Marine Anti-Fouling Coatings Market Size, Biofouling Control Technologies, and Maritime Decarbonization Outlook

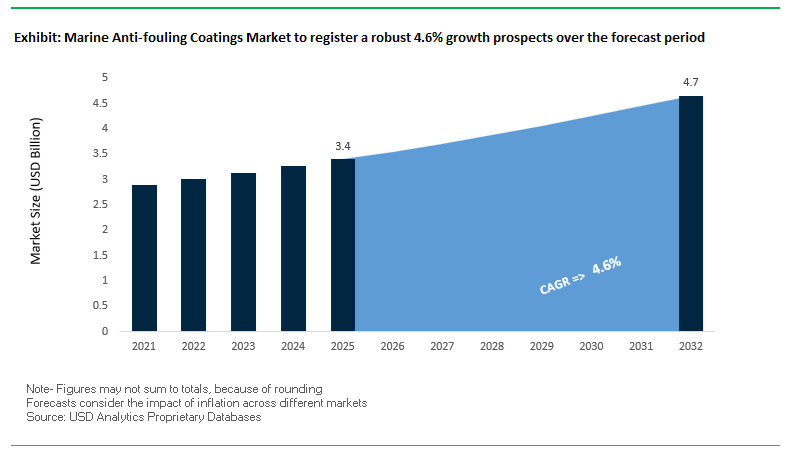

The global marine anti-fouling coatings market was valued at $3.4 billion in 2025 and is projected to reach $4.7 billion by 2032, expanding at a CAGR of 4.6%. Growth is being driven by increasing demand for antifouling coatings, foul-release coatings, biocide-free marine coatings, and low-friction hull coatings aimed at controlling biofouling, reducing hydrodynamic drag, and improving fuel efficiency. As global shipping faces tightening environmental regulations such as FuelEU Maritime and IMO Carbon Intensity Indicator (CII) standards, anti-fouling coatings are evolving into critical tools for emissions reduction and operational efficiency.

A key market driver is the direct relationship between biofouling accumulation and fuel consumption, where even minor hull roughness can significantly increase drag and energy usage. Advanced coatings such as silicone-based foul-release systems, silyl methacrylate self-polishing coatings, and slime-release technologies are enabling smoother hull surfaces and extended performance cycles. Additionally, the shift toward biocide-free and environmentally compliant coatings is accelerating due to stricter marine ecosystem protection regulations, particularly in Europe and North America.

The market is also benefiting from the growth of global shipping fleets, LNG carriers, cruise vessels, and offshore energy projects, where maintaining hull performance is critical for both cost efficiency and regulatory compliance. Innovations in coating application technologies, robotic hull cleaning systems, and integrated hull performance solutions are further enhancing the effectiveness of anti-fouling strategies. Regionally, Asia-Pacific dominates due to strong shipbuilding activity, while Europe leads in sustainability-driven marine coating innovations.

Market Analysis: Biocide-Free Innovation, Smart Hull Management Systems, and Strategic Expansion Driving Market Evolution

The marine anti-fouling coatings industry is undergoing a structural transformation driven by sustainability mandates, advanced coating chemistries, and integrated hull performance solutions. In March 2026, AkzoNobel secured a contract to supply advanced antifouling coatings for next-generation ferries, emphasizing low-emission operations and enhanced fuel efficiency through optimized hull smoothness. This highlights the increasing role of coatings in supporting energy-efficient vessel design.

Strategic repositioning toward high-performance marine coatings is evident across leading players. Hempel A/S, following its March 2026 transition to the “Accelerate to Win” strategy, is prioritizing high-performance marine coatings, supported by 9.8% organic growth in its marine segment in 2025. Similarly, Nippon Paint Marine’s February 2026 launch of next-generation antifouling coatings focuses on achieving ultra-low drag coefficients, enabling shipowners to meet stringent FuelEU Maritime and IMO CII targets.

Product innovation is increasingly centered on biocide-free and low-friction technologies. AkzoNobel’s Intersleek® 1100SR, deployed through its December 2025 agreement with Winning Shipping, represents a breakthrough in slime-release coating technology, offering effective biofouling control without relying on traditional biocides. Complementing this, Chugoku Marine Paints introduced SEAFLO NEO SL ZX in August 2025, utilizing silyl methacrylate hydrolysis technology for consistent polishing and long-term antifouling performance in deep-sea vessels. Additionally, CMP’s BIOCLEAN PLUS, launched in May 2025, leverages silicone-based surface tension modification to prevent organism attachment, further advancing environmentally friendly antifouling solutions.

Technological integration is also reshaping hull maintenance practices. Jotun’s Hull Skating Solutions (HSS), commercially rolled out in January 2025, combines robotic hull cleaning with advanced coating systems, enabling proactive removal of biofouling and maintaining zero speed loss. This represents a shift toward continuous hull performance management rather than periodic maintenance cycles. Similarly, PPG Industries’ electrostatic coating application technology, expanded globally in April 2025, enhances coating uniformity while reducing overspray and VOC emissions by up to 35%, improving both environmental performance and application efficiency.

Innovation in marine coatings is also supporting next-generation vessel technologies. AkzoNobel’s involvement in the world’s first sail-assisted Aframax tanker project in July 2025 demonstrates how low-friction antifouling coatings can enhance the efficiency of wind-assisted propulsion systems, reducing overall fuel consumption.

New product development is further strengthening market competitiveness. Hempel’s Hempaguard NB, launched in March 2025, provides fuel-saving performance from the first operational cycle, targeting the marine newbuild segment, where lifecycle efficiency is critical.

Market Trend: Commercial Shipping Industry Accelerating Transition to Silicone-Based Foul-Release Coatings for Fuel Efficiency and Compliance

The marine anti-fouling coatings market is undergoing a structural transformation as commercial fleet operator transition from traditional biocidal self-polishing copolymer (SPC) systems to advanced silicone-based foul-release coatings. This shift is strongly aligned with tightening International Maritime Organization (IMO) biofouling management frameworks for 2025 and 2026, which are increasingly emphasizing non-toxic, low-leach coating technologies to reduce environmental impact while enhancing vessel efficiency.

Silicone-based foul-release systems deliver significant hydrodynamic advantages by creating ultra-smooth hull surfaces that minimize biofouling adhesion and reduce drag. Performance benchmarks indicate drag reduction levels of 8% to 12% compared to conventional copper-based coatings, translating into substantial fuel cost savings. For large vessels such as Capesize bulk carriers, this equates to annual fuel savings in the range of $450,000 to $600,000, making these coatings a critical lever in decarbonization strategies and operational cost optimization.

Adoption rates are accelerating rapidly across newbuild vessels. As of early 2026, approximately 32% of global container and cargo ship orders specify biocide-free silicone or fluoropolymer-based systems, a significant increase from sub-10% penetration levels observed a decade earlier. This shift reflects both regulatory pressure and a growing recognition of lifecycle cost benefits. In addition to fuel savings, silicone coatings offer extended operational longevity, with service life cycles ranging from 90 to 120 months. This nearly doubles the conventional 60-month dry-docking intervals associated with copper-based systems, reducing maintenance frequency and improving fleet availability. These performance and economic advantages are positioning foul-release coatings as a core technology in next-generation sustainable shipping.

Market Trend: Naval Fleet Modernization Leveraging Biocide-Free Coatings for Acoustic Stealth and Structural Integrity

Naval forces globally are integrating biocide-free foul-release coatings into fleet modernization programs, driven by a combination of environmental compliance and operational performance requirements. Beyond regulatory considerations, a key driver is the enhancement of acoustic stealth capabilities. The ultra-smooth surface profile of foul-release coatings reduces cavitation and hydrodynamic noise, which is critical for maintaining low detectability in advanced naval operations.

Recent naval testing conducted in 2025 highlights significant material performance improvements. Biocide-free foul-release coatings demonstrate up to 90% reduction in localized corrosion rates over extended immersion periods of 50 weeks compared to untreated steel surfaces. This corrosion resistance is particularly valuable in harsh marine environments where hull degradation can compromise structural integrity and increase maintenance costs.

Operational efficiency gains are also substantial. Naval vessels coated with advanced foul-release systems report a 46% improvement in overall vessel performance metrics, including propulsion efficiency and maneuverability. Additionally, there is a 59% reduction in the frequency of emergency underwater hull cleaning during deployment cycles. This reduction in maintenance interventions enhances mission readiness and reduces logistical complexity, particularly during extended operations in remote or contested maritime regions.

The convergence of stealth optimization, corrosion mitigation, and maintenance efficiency is driving sustained adoption of biocide-free coating systems across naval fleets, reinforcing their role as a strategic material technology in modern defense maritime infrastructure.

Market Opportunity: European Regulatory Restrictions on Biocidal Coatings Unlocking Demand for DIY-Friendly Biocide-Free Solutions in Leisure Marine Segment

The European marine coatings market is entering a phase of regulatory-driven transformation, particularly within the leisure boating segment. Updated frameworks under the Urban Wastewater Treatment Directive and national-level regulations such as the Chemicals Prohibition Ordinance are imposing strict limitations on the use and distribution of biocide-heavy anti-fouling coatings. These policies are significantly altering purchasing behavior among private boat owners and marina operators.

One of the most immediate impacts is the restriction of point-of-sale access to high-biocide coatings for non-professional users. Under 2025 and 2026 mandates, self-service sales of such coatings are limited, creating a strong shift toward user-friendly, non-toxic alternatives. This regulatory change has triggered a 68% increase in demand for DIY-compatible biocide-free coatings across Europe’s estimated 6 million pleasure craft. Manufacturers are responding by developing easy-application foul-release systems and hydrogel-based coatings that offer effective fouling resistance without environmental toxicity.

The broader environmental objective of these regulations is to significantly reduce marine pollution, particularly copper leachates and other micro-pollutants originating from recreational marinas. The revised directive targets a reduction of approximately 365,000 tons of waterborne pollutants by 2040, creating a long-term growth runway for non-leaching coating technologies. This regulatory environment is fostering innovation in eco-friendly formulations and expanding market opportunities for suppliers capable of delivering compliant, high-performance alternatives tailored to the leisure marine sector.

Marine Antifouling Coatings Market Share and Segmentation Insights

Commercial Vessels Dominate with 58% Share Fueled by Fuel Efficiency and Dry Dock Optimization

The marine antifouling coatings market by vessel type is led by commercial vessels, accounting for 58% of the global market share in 2025, driven by strong economic incentives tied to fuel efficiency and operational uptime. Advanced antifouling technologies such as silicone-based foul-release coatings, copper-free silyl acrylate systems, and self-polishing copolymers (SPC) are widely adopted across container ships, tankers, and bulk carriers to reduce hull drag. Even a 3–5% reduction in fuel consumption translates into millions of dollars in annual savings for large fleets, making premium coatings a strategic investment. Additionally, commercial vessels operate on strict 5-year dry docking cycles, requiring long-life antifouling coatings with 60–90 months durability to minimize downtime and maximize revenue generation. This combination of cost efficiency, regulatory compliance, and performance durability firmly establishes commercial shipping as the dominant segment.

Deep-Sea Operations Hold 55% Share Driven by High Fouling Pressure and Global Trade Volume

In the marine antifouling coatings market by operating environment, deep-sea vessels dominate with a 55% market share in 2025, reflecting the intense biofouling challenges encountered across global shipping routes. Ships operating in tropical and temperate waters face heavy accumulation of barnacles, algae, and mussels, which significantly increase hydrodynamic drag and reduce vessel efficiency. To counter this, operators rely on high-performance solutions such as SPC antifouling coatings and silicone-based foul-release systems that maintain hull smoothness and optimal speed. Furthermore, deep-sea shipping accounts for over 80% of global trade tonnage, including containerized goods, crude oil, and bulk commodities, making it the largest and most critical application segment. The scale of global maritime trade, combined with stringent performance requirements, ensures sustained demand for durable, fuel-efficient, and environmentally compliant antifouling coatings.

Competitive Landscape in the Marine Anti-Fouling Coatings Market

AkzoNobel strengthens digital antifouling leadership with AI-driven hull performance systems

AkzoNobel, through its International® brand, leads the marine anti-fouling coatings market by combining high-performance chemistry with advanced digital analytics. In 2026, the company partnered with Winning Shipping to accelerate low-carbon fleet operations through large-scale application of its coatings portfolio. Its Intertrac® HullMS platform leverages AI and big data to predict hull fouling rates, enabling shipowners to maintain optimal CII ratings. The Intersleek® series remains a flagship biocide-free solution, reducing hull drag and fuel consumption by up to 9%. With 2025 revenues of €10.16 billion and ongoing merger plans with Axalta targeting $600 million in synergies, AkzoNobel continues to strengthen its leadership in sustainable marine coatings.

Jotun leads self-polishing antifouling systems with robotic hull cleaning integration

Jotun dominates the marine coatings segment with its advanced self-polishing copolymer (SPC) technology, particularly in new-build vessels. Its SeaQuantum Ultra S coating utilizes silyl acrylate chemistry to deliver superior protection during extended idle periods, addressing challenges associated with port congestion. The company holds an estimated 43.4% share of the global marine coatings application market by product type, supported by its Hull Performance Solutions (HPS) guarantee. Jotun is also pioneering robotic hull cleaning through its HullSkater system, enabling proactive biofilm removal before macro-fouling occurs. Its SeaForce Active line, introduced in late 2025, incorporates a triple-biocide system designed to meet localized environmental regulations while maintaining extended service intervals of up to 90 months.

Hempel advances silicone-based fouling release systems and predictive maintenance services

Hempel is a key innovator in marine coatings, particularly in the development of silicone-based fouling release technologies and double-layer protection systems. The company reported strong profitability in 2025, supporting the launch of Hempaguard Ultima, a next-generation coating building on the success of Hempaguard X7 with over 4,000 applications. Hempel has achieved an EcoVadis Gold rating and is targeting a 50% reduction in carbon intensity by 2030 through green chemistry initiatives. Its coatings are widely used in deep-sea and container vessels due to their ability to significantly reduce frictional resistance. Through Hempel Services, the company integrates hull inspection and predictive maintenance tools to optimize drydocking schedules and enhance vessel efficiency.

PPG enhances marine coating efficiency with biocide-free and self-polishing technologies

PPG Industries is strengthening its position in the marine anti-fouling coatings market through its Sigma Coatings® brand, focusing on commercial shipping efficiency and environmental compliance. In February 2026, the company introduced a biocide-free antifouling system capable of improving fuel efficiency by up to 8.5% for cargo fleets. Its SIGMAGLIDE® coatings utilize hydrolysis-based self-polishing mechanisms to maintain smooth hull surfaces even during prolonged idle conditions. PPG’s $380 million investment in manufacturing upgrades and its marine performance center in Tianjin reflect its commitment to the Asia-Pacific region, which accounts for over 50% of global shipbuilding orders. Additionally, its coatings have achieved UL GREENGUARD certification, reinforcing its leadership in low-VOC marine solutions.

Nippon Paint Marine pioneers hydrogel antifouling coatings for ultra-low drag performance

Nippon Paint Marine is a technological leader in hydrogel-based antifouling coatings, focusing on ultra-low friction surfaces for modern vessels. In March 2026, the company launched FASTAR, a next-generation coating that uses hydrogel technology to create a water-trapping surface, preventing marine organisms from adhering. Building on its legacy of ECOLOFLEX, the first tin-free hydrolyzing self-polishing coating, Nippon Paint continues to innovate with HydroSmoothXT™ technology for drag reduction. The company holds a strong position in Japanese and South Korean shipbuilding markets, which dominate global new-build activity. Its strategic focus extends to preventing the spread of invasive aquatic species, aligning coating performance with broader environmental protection objectives.

Chugoku Marine Paints expands high-performance antifouling solutions with polymer innovation

Chugoku Marine Paints (CMP) is a specialized player in high-performance marine coatings, focusing on advanced polymer technologies for vessel protection. The company reported revenues of approximately $916 million in 2025 and a market capitalization of $1.01 billion in 2026, reflecting steady growth in global markets. Its SEAFLO NEO CF PREMIUM coating utilizes unique cross-linking polymer chemistry to extend service life while significantly reducing fuel consumption for large bulk carriers. CMP’s expertise extends to cargo hold and ballast tank coatings, ensuring compliance with PSPC standards and offering a comprehensive vessel protection portfolio. The company is also expanding its water-based and solvent-free coatings to meet tightening global VOC regulations, strengthening its position in environmentally compliant marine solutions.

China’s Environmental Mandates Driving Large-Scale Transition to Copper-Free Anti-Fouling Systems in Commercial and Aquaculture Vessels

China’s regulatory landscape is emerging as a dominant force shaping the global marine anti-fouling coatings market. The revision of GB/T 6822-2025 introduces stringent environmental controls on coating emissions and biocide leaching, particularly in ecologically sensitive regions such as the Yangtze River Delta. These regulations are accelerating the transition toward low-copper and copper-free coating systems across both commercial shipping and inland waterway fleets.

The Asia-Pacific region already accounts for approximately 56.5% of global anti-fouling coating demand, and China’s policy direction is reinforcing its leadership in the adoption of environmentally compliant technologies. With green coating adoption growing at an annual rate of 10.2%, suppliers operating in this market are increasingly required to align with copper-free and non-toxic formulation standards to remain competitive.

A critical driver within this transition is the protection of China’s aquaculture industry, which exceeds $150 billion in economic value. New coastal regulations impose near-zero copper leach rate limits in aquaculture zones, effectively mandating the use of advanced biocide-free foul-release coatings for support vessels and infrastructure operating in these areas. This requirement is creating a substantial demand pipeline for innovative coating technologies that can deliver effective biofouling control without compromising marine ecosystems.

The combination of regulatory enforcement, environmental protection priorities, and large-scale industrial demand is positioning China as a central growth engine for next-generation anti-fouling coatings, with significant implications for global supply chains, product innovation, and competitive dynamics.

South Korea Marine Anti-Fouling Coatings Market: Smart Shipbuilding and AI-Driven Coating Precision

South Korea stands as the global epicenter for high-performance marine anti-fouling coatings, driven by its leadership in LNG carriers, ultra-large container ships (ULCS), and advanced shipbuilding technologies. The country is pioneering nano-hydrogel-based antifouling coatings, such as KCC’s Lo-Frick series, which significantly reduce hull friction and improve vessel fuel efficiency. These advanced coatings create ultra-smooth surfaces that minimize biofouling and optimize hydrodynamic performance, making them essential for high-value vessels.

The integration of AI-driven formulation systems and robotic coating technologies in smart shipyards across Ulsan and Geoje is transforming application precision and operational efficiency. Automated hull coating systems ensure uniform film thickness, a critical factor for long-term coating performance. Government-backed initiatives such as “Green Shipbuilding” are promoting the adoption of eco-friendly, ultra-low VOC antifouling coatings, supported by tax incentives. South Korea’s focus on specialized vessels, including LNG and ammonia carriers, further drives demand for coatings that maintain performance during extended idle periods and complex operational cycles.

China Marine Anti-Fouling Coatings Market: Green Chemistry and Offshore Wind Expansion Driving Growth

China’s marine anti-fouling coatings market is undergoing a major transformation, fueled by green chemistry initiatives and large-scale maritime infrastructure expansion. Under the 14th Five-Year Plan, the government is actively promoting the transition away from traditional biocide-based coatings, particularly copper-based formulations, in favor of environmentally sustainable alternatives.

Technological advancements include the rapid scaling of graphene-enhanced antifouling coatings, which offer superior mechanical strength and disrupt biofouling at a molecular level. Innovations in biomimetic coatings, inspired by marine organisms such as sharks, are enabling non-toxic solutions that prevent bio-settlement without chemical leaching. China is also investing heavily in production capacity, with major expansions in Yantai and Shanghai supporting Asia-Pacific demand. The market is further driven by the offshore wind energy sector, where coatings must withstand decades of exposure to harsh marine environments. Strict regulatory standards are reinforcing the adoption of low-leach-rate, eco-compliant coatings, positioning China as a leader in sustainable marine coating technologies.

Norway Marine Anti-Fouling Coatings Market: Digital Hull Performance and Zero-Emission Innovation

Norway is redefining the marine anti-fouling coatings market through its focus on digital hull performance optimization and zero-emission shipping technologies. The commercialization of Hull Skating Solutions (HSS), which deploy robotic cleaners to maintain hull efficiency without damaging coatings, represents a paradigm shift in marine maintenance. These systems are reducing fuel consumption and emissions, aligning with global decarbonization goals.

The country’s investment in AI-driven hull performance monitoring platforms, combined with satellite data analytics, is enabling predictive maintenance and optimized vessel operations. Government support through initiatives such as the NOx Fund is encouraging the adoption of high-performance foul-release coatings. Norway is also leading in the development of 100% biocide-free silicone coatings, which rely on surface physics rather than chemical toxicity to prevent marine growth. These innovations are particularly critical for vessels operating in environmentally sensitive Arctic and fjord regions, where strict compliance with IMO biofouling guidelines is mandatory.

Japan Marine Anti-Fouling Coatings Market: Nanotechnology and Long-Life Coating Systems

Japan’s marine anti-fouling coatings market is characterized by advanced material science, nanotechnology integration, and long-life coating systems. The development of silyl acrylate polymers enables controlled self-polishing coatings that extend dry-docking intervals significantly, reducing maintenance costs and operational downtime for shipping fleets.

Innovations such as photocatalytic coatings, which use sunlight to break down organic matter, are enhancing coating performance in harsh marine environments. Japan is also leading in the development of in-water repair coatings, allowing maintenance to be conducted without dry docking, significantly improving operational efficiency. The market is supported by government initiatives promoting low-friction coatings to reduce carbon emissions, particularly in domestic ferry operations. With strong R&D investments by companies like Nippon Paint Marine, Japan is also advancing coatings for autonomous vessels, where long-term durability and minimal maintenance are essential.

Singapore Marine Anti-Fouling Coatings Market: Global MRO Hub and Rapid-Return Coating Technologies

Singapore has established itself as a global hub for marine maintenance, repair, and overhaul (MRO), making it a key market for advanced anti-fouling coatings. The country’s shipyards, particularly in Tuas and Jurong, are at the forefront of adopting digital hull monitoring systems, enabling real-time assessment of coating performance using underwater drone technology.

The Green Port Programme, introduced by the Maritime and Port Authority (MPA), is incentivizing shipowners to adopt environmentally friendly coatings, including foul-release systems that improve fuel efficiency and reduce emissions. Singapore’s growing dry-docking throughput is driven by compliance with Carbon Intensity Indicator (CII) regulations, which require vessel operators to upgrade coating systems for improved efficiency. Innovations such as low-odor, solvent-free antifouling coatings are particularly suited for the region’s high-temperature and high-humidity conditions, supporting rapid application and reduced downtime.

Netherlands Marine Anti-Fouling Coatings Market: Offshore Wind Innovation and Sustainable Maritime Solutions

The Netherlands is emerging as a leader in marine anti-fouling coatings for offshore energy and sustainable shipping applications, driven by its strong focus on the energy transition and circular maritime economy. Technological breakthroughs in hydrogel-silicone hybrid coatings, such as Hempel’s Hempaguard series, are enabling long-term fouling resistance even during extended idle periods.

Government initiatives, including the Dutch Offshore Wind Innovation Guide, are supporting the adoption of sensor-integrated coatings that provide real-time data on corrosion and fouling. These smart coatings are critical for maintaining offshore wind turbine foundations and subsea infrastructure. Strict enforcement of the EU Biocidal Products Regulation (BPR) is pushing the industry toward eco-friendly formulations, reducing reliance on harmful biocides. The market is also benefiting from investments in sustainable propulsion technologies, where low-friction coatings are combined with wind-assisted propulsion systems to achieve near-zero emissions. Key applications include dredging vessels and offshore construction equipment, which require coatings that balance durability with environmental performance.

Marine Anti-fouling Coatings Market Report Scope

Marine Anti-fouling Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2032)

|

$4.7 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Copper-based, Biocide-Free, Co-Biocide Systems, Organometallic, Biomimetic and Natural-Based), By Technology (Solvent-borne, Water-borne, Solvent-Free), By Vessel Type (Commercial Vessels, Passenger and Leisure, Naval and Defense, Specialized Vessels), By Application Area (Underwater Hull, Boottop and Topsides, Internal Tanks and Ballast Systems, Niche Areas), By End-Use Sector (Newbuild, Repair and Maintenance), By Operating Environment (Deep Sea, Coastal, Stationary, Arctic)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., Jotun A/S, Hempel A/S, PPG Industries, Inc., Chugoku Marine Paints, Ltd., Nippon Paint Marine Coatings Co., Ltd., Kansai Paint Co., Ltd., Sherwin-Williams Marine Coatings, KCC Corporation, Axalta Coating Systems Ltd., RPM International Inc., BASF SE, Transocean Coatings, Boero YachtCoatings, Wilckens Vertriebsgesellschaft mbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Marine Anti fouling Coatings Market Segmentation

By Type

- Copper-based

- Biocide-Free

- Co-Biocide Systems

- Organometallic

- Biomimetic and Natural-Based

By Technology

- Solvent-borne

- Water-borne

- Solvent-Free

By Vessel Type

- Commercial Vessels

- Passenger and Leisure

- Naval and Defense

- Specialized Vessels

By Application Area

- Underwater Hull

- Boottop and Topsides

- Internal Tanks and Ballast Systems

- Niche Areas

By End-Use Sector

- Newbuild

- Repair and Maintenance

By Operating Environment

- Deep Sea

- Coastal

- Stationary

- Arctic

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Marine Anti fouling Coatings Industry

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- PPG Industries, Inc.

- Chugoku Marine Paints, Ltd.

- Nippon Paint Marine Coatings Co., Ltd.

- Kansai Paint Co., Ltd.

- Sherwin-Williams Marine Coatings

- KCC Corporation

- Axalta Coating Systems Ltd.

- RPM International Inc.

- BASF SE

- Transocean Coatings

- Boero YachtCoatings

- Wilckens Vertriebsgesellschaft mbH

*- List not Exhaustive