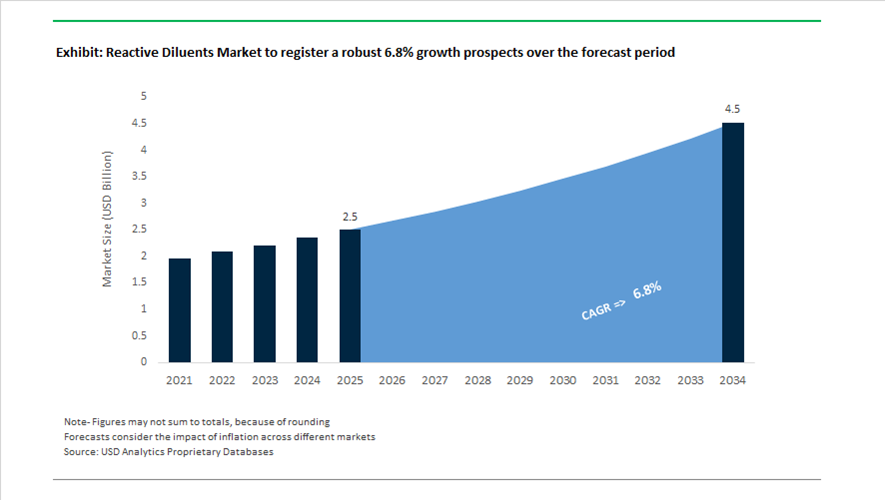

Reactive Diluents Market Valued at $2.5 Billion in 2025, Projected to Reach $4.5 Billion by 2034 at 6.8% CAGR

The global reactive diluents market is valued at $2.5 billion in 2025 and is projected to reach $4.5 billion by 2034, registering a CAGR of 6.8%. Growth is driven by rising demand for epoxy reactive diluents, aliphatic and aromatic glycidyl ethers, low-viscosity resin modifiers, UV-curable diluents, bio-based epoxy diluents, and composite-grade reactive systems used in marine coatings, wind turbine blades, EV battery encapsulation, industrial flooring, and structural adhesives. Increasing pressure to reduce VOC emissions while maintaining mechanical performance has accelerated adoption of high-functionality diluents that chemically integrate into cured resin matrices rather than volatilizing during application.

Capacity expansion and strategic acquisitions reshaped the competitive landscape in 2024. In early 2024, LG Chem expanded its epoxy resin and specialty reactive diluent production lines in South Korea to support EV and electronics sector growth, where high-performance composite materials require controlled viscosity and enhanced crosslink density. During the same period, Hexion upgraded its Ohio manufacturing facility to increase specialty reactive diluent output, targeting wind energy composites and lightweight automotive adhesives. Huntsman achieved REDcert2 certification at its Monthey, Switzerland site in 2024, enabling mass-balance production of bio-attributed epoxy resins and diluents to support circular economy mandates.

Market consolidation intensified through 2025 and into 2026. In June 2025, Aditya Birla Chemicals completed the acquisition of Cargill’s specialty chemical business in Dalton, Georgia, establishing a direct manufacturing footprint in the U.S. for reactive diluents, formulated resins, and curing agents serving marine and industrial coatings. By late 2025, Aditya Birla announced plans to double capacity at the Dalton site within two years to strengthen its North American advanced materials portfolio. In February 2025, Arxada introduced Polyboost™, a multifunctional additive incorporating reactive and quaternary chemistry to enhance antimicrobial durability in industrial coatings. At the European Coatings Show 2025, LANXESS launched Klarix XIT, a non-biocidal additive designed to integrate into reactive coating systems, enabling hygiene-focused formulations without conventional biocides. Throughout 2025, Evonik implemented its Tailor Made reorganization program, streamlining its Coating & Adhesive Resins division to prioritize high-growth segments such as liquid polybutadienes and specialty acrylic reactive systems while divesting non-core polyester lines. Olin Corporation accelerated its Beyond250 initiative in late 2025 and 2026, restructuring its epoxy segment to optimize supply rationalization and improve profitability across Europe and North America.

Downstream integration continued in January 2026 when Applied Adhesives acquired Interlock Adhesives, expanding formulation capabilities that utilize advanced reactive diluents for structural bonding and industrial assembly applications. The reactive diluents market is increasingly characterized by low-VOC epoxy modifiers, bio-attributed glycidyl ethers, composite-grade viscosity reducers, UV-curable acrylate diluents, EV battery encapsulation resins, marine and wind energy coating systems, and circular mass-balance certified production strategies. As electrification, renewable infrastructure, and industrial coating performance standards rise, reactive diluent innovation remains central to balancing processing efficiency, environmental compliance, and structural durability.

Strategic Trends and Growth Opportunities in the Reactive Diluents Market

Accelerated Regulatory Shift Toward Bio-Based and Low-VOC Reactive Diluent Systems

The reactive diluents market is undergoing a structural reset as regulatory pressure transitions from disclosure-based compliance to formulation-level enforcement. What was previously positioned as an ESG-driven preference has now become a non-negotiable requirement across coatings, composites, and adhesives. The European Commission’s Decision 2025/2607, finalized in December 2025, fundamentally reshaped Ecolabel criteria by imposing stricter limits on air and water emissions during application, directly impacting solvent-heavy and toxic diluent chemistries.

A critical inflection point occurred in 2024 when several widely used epoxy reactive diluents were reclassified under the EU’s H360F hazard category for reproductive toxicity. This reclassification immediately rendered many incumbent diluents commercially unviable for civil engineering, flooring, and industrial coatings. In response, the market has seen rapid adoption of next-generation, non-H360F “drop-in” epoxy diluents engineered to preserve viscosity reduction without triggering regulatory flags. New formulations are increasingly based on bio-renewable epoxides and modified aliphatic backbones that integrate fully into the polymer network rather than volatilizing during cure.

Regulatory momentum is not limited to Europe. In the United States, the EPA’s updated National VOC Emission Standards for Aerosol Coatings, which came into effect on January 6, 2025, introduced tighter ozone reactivity factors and effectively penalized evaporative diluents. This has accelerated the shift toward high-solids and solvent-free systems where reactive diluents function as permanent structural components of the cured matrix. As a result, demand growth is increasingly concentrated in low-VOC, bio-based reactive diluents that offer regulatory durability across multiple jurisdictions, making compliance predictability a core purchasing criterion for formulators.

Multi-Functional Reactive Diluents as Structural Co-Monomers in Advanced Composites

Reactive diluents are no longer treated as viscosity modifiers alone; they are being engineered as load-bearing co-monomers that directly influence mechanical performance, durability, and recyclability. This functional upgrade is most visible in high-growth composite applications across renewable energy, automotive lightweighting, and industrial infrastructure.

In wind energy, the validation of liquid reactive thermoplastic resin systems during 2024–2025 marked a major turning point. These systems rely on specialized reactive diluents to enable thermal welding, re-melting, and full recyclability of large composite structures such as 13-meter wind turbine blades. Performance testing demonstrated significantly higher structural damping, extending fatigue life and reducing maintenance cycles, which directly improves lifetime energy yield per turbine. This has positioned reactive diluents as enablers of circular composite architectures rather than auxiliary additives.

Simultaneously, the automotive and industrial repair sectors are driving demand for multi-functional, aliphatic reactive diluents with more than two reactive groups per molecule. These chemistries allow rapid curing at ambient or low temperatures while maintaining high crosslink density, a critical requirement for on-site infrastructure repair and fast-cycle composite molding. The market is therefore shifting toward reactive diluents that deliver simultaneous benefits in processability, cure kinetics, mechanical strength, and long-term durability, raising the technical and value threshold for supplier participation.

High-Solid and Solvent-Free Reactive Diluent Solutions for Marine and Infrastructure Coatings

The convergence of solvent restrictions, PFAS phase-outs, and large-scale infrastructure spending has created a high-impact opportunity for reactive diluents that enable 100% solids coatings. Marine, bridge, pipeline, and heavy industrial maintenance applications increasingly require thick-film, single-coat systems that can be applied with minimal VOC emissions while delivering long-term corrosion protection.

Global infrastructure investment is acting as a powerful demand multiplier. For the 2025–26 fiscal year, large economies significantly increased capital allocation for transportation and urban infrastructure, intensifying demand for protective coatings that reduce labor hours and lifecycle maintenance costs. Reactive diluent-enhanced high-solids epoxy systems allow applicators to achieve required film builds in fewer passes, directly lowering labor exposure, VOC taxes, and downtime. In marine environments, the same chemistry enables compliance with tightening REACH restrictions while maintaining resistance to saltwater ingress, mechanical abrasion, and biofouling.

From a supplier perspective, this opportunity favors reactive diluents with exceptional compatibility across epoxy, polyurethane, and hybrid resin systems. Products that balance ultra-low viscosity with strong network integration are increasingly specified as critical formulation components rather than optional modifiers, supporting premium pricing and long-term supply contracts.

Industrial 3D Printing and UV-Curable Resin Platforms as a Specialty Growth Engine

The industrialization of additive manufacturing using vat photopolymerization technologies is opening a structurally attractive niche for specialty reactive diluents. As SLA and DLP platforms move beyond prototyping into serial production of end-use components, resin performance requirements are becoming significantly more demanding.

Reactive diluents play a central role in controlling resin viscosity for recoating speed, cure depth, and dimensional accuracy. In 2025, demand is accelerating for acrylate and vinyl ether diluents that minimize shrinkage stress while maintaining high glass transition temperatures, enabling printed parts suitable for aerospace tooling, dental prosthetics, and functional industrial components. These applications demand a precise balance between flow, cure speed, and mechanical stability, positioning reactive diluents as performance-critical ingredients.

A further layer of opportunity is emerging through AI-enabled formulation platforms. Leading producers are deploying data-driven tools to design application-specific reactive diluent blends optimized for photoinitiator compatibility and UV absorption profiles. This capability is reducing development cycles for digital printing inks and high-speed UV-curable coatings, allowing suppliers to embed themselves deeper into customer innovation pipelines and secure long-term differentiation in a rapidly scaling market.

Reactive Diluents Market Share and Segmentation Insights

Aliphatic Reactive Diluents Dominate the Reactive Diluents Market Driven by Low-VOC Epoxy and Coating Formulations

Aliphatic reactive diluents accounted for 42.80% of the reactive diluents market in 2025, establishing them as the leading product category across epoxy resin systems. Their dominance is linked to superior weatherability, low viscosity reduction capability, and high reactivity, making them widely used in paints and coatings, adhesives, and composite formulations. These diluents enhance flexibility, impact resistance, and durability while maintaining the structural performance of cured epoxy networks. A major market catalyst in 2025 is the growing transition toward low-VOC and high-solids coating technologies, where aliphatic reactive diluents replace solvent-based diluents. Because these reactive monomers chemically integrate into the cured film, manufacturers achieve reduced VOC emissions while maintaining coating application viscosity and long-term durability.

Paints & Coatings Lead Application Demand as High-Solids Industrial Coatings Expand

Paints and coatings emerged as the largest application segment in the reactive diluents market, capturing 52.80% share in 2025 due to strong demand for epoxy-based industrial and protective coatings. Reactive diluents play a critical role in high-solids and solvent-free coating formulations, enabling viscosity reduction without introducing VOC-emitting solvents. Consumption is particularly high in industrial maintenance coatings, marine coatings, architectural coatings, tank linings, pipe coatings, and structural steel protection systems. The key 2025 growth driver is the adoption of high-solids industrial coatings designed to meet tightening environmental regulations. By enabling solvent-free or low-VOC formulations, reactive diluents allow coating manufacturers to deliver durable corrosion protection, chemical resistance, and regulatory-compliant coating performance across infrastructure and heavy industry applications.

Reactive Diluents Market Competitive Landscape

The 2026 reactive diluents market is transitioning toward non-toxic, bio-based monomers, low-viscosity glycidyl ethers, and low-VOC epoxy systems. Growth is driven by regulatory pressure under REACH and TSCA, alongside rising demand in UV-curable resins, automotive composites, and solvent-free coatings.

Huntsman advances high-performance epoxy diluents with sustainable ARALDITE innovation and global supply integration

Huntsman Corporation is strengthening its leadership in reactive diluents through advanced epoxy systems tailored for automotive and aerospace applications. The launch of ARALDITE® adhesives and specialized diluents focuses on reducing hazardous emissions and improving curing efficiency. The company reported approximately $6 billion in 2025 revenue, with strategic emphasis on expanding its Specialty Chemicals segment in 2026. Core offerings include JEFFAMINE® polyetheramines and high-purity reactive diluents used in wind energy composites and infrastructure coatings. Integrated operations across 25 countries ensure stable supply of mono- and di-functional glycidyl ethers amid logistics volatility. Focus on performance materials supports demand in high-durability and lightweight composite applications.

Evonik expands specialty diluent capacity with phenol-free formulations and advanced additives integration

Evonik Industries AG is advancing its reactive diluents portfolio through capacity expansion and development of environmentally compliant additives. The company reported €1.87 billion EBITDA in 2025 and maintains a strong outlook for specialty coatings and resin modifiers. Expansion of HTPB production in China and upcoming capacity in Germany support growth in advanced applications. Ancamine® and Ancamide® product lines eliminate phenol-based hazardous substances, aligning with evolving environmental standards. Establishment of new Asian production infrastructure enhances supply proximity to electronics and EV sectors. Focus on specialty additives strengthens positioning in high-performance coatings and advanced material systems.

Olin strengthens cost competitiveness in reactive diluents through epoxy integration and structural realignment

Olin Corporation is optimizing its reactive diluents business through integrated epoxy production and cost reduction initiatives. Closure of its Brazil facility under the Beyond250 program is expected to deliver $10 million in annual savings while consolidating supply chains. The company is targeting a return to profitability in 2026 supported by improved volumes in the U.S. and Europe and new supply agreements in Germany. Internal production of epichlorohydrin provides a cost advantage in manufacturing glycidyl ether-based diluents. Epoxy segment sales reached $359.3 million in Q4 2025, driven by higher volumes and improved product mix. Focus on industrial and marine coatings enhances demand for high-performance diluents.

Aditya Birla Chemicals expands bio-based and recyclable diluents portfolio with major North America capacity build-out

Aditya Birla Chemicals is scaling its presence in the reactive diluents market through acquisitions and expansion of advanced materials capacity. The Dalton, Georgia facility acquisition is being expanded from 16,000 to over 40,000 tons per year, strengthening its North American footprint. The Epotec® portfolio includes mono-, di-, and tri-functional glycidyl ethers designed for low viscosity and improved flexibility in coatings and flooring. Briozen bio-based products and Recyclamine technology support recyclability of epoxy thermosets, targeting wind energy and sports applications. Localized production enables delivery of low-VOC solutions tailored to U.S. construction and packaging markets. Integration of sustainable materials supports compliance with global environmental regulations.

Cardolite leads bio-based reactive diluents innovation with CNSL-derived products and label-friendly formulations

Cardolite Corporation is driving sustainable innovation in reactive diluents through its proprietary cashew nutshell liquid (CNSL) technology. The launch of Ultra LITE 513 introduces a 100% bio-based, light-color monofunctional diluent designed for high-purity applications. Expansion of the NX-202X series supports polyurethane systems with solvent-free viscosity reduction and improved durability. CNSL-based diluents offer up to 30% bio-based content in formulations, reducing reliance on petroleum-derived glycidyl ethers. Strong R&D investments are focused on nonylphenol-free and low-VOC resin modifiers. Portfolio strength in green chemistry supports adoption in coatings, adhesives, and composite materials.

Kukdo Chemical strengthens electronics-grade diluents supply with integrated epoxy systems and APAC capacity expansion

Kukdo Chemical Co., Ltd. is enhancing its reactive diluents portfolio through high-purity, low-chlorine formulations targeting electronics and advanced coatings markets. Strategic focus includes semiconductor laminating adhesives and electric insulation materials requiring low ionic content. Integrated product offerings enable customers to source both epoxy resins and customized diluents from a single supplier. Expansion of the YEOJU and Kunshan facilities supports growing demand in renewable energy and wind turbine manufacturing. Strong presence in marine and construction coatings highlights the role of diluents in improving flexibility and processability. Emphasis on high-performance and electronics-grade materials supports growth in precision applications.

United States: Capacity Consolidation, Additive Manufacturing, and EV-Driven Formulation Shifts

The United States reactive diluents industry is entering a phase of structural expansion driven by acquisitions, advanced materials investment, and downstream demand from construction, additive manufacturing, and electric vehicles. In June 2025, Aditya Birla Chemicals USA, part of the Aditya Birla Group, acquired Cargill’s specialty chemical facility in Dalton, Georgia. The site, focused on reactive diluents and formulated resins, is scheduled for a scale-up from 16,000 tonnes to more than 40,000 tonnes within two years, materially strengthening domestic supply of viscosity-modifying diluents for epoxy and composite systems. This acquisition is complemented by Aditya Birla’s $50 million investment in an advanced materials facility in Beaumont, Texas during 2024–2025, with a clear focus on aerospace- and renewable-energy-grade epoxy systems where low-volatility, high-reactivity diluents are critical for mechanical performance.

Downstream pull remains strong. Henkel USA completed a $35 million expansion of its North Carolina additive manufacturing hub across 2024–2025, significantly increasing output of UV-curable and 3D-printing resins that rely on specialized reactive diluents for viscosity control and cure-speed tuning. On the feedstock side, Olin Corporation commissioned a 15-ton-per-day hydrogen liquefaction unit in Louisiana in April 2025 through a joint venture, improving the sustainability profile of nitrogen-based chemical intermediates used upstream in epoxy value chains. With U.S. construction spending reaching $2.1 trillion in 2024, demand for high-performance reactive diluents in architectural and protective coatings is expected to remain resilient through 2026. At the same time, the shift toward electric vehicles has driven a 22% increase in adoption of trifunctional reactive diluents for battery potting compounds and thermally stable composite components by late 2025.

China: Policy-Led Shift Toward High-End Supply and AI-Optimized Dosing

China’s reactive diluents market is being reshaped by industrial policy that prioritizes value-added specialty chemicals over bulk refining. In September 2025, the Ministry of Industry and Information Technology issued the Work Plan for Stabilizing Growth (2025–2026), targeting a 5% annual increase in petrochemical added value while explicitly favoring high-end electronic and fine chemicals. The plan imposes strict limits on new refining capacity, accelerating the transition toward refining-to-chemicals conversions that structurally favor specialty intermediates such as reactive diluents used in coatings, electronics encapsulation, and advanced adhesives.

Technology deployment is a central differentiator. Under the national “AI plus petrochemicals” initiative launched in late 2025, large Chinese producers are integrating artificial intelligence into formulation and process control to reduce VOC emissions and optimize reactive diluent dosage in real time. This has direct implications for large-scale coatings and adhesive production, where overuse of diluents is both a regulatory and cost liability. With China’s electronics manufacturing output exceeding $520 billion, demand for cycloaliphatic and specialty diluents for PCB encapsulation and semiconductor packaging grew by 12% year on year by the third quarter of 2025. Looking ahead, the introduction of a Green Chemical Product Certification system in 2026 is incentivizing the development of bio-based reactive diluents derived from non-grain feedstocks, aligning environmental compliance with industrial competitiveness.

Germany and the European Union: Regulatory Redesign and Renewable Energy Pull

In Germany and across the European Union, the reactive diluents industry is increasingly defined by regulatory redesign and energy-transition-driven demand. In September 2025, Huntsman Corporation launched a newly reformulated ARALDITE epoxy adhesive range in Europe that is fully free from CMR substances and intentionally added BPA. This product strategy directly anticipates the 2026 CLP and REACH requirements, which are tightening scrutiny on reactive diluent blends used in professional and industrial applications. The ongoing REACH Revision, expected to be finalized in late 2025, introduces a Mixture Assessment Factor and digital safety data sheets, fundamentally changing how multi-component reactive diluent systems are assessed, documented, and marketed.

Sustainability and energy infrastructure provide additional momentum. Huntsman’s introduction of post-consumer recycled plastic cartridges for its European epoxy portfolio in 2025 reduced packaging-related CO₂ emissions by up to 36%, reinforcing the importance of lifecycle transparency alongside formulation chemistry. Demand from renewable energy applications is accelerating, particularly in wind turbine blade composites. With the EU targeting an estimated 8.4% compound annual growth rate in wind installations through 2026, epoxy systems with high-durability reactive diluents are becoming essential for large-scale composite manufacturing, anchoring long-term demand beyond traditional construction coatings.

South Korea: Export-Oriented Electronics and Automotive Composites

South Korea’s reactive diluents market is closely linked to its role as a global manufacturing and export hub for electronics and automobiles. LG Chem completed expansions of its high-performance epoxy resin and reactive diluent lines during 2024–2025, strengthening supply for lightweight composite applications used in automotive exports. These expansions reflect a broader industry shift toward materials that balance mechanical strength, thermal stability, and low VOC emissions.

Electronics manufacturing remains a critical demand driver. With total electronic equipment production valued at approximately $340 billion, South Korean producers such as Kukdo Chemical expanded eco-friendly reactive diluent product lines in 2025 to comply with tightening VOC and sustainability standards in Western export markets. This export-facing regulatory pressure is accelerating innovation in low-emission and bio-modified diluents, positioning South Korea as a supplier of compliant, high-performance materials for global OEMs.

Comparative Snapshot: Reactive Diluents Industry by Country

Reactive Diluents Market County Level Snapshot

|

Country / Region

|

Structural Driver

|

Impact on Reactive Diluents

|

|

United States

|

Acquisitions, construction spending, EV adoption

|

Capacity expansion, trifunctional diluents, additive manufacturing resins

|

|

China

|

Industrial policy and AI integration

|

High-end specialty diluents, optimized VOC-compliant dosing

|

|

Germany / EU

|

REACH and CLP revisions, renewable energy growth

|

CMR-free formulations, wind energy composite demand

|

|

South Korea

|

Export-oriented electronics and automotive sectors

|

Eco-friendly diluents for low-VOC, high-performance composites

|

Reactive Diluents Market Report Scope

Reactive Diluents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Type (Aliphatic Reactive Diluents, Aromatic Reactive Diluents, Cycloaliphatic Reactive Diluents, Bio-Based Reactive Diluents), By Chemical Structure (Monofunctional, Difunctional, Trifunctional & Higher), By Application (Paints & Coatings, Adhesives & Sealants, Composites, Electronics, Flooring)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huntsman Corporation, Aditya Birla Chemicals, Olin Corporation, Evonik Industries AG, Kukdo Chemical Co. Ltd., BASF SE, Hexion Inc., Arkema SA, Adeka Corporation, Cardolite Corporation, Atul Limited, Mitsubishi Chemical Group, Sakamoto Yakuhin Kogyo Co. Ltd., SACHEM Inc., Nan Ya Plastics Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Reactive Diluents Market Segmentation

By Type

- Aliphatic Reactive Diluents

- Aromatic Reactive Diluents

- Cycloaliphatic Reactive Diluents

- Bio-Based Reactive Diluents

By Chemical Structure

- Monofunctional

- Difunctional

- Trifunctional & Higher

By Application

- Paints & Coatings

- Adhesives & Sealants

- Composites

- Electronics

- Flooring

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Reactive Diluents Industry

- Huntsman Corporation

- Aditya Birla Chemicals

- Olin Corporation

- Evonik Industries AG

- Kukdo Chemical Co. Ltd.

- BASF SE

- Hexion Inc.

- Arkema SA

- Adeka Corporation

- Cardolite Corporation

- Atul Limited

- Mitsubishi Chemical Group

- Sakamoto Yakuhin Kogyo Co. Ltd.

- SACHEM Inc.

- Nan Ya Plastics Corporation

*- List not Exhaustive