Metal Deactivator Market 2025–2034: Fuel Stability Innovation, Zinc-Free Additive Systems, and Asia-Pacific Localization Driving $2.9 Billion Outlook at 6.7% CAGR

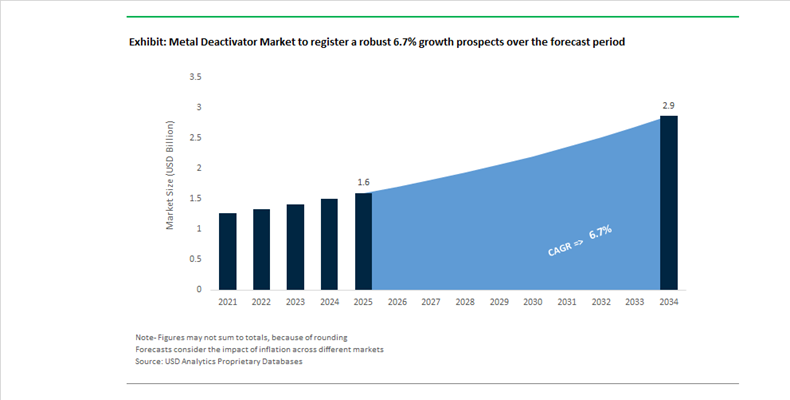

The Metal Deactivator (MDA) Market is projected to expand from $1.6 billion in 2025 to $2.9 billion by 2034, registering a CAGR of 6.7%. Growth is being driven by rising demand for high-performance fuel additives, lubricant stabilizers, hydraulic fluids, EV coolants, and oilfield intermediates that require protection against catalytic oxidation caused by trace metals such as copper, iron, and aluminum. Metal deactivators, typically based on triazole, benzotriazole, and other nitrogen-containing chelating chemistries, play a critical role in improving thermal stability, preventing gum formation, and extending service intervals in high-pressure injection systems and advanced industrial machinery. Increasing electrification, subsea oil production, and stricter fuel quality standards are reshaping the functional requirements for next-generation MDA molecules.

In late 2024, Innospec expanded its international oilfield intermediates portfolio, integrating metal deactivator technologies into refinery stabilization programs targeting jet fuel thermal oxidation stability. In March 2025, Innospec introduced the LaZuli product line for deepwater subsea production, incorporating specialized deactivation chemistries to prevent oxidation and sediment formation in high-pressure umbilical systems exposed to seawater-driven metal catalysis. In May 2025, ProFluid entered a strategic distribution alliance with Yasho Industries to supply high-purity triazole-based metal deactivators across North America for grease, lubricant, and metalworking fluid applications. In June 2025, Lubrizol launched MF9145V in China, a diesel additive integrating advanced MDA technology designed to neutralize trace metal catalysts in high-pressure injection systems and reduce diesel particulate matter formation at the source.

Capacity expansion and formulation innovation accelerated through late 2025 and early 2026. In October 2025, Lubrizol introduced AH933ZF, a zinc-free hydraulic additive package utilizing ashless chemistry to enhance yellow-metal protection while aligning with environmental mandates in forestry and marine sectors. In November 2025, BASF commenced core production at its Zhanjiang Verbund site, localizing precursor supply for Irganox and Irgamet additive lines to reinforce Asia-Pacific supply chain resilience. In April 2025, Clariant advanced restructuring of its Adsorbents and Additives business to focus on higher-margin, sustainability-driven deactivator technologies. At the Lubricant Expo 2026, Vanderbilt Chemicals presented updates to its VANCHEM NATD series engineered for lower pH stability in aqueous systems, targeting long-life EV coolant applications. Concurrently, Lubrizol strengthened its R&D footprint with the opening of innovation centers in Singapore in July 2025 and Shanghai in February 2026, concentrating on nitrogen-based chelating agents and hybrid metal deactivator molecules tailored for emerging fuel compositions and regional regulatory standards.

Metal Deactivator Market Trends and Opportunities

Trend: Mandatory Transition in Aviation Fuel Additives and DMD Replacement

The Metal Deactivator Market is undergoing a structural reset in aviation fuels as regulators and OEMs accelerate the phase-out of legacy chelators such as N,N'-disalicylidene-1,2-propanediamine (DMD). Concerns around filter clogging, thermal degradation, and long-term material incompatibility have pushed aviation authorities and airframe manufacturers to qualify safer, non-DMD chemistries. As of late 2024 and throughout 2025, aerospace OEMs finalized the transition away from legacy metal deactivators, aligning with the broader compliance posture reflected in updated Federal Aviation Administration directives, including FAA-2025-1104 issued in October 2025. Although focused on oxygen systems, these directives signal a wider intolerance for additive chemistries that introduce latent operational risks in critical flight systems.

Industry benchmarks have tightened accordingly. ASTM D1655 now allows a cumulative reblending threshold of 5.7 mg/L for approved metal deactivators, forcing refineries and airport fuel farms to adopt next-generation additives that preserve Jet Fuel Thermal Oxidation Tester performance during long-term storage and high-altitude operation. The shift is further amplified by Sustainable Aviation Fuel blending. In December 2025, the Government of India announced a 1% SAF mandate for 2027, mirroring similar policy momentum across Europe and the UK. SAF blends tend to oxidize faster than conventional jet fuel due to residual organic acids and trace metals, prompting refiners to integrate specialized metal deactivation packages that stabilize bio-derived feedstocks and prevent sediment formation.

Trend: Synergistic Deactivator Loadings for High-Temperature Hybrid Engine Oils

Hybrid Electric Vehicles are reshaping lubricant formulation requirements and elevating the strategic importance of metal deactivators. Frequent stop-start cycles in HEVs accelerate fuel dilution and moisture ingress, creating acidic conditions that catalyze copper corrosion in bearings and bushings. To address this, lubricant formulators are increasing deactivator treat rates and deploying synergistic chemistries that protect yellow metals without compromising low-viscosity performance. In December 2025, TotalEnergies introduced Quartz Ineo Xtra EC6 0W-20, among the first lubricants meeting the new API SQ and ILSAC GF-7 standards. These specifications demand heightened resistance to stochastic pre-ignition and metal-catalyzed oxidation, driving metal deactivator loadings 15 to 20% higher than prior-generation formulations.

The move toward ultra-low viscosity grades such as 0W-8 and 0W-12 adds further complexity. Metal deactivators must be surface-active enough to protect exposed metal interfaces while avoiding increases in fluid friction. As a result, formulators are combining triazole derivatives with advanced antioxidants to maintain film strength under extreme thermal stress in downsized, turbocharged engines. Innovation is also accelerating in ashless chemistry. In June 2025, Lubrizol launched MF9145V in China, an ashless metal deactivator designed to enhance combustion efficiency and reduce particulate matter generation, directly supporting the durability of gasoline particulate filters in next-generation hybrid platforms.

Opportunity: Biodegradable Metal Deactivators for Environmentally Acceptable Lubricants

Environmental regulation is converting biodegradable metal deactivators from a niche preference into a non-discretionary requirement. Under the U.S. Vessel Incidental Discharge Act, additives used in marine lubricants must meet strict OECD 301 biodegradability criteria, demonstrating more than 60% degradation within 28 days. This has created a high-value opportunity for tartaric acid and succinic acid-based chelators that replace persistent nitrogen-containing compounds traditionally used in metal deactivation. The addressable market spans the USD 2.5 billion marine and offshore lubricant segment, where oil-to-sea interfaces are under intense regulatory scrutiny.

Commercial momentum is building. In February 2025, TotalEnergies Lubrifiants expanded its portfolio through the acquisition of low-VOC and bio-based hydraulic fluid technologies, signaling consolidation around EAL-compliant formulations. These products rely on metal deactivation systems certified as non-toxic to aquatic life under OECD 201 to 203 testing. Parallel to this, Clariant is advancing its Winning Ways strategy by replacing petrochemical triazoles with plant-based ligands. This transition enables lubricant manufacturers to meet EU Ecolabel requirements while maintaining high-temperature protection for copper and brass components, opening durable, regulation-driven growth pathways.

Opportunity: Stabilization of Sustainable Aviation Fuel and Renewable Diesel

The global scale-up of Sustainable Aviation Fuel and renewable diesel is unlocking a second major growth vector for metal deactivators. As SAF production approaches 1.3 billion liters in 2025, fuel stability has emerged as a critical bottleneck. Bio-based fuels often contain residual acids and trace metals that accelerate peroxide formation and sediment buildup, particularly during long-term storage. Mandates are converting this challenge into guaranteed demand. The UK SAF Mandate, effective January 1, 2025, requires a 2% blend rising to 10% by 2030, creating sustained offtake for advanced metal deactivators capable of preserving fuel integrity across global distribution networks.

Technical barriers remain high, favoring specialized suppliers. Renewable diesel and SAF derived from Hydro-processed Esters and Fatty Acids are prone to catalytic degradation when exposed to copper or iron fuel system components. Industry research from late 2024 shows that Spec-Aid 8Q462-class stability additives can raise a fuel’s thermal threshold by approximately 100°F, a decisive advantage for military and commercial jet engines operating on bio-blends. Refiners are responding by integrating metal deactivation at the point of production. In December 2025, Indian Oil Corporation received ISCC-CORSIA certification for SAF and embedded metal deactivation chemistry into its refining workflow, ensuring drop-in readiness and mitigating filterability risks during international transport.

Metal Deactivator Market Share and Segmentation Insights

Copper Deactivators Lead Metal Deactivator Market with Oxidation Control in Fuel and Lubricant Systems

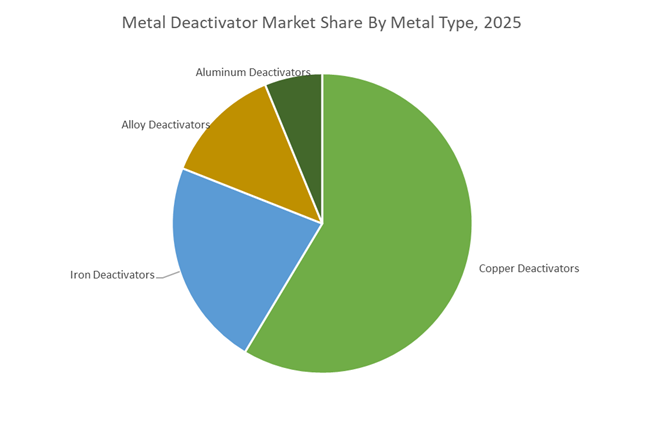

Copper deactivators accounted for 58.6% of the Metal Deactivator Market share in 2025, making them the dominant additive type used in fuel and lubricant stabilization formulations. Copper is highly catalytically active in hydrocarbon systems and can significantly accelerate oxidation reactions in fuels and lubricants, leading to gum formation, sludge buildup, and degradation of fluid quality. Even trace amounts of copper originating from fuel system components, pipelines, storage tanks, and engine parts can initiate these unwanted reactions. Copper deactivators function by forming stable complexes with dissolved copper ions, neutralizing their catalytic activity and preventing oxidative degradation. These additives are widely incorporated into gasoline, diesel, aviation fuels, industrial lubricants, and specialty fluids, where maintaining long-term chemical stability is essential for performance and storage reliability. In 2025, the increasing use of biofuels such as biodiesel and renewable diesel has introduced additional stability challenges, as bio-derived fuel components exhibit higher reactivity with copper surfaces. As a result, additive manufacturers have developed advanced copper deactivator chemistries optimized for modern biofuel blends, ensuring improved oxidation resistance and deposit control.

Fuel Additives Segment Drives the Largest Demand for Metal Deactivators

Fuel additives accounted for 42.8% of the Metal Deactivator Market share in 2025, making fuel stabilization the largest application for these chemical additives. Metal deactivators are essential components in gasoline, diesel, jet fuel, marine fuels, and emerging biofuel blends, where they protect fuel quality by preventing metal-catalyzed oxidation reactions during storage and operation. Without metal deactivators, fuels exposed to copper or other catalytic metals can develop oxidation products, gum deposits, and insoluble residues that negatively affect engine performance and fuel system reliability. These additives therefore play a critical role in meeting fuel quality standards, storage stability requirements, and engine cleanliness specifications established by global fuel regulations and industry standards. In 2025, the increasing complexity of fuel formulations has further strengthened demand for metal deactivators. Modern fuels often contain oxygenated components, renewable fuels, and advanced additive packages, which can increase susceptibility to oxidation under high-temperature and long-term storage conditions. Fuel formulators therefore rely on metal deactivators to maintain chemical stability, prevent deposit formation, and ensure consistent fuel performance across distribution and storage systems.

Metal Deactivator Market Competitive Landscape

The metal deactivator market in 2026 is driven by nitrogen-based chelating agents, surface-active passivation chemistry, and high-performance additive synergies. Demand is rising with SAF, biodiesel, and e-mobility fluids, where copper passivation, oxidation stability, and extended drain intervals are critical for modern fuel systems and industrial lubricants.

BASF strengthens metal passivation leadership through Verbund integration and APAC localization

BASF SE is reinforcing its leadership in metal deactivators through its Verbund-integrated production model and “local-for-local” strategy. The 2026 startup of its Zhanjiang site significantly enhances regional supply of high-performance fuel additives and metal passivators in Asia-Pacific. Its ECMS division is driving earnings growth through optimized cost structures and advanced catalyst systems. By divesting non-core businesses like decorative paints, BASF is sharpening its focus on specialty additives with higher margins. Its R&D capabilities enable rapid adaptation to REACH and TSCA regulations, particularly in copper deactivation and antioxidant synergy. BASF’s portfolio is increasingly aligned with sustainable fuels and high-voltage system protection in next-generation mobility.

Lubrizol advances sustainable grease and metal deactivation chemistry for heavy-duty applications

Lubrizol Corporation is expanding its footprint in metal deactivators through sustainable chemistry and localized innovation hubs in Asia. The HybriCal™ grease system introduces lithium-free formulations that enhance environmental compliance while maintaining high-load performance. Its Singapore and Shanghai innovation centers support advanced lubricant and coating additive development tailored to regional industrial needs. Strategic collaboration with Fulai New Material strengthens integration between coatings and additive technologies. Lubrizol is also focusing on mining and heavy machinery sectors, where metal deactivators are essential for extending equipment life. Its solutions emphasize oxidation control, wear protection, and compatibility with biofuels and electrified drivetrains.

Clariant drives circular additive innovation with high-efficiency deactivators and regulatory compliance

Clariant AG is positioning itself as a sustainability-driven leader in metal deactivators, supported by strong EBITDA margins of 17.8% in 2026. Its innovations in pyrolysis oil upgrading enable circular feedstocks for additive manufacturing, aligning with global decarbonization goals. The company’s compliance with EU Regulation 2026/245 highlights its strength in navigating stringent environmental and food-contact standards. Clariant’s portfolio emphasizes high-performance antioxidants and metal deactivators for agrochemicals and industrial fluids. Its streamlined organizational model enhances customer-centric innovation and faster commercialization. By integrating circular chemistry with advanced additive systems, Clariant is strengthening its competitive edge in sustainable passivation technologies.

Afton Chemical pioneers metal deactivation for hydrogen engines and e-mobility fluids

Afton Chemical is advancing metal deactivator technologies tailored for next-generation fuels and electrified drivetrains. Its HiTEC® 12582 additive is a breakthrough for hydrogen engines, addressing corrosion and metal-catalyzed degradation under extreme conditions. The company’s eVolving eMobility platform includes over 1,000,000 km of testing, ensuring durability and compatibility in high-voltage systems. Afton’s expertise in OEM specifications, including DEXRON®-VI evolution, supports its leadership in transmission and driveline fluids. Its research highlights the critical role of metal deactivators in stabilizing biodiesel and preventing injector fouling. Afton continues to focus on ultra-low viscosity fluids and advanced oxidation control for future mobility systems.

Vanderbilt Chemicals leads copper passivation with ashless metal deactivators for lubricants

Vanderbilt Chemicals, LLC is a key specialist in ashless metal deactivators and corrosion inhibitors for non-ferrous metals. Its CUVAN® 484 and CUVAN® 303 series are industry benchmarks for copper passivation in lubricants and greases. The VANLUBE® product line offers multifunctional solutions, combining metal deactivation with rust inhibition and oxidation stability. Innovations like VANLUBE® NA provide superior performance in low-pH environments, enhancing stability in water-based systems. Vanderbilt’s additives form protective molecular films that prevent catalytic oxidation in turbines and high-speed machinery. Its focus on clean chemistry and regulatory compliance supports demand for low-emission, high-efficiency lubricant formulations.

United States: Fuel Standard Tightening and Multisector Passivation Demand

The United States metal deactivator market is being reshaped by fuel performance regulation, alternative energy adoption, and rapid growth in data-intensive infrastructure. In September 2025, BASF launched its next-generation Keropur Gasoline Performance Additive Series to align with the U.S. TOP TIER Plus specification. These formulations embed advanced metal deactivators to exceed EPA Lowest Additive Concentration thresholds well ahead of the January 2027 compliance deadline. Parallel product innovation is visible at Afton Chemical, which introduced the first dedicated additive for hydrogen-powered heavy-duty engines in 2025, incorporating specialized metal passivators to manage oxidative stress unique to high-pressure hydrogen combustion systems.

Regulatory momentum under the Renewable Fuel Standard is also amplifying demand. The EPA’s proposed 2026–2027 RFS volumes are driving higher production of biomass-based diesel, where metal deactivators play a critical role in neutralizing residual transesterification catalysts that otherwise destabilize fuel during storage. Beyond fuels, application breadth is widening. Vanderbilt Worldwide expanded its CUVAN and VANLUBE portfolios in 2025 with ashless, oil-soluble deactivators for the fast-growing U.S. data center liquid cooling market, protecting copper-based loops from dielectric fluid degradation. Aviation is another growth vector, as U.S. lubricant formulators integrate triazole-based metal deactivators in 2026 to address metal-catalyzed gum formation risks in sustainable aviation fuel blends.

China: Export-Led Additives and AI-Optimized Blending

China’s metal deactivator market is advancing through coordinated industrial policy, capacity expansion, and digital manufacturing. In September 2025, the Ministry of Industry and Information Technology issued a growth stabilization plan prioritizing innovation platforms for advanced fine chemicals, accelerating domestic production of high-purity metal deactivators. This policy backdrop coincides with China’s transition from net importer to net exporter of lubricant additives between 2021 and 2025, with companies such as Richful scaling capacity toward integrated additive packages that include copper and iron passivators for global markets.

Foreign and domestic investments are reinforcing supply depth. Lubrizol is finalizing a major expansion at its Zhuhai blending facility during 2025–2026, adding 63,000 tons per year of capacity to serve Asia-Pacific automotive lubricants rich in metal deactivation chemistry. Product innovation is extending into electric mobility. Chinese formulators unveiled low-conductivity EV coolants in mid-2025 that rely on aluminum-alloy protection additives to preserve dielectric properties in battery cooling systems. Under the “AI plus Petrochemicals” initiative, blending plants are deploying real-time molecular monitoring to optimize metal deactivator dosing in turbine oils, reducing additive overuse and cutting chemical waste by an estimated 12%.

Germany and Benelux: REACH-Driven Reformulation and Automotive Performance

Germany and the Benelux region are at the regulatory forefront of metal deactivator reformulation. On November 5, 2025, the European Chemicals Agency expanded the REACH Candidate List of substances of very high concern to 251 entries, forcing lubricant and masterbatch producers to replace legacy benzotriazole-based deactivators with compliant alternatives by early 2026. This regulatory pressure is accelerating demand for next-generation passivators that deliver oxidation control without triggering toxicological flags.

Industry response has been swift. At Lube Expo Europe 2025, Chevron Oronite presented its OLOA 55620 technology, leveraging advanced metal deactivators to sustain low-temperature fluidity and oxidation resistance in European passenger car motor oils. Process industries are also affected. BASF deployed SYNSPIRE catalyst technology at the Nan Ya Plastics 2-EH facility in 2025, underscoring the need for precise post-reaction metal deactivation to protect downstream plasticizer purity. With UK REACH registration milestones approaching in October 2026, European suppliers are finalizing dossiers to ensure uninterrupted access to the British automotive and power generation markets.

Singapore and Southeast Asia: Marine Conditions and Biodiesel Compatibility

Singapore has emerged as a development hub for metal deactivators tailored to tropical and marine environments. In 2025, Lubrizol inaugurated its Southeast Asia Innovation Center in Jurong, focusing on local-for-local solutions that address high humidity and salt exposure. R&D efforts are centered on deactivators that prevent copper-induced corrosion in vessel steering systems and marine lubricants operating in aggressive coastal conditions.

Regional fuel transitions are shaping additive design. The Asian Lubricant Exhibition 2025 in Singapore showcased multiple biodiesel-compatible metal deactivators engineered to neutralize copper and iron activity in B20 and B30 blends prevalent in Indonesia and Thailand. These additives are increasingly specified for 2026 biodiesel standards, reflecting Southeast Asia’s dual focus on renewable fuels and asset durability in warm, high-moisture climates.

Country-Level Strategic Positioning in the Metal Deactivator Market

Metal Deactivator Market County Level Snapshot

|

Country / Region

|

Strategic Driver

|

Key Application Focus

|

Regulatory or Policy Catalyst

|

Competitive Differentiation

|

|

United States

|

Fuel standards and energy transition

|

Gasoline, SAF, data center cooling

|

TOP TIER Plus, RFS, EPA LAC

|

Multisector performance leadership

|

|

China

|

Export growth and digital blending

|

Automotive, EV coolants, turbines

|

MIIT growth plan, AI integration

|

Scale with precision dosing

|

|

Germany and Benelux

|

REACH compliance

|

PCMO, plastics, process catalysts

|

REACH Annex updates, UK REACH

|

Regulatory-led reformulation

|

|

Singapore and Southeast Asia

|

Marine and biodiesel conditions

|

Marine lubricants, B20/B30 fuels

|

Regional biodiesel mandates

|

Climate-specific formulations

|

Metal Deactivator Market Report Scope

Metal Deactivator Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.6 Billion

|

|

Market Size (2034)

|

$2.9 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Metal Type (Copper Deactivators, Aluminum Deactivators, Iron Deactivators, Alloy Deactivators), By Formulation (Oil-Soluble, Water-Soluble), By Chemistry (Triazole-Based Deactivators, Thiadiazole-Based Deactivators, Phenolic-Based Deactivators, Amine-Based Deactivators), By Application (Fuel Additives, Lubricant Additives, Industrial Fluids, Polymers and Plastics), By End-Use Sector (Automotive and Transportation, Aviation and Aerospace, Oil and Gas, Power Generation, Industrial Manufacturing, Electrical and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Lubrizol, Afton Chemical, Innospec, Chevron Oronite, Vanderbilt Chemicals, ADEKA, Clariant, Dorf Ketal Chemicals, PMC Specialties Group, King Industries, Mayzo, Richful Lube Additive, Songwon Industrial

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Deactivator Market Segmentation

By Metal Type

- Copper Deactivators

- Aluminum Deactivators

- Iron Deactivators

- Alloy Deactivators

By Formulation

- Oil-Soluble

- Water-Soluble

By Chemistry

- Triazole-Based Deactivators

- Thiadiazole-Based Deactivators

- Phenolic-Based Deactivators

- Amine-Based Deactivators

By Application

- Fuel Additives

- Lubricant Additives

- Industrial Fluids

- Polymers and Plastics

By End-Use Sector

- Automotive and Transportation

- Aviation and Aerospace

- Oil and Gas

- Power Generation

- Industrial Manufacturing

- Electrical and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metal Deactivator Market

- BASF

- Lubrizol

- Afton Chemical

- Innospec

- Chevron Oronite

- Vanderbilt Chemicals

- ADEKA

- Clariant

- Dorf Ketal Chemicals

- PMC Specialties Group

- King Industries

- Mayzo

- Richful Lube Additive

- Songwon Industrial

*- List not Exhaustive