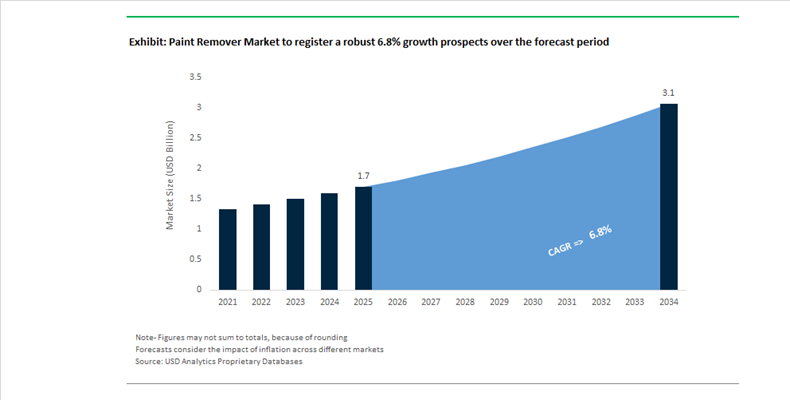

Paint Remover Market Valued at $1.7 Billion in 2025 with 6.8% CAGR Driven by NMP Bans and Bio-Based Stripper Reformulations

The Paint Remover Market is valued at $1.7 billion in 2025 and is projected to reach $3.1 billion by 2034, expanding at a CAGR of 6.8%. Market growth is being reshaped by regulatory pressure on methylene chloride and N-Methylpyrrolidone (NMP), accelerating innovation in low-VOC, biodegradable, and gel-based stripping technologies. Demand is rising across architectural renovation, automotive refinishing, marine maintenance, and industrial surface preparation. As global coatings volumes expand, the need for compliant, high-efficiency paint stripping solutions is intensifying, particularly in North America and Europe where occupational exposure limits are tightening.

In early 2024, AkzoNobel divested its Chinese decorative paints business to Sherwin-Williams, allowing strategic focus on premium industrial coatings and marine stripping technologies. In 2024, Propspeed introduced its dust-free “Stripspeed” solvent system targeting marine coating removal without abrasive grinding, reducing hazardous particulate generation in shipyards. In March 2025, Rust-Oleum, a subsidiary of RPM International, launched a no-drip gel paint remover optimized for vertical and intricate surfaces, improving dwell time and multi-layer stripping efficiency. In April 2025, RPM strengthened its consumer surface restoration portfolio through the acquisition of Star Brands Group, expanding abrasive and mild-chemical stripping capabilities.

Regulatory inflection accelerated in May 2025 when the U.S. Environmental Protection Agency proposed a formal ban on NMP in paint removers. This move triggered rapid reformulation toward dibasic esters, benzyl alcohol systems, and terpene-based solvents to maintain performance while complying with TSCA risk management frameworks. In April 2025, 3M launched a next-generation biodegradable solvent remover with reduced odor and improved VOC compliance for professional contractors and DIY users. In February 2025, Henkel expanded its Düsseldorf R&D center to accelerate green chemistry stripping technologies aligned with EU REACH directives.

Market consolidation is intensifying competitive dynamics. In June 2025, JSW Paints acquired a 74.7% stake in AkzoNobel India, expanding access to premium surface preparation and stripper portfolios across Asia. On October 1, 2025, Sherwin-Williams completed its acquisition of BASF’s Brazilian decorative paints business, including the Suvinil brand, strengthening its South American architectural remover presence. In December 2025, AkzoNobel and Axalta Coating Systems announced a merger of equals expected to close in late 2026, consolidating industrial and automotive paint remover portfolios under one entity. In February 2026, Henkel agreed to acquire Stahl Group for €2.1 billion, expanding its footprint in industrial surface treatment and stripping chemistries. The market is transitioning toward bio-based solvent systems, low-VOC gel formulations, marine dust-free stripping solutions, and integrated coatings-removal ecosystems supported by large-scale M&A consolidation.

Paint Remover Market Trends and Opportunities

Regulatory Phase-Out of Methylene Chloride and NMP Resets the Market

The paint remover market is undergoing a forced transformation as regulatory agencies effectively eliminate methylene chloride and N-methyl-2-pyrrolidone from consumer and most commercial uses. In April 2024, the U.S. EPA finalized a TSCA rule banning methylene chloride in consumer products, with retail distribution ending by May 2025 and most industrial uses prohibited by April 2026. In Europe, REACH restrictions on NMP tightened further in 2024, closing remaining exemptions and accelerating full market exit.

Major retailers including The Home Depot, Lowe’s, and Walmart removed these products ahead of regulatory deadlines. This created a significant supply gap in the DIY segment, rapidly filled by dimethyl adipate and benzyl alcohol-based formulations. Regulatory pressure has effectively shifted competitive advantage toward suppliers with ready-to-scale compliant alternatives.

Bio-Based and Safer Solvent Systems Gain Industrial Acceptance

Industrial maintenance and marine sectors are increasingly adopting green chemistry principles to reduce hazardous waste costs and workplace health liabilities. U.S. federal procurement rules under the BioPreferred Program now prioritize bio-based paint removers for government contracts exceeding $10,000 annually. This policy shift is accelerating demand for solvents derived from corn, soy, and citrus feedstocks.

In April 2025, 3M launched a biodegradable, low-odor paint remover designed to meet low-VOC standards while maintaining industrial stripping performance. This reflects a broader market trend where bio-based systems are no longer niche alternatives but direct competitors to traditional solvents. OSHA data further strengthens the business case, indicating that safer formulations can reduce PPE and medical surveillance costs by 15%–20% per industrial site.

Precision Paint Removers for Aerospace and Automotive Refinishing

The expansion of global aircraft fleets and aging vehicle populations is driving demand for precision paint removers that protect advanced substrates. Aerospace Maintenance, Repair, and Overhaul providers increasingly require strippers that can selectively remove coatings without damaging aluminum alloys or carbon fiber composites.

Advanced refinishing programs now integrate automated thickness tracking and controlled chemical application, enabling targeted stripping with minimal chemical usage. This approach is particularly critical for military and stealth aircraft, where radar-absorbing materials demand pH-neutral, substrate-safe formulations. In the automotive sector, the rising average vehicle age has boosted demand for gel-based, non-drip removers that enable localized repairs, reducing chemical waste by up to 30%.

Low-Odor, Water-Washable Removers for Residential and Heritage Restoration

Historic preservation and residential renovation are emerging as resilient demand drivers for paint removers. The EPA Renovation, Repair, and Painting Rule continues to enforce strict controls on lead-based paint removal, favoring chemical wet-method solutions that encapsulate lead particles and minimize airborne dust. Enforcement actions in 2024–2025, including six-figure penalties, have reinforced compliance urgency among contractors.

Large-scale public restoration projects, such as the Erasmus Bridge refurbishment in Rotterdam, demonstrate growing demand for semi-aqueous and water-based paint removers that can be applied safely in open, public environments. At the consumer level, surveys consistently show low odor and water washability as top purchase criteria. Brands such as Rust-Oleum have responded with gel-based formulations tailored for furniture restoration and architectural detailing, aligning with the growing trend of home upcycling and renovation.

Paint Remover Market Share and Segmentation Insights

Solvent-Based Paint Removers Lead Market Demand in High-Performance Coating Stripping Applications

Solvent-based paint removers accounted for 42.80% of the Paint Remover Market by product type in 2025, maintaining the largest share due to their superior stripping efficiency in demanding industrial and professional applications. These formulations are widely used in automotive refinishing, industrial maintenance, aerospace surface preparation, and heavy duty coating removal where rapid paint breakdown and deep penetration into multilayer coatings are required. Although regulatory pressure has restricted certain hazardous solvents, manufacturers continue to innovate with alternative solvent systems such as benzyl alcohol, dimethyl sulfoxide, and N-methyl pyrrolidone to maintain stripping performance while improving safety characteristics. These reformulated solvent systems allow effective coating removal across metals, composites, and wood substrates used in industrial and restoration projects.

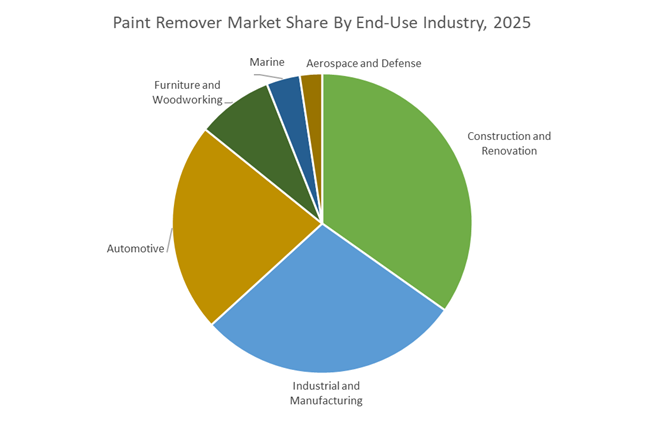

Construction and Renovation Sector Drives Paint Remover Consumption in Building Restoration Projects

Construction and renovation accounted for 34.80% of the Paint Remover Market by end-use industry in 2025, reflecting the high demand for coating removal solutions in residential and commercial building restoration activities. Paint removers are widely used in architectural renovation projects to strip coatings from doors, trim, metal surfaces, and structural components before repainting or refinishing. Aging building infrastructure in many regions continues to support steady demand for effective coating removal technologies. In 2025, the increasing focus on lead paint abatement in older buildings is influencing product development, with specialized paint removers designed to encapsulate lead residues and support safe removal procedures that integrate dust containment systems and HEPA vacuum equipment in regulated renovation environments.

Paint Remover Market Competitive Landscape

The Paint Remover Market is shifting toward bio-based, non-methylene chloride formulations and VOC-compliant stripping systems. Key players are focusing on water-based chemistries, circular coatings removal, and digital application tools to enhance worker safety, reduce hazardous waste, and improve efficiency across automotive, aerospace, and industrial maintenance sectors.

PPG drives waterborne coatings innovation to enable low-toxicity paint removal systems

PPG Industries, Inc. is strengthening its position in the paint remover market through sustainable coatings innovation and digital integration. Under its “Refresh & Sustain” strategy, PPG is prioritizing environmentally compliant stripping systems supported by waterborne coating technologies such as AQUACRON® WSP primers, which enable easier removal and reduced chemical intensity. With $15.8 billion in sales and operations in over 70 countries, the company maintains a strong global footprint. The renewal of its Asian Paints joint venture enhances distribution in high-growth Asia-Pacific refinish markets. Digital tools like MOONWALK® and ADJUSTRITE® optimize chemical usage and reduce waste by up to 15%. This integration of coatings design and removal efficiency strengthens PPG’s competitive advantage.

AkzoNobel-Axalta merger reshapes global leadership in low-VOC industrial paint removal

AkzoNobel N.V. is undergoing a transformative merger with Axalta, creating a $17 billion coatings powerhouse with strong capabilities in automotive refinish and industrial paint removers. The combined entity will integrate over 100 brands and 173 manufacturing sites, significantly expanding global reach. AkzoNobel’s 2025 EBITDA of €1.44 billion and margin improvement to 14.2% provide financial strength to accelerate low-VOC remover innovation. Strategic divestment of its Indian operations and €98 million OPEX reduction support portfolio optimization toward high-margin markets. Circular initiatives, including recycled-content stripping agents and paint return programs, align with sustainability regulations. This consolidation positions the company as a dominant force in next-generation paint removal technologies.

Sherwin-Williams expands industrial stripping solutions through acquisition-led growth

The Sherwin-Williams Company is enhancing its position in the paint remover market through strategic acquisitions and strong distribution channels. The $1.15 billion acquisition of BASF’s Brazilian decorative paints business strengthens its supply chain and presence in South America. With $23.57 billion in 2025 sales, the company demonstrates resilience despite softer demand conditions. Growth in Protective and Marine coatings segments is driving demand for heavy-duty industrial paint removers. Its Paint Stores Group provides a direct-to-professional channel for high-performance stripping products. Operational restructuring initiatives aim to optimize costs and improve margins by 2026. This combination of scale, distribution, and targeted growth supports its competitive positioning.

RPM leverages consumer brands and operational efficiency to scale specialty paint removers

RPM International Inc. is a leader in consumer and DIY paint remover segments, supported by brands such as Rust-Oleum® and Zinsser®. Its MAP 2025 program has driven consistent profitability, delivering record adjusted EBIT across multiple quarters. The Rust-Oleum® Krud Kutter® line remains a key product in eco-friendly and high-performance stripping solutions. Expansion into Southeast Asia through its Malaysia facility strengthens supply for infrastructure and construction applications. RPM’s strong financial discipline is reflected in its 52-year dividend growth record and ongoing cost-saving initiatives targeting $100 million annually by 2027. Acquisition-driven growth continues to expand its product portfolio. This balance of brand strength, operational efficiency, and regional expansion reinforces RPM’s market presence.

Henkel integrates advanced surface treatment technologies to expand green paint remover portfolio

Henkel AG & Co. KGaA is expanding its role in the paint remover market by integrating advanced surface treatment technologies into its Adhesive Technologies segment. The €2.1 billion acquisition of Stahl enhances its capabilities in high-performance coatings removal and flexible material processing. With €20.5 billion in 2025 sales and a 14.8% EBIT margin in Adhesive Technologies, Henkel maintains strong financial stability. The company is shifting toward water-based and environmentally responsible formulations, aligning with global regulatory trends. Completion of its Consumer Brands merger has generated over €525 million in savings, which are being reinvested into bio-based chemical R&D. This strategic integration of sustainability and innovation strengthens Henkel’s competitive positioning.

United States – Regulatory Shock and Rapid Reformulation of the Stripping Ecosystem

The United States paint remover industry entered a structural reset following the U.S. Environmental Protection Agency Final Rule effective February 3, 2025, which terminated retail distribution of methylene chloride-based paint removers and culminated in a nationwide consumer sales ban by May 5, 2025. This regulatory inflection point has forced manufacturers, distributors, and retailers to execute an accelerated transition toward alternative solvent chemistries, primarily centered on ethyl lactate, dibasic esters, benzyl alcohol blends, and soy-derived esters. The regulatory burden deepens further with the EPA-mandated prohibition on most industrial and commercial dichloromethane applications by April 28, 2026, excluding narrowly defined aerospace and defense use cases operating under Workplace Chemical Protection Programs. As a result, industrial users are redesigning stripping workflows around low-toxicity formulations, longer dwell times, and mechanical augmentation.

Market behavior is simultaneously being reshaped by retailer and workplace dynamics. Major home improvement chains, including Home Depot, have expanded shelf space for USDA BioPreferred-certified paint removers in partnership with brands such as Behr, reflecting both compliance and consumer risk aversion. The regulatory divergence between OSHA exposure standards and the EPA’s new 2 ppm 8-hour limit has triggered an estimated industry-wide investment exceeding USD 150 million in ventilation retrofits, real-time air monitoring, and operator training. Parallel to chemical substitution, aerospace maintenance hubs in Florida and Washington are scaling laser coating removal infrastructure, adopting robotic and automated systems to bypass solvent exposure entirely for high-value aircraft platforms.

China – Policy-Guided Green Substitution and Export Realignment

China’s paint remover industry is transitioning under a state-directed sustainability framework rather than outright bans. In June 2025, the Ministry of Industry and Information Technology of China issued a Green and Low-Carbon Standardization roadmap that prioritizes revisions to VOC-related standards for industrial paint removers, with formal adoption targeted by 2027. This policy signal is driving domestic formulators to re-engineer stripping products around oxygenated solvents and water-borne systems rather than chlorinated chemistries, particularly in electronics, shipbuilding, and heavy equipment maintenance.

Supply-side adjustments are already visible. Chemical producers in Zhejiang expanded output of electronic-grade isopropyl alcohol and related oxygenated solvents during 2025, enabling substitution of toxic strippers in semiconductor and PCB cleaning operations. In November 2025, BASF SE commissioned a specialty dispersant and additive line in Nanjing to support stabilization of next-generation water-based stripping formulations. Trade dynamics are also shifting, as U.S. restrictions on methylene chloride products have pushed Chinese exporters to reorient toward Southeast Asia and the Middle East, while domestic R&D increasingly favors high-pressure water jet and mechanical stripping technologies for shipyards and offshore structures.

Germany – Compliance-Driven Process Innovation and Solvent Recovery

Germany represents the most compliance-intensive environment for paint removers within Europe, shaped by expanding chemical restrictions and aggressive VOC reduction targets. The enforcement of Commission Regulation (EU) 2025/1731 under REACH Annex XVII in October 2025 added 16 CMR substances to the restricted list, directly constraining the availability of traditional high-solvency stripping feedstocks. This has accelerated a market-wide shift toward low-hazard solvent systems, hybrid mechanical-chemical removal, and non-solvent technologies in industrial refinishing and OEM manufacturing.

Industry response has been characterized by process innovation rather than simple substitution. BASF Coatings expanded its Biomass Balance Eco Balance portfolio in 2025, enabling refinish operations to reduce lifecycle carbon intensity across both paint removal and re-application stages. German automotive OEMs, including BMW and Mercedes-Benz, have increased adoption of pulse-laser stripping for E-coat removal to comply with 2026 plant-level VOC ceilings. Complementing these shifts, Bavaria-backed state programs in 2025 subsidized closed-loop solvent recovery systems for furniture and specialty refinishers, targeting recovery rates of up to 95% for volatile organic solvents.

India – Standards Enforcement and Infrastructure-Led Demand Expansion

India’s paint remover market is being reshaped by a combination of regulatory tightening and infrastructure-driven demand. In December 2025, the Department of Chemicals and Petrochemicals enforced mandatory Bureau of Indian Standards certification for critical solvents such as toluene and p-xylene, effectively excluding non-compliant imports from the domestic stripping supply chain. This move is strengthening quality assurance across industrial paint removal intermediates while indirectly encouraging local sourcing and formulation upgrades.

On the demand side, sustainability-linked product differentiation is gaining traction. Following the rollout of Dulux Better Living Air Clean Biobased, AkzoNobel India expanded its distribution of bio-based stripping and surface preparation solutions in late 2025 to align with green building certifications in major metros. Meanwhile, the PM Gati Shakti infrastructure program is increasing consumption of industrial-grade paint removers for bridge maintenance, rolling stock refurbishment, and public asset renewal. These applications are favoring non-corrosive, non-DCM formulations that balance safety with performance under high-throughput maintenance schedules.

Indonesia – Bio-Based Leadership in Tropical Conditions

Indonesia has emerged as a regional reference point for bio-based paint remover formulations, driven by both climatic suitability and renewable feedstock availability. Mowilex Indonesia maintained its leadership in 2025 as a supplier of USDA-certified bio-based paint removal gels, leveraging palm-derived esters to deliver VOC-free performance optimized for high humidity and temperature conditions. These formulations are increasingly specified across Southeast Asia for residential refurbishment, marine coatings removal, and heritage conservation projects where solvent emissions and worker exposure are tightly controlled.

Comparative Overview – Paint Remover Industry by Country

Paint Remover Market County Level Snapshot

|

Country

|

Primary Regulatory Driver

|

Technology Direction

|

Market Character

|

|

United States

|

EPA methylene chloride bans and exposure limits

|

Bio-based solvents, laser stripping

|

Compliance-driven reformulation

|

|

China

|

MIIT green standardization roadmap

|

Oxygenated solvents, water jet stripping

|

Policy-guided transition

|

|

Germany

|

REACH Annex XVII and VOC ceilings

|

Laser ablation, solvent recovery

|

Process innovation hub

|

|

India

|

BIS solvent standards, infrastructure growth

|

Bio-based and non-DCM removers

|

Demand-led expansion

|

|

Indonesia

|

Voluntary bio-based leadership

|

Palm-derived VOC-free gels

|

Regional sustainability benchmark

|

Paint Remover Market Report Scope

Paint Remover Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$3.1 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Product Type (Solvent-Based, Caustic-Based, Acidic-Based, Bio-Based and Green, Alternative Technologies), By Application Method (Gel and Paste, Liquid and Spray, Immersion and Dip Tank), By End-Use Industry (Construction and Renovation, Automotive, Aerospace and Defense, Marine, Furniture and Woodworking, Industrial and Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, AkzoNobel, Sherwin-Williams, Henkel, PPG Industries, Eastman Chemical, Solenis, 3M, Savogran Company, W.M. Barr & Company, Mitsubishi Chemical Group, Sunnyside Corporation, Mowilex, Green Products, Gekatex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paint Remover Market Segmentation

By Product Type

- Solvent-Based

- Caustic-Based

- Acidic-Based

- Bio-Based and Green

- Alternative Technologies

By Application Method

- Gel and Paste

- Liquid and Spray

- Immersion and Dip Tank

By End-Use Industry

- Construction and Renovation

- Automotive

- Aerospace and Defense

- Marine

- Furniture and Woodworking

- Industrial and Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Paint Remover Industry

- BASF

- AkzoNobel

- Sherwin-Williams

- Henkel

- PPG Industries

- Eastman Chemical

- Solenis

- 3M

- Savogran Company

- W.M. Barr & Company

- Mitsubishi Chemical Group

- Sunnyside Corporation

- Mowilex

- Green Products

- Gekatex

*- List not Exhaustive