins

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Radiation-Cured

- Powder Coatings

By Application

- Cargo Ships

- Passenger Ships

- Leisure Boats

- Naval Vessels

- Offshore Vessels

- Offshore Structures

By End-Use

- New Build

- Maintenance and Repair

By Application Method

- Airless Spraying

- Conventional Spraying

- Brush and Roller

- Plural Component Spraying

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Marine Coatings Industry

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- Chugoku Marine Paints, Ltd.

- Nippon Paint Marine Coatings Co., Ltd.

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- KCC Corporation

- Axalta Coating Systems Ltd.

- BASF SE

- RPM International Inc.

- Mapei S.p.A.

- Boero YachtCoatings

- Advanced Polymer Coatings, Inc.

*- List not Exhaustive