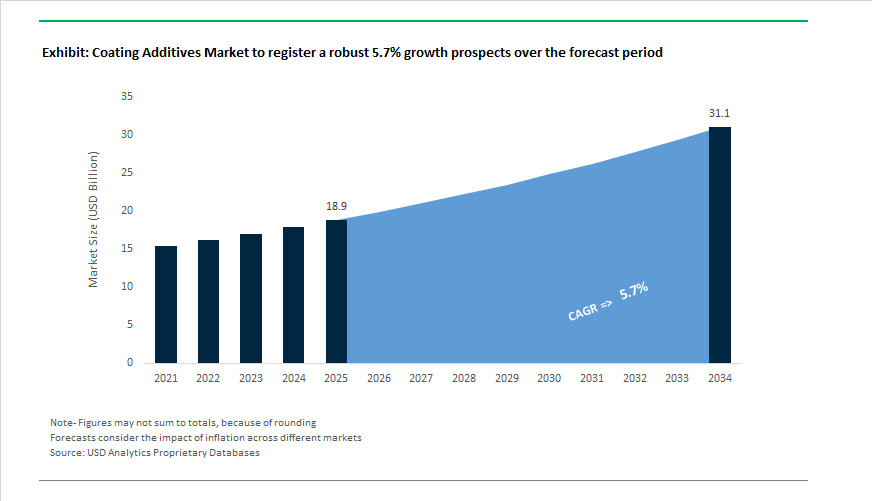

Coating Additives Market Outlook 2025–2034: $18.9 Billion to $31.1 Billion at 5.7% CAGR Fueled by Low-VOC Innovation, EV Safety, and Specialty Reformulation

The global Coating Additives Market is projected to expand from $18.9 billion in 2025 to $31.1 billion by 2034, registering a CAGR of 5.7%. Growth is anchored in rising demand for performance-enhancing additives across architectural coatings, industrial paints, automotive finishes, powder coatings, printing inks, and EV battery protection systems. Dispersants, rheology modifiers, coalescing agents, defoamers, wetting agents, texturing agents, driers, and lightweight fillers remain essential in optimizing viscosity control, film formation, pigment dispersion, scratch resistance, corrosion protection, and flame retardancy. Regulatory shifts toward low-VOC, PFAS-free, cobalt-free, and bio-attributed formulations are reshaping additive chemistry pipelines and accelerating specialty innovation.

Sustainability-driven reformulation accelerated during 2024–2026. In late 2024–2025, Clariant confirmed completion of its transition to a fully PFAS-free additives portfolio, including the launch of Ceridust 8170 M, a PTFE-free texturing agent that reduces extrusion energy consumption in powder coatings. In January 2025, Dow received the BIG Innovation Award for DALPAD™ A Plus, which reduces SVOC emissions by 60% while maintaining minimum film-forming temperature performance for waterborne industrial coatings. In April 2025, Arkema introduced Rheotech™ and Thixol™ bio-based thickeners derived from renewable feedstocks for architectural paints, strengthening rheology control without reliance on conventional petrochemical surfactants. Dow secured ISCC PLUS certification for its Freeport facility in November 2025, enabling mass-balanced sustainable intermediates for bio-attributed coating additives and resins. These actions align additive development with carbon reduction targets and tightening chemical safety regulations across North America and Europe.

Performance enhancement in advanced mobility and packaging segments is generating high-value growth corridors. In June 2024, Evonik expanded its TEGO® Therm range to address fire-resistant coatings for EV battery covers, supporting stricter lithium-ion battery safety requirements. Nouryon introduced a partially bio-based lightweight filler in December 2024, enabling lower-density coating formulations for aerospace and automotive applications, directly supporting fuel efficiency objectives. In August 2025, allnex showcased cobalt-free ADDITOL® Dry CF driers at CTT Summit 2025, addressing regulatory restrictions on cobalt in oxidative drying systems. BASF Coatings unveiled its 2025–2026 Automotive Color Trends collection in October 2025, leveraging next-generation interference pigments and specialty additives to deliver multidimensional surface effects in premium vehicle coatings. These developments illustrate how specialty coating additives are increasingly integrated into high-performance automotive, aerospace, and battery safety ecosystems.

Competitive restructuring and pricing discipline further shaped the coating additives landscape. Arkema announced in December 2025 its plan to divest its plastic additives business, refocusing its Coating Solutions segment on higher-margin specialty materials. BYK implemented a 5.2% global price increase effective February 2026, citing rising compliance costs and supply chain pressures while preserving R&D intensity. Evonik introduced TEGO® Dispers 695 in January 2026, targeting solvent-borne and radiation-curing polyurethane inks in packaging and digital printing markets, enhancing color strength and viscosity stability. In February 2026, Waters finalized its acquisition of BD’s Biosciences segment, integrating reagent and chromatography additive portfolios to deliver comprehensive analytical workflows for high-purity coating analysis and industrial quality testing. These structural, regulatory, and innovation-driven shifts position the coating additives market for sustained mid-single-digit expansion through 2034, underpinned by specialty differentiation, compliance-driven reformulation, and performance optimization across end-use industries.

Coating Additives Market Trends and Drivers

Shift Toward Reactive and Multifunctional Additives to Enable VOC Compliance and Film Durability

The regulatory tightening around air emissions and sustainability labeling—most notably following the EPA’s January 2025 National VOC Emission Standards update—is accelerating a decisive shift in how additives are engineered and selected. Traditional solvent-based additives are being replaced by reactive diluents and multifunctional additive systems that remain inside the cured coating film, eliminating risks of leaching and ensuring long-term performance durability.

In June 2025, BASF Coatings commercialized low-VOC epoxy formulations incorporating reactive curing agents, enabling benzyl-alcohol-free systems that demonstrate enhanced salt spray resistance and faster drying times. As a strategic differentiator, these non-migratory additives directly mitigate long-term degradation in adhesion and scratch resistance—two failure modes frequently observed in conventional solvent-borne coating systems.

Concurrently, the market is moving toward all-in-one multifunctional additives capable of replacing separate defoamers, wetting agents, and corrosion inhibitors. Beyond simplifying formulation, this directly lowers Product Carbon Footprint (PCF) and supports compliance pathways for IS 15489 (India), LEED-certified infrastructure, and ESG reporting metrics—transforming additive selection into a procurement-level sustainability lever.

Specialized Additives Enabling High-Performance Waterborne Industrial Coatings in Automotive and Marine

As solvent-based coatings lose regulatory acceptance, industrial segments—particularly automotive, marine, and coil-applied metal—are accelerating transition toward waterborne systems. To maintain legacy performance expectations, the industry is investing in additives that replicate flow, leveling, and early water resistance (EWR) typically achieved through solvent systems.

By mid-2025, global OEMs and CDMOs are prioritizing silicone-free defoamers and high-efficiency rheology modifiers that prevent surface pinholes and ensure high-gloss uniformity across complex metal and plastic substrates.

The advancement of Polyurethane Dispersion (PUD)-based coatings has intensified demand for additives that accelerate physical drying and enable early-rain resistance, preventing surface blistering in outdoor automotive, marine-hull, and architectural metal applications. In 2024–2025, Evonik’s R&D allocation targeted additive chemistries supporting immediate water-repellency, contributing to faster-turnaround application cycles and reducing downtime in industrial maintenance projects.

Smart Additives Delivering Self-Healing, Micro-Repair, and Sensor-Responsive Functionality

In September 2025, aerospace and drone-sector technical evaluations confirmed the commercial feasibility of extrinsic self-healing coatings, where microcapsules release embedded agents upon mechanical stress, sealing cracks before corrosion initiates. This technology has the potential to extend service-life cycles of aerospace composites, wind turbine blades, and military-grade equipment, fundamentally repositioning coatings as asset-protection systems, not consumables.

Simultaneously, biocide-free anti-fouling additive platforms are gaining traction, particularly in marine shipping fleets. Stimuli-responsive polymers—capable of dynamically altering surface energy based on pH or salinity—prevent barnacle and algae attachment without the ecotoxicity associated with copper or heavy-metal systems. With the IMO sustainability agenda pressuring ship operators to reduce ecological impact, this category represents a premium-margin pathway for coating formulators.

Additives Enabling Circular Materials and Stable Bio-Based Resin Adoption

As global resin markets transition from fossil-derived feedstocks toward recycled and lignin-based bio-resins, additives increasingly determine whether these materials are scalable for industrial use.

The EU-funded LIGNICOAT (April 2025) demonstrated that modifying lignin-based resin systems with bio-derived additive molecules such as hop extractives and thymol can achieve corrosion and microbial resistance comparable to traditional epoxy coatings—bridging a crucial performance gap that has slowed bio-resin adoption.

In parallel, innovation in post-consumer recycled (PCR) resin compatibilization is accelerating. In October 2025, Braskem’s bio-based polyethylene + MDO technology was unveiled, signaling that premium rigid-packaging will increasingly rely on additive packages that restore stiffness, optical clarity, and crack resistance to recycled polymers.

This represents a massive growth avenue: additives are becoming the upcycling enablers that transform waste-stream plastics into premium-grade inputs, directly impacting Scope-3 reduction metrics for brand owners.

Coating Additives Market Share and Segmentation Insights

Type-Based Segmentation: Rheology Modifiers Lead as Specialty Additives Drive Coating Durability

Rheology modifiers account for 28% of coating additives market share in 2025, reflecting their critical role in controlling viscosity, flow, leveling, and sag resistance across architectural and industrial coatings. These additives directly influence application behavior, determining roller spread, spray uniformity, and vertical stability. Dispersing and wetting agents form a major supporting segment, ensuring pigment stabilization, color consistency, gloss development, and hiding power by preventing agglomeration. Defoamers and deaerators contribute significantly by eliminating entrapped air during manufacturing and application, preventing surface defects such as craters and fisheyes. Specialty additives, including biocides, fungicides, UV stabilizers, light absorbers, and anti-corrosive agents, collectively represent over a quarter of total demand, highlighting the industry’s focus on long-term performance. Impact modifiers and slip additives further enhance scratch resistance and surface feel, reinforcing the shift toward high-durability, premium coating formulations across construction, automotive, and industrial markets.

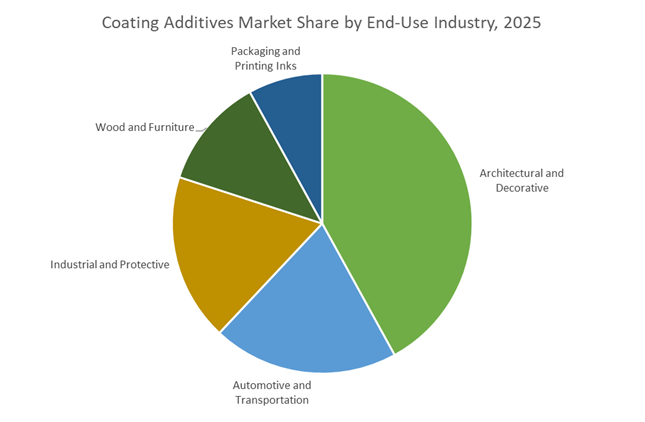

End-Use Industry Distribution: Architectural Coatings Anchor Demand as Automotive and Industrial Performance Accelerates

Architectural and decorative coatings dominate consumption with 42% market share, driven by large-scale residential and commercial construction activity and renovation cycles. Rheology modifiers and biocides are especially vital in this segment, supporting easy application and mold resistance on interior and exterior walls. Automotive and transportation coatings represent a high-value segment, requiring advanced additive packages including UV stabilizers, impact modifiers, and precision rheology control to achieve showroom-quality finishes and resistance to road debris. Industrial and protective coatings rely heavily on anti-corrosive additives and high-performance dispersants to safeguard infrastructure, pipelines, and heavy equipment against chemical and environmental exposure. Wood and furniture applications emphasize grain enhancement, scratch resistance, and slip control, while packaging and printing inks depend on defoamers and wetting agents for high-speed printability and adhesion. Together, these end-use industries sustain diversified growth across global coating additive supply chains.

Competitive Landscape of the Coating Additives Market

The Coating Additives Market is driven by global specialty chemical leaders advancing rheology modifiers, wetting agents, dispersants, coalescing agents, and flame retardant systems for architectural, automotive, industrial, and energy applications. Competitive differentiation centers on PFAS-free formulations, bio-based additives, Zero Product Carbon Footprint strategies, and AI-enabled formulation tools. Market leaders are accelerating digitalization, circular economy integration, and waterborne coating innovation to meet tightening REACH, FDA, and global indoor air quality regulations. Strategic expansion in Asia-Pacific and mobility-driven segments such as EV battery protection and composite coatings continues to reshape competitive positioning.

BASF advances ZeroPCF coating additives through Verbund integration and digital simulation

BASF remains the dominant force in the global coating additives market, leveraging its Verbund integrated production model to deliver high-performance stabilizers and pigments. In late 2025, BASF introduced its 2025–2026 Automotive Color Trends collection, “Driving the Proxy,” featuring sustainable interference pigments such as Tesseract Blue made from bio-based and recycled raw materials. Under its Winning Ways strategy, BASF is transitioning its additives portfolio toward ZeroPCF products using biomass balance and renewable energy. The company expanded capacity in Mangalore, India in early 2026 to meet rising waterborne architectural demand, while integrating digital simulation tools to allow OEMs to virtually model additive performance before production.

Evonik strengthens bio-based wetting and dispersion technologies under TEGO brand

Evonik is a high-margin additive specialist recognized globally for its TEGO® portfolio of defoamers, wetting agents, and dispersants. In January 2026, the company launched TEGO® Dispers 695, a hyperdispersant engineered for radiation-curing and solvent-borne polyurethane inks. It previously introduced the TEGO® Wet 570 and 580 Terra series, 100% bio-based surfactants designed to replace fossil-derived wetting agents. Effective May 1, 2026, Evonik streamlined its North American distribution network, appointing exclusive partners to strengthen supply security and technical support. Its core expertise in surface tension control makes Evonik a preferred supplier for plastics, recycled composites, and difficult-to-coat substrates.

BYK leads PFAS-free rheology innovation and digital specialty chemical distribution

BYK, part of ALTANA Group, is among the most innovation-driven players in coating additives, reinvesting heavily into R&D for both additives and measuring instruments. The company committed to eliminating all PFAS-containing additives by the end of 2025, transitioning to PFAS-free firefighting foams and PTFE-free wax coatings by 2026. In late 2025, BYK launched BYK-MAX P 4110, a PFAS-free polymer processing aid that increases production speeds and reduces clean-out time. Beginning January 1, 2026, BYK expanded partnerships across Poland, Finland, and the Baltic region, strengthening digitized specialty chemical distribution. It maintains industry leadership in rheology control and anti-sag thickeners.

Dow drives low-VOC architectural growth with AI-enabled performance additives

Dow leverages material science scale to lead high-volume architectural and industrial coatings. In early 2026, it launched the Transform to Outperform initiative targeting a USD 2 billion EBITDA uplift by 2028 through AI-driven analytics and digital simplification. Its DALPAD™ A PLUS coalescing agent remains a benchmark for low-VOC paints meeting strict European indoor air quality standards. Dow is also advancing Cool Roof technologies, supplying additives that enhance infrared reflectance and urban energy efficiency. Recent innovation includes freeze-thaw stabilizers enabling waterborne coatings to maintain viscosity stability during transport and storage in extreme climates.

Clariant expands bio-based wax additives with Safe-by-Design regulatory leadership

Clariant focuses on sustainable specialty additives, combining fire safety and renewable wax technologies. Its Exolit™ halogen-free flame retardants and AddWorks™ optimized additive combinations address industrial and packaging performance needs. In 2026, Clariant showcased Licocare® RBW Vita additives derived from renewable rice bran wax, functioning as high-efficiency lubricants and dispersing agents. The company emphasizes Safe-by-Design chemistry, ensuring compliance with tightening REACH and FDA food-contact regulations. It is also expanding CLARITY™ Prime digital services in China, providing real-time performance analytics and batch consistency data to coating manufacturers.

Arkema pioneers bio-based thickeners and recyclable composite coating solutions

Arkema is a leader in circular and bio-sourced coating additives, particularly rheology modifiers and advanced crosslinking systems. In early 2026, Arkema launched bio-based acrylic thickeners under the Rheotech™, Thixol™, and Viscoatex™ brands using bio-sourced ethyl acrylate from its Carling, France site. The company dominates composite coatings, with Elium® recyclable resins and Rilsan® Polyamide 11 additives supporting hydrogen tanks and next-generation aerospace components. Arkema’s core strength lies in rheology and thermal-activation crosslinking technologies, enabling coatings that can be disassembled at end-of-life. Strategically, Arkema targets green energy and mobility sectors including EV battery housing protection and wind turbine blade durability.

United States: Low-SVOC Reformulation and AI-Accelerated Additive Development

The United States coating additives industry in 2025–2026 is defined by a rapid convergence of regulatory compliance, green chemistry innovation, and data-driven formulation science. A major signal of technological direction came in early 2025 when Dow received the Gold Edison Award for its TRITON FCX surfactants, a patented biodegradable and toxin-free alternative to fluoro-containing materials. These surfactants are gaining traction in architectural paints due to their ability to deliver superior block resistance without relying on persistent chemistries, aligning with growing restrictions on fluorinated substances. This sustainability momentum continued with Dow’s 2025 launch of DALPAD A Plus, a low-SVOC coalescing agent that achieves a 60% reduction in semi-volatile organic compounds while enhancing low-temperature crack resistance in waterborne coatings.

R&D productivity and regulatory timelines are also reshaping competitive strategies. In 2025, Dow introduced the Integrated Research Imaging Solution, an AI-powered assessment platform that converts subjective coating attributes such as smoothness and visual appeal into quantitative metrics. This system has reduced additive testing cycles by an estimated 40 %, accelerating time-to-market for next-generation coating additives. On the policy front, the U.S. Environmental Protection Agency issued an interim final rule in June 2025 extending compliance deadlines for National VOC Emission Standards to January 17, 2027. This two-year reformulation window is driving proactive substitution of legacy additives across aerosol and industrial coatings. Demand-side innovation is equally active. BASF Coatings unveiled its Driving the Proxy collection for 2025–2026, featuring sparkle-enhanced additive technologies such as Auxetic Neutral that merge fashion-led aesthetics with industrial durability. Additionally, the launch of DOWSIL 650+ introduced a waterborne, peelable acrylic additive formulated without alkylphenol ethoxylates, targeting temporary protection for high-value facade glazing and reinforcing the U.S. focus on functional, regulation-ready coating additives.

Germany: PFAS Exit, Digital Coating Lines, and Bio-Based Acceleration

Germany represents one of the most regulation-intensive and innovation-forward markets for coating additives, with 2025 marking a decisive shift toward PFAS-free, bio-based, and digitally optimized formulations. Early in 2025, Clariant completed its transition to a fully PFAS-free additive portfolio. Products such as Ceridust 8170 M now eliminate PTFE while reducing energy consumption during powder coating extrusion, directly addressing both substance restrictions and process efficiency goals. This transition is reinforced by national green chemistry mandates, under which bio-based powder coating additives are expected to grow significantly faster than conventional alternatives through 2026, reflecting strong downstream pull from architectural and industrial users.

Manufacturing digitization is amplifying additive performance requirements. By late 2025, more than half of German industrial coatings were applied using automated, IoT-enabled systems, forcing formulators to develop additives with highly consistent and digitally predictable rheological behavior. This environment has stimulated coordinated sustainability efforts across the value chain. In late 2025, BASF, AkzoNobel, and Arkema formed a strategic alliance to produce superdurable architectural powder coatings with substantially lower carbon footprints using bio-attributed resins and additives. Regulatory pressure continues to intensify. Commission Regulation (EU) 2025/1090 added DMAC and NEP to the restricted substances list, imposing concentration limits below 0.3% by December 2026. In response, German chemical firms reported significant 2025 investments in Industry 4.0-oriented additive R&D, specifically targeting automated, high-speed coating lines that demand both regulatory compliance and process stability.

China: Localization of High-Performance Additives and Nano-Enabled Differentiation

China’s coating additives industry is evolving rapidly under the dual influence of industrial policy liberalization and targeted environmental mandates. In November 2025, BASF commissioned a high-performance dispersant production line at the Jiangbei New Material Technology Park in Nanjing. Utilizing Controlled Free Radical Polymerization technology, the facility supports the green transformation of automotive and industrial coatings by enabling dispersants and additives with lower carbon footprints and higher formulation precision. The designation of Jiangbei as a specialty chemicals hub has strengthened regional supply chains and reduced reliance on imported high-end additives.

Policy adjustments in 2025 have further reshaped market dynamics. The Chinese government removed mandatory testing requirements for certain imported paints and coatings, accelerating the entry of specialized international additives and intensifying competitive pressure on domestic suppliers. At the same time, the Ministry of Industry and Information Technology issued guidelines emphasizing nano-additives to improve scratch resistance and UV stability in electronics and automotive coatings. Aesthetic innovation is also gaining prominence. BASF Asia Pacific introduced Phygital Magnetar, a warm metallic additive shade based on two-coat technology that integrates physical and digital surface effects. Environmental policy remains a strong driver. A 2025 mandate to gradually eliminate lead from industrial paints has triggered widespread substitution with organic anti-corrosive additives and metallic-free driers. In parallel, AkzoNobel expanded its marine coatings partnership in China to focus on bio-fouling control additives, aligning coating performance with sustainable shipping objectives.

India: Infrastructure-Led Demand and Nano-Additive Industrialization

India’s coating additives market is scaling rapidly due to infrastructure expansion, automotive production growth, and targeted government support for specialty chemicals. The Production Linked Incentive scheme reached peak disbursement in 2025, with a strong focus on reducing import dependence for advanced rheology modifiers, epoxy additives, and performance enhancers used in industrial and architectural coatings. This policy backdrop has accelerated domestic capacity creation. In 2025, Pellucere Technologies commissioned a nanoparticle manufacturing facility in Maharashtra with significant annual capacity dedicated to nano-coatings for solar panels and automotive glass, signaling India’s entry into high-value nano-additive production.

End-use demand fundamentals are equally strong. Hempel India launched its Avantguard solution in 2025, engineered for infrastructure assets exposed to high-corrosivity environments and reliant on advanced zinc-activator additives. Automotive manufacturing remains a powerful growth engine. With vehicle production exceeding 30 million units in the 2024–25 fiscal year, demand for multifunctional coating additives that extend shelf life and enhance durability has reached unprecedented levels. Industrial usage milestones further underline scale. Annual industrial coating consumption in India reached approximately two million tons in 2025, driving high-volume procurement of wetting agents, dispersants, and process-efficient additives. Collectively, these trends position India as both a fast-growing consumption market and an emerging manufacturing base for advanced coating additives.

Comparative Snapshot: Country-Level Strategic Direction in the Coating Additives Industry

Coating Additives Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Industrial Focus

|

Direction of Additive Innovation

|

|

United States

|

VOC reformulation and AI-enabled R&D

|

Architectural, automotive, protective coatings

|

Low-SVOC, biodegradable, data-validated additives

|

|

Germany

|

PFAS elimination and automated coating lines

|

Powder and architectural coatings

|

Bio-based, digital-ready, REACH-compliant additives

|

|

China

|

Localization and nano-technology adoption

|

Automotive, electronics, marine coatings

|

Nano-enhanced, low-carbon, metallic-free additives

|

|

India

|

Infrastructure stimulus and automotive growth

|

Industrial and architectural coatings

|

Nano-additives, corrosion-resistant, high-throughput agents

|

Coating Additives Market Report Scope

Coating Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.9 Billion

|

|

Market Size (2034)

|

$31.1 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Rheology Modifiers, Dispersing and Wetting Agents, Defoamers and Deaerators, Impact Modifiers and Slip Additives, Anti-corrosive Additives, Biocides and Fungicides, UV Stabilizers and Light Absorbers), By Formulation (Water-borne Additives, Solvent-borne Additives, Powder-based Additives, Radiation-curable Additives), By Functionality (Surface Processing Additives, Rheological Control Additives, Environmental and Regulatory Compliance Additives, Functional Coating Additives), By End-Use Industry (Architectural and Decorative, Automotive and Transportation, Industrial and Protective, Wood and Furniture, Packaging and Printing Inks)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, BYK-Chemie GmbH, Dow Inc., Akzo Nobel N.V., Arkema S.A., Clariant AG, Eastman Chemical Company, Elementis Plc, Lubrizol Corporation, Allnex GmbH, PPG Industries, Inc., Cabot Corporation, Solvay S.A., Hempel A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coating Additives Market Segmentation

By Type

- Rheology Modifiers

- Dispersing and Wetting Agents

- Defoamers and Deaerators

- Impact Modifiers and Slip Additives

- Anti-corrosive Additives

- Biocides and Fungicides

- UV Stabilizers and Light Absorbers

By Formulation

- Water-borne Additives

- Solvent-borne Additives

- Powder-based Additives

- Radiation-curable Additives

By Functionality

- Surface Processing Additives

- Rheological Control Additives

- Environmental and Regulatory Compliance Additives

- Functional Coating Additives

By End-Use Industry

- Architectural and Decorative

- Automotive and Transportation

- Industrial and Protective

- Wood and Furniture

- Packaging and Printing Inks

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Coating Additives Industry

- BASF SE

- Evonik Industries AG

- BYK-Chemie GmbH

- Dow Inc.

- Akzo Nobel N.V.

- Arkema S.A.

- Clariant AG

- Eastman Chemical Company

- Elementis Plc

- Lubrizol Corporation

- Allnex GmbH

- PPG Industries, Inc.

- Cabot Corporation

- Solvay S.A.

- Hempel A/S

*- List not Exhaustive