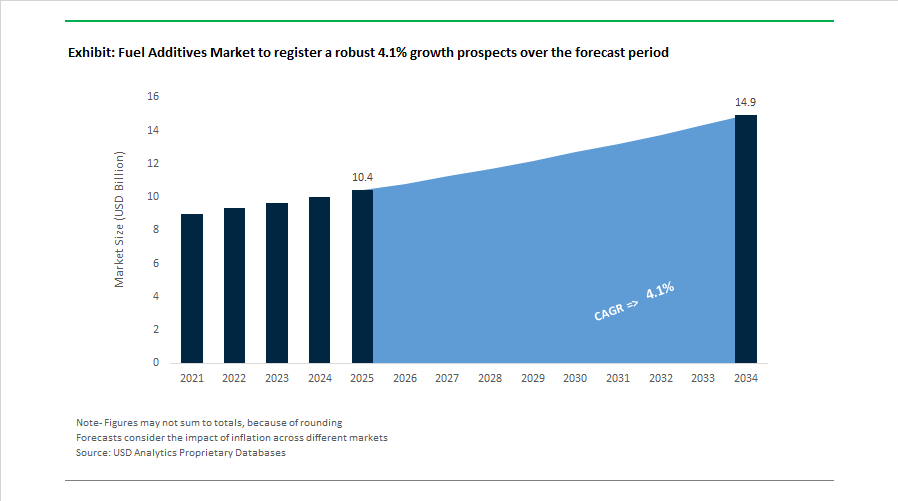

Fuel Additives Market Size 2025–2034: $10.4 Billion to $14.9 Billion at 4.1% CAGR Driven by Hydrogen Engines, GDI Standards and Renewable Fuel Stability

The Fuel Additives Market is projected to grow from $10.4 billion in 2025 to $14.9 billion by 2034, registering a CAGR of 4.1%. Market expansion is being shaped by the evolution of gasoline direct injection engines, hydrogen internal combustion platforms, renewable fuel blends, and stricter deposit control standards such as TOP TIER+™. Deposit control additives, cetane improvers, cold flow improvers, antioxidants, corrosion inhibitors, lubricity enhancers, and combustion modifiers remain core product categories. Increasing penetration of hybrid vehicles, biofuel blends, and high-pressure fuel systems is driving demand for high-performance additive chemistries that enhance combustion efficiency while maintaining regulatory compliance.

In February 2026, Lubrizol inaugurated its Shanghai Innovation Center, reinforcing a local-for-local R&D model to tailor fuel additive packages to Asia-Pacific fuel quality variations and hybrid vehicle growth. In early 2026, Infineum signed a strategic framework agreement with Rianlon Corporation to stabilize antioxidant and friction-modifier intermediate supply across the region, following prior capacity expansion in China during 2024. Commercial deliveries of BASF’s Keropur® AP 225-20 gasoline performance additive are scheduled to begin in the first half of 2026, engineered to meet the revised U.S. TOP TIER+™ specification targeting deposit control in GDI engines ahead of the 2027 mandate.

Innovation momentum accelerated throughout 2025. In September 2025, Afton Chemical launched HiTEC® 12582, the first commercially available dedicated additive for hydrogen internal combustion engines, addressing oxidation stability, water management, and stochastic pre-ignition risks in heavy-duty applications. In August 2025, Afton introduced the HiTEC® 65522 series approved for TOP TIER+™, designed to mitigate injector deposits and particulate formation in GDI-powered vehicles, which account for over 70% of new vehicles in North America. In September 2025, Evonik initiated its Next Markets Program, redirecting additive R&D toward combustion efficiency and storage stability for renewable diesel and bio-blended fuels. In March 2025, Innospec launched the LaZuli™ product line certified for deepwater subsea production, including specialty additives for hydrate inhibition and flow assurance in high-pressure offshore environments. During 2025, LANXESS highlighted Additin® RC 2515 at the Rosefield Conference, reducing product carbon footprint by 34% with over 80% sustainable raw material content under its Scopeblue label. Chevron Oronite introduced OLOA® 55620 targeting motorcycle and small-engine segments in Asia, addressing high-temperature protection and deposit control needs.

Strategic investments and certification milestones strengthened operational capabilities during 2024 and early 2025. In July 2024, Clariant initiated expansion of its Ningbo facility, scheduled for completion in late 2026, to increase output of stabilizers and antioxidants critical for modern fuel blend shelf life. In Q4 2024, Innospec’s Oklahoma City plant achieved ISO 9001 certification and subsequently earned a Gold EcoVadis rating, reflecting rising demand for quality assurance and environmental transparency in specialty fuel chemical manufacturing.

Trends and Opportunities Shaping the Global Fuel Additives Market

Mandated Detergency to Meet Ultra-Low Emission and Engine Durability Standards

As emission norms tighten globally, fuel detergency has transitioned from a premium differentiation tool into a regulatory necessity. Modern Gasoline Direct Injection engines operate at injector pressures exceeding 350 bar, making them highly sensitive to deposit formation that directly impacts fuel economy, particulate emissions, and power output. Following the full rollout of China 6B standards, demand for high-molecular-weight Polyisobutylene Amine detergents has accelerated sharply. Refinery and patent activity in late 2025 confirms a shift toward fourth-generation PIBA chemistries engineered to maintain injector cleanliness under extreme thermal and pressure conditions, reducing particulate matter formation at the source.

India’s Bharat Stage VI framework has reinforced this trend. The mandated reduction of sulfur to 10 ppm has removed the natural lubricity once provided by sulfur compounds. Technical guidance issued by Indian refiners in 2025 shows that this has increased the treat rates of deposit control additives and lubricity improvers to protect high-precision fuel pumps, injectors, and Selective Catalytic Reduction systems from accelerated wear. In parallel, the emergence of enhanced fuel quality benchmarks such as TOP TIER+ is pushing additive suppliers to design packages that exceed minimum compliance and align with OEM lifetime durability targets. The launch of next-generation detergent systems approved for TOP TIER+ gasoline in 2025 underscores how additive performance is increasingly benchmarked against ultra-clean standards rather than regulatory baselines.

Additive Chemistry Tailored for Sustainable Aviation Fuel and Renewable Diesel

The commercial scaling of Sustainable Aviation Fuel and Hydrotreated Vegetable Oil has exposed structural weaknesses in these fuels that must be addressed chemically. As the ReFuelEU Aviation mandate enforced a 2% SAF blending requirement from January 2025, airlines and fuel producers prioritized thermal stability. SAF produced via HEFA pathways lacks some of the stabilizing aromatics present in fossil jet fuel, increasing the risk of deposit formation in high-temperature turbine zones. This has intensified demand for advanced antioxidants and metal deactivators that ensure compliance with ASTM D7566 and protect fuel systems under long-haul operating conditions.

In the road transport sector, HVO adoption is accelerating due to its high cetane number and low lifecycle carbon intensity. However, its near-zero sulfur and aromatic content significantly reduce natural lubricity. Studies published in late 2025 confirm that heavy-duty fleets operating on HVO100 without ester-based lubricity improvers face elevated risks of fuel pump and injector failure. As a result, lubricity enhancement has become a non-negotiable additive function in renewable diesel formulations, driving sustained volume growth for ester-based and multifunctional additive packages.

Specialized Additives for Hydrogen Combustion and Hybrid Powertrains

The diversification of propulsion technologies is opening a high-margin opportunity space for next-generation fuel and lubricant additives. Hydrogen combustion engines present fundamentally different chemical challenges than hydrocarbon fuels. Hydrogen produces no carbon soot, but it generates high water content and elevated nitrogen oxide formation. In 2025, the commercial launch of the first dedicated additive system for hydrogen heavy-duty engines validated the emergence of a new sub-segment. These formulations focus on water emulsification control, ashless detergency, and NOx mitigation, requiring a complete redesign of conventional additive architectures.

Hybrid and electrified drivelines are creating parallel demand for specialized e-fluids. Integrated e-axle systems combine electric motors, power electronics, and gear sets in compact housings, exposing fluids to high shear, thermal stress, and electrical fields. Additive packages introduced in 2025 for hybrid drivetrains emphasize controlled electrical conductivity, copper corrosion inhibition, and long-term oxidation stability. This positions fuel and lubricant additive suppliers as critical partners in the reliability of next-generation mobility platforms.

Carbon Intensity Optimization and Fuel Efficiency in Maritime Shipping

Maritime shipping represents one of the most commercially attractive near-term opportunities for fuel additives. With the International Maritime Organization’s Carbon Intensity Indicator ratings now enforceable, vessel operators are under immediate pressure to improve efficiency without expensive hardware retrofits. Combustion improvers and fuel catalysts have emerged as cost-effective levers. Sea trials reported in 2025 show that advanced marine additives can deliver fuel savings between 2.1% and 3.9%, often sufficient to shift a vessel from a non-compliant rating into an acceptable performance band, avoiding mandatory corrective action plans.

The transition toward alternative marine fuels is reinforcing this opportunity. Methanol-fueled and dual-fuel vessels are expanding rapidly, but methanol’s corrosivity and low lubricity introduce new operational risks. Safety advisories issued in late 2025 highlight the need for methanol-specific corrosion inhibitors and stabilizers, while Very Low Sulfur Fuel Oil continues to require advanced stability additives to prevent sludge formation that currently accounts for roughly 2% of global marine fuel losses. Together, these dynamics position fuel additives as a central enabler of decarbonization, compliance, and cost control across the global shipping fleet.

Fuel Additives Market Share and Segmentation Insights

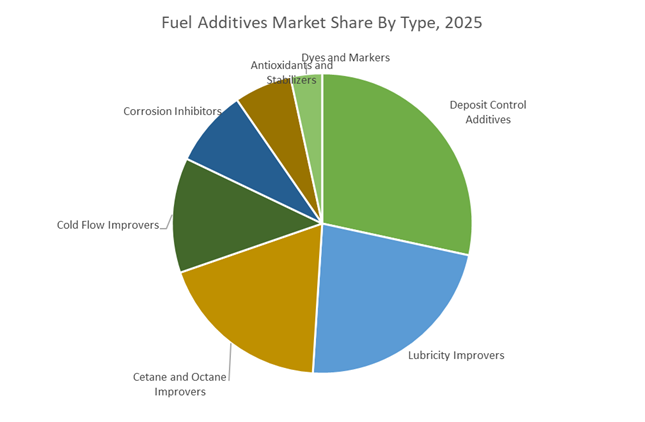

Deposit Control Additives Lead Fuel Additive Demand Through Engine Cleanliness and Performance Optimization

Deposit Control Additives accounted for 28.40% of the Fuel Additives Market share in 2025, making them the most widely used additive category in gasoline and diesel fuel formulations. These additives—commonly referred to as fuel detergents—play a critical role in preventing the accumulation of carbon deposits on fuel injectors, intake valves, and combustion chambers, which can negatively impact engine efficiency, fuel economy, and emissions performance. Modern internal combustion engines operate with tighter tolerances and advanced fuel injection systems, making effective deposit control essential for maintaining optimal combustion efficiency and long-term engine durability. Deposit control additives are therefore incorporated into refinery fuel blends, premium fuels, and aftermarket fuel treatment products used across passenger and commercial vehicles. In 2025, the segment is experiencing significant growth driven by the widespread adoption of gasoline direct injection (GDI) engine technology, which is now dominant in passenger vehicle powertrains. GDI engines provide improved fuel efficiency but are also more prone to carbon buildup on injectors and intake systems. To address this challenge, additive manufacturers have developed advanced detergent chemistries such as polyetheramine (PEA) and polyisobutylene amine (PIBA) specifically engineered for high-performance injector cleaning. These advanced formulations are rapidly expanding within the global deposit control additives market.

Commercial Vehicles Drive the Largest Consumption of Fuel Additives in Heavy-Duty Transport Operations

Commercial Vehicles represented 34.80% of the Fuel Additives Market share in 2025, making them the largest application segment within the global fuel additives industry. Heavy-duty trucks, buses, and commercial delivery vehicles consume large volumes of diesel fuel, often operating under demanding conditions involving long-distance transportation, heavy loads, and extended engine operating hours. These operational characteristics require fuel formulations enhanced with additives that improve engine cleanliness, fuel stability, lubricity, and corrosion protection, ensuring reliable engine performance and reduced maintenance costs. In addition, commercial vehicles must comply with increasingly strict emissions regulations for heavy-duty diesel engines, which depend on consistent fuel quality and effective additive performance. In 2025, the commercial transport sector is increasingly adopting fleet-specific fuel additive optimization programs designed to improve operational efficiency and reduce total fuel costs. Large logistics companies and fleet operators are implementing bulk additive dosing systems at centralized fueling stations, allowing customized treatment levels based on vehicle duty cycles, fuel quality, and route conditions. This approach enables precise additive usage, improves fuel efficiency and engine longevity, and reduces costs compared with standard retail fuel purchasing practices. As commercial transportation continues to expand globally, fleet-focused fuel additive strategies are strengthening the sector’s role as the primary demand driver in the global fuel additives market.

Competitive Landscape in Fuel Additives Market

Afton Chemical Expands Hydrogen Engine and TOP TIER+™ Additive Leadership

Afton Chemical Corporation continues to position itself at the forefront of fuel additive technology, particularly in gasoline direct injection and emerging hydrogen heavy-duty engines. In September 2025, Afton introduced the first commercially available dedicated additive package for Hydrogen Internal Combustion Engines, addressing lubrication film retention and abnormal combustion control unique to HICE applications. The company launched the HiTEC® 65522 series in late 2025 to meet the upgraded TOP TIER+™ gasoline standards requiring a 60% improvement in injector cleanliness. In January 2026, Afton expanded its eVolving eMobility initiative to include Electrified Transmission Fluids designed for high-torque electric drivetrains. Capacity at its Jurong Island facility in Singapore was doubled in late 2025, strengthening supply of ashless dispersants across Asia-Pacific, the fastest-growing fuel additives market.

Lubrizol Advances GDI Protection and Regional Technical Support

The Lubrizol Corporation remains a dominant player in high-specification fuel detergent and lubricant chemistry. In August 2025, Lubrizol certified its GA9110 Series as one of the earliest additive lines compliant with updated TOP TIER+™ fuel performance benchmarks for modern gasoline direct injection engines. In early 2026, the company unveiled next-generation detergent blends engineered to mitigate stochastic pre-ignition in high-pressure direct-injection engines, a growing durability concern in turbocharged platforms. Lubrizol expanded its U.S. West Coast distribution footprint in February 2026 through a strategic partnership with Commerce Hose & Industrial Products. Its Local-for-Local growth strategy was reinforced by opening a Bangkok office in late 2025 to accelerate technical support across Southeast Asia’s expanding automotive and refining markets.

BASF Localizes Keropur® Production to Capture Asia-Pacific Growth

BASF SE leverages its integrated Verbund manufacturing platform to deliver high-performance fuel additives under the Keropur® brand. In September 2025, BASF introduced the Keropur® Gasoline Performance Additive Series engineered to exceed EPA Lowest Additive Concentration requirements while improving injector cleanliness and emissions control. For fiscal year 2026, BASF expects EBITDA before special items between €6.2 billion and €7.0 billion, supported by Chemicals and Nutrition & Care segments. The company localized production of fuel performance additives at its Pudong site in Shanghai to secure share in China, the world’s largest automotive market. Despite commissioning the large-scale Zhanjiang Verbund site, BASF aims to maintain 2026 CO2 emissions within 17.2 to 18.2 million metric tons, reinforcing its decarbonization commitments within the fuel additives value chain.

Infineum Enhances Hybrid Power Unit and Eco-Friendly Additive Suites

Infineum International Limited, a joint venture between Shell and ExxonMobil, specializes in advanced driveline and fuel additive packages. In July 2025, the company introduced eco-friendly gasoline additive suites across Europe that significantly reduce pollutant formation in passenger vehicles. Mid-2025 saw trial production begin at a new blending facility in India to serve localized demand for sulfonate and salicylate additive packages. In early 2026, Infineum launched enhanced additive systems for Hybrid Power Units designed to maintain oxidation stability during frequent stop-start engine cycles. Through collaborative supply security initiatives, including joint ventures with regional OEMs in China and the Middle East, Infineum is strengthening feedstock access and refining hub penetration, supporting long-term growth in performance fuel additives.

Innospec Focuses on Refinery Optimization and Drag Reducing Agents

Innospec Inc. maintains a strong position in refinery fuel additives, pipeline drag reducing agents, and marine fuel treatment chemistries. In March 2025, the company announced a major expansion of its Drag Reducing Agent production in Pleasanton, Texas, which became operational in Q4 2025 to meet rising pipeline throughput demands. Its Fuel Specialties division continues to generate the majority of the company’s annual revenue exceeding $2 billion. The FOA-3 and FOA-5 additive series remain industry benchmarks for stabilizing higher-sulfur distillate fuels and preventing particulate formation in marine and industrial diesel applications. In early 2026, Innospec prioritized refinery economics by developing customized additive solutions that enable refiners to increase the use of lower-cost cracked components in diesel blending pools without compromising fuel stability or emissions compliance.

United States: Injector Cleanliness Standards and New-Fuel Pathways Reshaping Additive Design

The United States fuel additives market is being redefined by tighter OEM performance standards and diversification of fuel pathways. In early 2025, major automakers introduced the TOP TIER+™ gasoline standard, Revision G, raising injector deposit control thresholds for GDI engines and explicitly targeting stochastic pre-ignition and particulate emissions. In response, Afton Chemical launched the HiTEC 65522 series in August 2025, purpose-built to meet TOP TIER+™ certification requirements. This development has accelerated demand for advanced detergent chemistries capable of maintaining injector cleanliness under higher injection pressures and elevated thermal loads.

Supply-side readiness is improving in parallel. BASF unveiled its next-generation Keropur AP 225-20 gasoline performance additive in September 2025 and is upgrading North American manufacturing infrastructure to support commercial deliveries in the first half of 2026. Regulatory dynamics are also influencing formulation strategy. Under the Lowest Additive Concentration framework, the U.S. Environmental Protection Agency finalized a March 2025 rule extending Renewable Fuel Standard compliance timelines, giving additive producers additional lead time to integrate robust detergency with higher biofuel blends. Beyond conventional fuels, Afton Chemical’s September 2025 launch of a dedicated additive for hydrogen-combustion heavy-duty engines signals early market formation around corrosion control and lubrication challenges unique to carbon-free combustion.

India: Ethanol Blending Acceleration Driving Corrosion and Stability Solutions

India’s fuel additives market is expanding rapidly alongside national biofuel policy execution. By July 2025, India achieved an average ethanol blending rate of 19.93%, placing the country on a fast track toward the E20 target for the 2025–26 Ethanol Supply Year. This shift is materially increasing demand for corrosion inhibitors, phase-separation suppressants, and oxidation stability additives to protect fuel systems from ethanol-induced water uptake and material compatibility issues.

Localization of additive supply is strengthening market depth. Infineum progressed construction of a new additive manufacturing plant in India throughout 2025, aimed at serving domestic automotive, marine, and industrial fuel markets with localized formulations. Policy support is extending upstream. Expansion of the Pradhan Mantri JI-VAN Yojana in August 2025 is catalyzing second-generation ethanol projects, driving R&D demand for specialized enzymes and processing additives required for lignocellulosic biomass conversion. Collectively, these developments are positioning India as a growth center for ethanol-compatible fuel additive technologies.

China: Efficiency Mandates and Ashless Chemistries Elevating Performance Thresholds

China’s fuel additives market is entering a stricter compliance cycle driven by national efficiency mandates. Effective January 1, 2026, three mandatory standards came into force requiring an 18% reduction in fuel consumption limits for traditional and hybrid passenger vehicles. These targets are pushing OEMs and fuel suppliers to adopt high-performance friction modifiers and advanced fuel system cleaners that deliver measurable efficiency gains without compromising emissions durability.

Specification alignment is reinforcing this trend. Updates to the GB 17930 gasoline standard are driving a pivot toward low-sulfur, ashless detergent chemistries compatible with China VI-b emissions requirements, now the most stringent in the region for 2026. Capacity building and talent development are supporting domestic innovation. In June 2025, Afton Chemical expanded regional R&D engagement through scholarships at the Lanzhou Institute of Chemical Physics, focusing on tribology and molecular-level performance for next-generation Chinese engines.

Germany and the European Union: Aviation Transition and Green Additive Scale-Up

Germany and the broader European Union are anchoring fuel additive demand to aviation decarbonization and energy transition policies. In February 2025, the EU adopted a Delegated Regulation under the Emissions Trading System to bridge the cost gap between fossil kerosene and sustainable aviation fuels, backed by a €1.6 billion incentive pool. This framework is accelerating uptake of performance-enhanced e-fuels and driving demand for SAF-compatible antioxidants, metal deactivators, and thermal stabilizers.

ReFuelEU Aviation entered into force in January 2025, mandating a 2% SAF blend at EU airports with a trajectory to 6% by 2030. German producers including BASF and Evonik are scaling industrial production of aviation-grade fuel additives to meet these requirements. Evonik reported higher sales volumes in its oil and fuel additive divisions in Q1 2025, supported by demand for high-viscosity index improvers and electrification-driven investments at specialty chemical assets.

Brazil: Biodiesel Compatibility and Regional Distribution Expansion

Brazil’s fuel additives market is advancing through distribution consolidation and biodiesel specialization. In June 2025, Chevron Oronite partnered with ICONIC Base Oil Solutions as its official distributor, integrating OLOA lubricant additives and OGA aftermarket fuel additives into a single supply platform for the Mercosur region. This move is improving access to performance additives across Brazil’s logistics and transportation networks.

Biofuel intensity remains a defining demand driver. At the Asian Lubricant Exhibition 2025, Chevron Oronite showcased additive solutions optimized for high-blend biodiesel usage in heavy-duty engines. These formulations address deposit control, oxidation stability, and fuel system protection in agricultural and freight applications that dominate Brazil’s diesel consumption profile.

Singapore: Marine Decarbonization and Regional Formulation Hub

Singapore is consolidating its role as a regional center for marine and energy-sector fuel additive innovation. In June 2025, Innospec reported that its marine fuel additives enabled customers to avoid 20 million metric tonnes of CO2 in 2024, delivering innovation-endorsed fuel savings for vessels operating under FuelEU Maritime and IMO decarbonization frameworks. The company is scaling Singapore-based operations to support verified efficiency gains in the range of 2.1 to 3.9%.

Regional customization is being strengthened through infrastructure investment. Lubrizol inaugurated its Southeast Asia Innovation Center in Jurong in late 2025, focusing on localizing additive formulations for diverse regional fuel qualities. The center supports development of specialty surfactants and coating solutions aligned with evolving energy-sector requirements across Asia-Pacific.

Summary of Country-Level Strategic Drivers in the Fuel Additives Market

Fuel Additives Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Implications for Fuel Additives

|

|

United States

|

TOP TIER+™ standards and alternative fuels

|

Advanced detergents, hydrogen-engine additives

|

|

India

|

E20 ethanol rollout

|

Corrosion inhibitors and stability enhancers

|

|

China

|

Fuel efficiency mandates

|

Ashless detergents and friction modifiers

|

|

Germany / EU

|

SAF mandates and ETS incentives

|

Aviation-grade antioxidants and stabilizers

|

|

Brazil

|

High biodiesel blends

|

Deposit control and oxidation stability additives

|

|

Singapore

|

Marine decarbonization

|

Efficiency-driven marine fuel additives

|

Fuel Additives Market Report Scope

Fuel Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.4 Billion

|

|

Market Size (2034)

|

$14.9 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type (Deposit Control Additives, Cetane and Octane Improvers, Lubricity Improvers, Antioxidants and Stabilizers, Cold Flow Improvers, Corrosion Inhibitors, Dyes and Markers), By Fuel Type (Gasoline, Diesel, Aviation Fuel, Marine Fuel), By Application (Passenger Vehicles, Commercial Vehicles, Off-Road Equipment, Marine and Aerospace, Industrial Power Generation), By Distribution Channel (Refineries, Aftermarket, Fleet and B2B Services)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Afton Chemical Corporation, The Lubrizol Corporation, Innospec Inc., BASF SE, Chevron Oronite Company LLC, Infineum International Ltd., Evonik Industries AG, LANXESS AG, Dorf Ketal Chemicals, Clariant AG, TotalEnergies, Shell plc, Baker Hughes Company, Sanyo Chemical Industries, Ltd., ENEOS Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fuel Additives Market Segmentation

By Type

- Deposit Control Additives

- Cetane and Octane Improvers

- Lubricity Improvers

- Antioxidants and Stabilizers

- Cold Flow Improvers

- Corrosion Inhibitors

- Dyes and Markers

By Fuel Type

- Gasoline

- Diesel

- Aviation Fuel

- Marine Fuel

By Application

- Passenger Vehicles

- Commercial Vehicles

- Off-Road Equipment

- Marine and Aerospace

- Industrial Power Generation

By Distribution Channel

- Refineries

- Aftermarket

- Fleet and B2B Services

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fuel Additives Industry

- Afton Chemical Corporation

- The Lubrizol Corporation

- Innospec Inc.

- BASF SE

- Chevron Oronite Company LLC

- Infineum International Ltd.

- Evonik Industries AG

- LANXESS AG

- Dorf Ketal Chemicals

- Clariant AG

- TotalEnergies

- Shell plc

- Baker Hughes Company

- Sanyo Chemical Industries, Ltd.

- ENEOS Corporation

*- List not Exhaustive