Methylene Chloride Market 2025–2034: Regulatory Ban Reshaping Demand, Closed-Loop Polycarbonate Growth, and Chlor-Alkali Realignment Driving $6.6 Billion Outlook at 5.2% CAGR

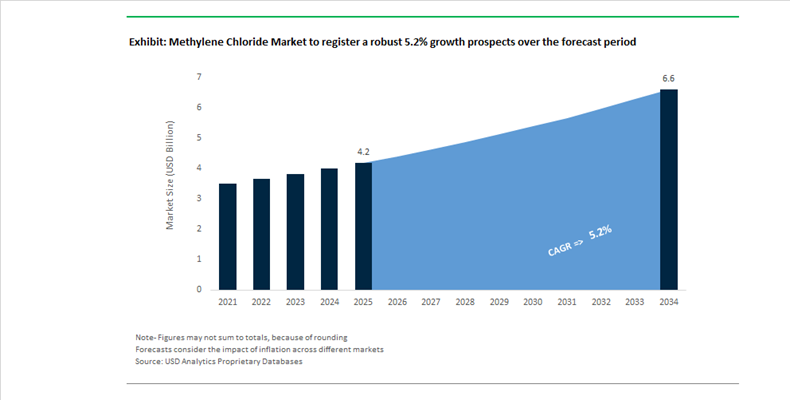

The Methylene Chloride Market is projected to expand from $4.2 billion in 2025 to $6.6 billion by 2034, registering a CAGR of 5.2%. Market dynamics are being fundamentally reshaped by stringent regulatory controls under the U.S. Toxic Substances Control Act (TSCA), supply chain realignment in the chlor-alkali value chain, and selective growth in high-purity industrial applications. Methylene chloride, also known as dichloromethane (DCM), remains critical as a process solvent in pharmaceutical manufacturing, polycarbonate production via interfacial polymerization, and certain closed-loop extraction systems. However, consumer and open-use applications such as paint stripping and adhesive removal have undergone structural contraction following regulatory intervention.

On April 30, 2024, the U.S. Environmental Protection Agency finalized a landmark rule banning most consumer and commercial uses of methylene chloride, mandating a phaseout of all consumer sales within one year and restricting industrial uses. In August 2024, Olin Corporation lifted its systemwide force majeure on chlor-alkali products following hurricane-related disruptions, stabilizing feedstock availability for chlorinated solvent production. In early 2025, new U.S. tariffs on imported chlorinated intermediates disrupted global trade flows, encouraging a shift toward domestic production. A critical regulatory milestone occurred in May 2025, when retailers were formally prohibited from distributing methylene chloride products to any customers, effectively removing the solvent from major hardware and home improvement retail channels. In November and December 2025, the EPA extended compliance deadlines for non-federal laboratories by 18 months, pushing initial monitoring requirements to November 2026 and easing short-term operational pressures for research institutions.

Corporate restructuring and industrial repositioning intensified into 2026. In early January 2026, Occidental Petroleum completed the sale of OxyChem, altering competitive dynamics among global chlorinated solvent producers. In February 2026, Olin recorded a $75 million litigation-related charge amid broader chlor-alkali cycle headwinds. Concurrently, Adani Enterprises advanced its $4 billion petrochemical cluster in Mundra, India, with commissioning targeted for December 2026, strengthening regional chlor-alkali integration. Despite regulatory contraction in open-use markets, 2025 witnessed increased consumption of high-purity methylene chloride in closed-loop polycarbonate manufacturing for automotive and electronics applications. Parallel sustainability shifts were evident in February 2026, when Nouryon introduced 100% bio-based CMC as a strategic alternative in cleaning formulations, reflecting broader substitution trends away from chlorinated solvents toward greener chemistries.

Methylene Chloride Market Trends and Opportunities

Trend: Regulatory Phase-Out and Mandatory Reformulation in Retail and General Commercial Channels

The methylene chloride (DCM) market is undergoing a structurally enforced contraction following the U.S. Environmental Protection Agency’s April 2024 Final Rule under the Toxic Substances Control Act. This rule has moved the industry from risk management into outright prohibition for consumer and general commercial applications, triggering a rapid collapse of retail-facing demand and accelerating solvent substitution across paint removal, adhesives, and surface preparation products.

A critical inflection point was reached on February 3, 2025, when distributors were legally prohibited from supplying methylene chloride-containing products to retail channels. This was followed by a full retail distribution ban effective May 5, 2025, which resulted in the removal of DCM-based paint strippers from large-format hardware chains such as Lowe’s and The Home Depot. Beyond retail, most remaining non-exempt commercial and industrial uses are required to cease by April 28, 2026, creating an accelerated reformulation cycle for downstream formulators.

This regulatory cliff has catalyzed a large-scale pivot toward alternative solvent systems, including benzyl alcohol, dibasic esters, and selected N-methylpyrrolidone blends. However, the transition is not performance-neutral. Traditional DCM-based strippers typically achieve coating removal within 20 minutes, while many substitutes require 6 to 12 hours under comparable conditions. To close this gap, formulators are increasingly deploying “activated” benzyl alcohol systems enhanced with amines and surfactant boosters, positioning green solvent innovation as a central competitive differentiator rather than a compliance afterthought.

Trend: Strategic Scaling of WCPP-Compliant Pharmaceutical and Laboratory Infrastructure

While broad commercial use is being phased out, the EPA has carved out tightly regulated pathways for continued methylene chloride usage in critical applications such as pharmaceutical manufacturing and laboratory synthesis. These exemptions are conditional upon the implementation of a Workplace Chemical Protection Program, which has materially altered the cost structure and operational design of DCM-consuming facilities.

As of May 5, 2025, facilities using methylene chloride must comply with an Existing Chemical Exposure Limit of just 2 ppm as an eight-hour time-weighted average, representing a 92% reduction from the previous OSHA permissible exposure limit. This has necessitated capital-intensive investments in sealed reaction vessels, localized exhaust ventilation, and solvent vapor recovery systems. In parallel, the new compliance framework mandates recurring exposure monitoring. If initial measurements exceed the 1 ppm action level, monitoring must be repeated every six months, escalating to quarterly cycles if exposure surpasses the 2 ppm threshold.

These requirements are driving demand for real-time volatile organic compound sensors and automated monitoring platforms, effectively creating a technology-led compliance submarket around methylene chloride. Pharmaceutical manufacturers are responding by retrofitting active pharmaceutical ingredient synthesis lines with closed-loop solvent recovery units capable of achieving recovery rates above 95%. This approach not only ensures regulatory compliance but also mitigates procurement risk as laboratory-grade DCM becomes more scarce and expensive due to upstream capacity rationalization.

Opportunity: High-Performance Specifications in Aerospace and Defense Applications

Despite widespread regulatory restrictions, methylene chloride remains a mission-critical solvent in aerospace and defense maintenance, where no scalable alternative currently matches its performance profile. The 2024 EPA rule explicitly preserves continued use for national security and aerospace applications, recognizing DCM’s unmatched ability to remove polysulfide sealants and high-performance epoxy coatings without damaging aluminum alloys or advanced composite substrates.

In aircraft Maintenance, Repair, and Overhaul operations, methylene chloride is favored for its ability to minimize substrate corrosion, prevent rust bloom, and preserve tight dimensional tolerances. As a result, MRO facilities servicing major commercial and defense aircraft platforms continue to represent a high-value demand segment, provided operations are conducted within strictly defined regulated areas. From August 1, 2025 onward, these facilities must demonstrate full WCPP compliance, including controlled access zones, enhanced worker training, and documented exposure controls.

This regulatory complexity is reshaping procurement models. Defense contractors and aerospace service providers are increasingly seeking integrated solvent management solutions that bundle compliant DCM supply with monitoring equipment, exposure documentation, and regulatory reporting. This service-oriented model creates an opportunity for specialty chemical distributors to defend margins through compliance expertise rather than volume sales alone.

Opportunity: Industrial-Scale Extraction of High-Value Natural and Pharmaceutical Compounds

Methylene chloride continues to play a strategic role in the extraction of high-value natural products and pharmaceutical intermediates, where its solvent properties remain difficult to replicate. As a polar aprotic solvent with a low boiling point of approximately 40 degrees Celsius, DCM enables efficient extraction of heat-sensitive alkaloids, cannabinoids, and complex organic molecules while minimizing thermal degradation and energy consumption.

Although food-grade applications such as caffeine extraction have largely transitioned to supercritical CO₂, methylene chloride remains indispensable in regulated pharmaceutical and medical extraction processes that demand high selectivity and tight impurity control. In these contexts, ethanol-based systems often introduce co-extraction challenges and higher downstream purification costs, reinforcing DCM’s technical relevance despite regulatory headwinds.

A notable growth avenue is the emergence of centralized, GMP-compliant extraction hubs that operate methylene chloride systems under fully controlled conditions. These facilities absorb the capital and compliance burden of WCPP implementation, allowing smaller nutraceutical and pharmaceutical firms to access DCM-based extraction without direct exposure to regulatory risk. Demand is particularly strong for ultra-pure 99.9% methylene chloride grades with minimized stabilizer content, enabling extractors to meet stringent FDA residue limits and deliver medical-grade end products. In this controlled, high-purity niche, methylene chloride is transitioning from a commodity solvent to a precision chemical input with defensible long-term demand.

Methylene Chloride Market Share and Segmentation Insights

Industrial Grade Methylene Chloride Dominates Market Due to Extensive Use in Industrial Solvent Applications

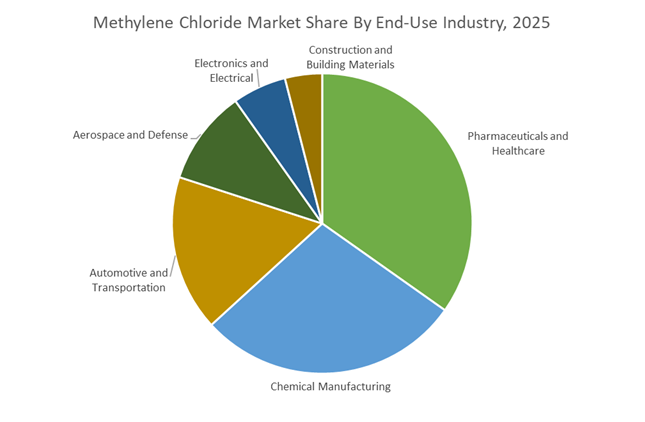

Industrial grade methylene chloride accounted for 68.40% of the Methylene Chloride Market share in 2025, making it the most widely used grade across industrial chemical processing and solvent-based manufacturing operations. Industrial grade dichloromethane is extensively utilized in paint stripping, metal cleaning, foam blowing agents, adhesive formulations, and chemical processing, where its strong solvency power and volatility enable efficient removal of coatings, grease, and polymer residues. The compound is also widely used as a reaction and extraction solvent in industrial chemical synthesis, providing reliable performance in numerous manufacturing environments. Because these applications typically require standard purity levels rather than ultra-high purity grades, industrial grade methylene chloride remains the most cost-effective option for high-volume consumption sectors. In 2025, regulatory frameworks in North America and Europe have placed tighter restrictions on methylene chloride use in consumer paint removers and open industrial applications due to health and environmental concerns. As a result, industrial demand is increasingly concentrated in controlled industrial systems and manufacturing environments where closed-loop solvent recovery and worker exposure controls are implemented, while emerging markets continue to support strong industrial consumption.

Pharmaceutical and Healthcare Sector Leads Global Demand for Methylene Chloride

Pharmaceuticals and healthcare accounted for 34.80% of the Methylene Chloride Market share in 2025, making drug manufacturing and pharmaceutical chemical processing the largest end-use sector for this solvent. Methylene chloride plays a critical role in pharmaceutical synthesis, active pharmaceutical ingredient (API) production, extraction processes, and crystallization steps, where its solvency properties enable efficient dissolution of complex organic compounds and facilitate selective purification. The solvent is widely used in reaction media and intermediate purification stages during the production of numerous small-molecule drugs and specialty pharmaceutical ingredients. Pharmaceutical manufacturers rely on methylene chloride because it offers excellent solubility for many organic intermediates, rapid evaporation characteristics, and compatibility with multiple reaction pathways, which makes it difficult to substitute in certain synthesis processes. In 2025, pharmaceutical producers are also increasingly focused on strict residual solvent control and regulatory compliance, following International Council for Harmonisation (ICH) guidelines that specify permissible solvent residue levels in finished drug products. As a result, manufacturers have implemented advanced purification techniques, solvent recovery systems, and analytical testing protocols to ensure residual methylene chloride levels remain within regulatory safety limits during pharmaceutical production.

Methylene Chloride Market Competitive Landscape

The methylene chloride (DCM) market in 2026 is driven by regulatory realignment under TSCA, with demand shifting toward pharmaceutical-grade solvents, HFC-32 refrigerants, and electronics applications. Competitive advantage lies in regulatory-compliant production, ISCC PLUS-certified green chloromethanes, and high-purity supply chains across Asia and Europe.

Olin prioritizes margin-driven DCM production with focus on pharmaceutical and high-value applications

Olin Corporation is executing a value-first strategy in the methylene chloride market, prioritizing ECU margin optimization over volume expansion. Through its Beyond250 initiative, the company achieved $44 million in cost savings in 2025 and continues targeting structural efficiencies in 2026. The closure of its Brazil epoxy facility allows consolidation of DCM production at competitive hubs like Freeport, Texas. Post-maintenance normalization at Freeport ensures stable supply for high-purity applications in pharmaceuticals and chemical processing. Olin’s disciplined commercial model focuses on high-value, WCPP-compliant sectors amid TSCA restrictions. Strong liquidity of approximately $1.0 billion supports operational resilience and strategic flexibility.

Nouryon expands green chloromethanes capacity with ISCC PLUS certification and renewable integration

Nouryon is strengthening its position in the methylene chloride market through sustainable chloromethane production and capacity expansion. Its Frankfurt facility expansion increased chloromethanes output by up to 50%, targeting pharmaceutical-grade solvent demand in India and other emerging markets. ISCC PLUS certification and renewable energy integration at its European sites enhance its low-carbon chemical portfolio. Recognition through the Henkel Sustainability Award reinforces its leadership in eco-friendly solvent innovation. Nouryon’s DCM is increasingly used in next-generation HFO refrigerants with low global warming potential. Its focus on circular chemistry and regulatory compliance positions it strongly in the evolving global DCM landscape.

Shin-Etsu leverages vertical integration to deliver ultra-high-purity DCM for electronics and silicones

Shin-Etsu Chemical maintains a dominant position through its fully integrated chlor-alkali and derivatives value chain, ensuring consistent high-purity methylene chloride supply. Its specialized DCM grades are engineered for polycarbonate production and complex agrochemical synthesis. The company utilizes DCM and methyl chloride as critical intermediates in its global silicone and methylcellulose businesses. Under its 2026 strategy, Shin-Etsu is aligning DCM production with low-GWP fluorocarbon development to support climate mitigation goals. Its strong presence in Japan’s electronics and precision manufacturing sectors reinforces demand stability. Technical purity and supply chain control remain its key competitive differentiators.

Kem One advances circular chloromethane production with ISCC-certified logistics and API focus

Kem One is emerging as a European leader in sustainable methylene chloride through its circular salt chemistry model and ISCC PLUS-certified production. Its Lavéra plant serves as a strategic logistics hub, enabling multimodal distribution of DCM across Europe and global markets. The company’s Kemaia® product range emphasizes reduced environmental footprint and compliance with pharmaceutical-grade standards. DCM’s low boiling point and high solvency make it essential for API extraction processes with minimal residue. With €1.5 billion in turnover, Kem One maintains stable production capacity for chloromethanes supporting aviation and polyurethane sectors. Its sustainability-led approach strengthens its competitive positioning.

Tokuyama shifts toward high-value DCM applications in electronics and life sciences

Tokuyama Corporation is transforming its portfolio toward advanced materials, leveraging methylene chloride as a key solvent in electronics and life science applications. The transfer of chemical sales operations to Tokuyama Soda Trading enhances organizational efficiency and customer responsiveness. Expansion of its Electronic & Advanced Materials segment through global joint ventures supports semiconductor-grade chemical demand. The company is focusing on rapid commercialization of solvent-based innovations aligned with its ion exchange and salt chemistry expertise. Strong cash flow from legacy businesses funds investments in diagnostics and specialty materials. Tokuyama’s strategic pivot positions it for growth in high-purity, technology-driven DCM applications.

United States: Regulatory Reset and Accelerated Substitution Pathways

The United States has entered a decisive regulatory phase for methylene chloride following the April 2024 final rule issued under TSCA Section 6 by the U.S. Environmental Protection Agency. Retail distribution of methylene chloride was prohibited from February 3, 2025, while most industrial applications, including paint stripping, face a hard stop after April 28, 2026. Manufacturing remains permissible only for narrowly defined critical uses such as refrigerant manufacturing and select laboratory chemical processing. This regulatory reset has forced rapid portfolio realignment across coatings, aerospace maintenance, and industrial cleaning value chains.

For remaining Conditions of Use, compliance requirements have intensified. The mandated Workplace Chemical Protection Program now includes an Existing Chemical Exposure Limit of 2 ppm as an 8-hour TWA, sharply below the legacy OSHA PEL. In November 2025, the EPA granted non-federal laboratories an 18-month compliance extension, shifting initial exposure monitoring to November 9, 2026, and full exposure control plans to May 10, 2027. Market dynamics reflect this transition. Feedstock-driven volatility lifted the U.S. methylene dichloride price index by 5.33% quarter-over-quarter in late 2025 as chlorine and methanol costs firmed along the Gulf Coast. Downstream, aerospace operators have accelerated adoption of DCM-free technologies, including superoxalloy abrasive blasting and benzyl alcohol-based strippers, with suppliers such as 10X Engineered Materials reporting strong uptake for high-pressure, non-chlorinated alternatives.

China: Capacity Leadership Anchored by Refrigerants and Green Upgrades

China continues to anchor global methylene chloride supply through scale and integration, even as end-use demand patterns evolve. Large producers such as Jiujiang Jiuhong and Luxi Chemical have sustained high operating rates. Temporary supply tightening linked to scheduled maintenance lifted domestic MIBK and DCM prices by 0.7% in July 2025. More structurally, refrigerant manufacturing has become a stabilizing demand pillar, with HFC-32 production providing price support as traditional paint and coating consumption softened.

Policy direction is reinforcing consolidation and cleaner production. Under 2025 directives from the Ministry of Industry and Information Technology, chloromethane units are required to cut hazardous byproduct emissions by 15% by 2026. This favors centralized chemical parks with advanced vapor recovery and solvent handling systems. China also retains a strong position in pharmacopeia-grade methylene chloride. In March 2025, suppliers reported a 4.5% increase in API-sector orders, driven by antibiotic and steroid crystallization needs that require consistent solvent purity and moisture control.

India: Trade Defense, Solvent Recovery, and Infrastructure Demand

India’s methylene chloride landscape is shaped by trade protection and environmental compliance in pharmaceutical hubs. The extension of anti-dumping duties in late 2024 by the Ministry of Finance has insulated domestic producers such as Gujarat Fluorochemicals and Chemplast Sanmar from low-cost imports originating in China and the European Union. This policy continuity has provided operational visibility through 2025 and into 2026.

Environmental mandates are equally influential. The Central Pollution Control Board has enforced Zero Liquid Discharge requirements across pharmaceutical clusters in Telangana and Andhra Pradesh for 2025–2026. As a result, manufacturers have invested in solvent recovery systems capable of reclaiming up to 98% of methylene chloride used in extraction, reshaping demand toward closed-loop, high-purity grades. Beyond pharmaceuticals, construction chemicals remain a durable outlet. Large-scale infrastructure programs aligned with India’s 2032 Agenda continue to consume significant volumes of chlorinated solvents, sustaining baseline industrial demand despite tightening global scrutiny.

European Union: Progressive Restrictions and Specialty Refining Advantage

The European Union is advancing a phased exit from methylene chloride in open industrial systems while preserving tightly controlled, high-purity uses. Commission Regulation (EU) 2025/1090, issued in June 2025 under REACH Annex XVII, reinforces the Zero Pollution Action Plan trajectory by aligning solvent controls and signaling a phase-out of DCM in non-enclosed applications by 2027. Although the regulation primarily targeted DMAC, its implications for methylene chloride are material, accelerating substitution timelines across surface treatment and maintenance operations.

Within this framework, Germany has remained a stabilizing production hub. Producers such as Vinnolit maintained steady output through Q3 2025 despite elevated energy costs. The European methylene dichloride price index increased 4.34 percent in early 2025, reflecting inventory discipline and stable methanol availability. Importantly, regulatory refinement has favored specialized European refiners. Updates to the European Pharmacopoeia in 2025 imposed stricter moisture limits for residual solvents in peptide synthesis, advantaging suppliers capable of delivering ultra-dry, high-purity methylene chloride for advanced pharmaceutical applications.

Comparative Snapshot: Country-Level Positioning in the Methylene Chloride Market

Methylene Chloride Market County Level Snapshot

|

Country / Region

|

Primary Driver

|

Regulatory Catalyst

|

Industrial Response

|

Strategic Outcome

|

|

United States

|

TSCA Section 6 enforcement

|

EPA ban and ECEL tightening

|

Substitution, WCPP compliance, specialty uses

|

Rapid demand contraction with niche continuity

|

|

China

|

Refrigerant and API demand

|

MIIT green development mandates

|

Park-based upgrades, purity control

|

Sustained scale with cleaner production

|

|

India

|

Pharma extraction and infrastructure

|

Anti-dumping duties, ZLD rules

|

Solvent recovery investment

|

Protected domestic supply chain

|

|

European Union

|

Zero Pollution Action Plan

|

REACH Annex XVII updates

|

Specialty refining, controlled use

|

Shift toward high-purity niche demand

|

Methylene Chloride Market Report Scope

Methylene Chloride Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.2 Billion

|

|

Market Size (2034)

|

$6.6 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade), By Application (Paint Stripping and Coating Removal, Pharmaceutical Processing, Chemical Processing, Metal Cleaning and Degreasing, Adhesives and Sealants), By End-Use Industry (Pharmaceuticals and Healthcare, Automotive and Transportation, Aerospace and Defense, Construction and Building Materials, Food and Beverage, Electronics and Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Olin Corporation, Occidental Petroleum, Westlake Chemical, Akzo Nobel, KEM ONE, Vinnolit, Shin-Etsu Chemical, Gujarat Fluorochemicals, Chemplast Sanmar, Tokuyama Corporation, Luxi Chemical Group, Jiujiang Jiuhong Chemical, Shandong Aojin Chemical Technology, AGC, INEOS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methylene Chloride Market Segmentation

By Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic Grade

By Application

- Paint Stripping and Coating Removal

- Pharmaceutical Processing

- Chemical Processing

- Metal Cleaning and Degreasing

- Adhesives and Sealants

By End-Use Industry

- Pharmaceuticals and Healthcare

- Automotive and Transportation

- Aerospace and Defense

- Construction and Building Materials

- Food and Beverage

- Electronics and Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methylene Chloride Market

- Olin Corporation

- Occidental Petroleum

- Westlake Chemical

- Akzo Nobel

- KEM ONE

- Vinnolit

- Shin-Etsu Chemical

- Gujarat Fluorochemicals

- Chemplast Sanmar

- Tokuyama Corporation

- Luxi Chemical Group

- Jiujiang Jiuhong Chemical

- Shandong Aojin Chemical Technology

- AGC

- INEOS

*- List not Exhaustive