Production Chemicals Market Valued at $15.8 Billion in 2025, Projected to Reach $27.4 Billion by 2034 at 6.3% CAGR

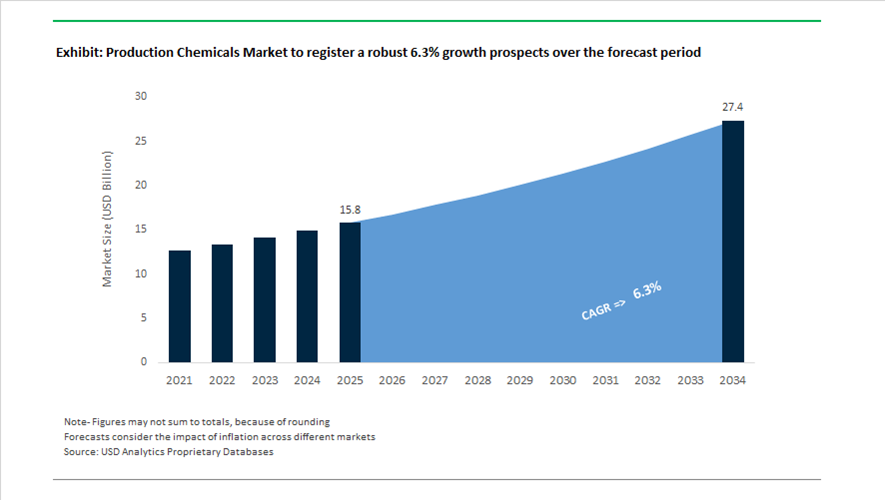

The global production chemicals market is valued at $15.8 billion in 2025 and is projected to reach $27.4 billion by 2034, expanding at a CAGR of 6.3%. Growth is driven by rising demand for corrosion inhibitors, demulsifiers, scale inhibitors, coagulants, dispersants, production fluids, artificial lift chemicals, and high-purity process additives across upstream oil and gas, downstream refining, petrochemicals, desalination, metals processing, and semiconductor manufacturing. Increasing digitalization of chemical dosing systems, offshore field maturity, refinery optimization programs, and industrial water reuse mandates are accelerating adoption of performance-driven and AI-optimized production chemical solutions.

Strategic consolidation reshaped the competitive landscape in 2025. In March 2025, Honeywell acquired Sundyne for $2.16 billion, integrating high-pressure pump technologies with chemical dosing and flow control systems for petrochemical and refining clients. In July 2025, SLB finalized its $7.8 billion all-stock acquisition of ChampionX, forming the world’s largest integrated production chemistry platform under its Production Systems division. The transaction merges artificial lift technologies with chemical treatment portfolios, enabling bundled service offerings for offshore and mature fields. In late 2025, Ecolab acquired Ovivo’s electronics ultrapure water division, strengthening its position in semiconductor fabrication where high-purity production chemicals are essential for wafer processing and contamination control.

Digital chemical optimization became a focal point in 2025. Following the ChampionX acquisition, SLB launched an AI-enabled production chemical management platform that uses real-time field sensors to automate dosing of corrosion inhibitors and demulsifiers, reducing chemical consumption by up to 20% in mature offshore assets. In late 2025, BASF introduced Sokalan DCS, a high-performance dispersant engineered to prevent mineral scaling in membrane-based desalination and high-temperature industrial water systems, improving operational uptime in production facilities. Earlier, in August 2024, Nalco Water signed a strategic cooperation agreement with Danieli to develop chemicals aimed at reducing water and carbon footprints in steel production, linking metallurgy and industrial process chemistry.

Expansion into 2026 reflects deeper integration of sustainability and localization strategies. In January 2026, Halliburton and Singapore’s A*STAR launched the NEX Lab℠, focused on next-generation well completion fluids and specialty production chemicals for energy applications. In February 2026, Baker Hughes entered a multi-year agreement with Marathon Petroleum to supply downstream chemicals across 12 refineries, introducing XERIC™ heavy oil demulsifiers and TOPGUARD™ corrosion inhibitors integrated with digital monitoring platforms. In the same month, Kemira completed the acquisition of SIDRA Wasserchemie, expanding its European footprint in inorganic coagulants and industrial production chemicals. Also in February 2026, India allocated ₹600 crore under its Union Budget to establish three Chemical Parks, creating plug-and-play infrastructure for localized manufacturing of bulk and specialty production chemicals. At the start of 2026, Clariant expanded its bio-based Licocare RBW Vita additives derived from rice bran wax, offering renewable processing aids for polymers and industrial coatings.

The production chemicals market is increasingly characterized by AI-driven dosing optimization, integrated artificial lift and chemical service bundles, refinery-scale corrosion inhibitor contracts, high-performance desalination dispersants, bio-based production additives, semiconductor-grade ultrapure chemicals, and government-backed localization initiatives. Consolidation among oilfield service leaders, digital transformation of chemical management systems, and decarbonization efforts across refining and metals processing are reshaping global competitive dynamics.

Key Trends and High-Impact Opportunities in the Production Chemicals Market

Accelerated Pivot to Bio-Based and Low-Carbon Production Chemistries

The production chemicals market is undergoing a structural reset as upstream operators embed carbon intensity and environmental toxicity into procurement decisions. What began as pilot sustainability initiatives has evolved into formal supplier qualification criteria, forcing chemical manufacturers to redesign portfolios around biodegradable, low-toxicity, and lower-carbon-intensity formulations. Traditional aromatic solvents and persistent synthetic inhibitors are increasingly being replaced by bio-sourced scale inhibitors, green corrosion inhibitors, and next-generation demulsifiers that can withstand high salinity and elevated reservoir temperatures without compromising environmental compliance.

This transition is strongly reinforced by capital allocation strategies at the operator level. In April 2025, ExxonMobil outlined plans to deploy up to USD 30 billion in lower-emission investments through 2030, with molecule optimization and emissions reduction embedded into industrial supply chains. Production chemicals sit directly within this scope, as they influence produced water toxicity, offshore discharge profiles, and methane intensity across the production lifecycle. As a result, chemical suppliers are now required to provide auditable lifecycle data, carbon footprint documentation, and biodegradability metrics as part of long-term supply agreements.

Environmental performance thresholds are also tightening. During 2024–2025, TotalEnergies formalized an upstream emissions intensity ceiling of 17 kg CO₂ per barrel of oil equivalent for new developments. This has created a direct incentive to deploy production chemical programs that reduce secondary emissions from water treatment, minimize hazardous discharge, and support methane mitigation strategies. In practice, this is accelerating adoption of green demulsifiers, low-zinc corrosion inhibitors, and enzyme-assisted formulations that deliver operational performance while lowering the environmental footprint of producing assets.

Rise of Digital Integration and Chemical Management as a Service (CMaaS)

The commercial model for production chemicals is shifting from volume-based supply to outcome-based performance delivery. Operators are increasingly outsourcing chemical optimization to suppliers under Chemical Management as a Service frameworks, where corrosion control, flow assurance, or scale mitigation are contracted as measurable outcomes rather than as chemical volumes. This shift is enabled by the rapid integration of Industrial Internet of Things platforms, automated dosing systems, and cloud-based analytics across mature and greenfield assets.

Late-2025 industry benchmarks indicate that Digital Oilfield implementations linked to chemical management can reduce total operating costs by up to 25%. AI-driven analytics continuously evaluate flow rates, pressures, water chemistry, and production profiles to optimize chemical injection in real time. These systems not only improve flow assurance and asset integrity but also reduce chemical overuse, delivering up to a 15% uplift in overall production efficiency while lowering chemical consumption intensity.

Operationally, real-time automation is redefining field logistics and safety. Modern chemical management platforms integrate satellite telemetry, GPS-enabled delivery tracking, and smart tank monitoring to create closed-loop injection systems. Solutions deployed by providers such as Nalco Water and Baker Hughes now automatically trigger replenishment schedules based on live inventory data, eliminating manual intervention in remote or offshore environments. This reduces personnel exposure, minimizes downtime caused by stockouts, and prevents costly failures linked to under- or over-dosing, reinforcing CMaaS as a core efficiency lever rather than a digital add-on.

Engineering Solutions for Ultra-HPHT and 20,000 PSI Reservoirs

As conventional reservoirs mature, capital is flowing into frontier developments characterized by extreme pressure and temperature conditions. Deepwater projects in the U.S. Gulf of Mexico and the North Sea are now operating at pressures approaching 20,000 psi and temperatures exceeding 400°F, fundamentally redefining performance requirements for production chemicals. In these environments, traditional polymer-based inhibitors rapidly degrade, creating a critical demand for chemically robust formulations with exceptional thermal and mechanical stability.

A defining inflection point occurred in August 2024 with the successful start-up of Chevron’s Anchor project, the first subsea development rated for 20,000 psi. With reservoir depths reaching 34,000 feet, the project established a new benchmark for chemical performance, requiring scale and corrosion inhibitors that maintain molecular integrity under prolonged exposure to extreme HPHT conditions. This has accelerated innovation in high-temperature polymer chemistry, advanced viscoplastic modeling, and compatibility testing with ultra-high-strength alloys used in next-generation wellheads and subsea infrastructure.

By 2025, R&D focus across the sector had expanded toward Extreme HPHT environments exceeding 260°C. Chemical suppliers are now engineering inhibitors and treatment packages that not only survive these conditions but also avoid inducing pitting, hydrogen embrittlement, or stress corrosion cracking in advanced metallurgy. This capability is becoming a decisive differentiator as more operators push into deepwater and ultra-deep reservoirs to sustain long-term production growth.

Strategic Expansion into Geothermal and CCUS Infrastructure

The global energy transition is unlocking structurally new demand for production chemistry beyond conventional oil and gas. Geothermal energy and Carbon Capture, Utilization, and Storage projects present complex fluid management challenges that closely mirror upstream production environments, positioning production chemical suppliers for adjacent-market expansion.

Geothermal power capacity reached 16,335 MW by the end of 2023, with aggressive expansion targets through 2030, including India’s stated ambition of 10,000 MW. These assets operate with highly corrosive, mineral-rich brines at elevated temperatures, creating demand for advanced silica scale inhibitors, H₂S scavengers, and corrosion protection systems. Suppliers such as Italmatch and Clariant are now deploying IoT-enabled chemical treatment programs in geothermal plants, allowing real-time adjustment of dosing strategies to manage scaling and corrosion while maximizing plant uptime.

CCUS infrastructure represents an even larger strategic opportunity. As ExxonMobil’s Low Carbon Solutions platform and Occidental’s net-zero initiatives scale toward capturing and storing billions of metric tons of CO₂, the chemical intensity of the value chain is rising sharply. Specialized amine-based solvents for CO₂ capture, corrosion inhibitors for dense-phase CO₂ pipelines, and chemical treatments for injection wells are becoming mission-critical components of CCUS economics. For production chemical manufacturers, this transition represents a multi-billion-dollar portfolio pivot, enabling long-term growth anchored in decarbonization rather than hydrocarbon volume expansion.

Production Chemicals Market Share and Segmentation Insights

Corrosion Inhibitors Lead Oilfield Chemical Treatment Programs for Asset Protection

Corrosion inhibitors accounted for 28.40% of the Production Chemicals Market by product type in 2025, reflecting their critical role in protecting pipelines, production tubing, separators, and processing equipment used in oil and gas operations. These chemicals prevent metal degradation caused by corrosive production fluids containing water, carbon dioxide, hydrogen sulfide, and dissolved salts. The high capital value of upstream infrastructure and the operational risks associated with corrosion damage continue to support strong demand for inhibitor treatment programs across global production fields. In 2025, advanced corrosion monitoring technologies are enabling optimized inhibitor injection strategies, allowing operators to adjust dosing rates based on real time corrosion data, fluid chemistry, and production conditions to improve protection efficiency and reduce chemical consumption.

Oil and Gas Production Operations Drive Global Demand for Production Chemicals

Oil and gas production represented 58.60% of the Production Chemicals Market by application in 2025, reflecting the continuous need for chemical treatment programs that maintain flow assurance, protect infrastructure, and optimize hydrocarbon recovery. Production facilities rely on corrosion inhibitors, scale inhibitors, demulsifiers, and biocides to control scaling, bacterial growth, emulsions, and deposition issues that can disrupt operations. The large scale of global upstream production activities continues to drive sustained consumption of oilfield production chemicals. In 2025, maturing unconventional oil and gas reservoirs are increasing chemical treatment complexity, as operators manage higher water cuts, scaling tendencies, and microbial contamination challenges requiring more advanced chemical treatment programs to maintain efficient hydrocarbon production.

Production Chemicals Market Competitive Landscape

The global production chemicals market in 2026 is shaped by consolidation, digital-chemical convergence, and automated injection systems. Companies are prioritizing ultra-deepwater flow assurance, low-carbon surfactants, and real-time subsurface analytics to enable recurring revenue models and optimize production efficiency in complex offshore environments.

SLB Redefines Production Chemistry with ChampionX Integration and Digital Twin Optimization

SLB has transformed into a production chemicals powerhouse following the July 2025 acquisition of ChampionX, integrating artificial lift and chemical technologies. The deal delivers $400 million in expected pretax synergies by 2028 and adds recurring high-margin chemical revenues. In 2025, SLB reported $35.71 billion in revenue despite a strategic 2% decline due to contract optimization. ChampionX’s HSCI38130A technology enables single-point injection for flow assurance, asset integrity, and H2S treatment, reducing downtime and footprint. The company is leveraging digital twins to optimize chemical dosing in real time, reducing Total Cost of Ownership (TCO). This positions SLB as the leader in automated, data-driven production chemistry solutions.

Halliburton Advances Digital Well Construction and Expands Chemical Capabilities in Global Energy Markets

Halliburton is strengthening its production chemicals portfolio through digital well construction and automation-driven fracturing technologies. In March 2026, it achieved the first fully automated closed-loop well placement in collaboration with ExxonMobil, integrating subsurface data with execution systems. The company reported Q4 2025 revenue of $5.7 billion, with $3.2 billion generated from its Completion and Production segment. Strategic expansion includes an MOU with Pertamina to scale unconventional fracturing in Indonesia. Halliburton is also entering geothermal and Direct Lithium Extraction (DLE) projects, diversifying its chemical expertise. This positions the company at the intersection of traditional oilfield chemistry and next-generation energy solutions.

Baker Hughes Expands Refining Chemistry Leadership with Strategic Contracts and Portfolio Optimization

Baker Hughes is focusing on downstream chemical technologies and energy transition infrastructure under its Industrial & Energy Technology (IET) segment. In February 2026, it secured a multiyear agreement with Marathon Petroleum covering 12 refineries and renewable fuel sites, deploying XERIC™ demulsifiers and BIOQUEST™ additives. The company reported record IET orders of $14.9 billion in 2025, contributing to a $35.9 billion RPO. It divested its PSI business for $1.15 billion to sharpen its focus on integrated chemical platforms. Its TOPGUARD™ corrosion inhibitors are widely used in high-temperature and sulfur-rich environments. Baker Hughes is positioning itself as a leader in refinery-focused production chemicals and digital monitoring integration.

BASF Strengthens Cost Leadership Through Verbund Integration and High-Purity Chemical Supply

BASF is leveraging its Verbund-integrated production model to maintain cost competitiveness in oilfield and production chemicals. The startup of its Zhanjiang Verbund site in 2026 enhances supply of high-purity intermediates despite increasing CO2 emissions during scale-up. The company projects EBITDA of €6.2 billion to €7.0 billion in 2026, driven by growth in Chemicals and Nutrition & Care segments. BASF completed divestiture of its decorative paints business, targeting €2.3 billion in cost savings by 2026. Its portfolio supports Enhanced Oil Recovery (EOR) through polyacrylamides and specialty surfactants. This integration enables BASF to remain a key upstream supplier in the global production chemicals value chain.

Clariant Accelerates Digital Oilfield Services with CLARITY Platform and Bio-Based Innovation

Clariant is positioning itself as a specialty leader in oilfield chemicals with a strong focus on digitalization and sustainability. The company achieved a 17.8% EBITDA margin in 2025, supported by CHF 50 million in cost savings from operational improvements. Its CLARITY™ digital platform expanded to over 800 users across 38 countries, optimizing chemical performance and catalyst management. Innovation sales reached 18.8%, driven by bio-based and EcoTain® solutions aligned with decarbonization goals. Clariant targets 4%–6% sales growth and EBITDA margins of up to 21% by 2027. This positions the company as a digital-first provider of sustainable production chemistry solutions.

Evonik Focuses on Specialty Oilfield Chemicals and Organizational Agility Through Strategic Restructuring

Evonik is advancing its position in specialty production chemicals through its “Custom Solutions” strategy and portfolio optimization. The company reported €1.87 billion EBITDA in 2025 and targets up to €2.0 billion in 2026, supported by a dynamic dividend policy. It is focusing on improving Return on Capital Employed (ROCE), targeting 11% in the medium term. Operational restructuring includes cutting 2,000 jobs and spinning off its chemical park operations into SYNEQT. Evonik’s oilfield portfolio emphasizes low-dose hydrate inhibitors (LDHIs) and environmentally friendly biocides for regulated offshore markets. This strategy strengthens its role in high-margin, compliance-driven production chemical applications.

United States: Regulatory-Driven Reformulation and Digital Oilfield Scale-Up

The United States production chemicals landscape is undergoing a structural transition driven by federal regulation, digital oilfield adoption, and consolidation across upstream supply chains. Following the EPA’s 2025 finalization of CERCLA hazardous substance designations for PFAS, domestic manufacturers have accelerated the elimination of fluorinated surfactants from hydraulic fracturing and production fluid formulations. This regulatory pivot has materially increased the adoption of bio-based wetting agents and biodegradable dispersants, particularly in shale basins where chemical intensity is highest. At the same time, methane mitigation obligations under the Inflation Reduction Act are reshaping dehydration chemistry. Operators in the 2025–2026 window are increasingly specifying low-emission triethylene glycol systems to reduce venting losses and avoid federal methane fees, reinforcing demand for higher-purity, lower-volatility production chemicals.

Digitalization is now a defining competitive lever. In late 2025, Solenis reported a 300% increase in deployments of its IntelliRelease™ intelligent dosing platform in the Permian Basin, highlighting the shift toward microencapsulated scale and corrosion inhibitors with extended residence time. Parallel to this, major service providers such as Halliburton and Baker Hughes expanded Chemicals-as-a-Service models that integrate real-time sensor feedback with automated injection. These systems are reducing overdosing and cutting chemical waste by an estimated 15% on average. Structurally, consolidation is reshaping precursor supply. The October 2025 completion of Berkshire Hathaway’s $9.7 billion acquisition of OxyChem has strengthened domestic chlorine and caustic soda integration, stabilizing feedstock availability for a broad range of oilfield and industrial production chemicals.

India: Policy Simplification, Upstream Expansion, and Green Chemistry Pilots

India’s production chemicals market is being unlocked by regulatory simplification, upstream acreage expansion, and localized specialty chemical capacity additions. The Petroleum and Natural Gas Rules, 2025 introduced the Single Petroleum Lease framework, materially reducing administrative lead times for exploration and production projects. This reform has streamlined chemical procurement across drilling, cementing, and production phases. In parallel, the Hydrocarbon Exploration and Licensing Policy has reached a critical inflection point. By late 2025, 172 exploration blocks had been awarded across OALP rounds, triggering a surge in demand for drilling mud additives, fluid loss control agents, and cementing accelerators across both onshore and offshore basins.

Decarbonization has moved from policy intent to operational pilots. The 2025 rule amendments explicitly allow integrated decarbonization projects within oilfields, leading to early-stage trials of green hydrogen-derived production chemicals and low-carbon surfactant systems. On the supply side, domestic specialty chemical manufacturers are scaling to capture this demand. Aarti Industries and Fineotex Chemical expanded capacity in Gujarat in mid-2025, focusing on non-toxic enzymes, polymeric surfactants, and export-compliant formulations for Middle Eastern oil and gas operators. Beyond upstream hydrocarbons, government approval of a ₹3,184 crore infrastructure package for STP and industrial water modernization is indirectly boosting volumes of flocculants, coagulants, and antiscalants supplied by production chemical vendors with cross-sector portfolios.

China: Energy Efficiency Mandates and CCUS-Linked Chemical Innovation

China’s production chemicals industry is being reshaped by state-led efficiency mandates, carbon capture utilization strategies, and tightening water management rules. Under the MIIT Work Plan 2025–2026, chemical plants are required to achieve a 20% improvement in energy efficiency, with sulfur-based chemical production identified as a priority segment. This directive is accelerating the replacement of legacy reaction pathways with energy-optimized processes and higher-activity catalysts, directly influencing the cost structure and formulation design of production chemicals used in refining and upstream operations.

Carbon management is emerging as a differentiator. In 2025, Sinopec scaled its megaton-level CCUS initiative, deploying advanced amine-based solvents for CO₂ capture that are subsequently repurposed as enhanced oil recovery agents in depleted reservoirs. This closed-loop approach is creating a new class of dual-purpose production chemicals that align emissions reduction with recovery optimization. Regulatory pressure is also intensifying around water. Zero Liquid Discharge mandates introduced in Shandong in early 2025 have forced operators to adopt high-TDS tolerant antiscalants and aggressive membrane cleaners capable of maintaining performance under extreme salinity. In parallel, bio-based engineering is gaining traction. Wanhua Chemical announced commercialization of bio-succinic-acid-based production chemicals in 2025, targeting Green Oilfield certifications required for European-bound projects.

Brazil: Bio-Feedstock Integration and Deepwater Performance Chemistry

Brazil’s production chemicals market is closely tied to bio-feedstock leadership and the technical demands of deepwater offshore production. In 2025, Braskem expanded capacity under its I’m green™ platform, increasing the availability of sugarcane-derived bio-ethylene used in polyethylene pipe liners and chemical containers. This has improved the sustainability profile of chemical handling infrastructure used across oil and gas and industrial sectors.

Offshore complexity continues to drive high-performance chemistry demand. Petrobras awarded multiple multi-year contracts in late 2025 for high-enthalpy scale inhibitors engineered for Pre-salt reservoirs, where temperatures exceed 150°C and pressure conditions are extreme. These applications favor thermally stable phosphonate and polymer-based inhibitor systems with long squeeze life, reinforcing Brazil’s role as a proving ground for advanced production chemical formulations.

Norway and European Union: CCS Readiness and PFAS-Free Compliance

Across Norway and the broader European Union, production chemicals are increasingly aligned with carbon storage infrastructure and regulatory compliance under REACH. In 2025, the Northern Lights subsea CO₂ storage project reached a key operational milestone, deploying specialized mineral-buildup inhibitors to prevent salt precipitation during high-pressure CO₂ injection. These formulations are critical for maintaining injectivity and long-term storage integrity in saline aquifers, positioning CCS-linked chemistry as a strategic growth segment.

Regulatory readiness is equally influential. EU manufacturers have completed registration of polymer-only substances under the latest REACH revisions ahead of 2026 deadlines. This has accelerated the commercial rollout of PFAS-free firefighting foams, surfactants, and production additives that meet stringent environmental and occupational safety requirements. As a result, European production chemicals are increasingly specified not only for performance, but also for lifecycle compliance and export acceptance across global energy markets.

Country-Level Snapshot: Production Chemicals Industry

Production Chemicals Market County Level Snapshot

|

Region

|

Primary Policy or Market Driver

|

Production Chemicals Impact

|

|

United States

|

PFAS regulation, methane fees, digital oilfields

|

Bio-based surfactants, intelligent dosing, feedstock consolidation

|

|

India

|

Lease reform, OALP expansion, decarbonization pilots

|

Growth in drilling additives, green chemistry, specialty surfactants

|

|

China

|

Energy efficiency mandates, CCUS, ZLD

|

Amine solvents, high-TDS antiscalants, bio-based chemicals

|

|

Brazil

|

Bio-ethylene leadership, deepwater offshore

|

Sustainable containers, high-enthalpy scale inhibitors

|

|

Norway and EU

|

CCS deployment, REACH compliance

|

Mineral-buildup inhibitors, PFAS-free production surfactants

|

Production Chemicals Market Report Scope

Production Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.8 Billion

|

|

Market Size (2034)

|

$27.4 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Product Type (Corrosion Inhibitors, Scale Inhibitors, Biocides, Demulsifiers, Asphaltene & Paraffin Inhibitors, Surfactants & Wetting Agents), By Application (Oil & Gas Production, Enhanced Oil Recovery, Water Treatment, Refining & Petrochemicals), By Functional Grade (Standard Industrial Grade, High-Purity Specialty Grade, Environmental Grade)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Solenis, ChampionX Corporation, Ecolab, Baker Hughes Company, Halliburton Company, SLB, Dow Inc., Clariant AG, Evonik Industries AG, Sinopec Group, Innospec Inc., Kemira Oyj, Croda International Plc, Reliance Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Production Chemicals Market Segmentation

By Product Type

- Corrosion Inhibitors

- Scale Inhibitors

- Biocides

- Demulsifiers

- Asphaltene & Paraffin Inhibitors

- Surfactants & Wetting Agents

By Application

- Oil & Gas Production

- Enhanced Oil Recovery

- Water Treatment

- Refining & Petrochemicals

By Functional Grade

- Standard Industrial Grade

- High-Purity Specialty Grade

- Environmental Grade

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Production Chemicals Industry

- BASF SE

- Solenis

- ChampionX Corporation

- Ecolab

- Baker Hughes Company

- Halliburton Company

- SLB

- Dow Inc.

- Clariant AG

- Evonik Industries AG

- Sinopec Group

- Innospec Inc.

- Kemira Oyj

- Croda International Plc

- Reliance Industries Limited

*- List not Exhaustive