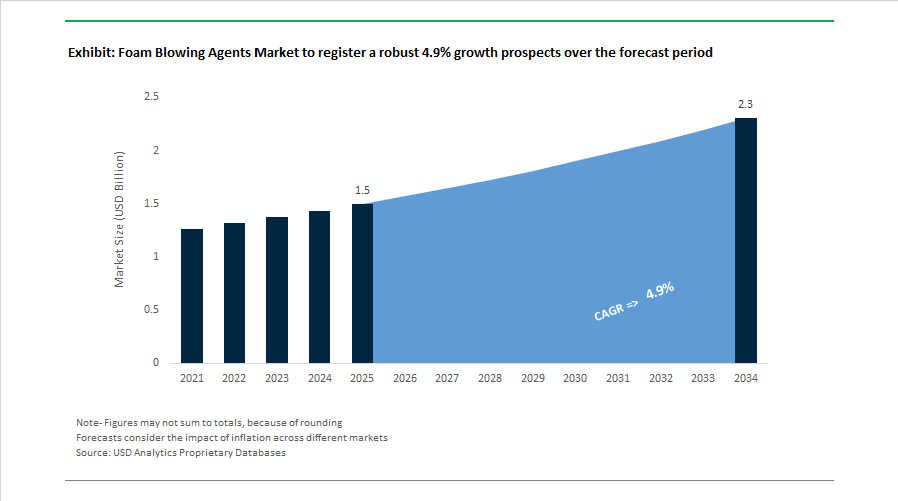

Foam Blowing Agents Market Size 2025–2034: $1.5 Billion to $2.3 Billion at 4.9% CAGR Driven by HFO Transition and Low-GWP Regulations

The Foam Blowing Agents Market is projected to grow from $1.5 billion in 2025 to $2.3 billion by 2034, registering a CAGR of 4.9%. Market growth is primarily driven by the accelerated transition from high-GWP hydrofluorocarbons (HFCs) toward hydrofluoroolefins (HFOs), hydrocarbons, and bio-integrated polyurethane systems in construction insulation, refrigeration, appliance manufacturing, and cold-chain logistics. Regulatory mandates across North America and Europe, coupled with decarbonization targets in building materials and electric vehicle battery insulation, are reshaping the blowing agent chemistry landscape. HFO-1233zd, HFO-1234ze, HFC-152a bridge agents, and hydrocarbon blends remain central to rigid polyurethane foam, spray polyurethane foam (SPF), and extruded polystyrene (XPS) applications.

In December 2025, BASF introduced WALLTITE® RSB, a next-generation closed-cell spray polyurethane foam incorporating recycled and bio-based resin content combined with low-GWP blowing agents to reduce embodied carbon in building envelopes. The same month, BASF launched Lupragen® N 208, an advanced amine catalyst engineered for compatibility with next-generation HFO blowing agents, addressing foam stability challenges commonly associated with low-VOC polyurethane systems. In October 2025, SNF Group agreed to acquire Syensqo’s Oil & Gas and mining portfolio, consolidating specialty chemical supply chains that intersect with polymer processing and foam stabilization chemistry. During late 2025, the newly independent Solstice Advanced Materials implemented its “Solstice Accelerator” operating model, focusing on customer-driven formulation development for EV battery insulation and temperature-controlled logistics.

In May 2025, Arkema completed a $60 million expansion of its Forane® 1233zd production facility in Kentucky, increasing North American output to 15 kilotons annually to meet rising demand from construction and appliance insulation manufacturers. In May 2025, Chemours entered a strategic agreement with Navin Fluorine to manufacture Opteon™ specialty fluids, reinforcing the supply chain for intermediates used in Opteon™ 1100 foam blowing agents. Early 2025 also saw Huntsman launch its Revised Construction Products Regulation compliance initiative in Europe, aligning rigid insulation resin systems with low-GWP blowing agents to ensure regulatory stability. Honeywell progressed with the spin-off of its Advanced Materials division in 2024 and 2025, separating the Solstice® low-GWP blowing agent portfolio into a publicly traded entity focused on next-generation fluorine chemistry.

Regulatory acceleration began in 2024. State-level bans in Massachusetts and New York prohibiting the sale of XPS foam containing high-GWP HFCs such as HFC-134a took effect in January 2024, catalyzing rapid regional adoption of HFO and hydrocarbon alternatives. In August 2024, Honeywell announced collaboration with Mighty Buildings to integrate Solstice Liquid Blowing Agent into 3D-printed housing panels, demonstrating application expansion into construction technology. In late 2023 and through 2024, Chemours expanded HFC-152a production by 20%, stabilizing supply of this transitional blowing agent widely used in aerosol and extrusion foam markets during the phasedown of higher-GWP HFCs.

Trends and Opportunities in the Foam Blowing Agents Market

Global Mandatory Transition to Low-GWP HFOs and Advanced Liquid Blends

Regulatory enforcement has reached a point of no return for high-GWP hydrofluorocarbons in foam applications. The EU F-Gas Regulation (2024/573) and the U.S. EPA SNAP rules have effectively eliminated HFC-134a and HFC-245fa from new foam manufacturing, accelerating a structural shift toward hydrofluoroolefins (HFOs) with near-zero global warming potential.

From January 1, 2025, HFC-based foam production is prohibited in the United States, forcing insulation and appliance manufacturers to fully transition to HFO-1234ze and HFO-1336mzz. These agents deliver GWPs below 1 while maintaining comparable thermal performance, making them the default compliance solution for polyurethane and polyisocyanurate foams. As a result, capacity availability has become a strategic differentiator. In May 2025, Arkema completed a USD 60 million expansion at its Calvert City, Kentucky site, lifting North American Forane® 1233zd capacity to 15 kilotons per year. This expansion is explicitly aligned with demand from building insulation, appliances, and cold-chain logistics.

Strategic portfolio realignment is reinforcing this trend. In October 2024, Honeywell announced the spin-off of its Advanced Materials business into Solstice Advanced Materials Inc., expected to list in late 2025. This move underscores how Solstice® HFO technology has transitioned from a regulatory hedge to a core growth engine, with blowing agents now positioned as long-term infrastructure chemicals rather than transitional substitutes.

Material Innovation for CO₂ and Hydrocarbon Optimization

While HFOs dominate high-performance insulation, hydrocarbons and CO₂-based systems continue to expand in cost-sensitive and high-volume applications. Cyclopentane and n-pentane have become the leading blowing agents for domestic refrigeration due to zero ozone depletion potential and low cost. By 2025, purpose-built “pentane-ready” production lines with advanced ventilation and gas detection systems reduced fire risk by more than 90% compared with retrofitted legacy facilities, enabling hydrocarbons to scale safely across Asia and Europe.

CO₂, generated in situ via water-blown chemistry, is also regaining momentum. Historically constrained by higher thermal conductivity, water-blown foams have benefited from new polyol architectures and cell-structure optimization. Technical demonstrations at K 2025 showed that modern CO₂-blown systems can achieve a 10 to 15% improvement in R-value, positioning them as viable solutions for non-critical insulation, furniture, and packaging foams where cost and sustainability outweigh maximum thermal performance.

Digitalization is accelerating this optimization cycle. In February 2025, Honeywell integrated generative AI capabilities into its Forge Production Intelligence platform, enabling real-time dosing and stabilization of blowing agent addition. Early adopters report a 5 to 8% reduction in chemical waste and improved consistency in high-speed foam production, highlighting how process intelligence is becoming integral to blowing agent efficiency.

Next-Generation Safety Applications in EVs and Aerospace

Electrification and lightweighting trends are unlocking premium niches for blowing agents that function as active safety and performance enablers. In electric vehicles, foam systems are increasingly specified as thermal and fire-propagation barriers rather than passive insulation. In 2025, Arkema launched its Foranext® Gaseous Thermal Barrier technology, engineered to delay and suppress thermal runaway propagation in lithium-ion battery packs. These systems are designed to act at the point of failure, providing OEMs with additional minutes of containment, a critical safety metric for high-energy-density batteries.

Aerospace composites represent another high-margin opportunity. With composite-heavy aircraft deliveries projected to rise by 25% through 2026, demand is growing for blowing agents compatible with polyimide and phenolic foams that maintain structural integrity above 200°C. Traditional agents fail under these conditions, creating a defensible niche for advanced HFO blends and specialty agents qualified to aerospace certification standards.

Synergies are also emerging between blowing agents and thermal management fluids. Chemours is increasingly positioning its Opteon™ portfolio as part of an integrated thermal management solution, aligning foam insulation chemistries with dielectric immersion cooling fluids. This convergence allows EV manufacturers to simplify chemical qualification while improving system-level thermal safety.

Circular Economy Models for Blowing Agent Recovery and Recycling

End-of-life management of foam insulation is evolving into a regulated revenue stream as governments target embodied carbon and legacy emissions. New EU building regulations enacted in late 2025 require at least 20% of demolition waste from commercial buildings to undergo chemical recovery, catalyzing demand for technologies that extract and reclaim blowing agents before disposal.

At K 2025 in Düsseldorf, Asahi Kasei unveiled a breakthrough recycling process for carbon fiber-reinforced plastics and foam cores using electrolyzed sulfuric acid. The technology enables recovery rates exceeding 95% for both structural fibers and trapped blowing agents, transforming demolition waste into a secondary feedstock rather than a liability.

Parallel investments are underway in chemical recycling infrastructure. Polyol and insulation producers are expanding glycolysis and pyrolysis capacity to process production scrap and post-consumer foams. By recovering blowing agents during polyurethane depolymerization, manufacturers can reduce the lifecycle carbon footprint of new foam products by approximately 30%, while securing supply in an increasingly regulated market.

Foam Blowing Agents Market Share and Segmentation Insights

Hydrofluoroolefins Lead the Transition Toward Low-GWP Foam Blowing Technologies

Hydrofluoroolefins (HFOs) accounted for 38.60% of the Foam Blowing Agents Market share in 2025, establishing them as the dominant blowing agent category used in modern polyurethane foam manufacturing. HFOs have rapidly replaced older hydrofluorocarbon (HFC) blowing agents due to their superior environmental profile, characterized by zero ozone depletion potential (ODP) and extremely low global warming potential (GWP below 10). These characteristics align with global environmental regulations and climate commitments, particularly those associated with the Kigali Amendment to the Montreal Protocol, which targets the phasedown of high-GWP HFC refrigerants and blowing agents. HFO blowing agents are widely used in rigid polyurethane foam insulation, spray foam insulation systems, and structural insulated panels, where they enable excellent thermal insulation performance and dimensional stability. In 2025, a key market development is the declining cost of HFO production driven by patent expirations and expanded manufacturing capacity worldwide. As proprietary technologies become more widely accessible, increased competition among chemical manufacturers has reduced product prices, accelerating adoption across both developed and emerging markets. Additionally, manufacturers are introducing advanced HFO blend formulations that improve foam cell structure, insulation performance, and process stability, further strengthening HFOs’ leadership in the global foam blowing agents market.

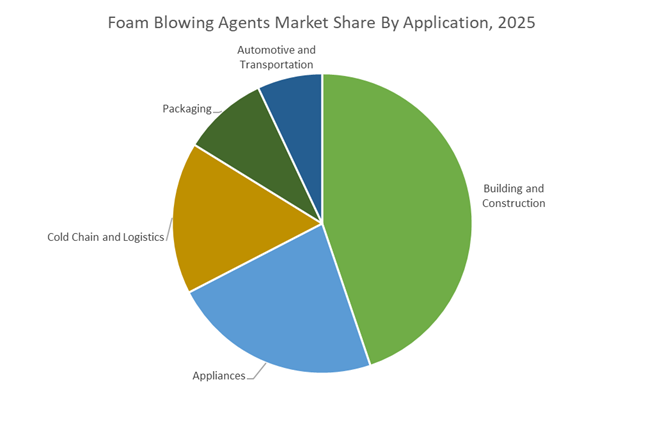

Building and Construction Sector Drives Largest Demand for High-Performance Foam Insulation

Building and Construction represented 44.80% of the Foam Blowing Agents Market share in 2025, making it the most significant application segment for blowing agent technologies. Foam insulation materials—particularly spray polyurethane foam, rigid polyurethane insulation boards, and structural insulated panels (SIPs)—play a crucial role in improving thermal efficiency and energy performance in residential and commercial buildings. Blowing agents are essential in the foam manufacturing process, creating the cellular structure that provides the low thermal conductivity required for high-performance building insulation systems. Global demand for insulation materials has expanded significantly as governments and construction industries pursue energy-efficient building standards and carbon reduction targets. In 2025, building energy regulations are becoming increasingly stringent, with standards such as passive house certification, net-zero energy building frameworks, and enhanced thermal performance codes driving higher insulation requirements. As insulation thickness and performance expectations increase, foam manufacturers are adopting next-generation blowing agents capable of delivering lower thermal conductivity and improved foam cell stability.

Competitive Landscape in Foam Blowing Agents Market

Honeywell Sets the Standard in Ultra-Low GWP HFO Blowing Agents

Honeywell International remains the technology leader in high-performance foam blowing agents through its Solstice® platform of liquid and gas blowing agents based on hydrofluoroolefin chemistry. These agents deliver a global warming potential below 1, representing a 99.9% reduction compared to legacy HFC systems. In early 2026, Honeywell integrated Generative AI into its Forge Production Intelligence platform to optimize chemical yields and foam cell morphology, enabling customers to achieve consistent thermal performance across production lines. The launch of Stablebase 2.0 Max R in 2026 introduced a spray foam system delivering an R-value of 7.5, strengthening its position in energy-efficient residential construction. With deep vertical integration and a substantial patent portfolio, Honeywell has transitioned major insulation OEMs to HFO technology, effectively establishing regulatory benchmarks in North America and Europe. This combination of compliance leadership and digital optimization secures its dominance in premium low-GWP blowing agents.

Arkema Expands High-Purity HFO Capacity and Recyclable Foam Systems

Arkema operates as a specialty materials leader with its Forane® FBA 1233zd series designed for rigid polyurethane and spray foam insulation. The product is non-flammable and engineered for superior thermal insulation performance in commercial and residential construction. In late 2025, Arkema patented new recyclable foam system technologies addressing end-of-life circularity, a growing priority in 2026 sustainability mandates. The company ramped its Calvert City facility to 15,000 metric tons annually to meet rising demand for low-GWP blowing agents across the United States and Europe. Arkema’s local-for-local strategy includes a 5,000-ton partnership in China to serve Asia-Pacific markets with reduced logistical exposure. By combining high-purity HFO manufacturing with circular design innovation, Arkema strengthens its competitive stance in next-generation polyurethane foam systems.

BASF Integrates Biomass-Balanced Blowing Agents with Downstream Foam Systems

BASF leverages its global polyurethane production footprint to drive adoption of integrated blowing agent solutions aligned with its Bio-based Circularity strategy. By 2026, the company aims to offer net-zero variants across its foam portfolio using renewable feedstocks and biomass-balanced chemical inputs. Following its 2025 Performance Materials reorganization, BASF integrated blowing agent research more closely with appliance and automotive insulation systems, enhancing system-level efficiency. The company maintains leadership in automotive battery enclosures and high-efficiency refrigeration insulation, providing fully integrated resin and blowing agent packages. Through its Verbund production model, BASF manufactures carbon dioxide and water-based chemical blowing agents with reduced lifecycle emissions. This system-level integration and renewable feedstock focus differentiate BASF in sustainable foam chemistry.

Chemours Scales HFO Production for Cold Chain and Industrial Insulation

The Chemours Company is expanding its Opteon™ 1100 and 1150 blowing agents to address high-growth insulation markets requiring thermal stability and long-term performance. Between 2025 and 2026, Chemours tripled HFO production capacity at its Texas facility, establishing one of the world’s largest hubs for low-GWP foam blowing agents. The company’s Pathway to Thrive strategy prioritizes high-performance fluids and specialized thermal solutions serving AI-driven data centers and advanced industrial insulation systems. Chemours maintains strong positioning in cold chain logistics, where insulation integrity is critical for supermarket refrigeration and temperature-controlled transport. Its vertical integration in fluorine chemistry and growing immersion cooling portfolio reinforce cross-market synergies. This scale expansion and thermal performance specialization secure Chemours’ position in premium insulation and refrigeration applications.

Daikin Advances Mission-Critical Low-GWP Foam Technologies in Asia-Pacific

Daikin Industries is a major innovation leader in the Asia-Pacific foam blowing agents market, integrating HFO and R-32 based systems into HVAC and refrigeration hardware. At the 2026 AHR Expo, Daikin unveiled next-generation low-GWP foam solutions engineered for hyperscale data centers and mission-critical cooling environments. Recognized in the Clarivate Top 100 Global Innovators for the eleventh time, the company continues to share patents for low-GWP technologies to accelerate global decarbonization. Under its FUSION 25 plan, Daikin invested $163 million in an advanced Minnesota R&D facility focused on oil-free and ultra-low GWP foam-insulated chillers. Its dominance in Japan and Southeast Asia is reinforced by vertically integrated HVAC manufacturing, where blowing agents are embedded directly into system design. This hardware-chemical integration strengthens its regional leadership in advanced insulation technologies.

ExxonMobil Dominates Cost-Effective Hydrocarbon Blowing Agents

ExxonMobil Corporation leads the hydrocarbon blowing agent segment through high-purity pentanes including iso-pentane, n-pentane, and cyclopentane. These agents provide zero ozone depletion potential and very low global warming potential at significantly lower cost than HFO alternatives. In 2025, ExxonMobil expanded specialty hydrocarbon refinery capacity to serve growing polystyrene and polyethylene foam markets in Asia, which are expanding at double-digit rates. The company remains a primary supplier for protective packaging and extruded polystyrene boardstock applications where cost efficiency and fire safety compliance are critical. Its scale, feedstock security, and global refining network ensure stable pricing in the commodity segment of the blowing agent market. This structural cost advantage sustains ExxonMobil’s leadership in emerging markets and volume-driven foam applications.

United States: Low-GWP HFO Leadership Anchored by Onshoring and Regulatory Acceleration

The United States foam blowing agents market is being structurally reshaped by portfolio realignment, capacity onshoring, and an intensifying regulatory step-down. In October 2025, Honeywell completed the spin-off of its Advanced Materials business into Solstice Advanced Materials (NASDAQ: SOLS). The newly independent entity now exclusively manages the Solstice HFO-1233zd and HFO-1234ze portfolios, sharpening strategic focus on low-GWP blowing agents for spray foam insulation and household appliances. This specialization is accelerating commercialization cycles for next-generation HFOs across U.S. construction, cold-chain logistics, and appliance manufacturing.

Supply-side resilience has strengthened through targeted capital investment. In August 2025, Arkema commissioned a USD 60 million Forane 1233zd unit in Calvert City, Kentucky, lifting North American capacity to 15 kilotons per year and reinforcing domestic availability of sustainable blowing agents. Regulatory pressure is compounding these shifts. Under the AIM Act, the U.S. Environmental Protection Agency will enforce an additional 30% reduction in HFC consumption allowances from January 1, 2026. This is accelerating substitution away from HFC-245fa and blended systems toward fourth-generation HFOs. Downstream validation is also advancing, with Daikin Applied announcing a USD 163 million R&D lab in Plymouth, Minnesota, dedicated to high-density insulation performance for data centers and HVAC infrastructure.

China: Mandatory Phase-Outs Forcing Rapid Technology Substitution

China’s foam blowing agents market is entering a decisive compliance phase, driven by hard regulatory cutoffs and strategic alliances to secure low-GWP supply. The Ministry of Ecology and Environment has clarified that from January 1, 2026, polyurethane products using HCFC-141b are prohibited, with a narrow temporary exemption for sprayed PU foam that expires on July 1, 2026. This mandate is compressing transition timelines across insulation, construction, and industrial foam producers. A parallel ban effective July 1, 2026 will eliminate HCFC use in extruded polystyrene foam production, displacing more than 2,000 tons of residual HCFC-22 and HCFC-142b consumption and forcing adoption of CO₂, alcohol-based systems, and HFC-152a alternatives.

Strategic capacity additions are aligning with this regulatory cliff. The Chemours Company has partnered with Zhejiang Juhua Group to triple Opteon 1100 (HFO-1336mzzZ) capacity, with startup in late 2025 and global supply scaling in early 2026. The appliance sector is also a catalyst. From January 1, 2026, China will prohibit household refrigerators and freezers using HFC refrigerants, driving appliance manufacturers toward cyclopentane and HFO-blown rigid foam systems to meet energy labeling requirements. Collectively, these measures are converting China from a managed transition market into one of enforced substitution.

European Union: Fiscal Signals and Circularity Redefining Blowing Agent Choices

The European Union foam blowing agents market is being reshaped by a combination of fiscal disincentives, emissions control, and energy transition objectives. Under F-Gas Regulation 2024/573, effective January 1, 2026, a quota payment of EUR 3 per tonne of CO₂ equivalent will apply to HFC allocations. This materially raises the cost base of legacy blowing agents and structurally favors pentane systems and liquid HFO solutions such as Solstice formulations in insulation and appliance foams.

Environmental controls are extending into end-of-life management. Regulatory updates in 2025–2026 expand requirements to prevent blowing agent leakage during demolition and disposal of building foams. This has accelerated development of recoverable blowing agent technologies in Germany and France, aligning foam systems with circular economy procurement criteria. At the same time, REPowerEU deployment targets have prompted the EU to grant a limited additional HFC quota of 10.3% for 2025–2026, reserved for high-efficiency heat pump insulation. This calibrated flexibility is stabilizing supply chains during the energy transition while preserving the long-term direction toward low-GWP alternatives.

Saudi Arabia: Vision 2030 Construction Driving High-Performance HFO Adoption

Saudi Arabia’s foam blowing agents market is expanding on the back of unprecedented construction activity linked to Vision 2030. Mega-projects such as NEOM and Red Sea Global are driving an estimated USD 185 billion demand for structural insulation and sandwich panels. The Saudi Building Code SBC 601 on energy conservation mandates high-performance thermal barriers, accelerating adoption of HFO-blown polyisocyanurate panels that deliver superior insulation values under extreme climatic conditions.

Localization initiatives are reinforcing this demand shift. SABIC has expanded its Nusaned local content program to provide technical support for small and mid-sized manufacturers transitioning from high-GWP agents to hydrocarbon technologies, particularly pentane, in appliance and insulation board production. This combination of regulatory enforcement and industrial support is positioning Saudi Arabia as a fast-scaling market for advanced, compliant foam blowing agents rather than transitional chemistries.

Summary of Country-Level Strategic Drivers in the Foam Blowing Agents Market

Foam Blowing Agents Market County Level Snapshot

|

Country

|

Core Policy or Investment Driver

|

Implications for Foam Blowing Agents

|

|

United States

|

AIM Act step-down and HFO onshoring

|

Rapid migration from HFCs to HFO-1233zd and HFO-1234ze

|

|

China

|

HCFC bans and appliance regulations

|

Forced substitution toward CO₂, pentane, and ultra-low GWP HFOs

|

|

European Union

|

F-Gas fiscal penalties and circular mandates

|

Structural shift to pentane and recoverable HFO systems

|

|

Saudi Arabia

|

Vision 2030 construction and energy codes

|

Rising demand for HFO-blown PIR and hydrocarbon technologies

|

Foam Blowing Agents Market Report Scope

Foam Blowing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.3 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product Type (Hydrofluoroolefins, Hydrocarbons, Hydrofluorocarbons, Natural Blowing Agents), By Foam Type (Polyurethane Foam, Polystyrene Foam, Phenolic Foam, Polyolefin Foam), By Application (Building and Construction, Appliances, Cold Chain and Logistics, Automotive and Transportation, Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International Inc., The Chemours Company, Arkema S.A., Daikin Industries, Ltd., Covestro AG, Sinopec, Zhejiang Juhua Co., Ltd., Huntsman Corporation, Linde plc, Solvay S.A., SABIC, BASF SE, Evonik Industries AG, Tosoh Corporation, Harp International Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Foam Blowing Agents Market Segmentation

By Product Type

- Hydrofluoroolefins

- Hydrocarbons

- Hydrofluorocarbons

- Natural Blowing Agents

By Foam Type

- Polyurethane Foam

- Polystyrene Foam

- Phenolic Foam

- Polyolefin Foam

By Application

- Building and Construction

- Appliances

- Cold Chain and Logistics

- Automotive and Transportation

- Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Foam Blowing Agents Industry

- Honeywell International Inc.

- The Chemours Company

- Arkema S.A.

- Daikin Industries, Ltd.

- Covestro AG

- Sinopec

- Zhejiang Juhua Co., Ltd.

- Huntsman Corporation

- Linde plc

- Solvay S.A.

- SABIC

- BASF SE

- Evonik Industries AG

- Tosoh Corporation

- Harp International Ltd.

*- List not Exhaustive