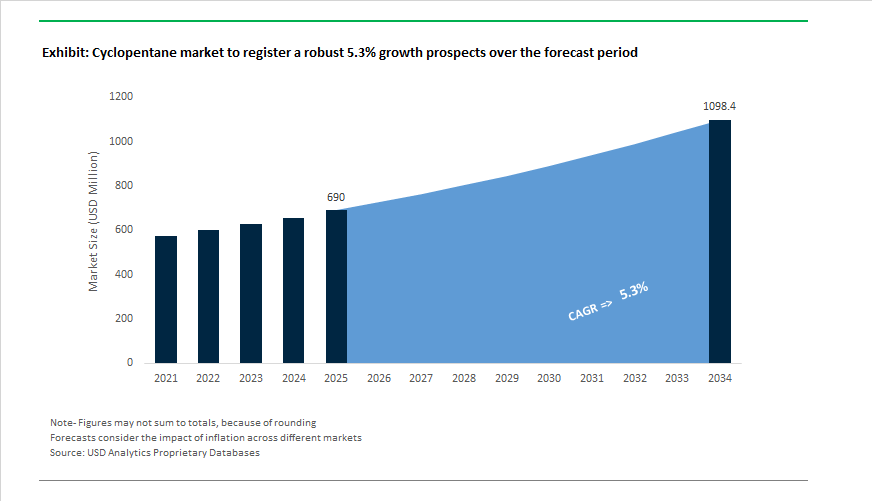

Cyclopentane Market to Reach $1,098.3 Million by 2034 at 5.3% CAGR Driven by Insulation Demand, Feedstock Integration, and Low-Carbon Pentane Innovation

The Cyclopentane Market is projected to expand from $690 Million in 2025 to $1,098.3 Million by 2034, registering a CAGR of 5.3%. Cyclopentane remains a critical hydrocarbon blowing agent in polyurethane (PU) rigid foam applications, particularly in refrigeration, cold chain logistics, and high-performance building insulation. Growth momentum is closely tied to global phase-outs of high-GWP hydrofluorocarbons, rising construction energy-efficiency mandates, and integrated C5 feedstock investments across Asia and Europe. Demand is increasingly shaped by regulatory compliance under EPA SNAP programs, European carbon accounting frameworks, and emerging green building standards in developing economies.

Feedstock security and upstream integration became a focal point in June 2024, when Haldia Petrochemicals signed a 10-year naphtha supply agreement with QatarEnergy to ensure stable C5 hydrocarbon availability for its cracker operations. This agreement underpins India’s expanding cold chain infrastructure and domestic high-purity cyclopentane production. In November 2024, Haldia Petrochemicals further strengthened its phenol chain integration through a license amendment with Lummus Technology, expanding phenol capacity to 345 KTPA as part of a ₹5,000 crore greenfield investment in West Bengal. These developments are strategically aligned with securing benzene and C5 streams required for downstream cyclopentane refinement. Supply-side volatility emerged in August 2024, when maintenance turnarounds across major Chinese and South Korean petrochemical complexes curtailed Asian output, triggering a regional price surge during peak air-conditioning and refrigeration demand. Simultaneously, Whirlpool completed the transition of its North American refrigerator lines to cyclopentane-blown foam in 2024, reinforcing compliance with the U.S. EPA Significant New Alternatives Policy and improving appliance insulation R-values. Electrolux implemented a full cyclopentane integration across Brazilian production facilities in the same year, aligning with Latin American environmental targets to eliminate high-GWP gases.

Sustainability-led product innovation accelerated in 2024, when HCS Group introduced ISCC PLUS certified low-carbon pentanes, including cyclopentane and iso-pentane, produced via mass-balance renewable feedstocks. These certified grades enable appliance and insulation panel manufacturers to reduce Scope 3 emissions in European and North American markets. In 2025, Honeywell showcased blended insulation solutions combining Solstice® Liquid Blowing Agent with cyclopentane, allowing foam producers to achieve A+++ energy efficiency ratings while mitigating flammability management challenges inherent to pure hydrocarbon systems. Structural capacity expansion reshaped the competitive landscape in January 2026, when HCS Group completed integration of its new hydrogenation plant in Speyer, Germany, increasing cyclopentane production capacity by approximately 70% and positioning itself as the world’s largest producer under the Haltermann Carless brand. In parallel, Zeon Corporation announced a portfolio restructuring in December 2025, prioritizing cyclopentane-related intermediates such as cyclopentyl methyl ether and cyclopentanone to serve pharmaceutical and semiconductor applications. Government-driven adoption further intensified in 2024–2025, when India allocated ₹1,500 crore toward green technologies, incentivizing hydrocarbon blowing agents. By early 2026, India’s Bureau of Energy Efficiency reported that cyclopentane-based insulation delivered average energy savings of 20% in new construction projects, accelerating uptake among commercial developers and reinforcing cyclopentane’s position in energy-efficient building envelopes and refrigeration systems.

Trends and Opportunities in the Global Cyclopentane Market

Regulatory Phase-Down of HFCs Accelerating Blowing Agent Substitution

- Global phase-downs of hydrofluorocarbons are structurally reshaping the rigid polyurethane foam industry, positioning cyclopentane as the dominant blowing agent for refrigerators, freezers, and insulated building panels. In the United States, the implementation of SNAP Rule 26 by the United States Environmental Protection Agency through late 2024 and 2025 streamlined approvals for hydrocarbon alternatives. This regulatory clarity accelerated retrofitting of domestic appliance manufacturing lines, where cyclopentane systems can reduce facility level greenhouse gas emissions by up to 99% compared with legacy HFC 245fa technologies.

- A similar shift is underway in Europe. Under the European Union F Gas Regulation, HFC quotas are set to decline to 9 million tonnes of CO2 equivalent by 2030. By September 2025, appliance manufacturing hubs in Turkey and Poland had converted more than 85% of insulation lines to cyclopentane based foaming systems to maintain export eligibility into the Eurozone. These conversions reflect not only compliance requirements but also long term cost advantages, as hydrocarbon blowing agents reduce exposure to quota driven price volatility associated with fluorinated gases.

Hybrid HFO Cyclopentane Blowing Systems Improving Insulation Performance

- While cyclopentane has become the default low GWP blowing agent, formulators are increasingly adopting hybrid systems that combine hydrocarbons with fourth generation hydrofluoroolefins to push insulation performance beyond traditional limits. Industrial data published in December 2025 show that blending cyclopentane with HFO 1233zd(E) can reduce the thermal conductivity of polyurethane foam to around 10.2 milliwatts per meter Kelvin. This improvement allows appliance manufacturers to use thinner insulation walls while increasing usable internal volume, a critical differentiator for products designed to meet Energy Star 7.0 efficiency standards.

- Safety and process control are evolving in parallel. Given the inherent flammability of cyclopentane, foam system suppliers are deploying phosphorus based flame retardants, specialized silicone surfactants, and latent catalyst technologies. By 2025, these advanced catalyst systems were enabling tighter control over exothermic reactions during foaming, supporting safer continuous production of laminated sandwich panels for commercial and residential construction. This combination of performance gains and risk mitigation is reinforcing cyclopentane’s long term role in both appliance and building insulation markets.

High Purity Cyclopentane for Semiconductor and Pharmaceutical Manufacturing

- Beyond insulation, electronic grade cyclopentane is emerging as a high margin opportunity driven by advanced manufacturing requirements. In June 2025, Maruzen Petrochemical introduced 99.9% plus purity cyclopentane grades tailored for electronics cooling and semiconductor processing. The solvent’s low polarity and non corrosive behavior make it suitable for niche roles in extreme ultraviolet lithography, where it is used in photoresist development and residue removal without damaging sub 5 nanometer transistor architectures.

- The pharmaceutical sector is also increasing its adoption of cyclopentane as a safer solvent alternative. Compared with n hexane, cyclopentane offers a lower toxicity profile, supporting compliance with ICH Q3C R8 guidelines on residual solvents. As a result, pharmaceutical manufacturers are incorporating cyclopentane into extraction and crystallization steps for active pharmaceutical ingredients, reducing toxicological risk while maintaining process efficiency. This regulatory alignment is steadily expanding cyclopentane demand beyond industrial applications into regulated life sciences markets.

Feedstock Potential for Bio Aromatic and Specialty Chemical Pathways

- Cyclopentane’s strained ring structure is unlocking new opportunities in specialty chemicals and sustainable synthesis routes. In 2025, the permanent shutdown of several European adipic acid and cyclopentanone production units, including closures announced by BASF, created supply gaps for cyclopentanone. This molecule is a critical precursor for synthetic jasmine fragrances and selected agrochemicals, opening a pathway for cyclopentane producers to integrate downstream and capture higher value margins.

- Sustainability driven innovation is further strengthening this opportunity. Catalytic oxidation research published in 2025 demonstrated the feasibility of converting cyclopentane directly into adipic acid using novel zeolite based catalysts. This benzene free route bypasses the traditional cyclohexane to KA oil process, which is both energy intensive and emission heavy. For the Nylon 6,6 value chain, especially in automotive plastics, this alternative pathway could reduce carbon footprints by an estimated 30 to 40%. As pressure mounts to decarbonize engineering polymers, cyclopentane is increasingly viewed as a versatile feedstock for next generation green chemical platforms rather than a single use blowing agent.

Cyclopentane Market Share and Segmentation Insights

Function-Based Segmentation: Blowing Agents Dominate as Low-GWP Insulation Accelerates Adoption

Blowing agents and refrigerants account for 72% of cyclopentane consumption in 2025, positioning cyclopentane as the preferred physical blowing agent for rigid polyurethane foam insulation. Its zero ozone depletion potential (ODP), low global warming potential (GWP), and excellent thermal insulation performance (low k-factor) have made it a cornerstone material in sustainable refrigeration and building insulation systems. Solvents and reagents represent a smaller but important niche, utilizing cyclopentane in pharmaceutical synthesis, polymer processing, and laboratory applications where controlled volatility and chemical inertness are required. Fuel and fuel additives remain the smallest segment, with cyclopentane used selectively in specialty fuel blends, octane enhancement, and combustion research as a model hydrocarbon due to its well-characterized ignition behavior. Overall, regulatory-driven transition away from HFCs continues to reinforce cyclopentane’s leadership in environmentally compliant foam blowing technologies.

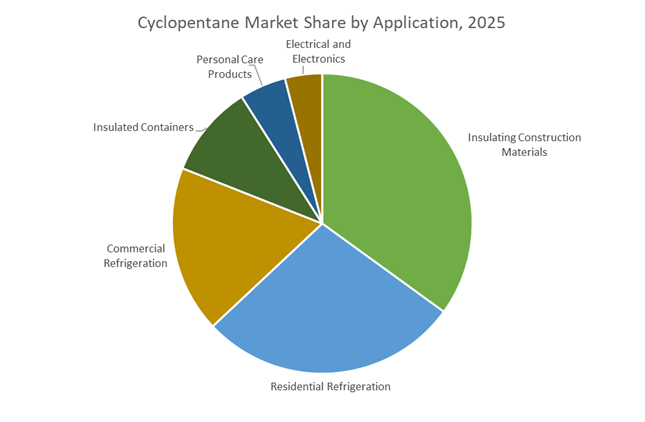

Application Landscape: Construction Insulation Leads as Refrigeration and Cold Chain Logistics Expand

Insulating construction materials command 35% of cyclopentane demand, driven by global energy-efficiency building codes promoting high-performance spray foams, rigid panels, and insulated concrete forms. Residential refrigeration represents a major secondary application, with cyclopentane widely adopted for cabinet insulation in refrigerators and freezers following the Kigali Amendment-driven phase-out of high-GWP HFCs. Commercial refrigeration is growing steadily across retail and foodservice equipment, including beverage coolers and walk-in freezers seeking sustainable insulation solutions. Insulated containers for cold-chain logistics form an expanding segment, supported by pharmaceutical distribution and e-commerce food delivery. Personal care products utilize cyclopentane as a volatile carrier in aerosols and as a silicone alternative in hair and skin formulations, while electrical and electronics applications include precision cleaning and specialty coating carriers, although VOC regulations continue to shape this niche.

Competitive Landscape of the Cyclopentane Market

The Cyclopentane Market is increasingly defined by low-GWP blowing agent demand, sustainable mass-balance production, and rising adoption in rigid polyurethane foam insulation for appliances, cold chain logistics, and green buildings. Market leaders are differentiating through ISCC PLUS certification, vertical feedstock integration, and expansion into high-purity grades for semiconductor and electronics applications.

HCS Group scales ISCC PLUS-certified low-carbon cyclopentane production in Europe

HCS Group, through Haltermann Carless, serves as the European benchmark for high-purity and sustainable cyclopentane production. During 2025–2026, the company expanded its ISCC PLUS-certified low-carbon cyclopentane portfolio using a mass-balance approach that integrates renewable feedstocks into hydrocarbon solvent production. Following a multi-million-euro hydrogenation plant upgrade at its Speyer, Germany facility, cyclopentane capacity increased by 70%, reinforcing supply reliability for polyurethane foam manufacturers. With distribution across 90+ countries, HCS is aggressively targeting the North American commercial refrigeration retrofit market in 2026. Its “Low-Carbon Solutions” strategy focuses on reducing Scope 3 emissions for appliance and construction customers by 2030.

Chevron Phillips Chemical ensures high-volume cyclopentane supply through vertical integration

Chevron Phillips Chemical Company remains a dominant North American cyclopentane supplier, supported by deep petrochemical feedstock integration. The company benefits from internal production of key raw materials, shielding cyclopentane pricing from merchant market volatility. As part of Chevron’s broader 2026 capital expenditure program of $18 to $19 billion, nearly half is directed toward new world-scale facilities strengthening specialty chemical value chains. CPChem’s Orfom® and specialty hydrocarbon blends are widely used in rigid polyurethane foams that enhance thermal insulation in residential refrigerators. The company plays a central role in supporting U.S. OEMs transitioning toward next-generation energy efficiency standards and low-GWP insulation technologies.

Zeon advances ultra-high-purity cyclopentane for semiconductor and advanced polymer markets

Zeon Corporation leverages deep expertise in C5 hydrocarbon chemistry to deliver 99%+ purity cyclopentane grades tailored for electronics and semiconductor cleaning applications. In February 2026, Zeon commenced construction of its Tokuyama East Plant, a next-generation facility dedicated to cyclo-olefin polymers that utilize cyclopentane as a synthesis intermediate. The expansion is projected to boost Zeon’s overall high-performance material capacity by 30% by fiscal 2028. Under its STAGE30 medium-term plan, Zeon prioritizes healthcare, life sciences, and green transformation initiatives. Its focus on high-value, high-purity applications differentiates it from commodity blowing agent producers in the global cyclopentane market.

INEOS leverages global petrochemical scale to serve cold chain and green building markets

INEOS Group provides unmatched production scale with operations spanning 173 sites across 32 countries, positioning it as a global cyclopentane powerhouse. The company supplies cyclopentane as a drop-in solution integrated with its resin and plastics portfolio for appliance and construction manufacturers. INEOS is a leading supplier for global cold chain infrastructure, including insulated panels for refrigerated warehouses and transport containers. In early 2026, it expanded its Hygienics and Automotive frameworks to explore lightweight insulation materials for EV applications. Strategic joint ventures in Asia-Pacific further strengthen its presence in India and China’s green building and sustainable construction initiatives.

SK Geo Centric drives circular cyclopentane production across Asia-Pacific

SK Geo Centric, a pioneer of the “Urban Oil Field” model, holds a dominant position in Asia-Pacific, a region accounting for over 43% of global cyclopentane market value. The company is advancing waste-to-chemicals technology, converting recycled plastics into circular naphtha for downstream recycled cyclopentane production. In 2025, it introduced a high-efficiency blowing agent blend combining cyclopentane with HFOs, delivering a 5% insulation performance improvement in premium refrigerators. During 2026, SK expanded its Global Solution Centers to provide localized technical support to Chinese and Southeast Asian appliance OEMs, reinforcing its leadership in sustainable insulation chemistry.

China: Montreal Protocol Enforcement as a Structural Demand Catalyst

China is entering a decisive transition phase for the cyclopentane industry, driven by binding environmental regulation and large-scale appliance manufacturing. In December 2025, the Ministry of Ecology and Environment issued a landmark prohibition on the use of HCFC-141b as a blowing agent in extruded polystyrene and polyurethane products, effective July 1, 2026. This single regulatory action is expected to displace more than 2,000 tons of residual HCFC demand, redirecting it almost entirely toward cyclopentane and other low-global-warming-potential alternatives. Unlike earlier voluntary transitions, this mandate enforces a hard compliance deadline, accelerating conversion across appliance, insulation, and construction material manufacturers.

Supply-side readiness is being addressed through targeted green material investments. In April 2024, BSM (Tongling) Chemical committed ¥121 million to a new Anhui-based facility designed to produce over 12,100 tons of cyclopentane series materials annually by 2025–2026. This capacity expansion aligns with China’s 2025–2030 National Plan for the Implementation of the Montreal Protocol, which also bans household refrigerators and freezers using HFC refrigerants from January 2026.

India: Appliance Growth, SME Conversion, and Cold-Chain Pull

India’s cyclopentane market is being shaped by simultaneous upstream petrochemical expansion and downstream appliance and logistics growth. Haldia Petrochemicals’ $10 billion oil-to-chemicals project in Tamil Nadu represents a long-cycle strategic bet on domestic intermediates, with cyclopentane positioned as a core product as commissioning progresses toward 2028. This investment directly supports India’s rising demand for energy-efficient refrigerators and freezers, which is expanding at an estimated high single-digit rate as electrification and income levels rise.

On the regulatory front, India has already exceeded its Montreal Protocol obligations. A 2025 government report confirmed a 44% HCFC phase-out, well ahead of the 35% target, largely due to incentives encouraging SMEs to adopt cyclopentane-based high-pressure foaming systems. This early compliance has reduced transition risk and normalized cyclopentane usage even among smaller manufacturers. Additionally, the 2025–2026 budgetary push for cold-chain logistics under the PM Gatishakti master plan is stimulating demand for cyclopentane-blown rigid foam in refrigerated transport, embedding the molecule deeper into India’s food security and pharmaceutical distribution infrastructure.

Germany: Low-Carbon Certification and Circular Chemistry Integration

Germany’s cyclopentane industry is evolving through capacity scaling paired with sustainability-led differentiation. Following the completion of its Speyer hydrogenation plant, HCS Group reported a 70% increase in cyclopentane production capacity. In 2025, this expansion was complemented by the launch of ISCC PLUS-certified low-carbon pentane grades, directly addressing demand from European insulation producers facing tighter Scope 3 emissions scrutiny.

Beyond volume growth, German manufacturers are embedding cyclopentane into the circular economy framework. During 2025, the industry began adopting mass-balanced cyclopentane produced using bio-naphtha feedstocks, ensuring compliance with evolving EU REACH sustainability expectations. This approach allows insulation and appliance OEMs to decarbonize upstream inputs without altering foam performance, positioning Germany as a supplier of premium, regulation-aligned cyclopentane rather than a cost-driven exporter.

United States: Regulatory Pivot and Cold Storage Expansion

The United States is approaching a critical inflection point in cyclopentane adoption. Effective January 1, 2025, the Environmental Protection Agency implemented a nationwide ban on the manufacture of HFC-based closed-cell spray polyurethane foam systems. Although existing inventories may be sold until 2028, 2026 is widely regarded by contractors as the pivot year for full conversion to cyclopentane and hydrofluoroolefin systems. This staged timeline is compressing decision cycles for foam formulators and insulation installers.

At the same time, structural demand is being reinforced by logistics infrastructure. According to the Global Cold Chain Alliance, cold storage operators, heavily concentrated in the U.S., added over 600 million cubic feet of capacity during 2024–2025. This expansion is significantly increasing the use of cyclopentane-blown insulated panels in industrial warehousing, linking cyclopentane demand to long-term growth in food distribution, pharmaceuticals, and e-commerce fulfillment rather than short-term regulatory substitution alone.

South Korea: Export Appliances and High-Purity Diversification

South Korea’s cyclopentane market is characterized by formulation innovation and export-oriented appliance manufacturing. At Chinaplas 2024–2025, SK Geo Centric showcased advanced cyclopentane formulations under its Lifestyle Solutions portfolio, emphasizing superior thermal resistance for premium, export-grade appliances. This positioning reflects South Korea’s focus on high-efficiency products destined for markets with strict energy labeling requirements.

Looking beyond insulation, joint R&D programs announced for 2026 indicate a strategic move into high-purity cyclopentane above 99% as a specialty solvent. These initiatives target advanced polymer manufacturing for semiconductor and aerospace applications, signaling early diversification of cyclopentane use cases beyond traditional blowing agent demand.

Summary Snapshot: Cyclopentane Industry by Country

Cyclopentane Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Strategic Emphasis

|

Industry Direction

|

|

China

|

Mandatory HCFC and HFC phase-out

|

Appliance insulation, green capacity build-out

|

Regulation-locked structural demand

|

|

India

|

O2C expansion and cold-chain logistics

|

SME adoption, domestic supply localization

|

Broad-based consumption growth

|

|

Germany

|

Low-carbon certification and REACH alignment

|

ISCC PLUS and mass-balanced grades

|

Premium, sustainability-led supply

|

|

United States

|

HFC ban and cold storage expansion

|

Contractor transition and logistics insulation

|

Policy-driven pivot with infrastructure pull

|

|

South Korea

|

Export appliances and R&D diversification

|

High-performance formulations and purity upgrades

|

Value-added, export-focused evolution

|

Cyclopentane Market Report Scope

Cyclopentane market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$690 Million

|

|

Market Size (2034)

|

$1098.3 Million

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Function (Blowing Agents and Refrigerants, Solvents and Reagents, Fuel and Fuel Additives), By Application (Residential Refrigeration, Commercial Refrigeration, Insulated Containers, Insulating Construction Materials, Electrical and Electronics, Personal Care Products), By Purity Level (High Purity, Standard Purity, Low Purity)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

HCS Group GmbH, Chevron Phillips Chemical Company LLC, Haldia Petrochemicals Limited, INEOS Group Limited, Maruzen Petrochemical Co., Ltd., LG Chem Ltd., SK Geo Centric Co., Ltd., DYMATIC Chemicals, Inc., South Hampton Resources, Inc., Yeochun NCC Co., Ltd., Liaoning Yufeng Chemical Co., Ltd., Zibo Luhua Hongjin New Material Co., Ltd., Jilin Beihua Fine Chemical Co., Ltd., Tokyo Chemical Industry Co., Ltd., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cyclopentane Market Segmentation

By Function

- Blowing Agents and Refrigerants

- Solvents and Reagents

- Fuel and Fuel Additives

By Application

- Residential Refrigeration

- Commercial Refrigeration

- Insulated Containers

- Insulating Construction Materials

- Electrical and Electronics

- Personal Care Products

By Purity Level

- High Purity

- Standard Purity

- Low Purity

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Cyclopentane Industry

- HCS Group GmbH

- Chevron Phillips Chemical Company LLC

- Haldia Petrochemicals Limited

- INEOS Group Limited

- Maruzen Petrochemical Co., Ltd.

- LG Chem Ltd.

- SK Geo Centric Co., Ltd.

- DYMATIC Chemicals, Inc.

- South Hampton Resources, Inc.

- Yeochun NCC Co., Ltd.

- Liaoning Yufeng Chemical Co., Ltd.

- Zibo Luhua Hongjin New Material Co., Ltd.

- Jilin Beihua Fine Chemical Co., Ltd.

- Tokyo Chemical Industry Co., Ltd.

- Huntsman Corporation

*- List not Exhaustive

Table of Contents: Cyclopentane Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Cyclopentane Market Landscape & Outlook (2026–2034)

2.1. Introduction to Cyclopentane Market

2.2. Market Valuation and Growth Projections (2026–2034)

2.3. HFC Phase-Down, EPA SNAP, and EU F-Gas Regulatory Alignment

2.4. C5 Feedstock Integration, Naphtha Security, and Upstream Investments

2.5. Low-Carbon Pentane Innovation, ISCC PLUS Certification, and Energy-Efficiency Mandates

3. Innovations Reshaping the Cyclopentane Market

3.1. Trend: Global Substitution of HFC-245fa with Hydrocarbon Blowing Systems

3.2. Trend: Hybrid HFO-Cyclopentane Blowing Technologies for Enhanced Thermal Performance

3.3. Opportunity: High-Purity Cyclopentane for Semiconductor and Pharmaceutical Applications

3.4. Opportunity: Cyclopentane as a Feedstock for Adipic Acid and Specialty Chemical Pathways

4. Competitive Landscape and Strategic Initiatives

4.1. Capacity Expansion, Hydrogenation Integration, and Feedstock Security Agreements

4.2. R&D in Low-Carbon, Mass-Balance, and High-Purity Grades

4.3. Sustainability and ESG Strategies Including Renewable Feedstocks and Carbon Accounting

4.4. Regional Expansion, Appliance OEM Partnerships, and Cold-Chain Infrastructure Focus

5. Market Share and Segmentation Insights: Cyclopentane Market

5.1. By Function

5.1.1. Blowing Agents and Refrigerants

5.1.2. Solvents and Reagents

5.1.3. Fuel and Fuel Additives

5.2. By Application

5.2.1. Residential Refrigeration

5.2.2. Commercial Refrigeration

5.2.3. Insulated Containers

5.2.4. Insulating Construction Materials

5.2.5. Electrical and Electronics

5.2.6. Personal Care Products

5.3. By Purity Level

5.3.1. High Purity

5.3.2. Standard Purity

5.3.3. Low Purity

5.4. By Region

5.4.1. North America

5.4.2. Europe

5.4.3. Asia Pacific

5.4.4. South and Central America

5.4.5. Middle East and Africa

6. Country Analysis and Outlook of Cyclopentane Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Cyclopentane Market Size Outlook by Region (2026–2034)

7.1. North America Cyclopentane Market Size Outlook to 2034

7.1.1. By Function

7.1.2. By Application

7.1.3. By Purity Level

7.1.4. By End-Use Integration

7.2. Europe Cyclopentane Market Size Outlook to 2034

7.2.1. By Function

7.2.2. By Application

7.2.3. By Purity Level

7.2.4. By End-Use Integration

7.3. Asia Pacific Cyclopentane Market Size Outlook to 2034

7.3.1. By Function

7.3.2. By Application

7.3.3. By Purity Level

7.3.4. By End-Use Integration

7.4. South America Cyclopentane Market Size Outlook to 2034

7.4.1. By Function

7.4.2. By Application

7.4.3. By Purity Level

7.4.4. By End-Use Integration

7.5. Middle East and Africa Cyclopentane Market Size Outlook to 2034

7.5.1. By Function

7.5.2. By Application

7.5.3. By Purity Level

7.5.4. By End-Use Integration

8. Company Profiles: Leading Players in the Cyclopentane Market

8.1. HCS Group GmbH

8.2. Chevron Phillips Chemical Company LLC

8.3. Haldia Petrochemicals Limited

8.4. INEOS Group Limited

8.5. Maruzen Petrochemical Co., Ltd.

8.6. LG Chem Ltd.

8.7. SK Geo Centric Co., Ltd.

8.8. DYMATIC Chemicals, Inc.

8.9. South Hampton Resources, Inc.

8.10. Yeochun NCC Co., Ltd.

8.11. Liaoning Yufeng Chemical Co., Ltd.

8.12. Zibo Luhua Hongjin New Material Co., Ltd.

8.13. Jilin Beihua Fine Chemical Co., Ltd.

8.14. Tokyo Chemical Industry Co., Ltd.

8.15. Huntsman Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures