Market Overview: CNSL-Based Polyols, High-Purity Cardanol, and Biofuel Pilots Accelerate Cashew Nutshell Liquid Market Expansion

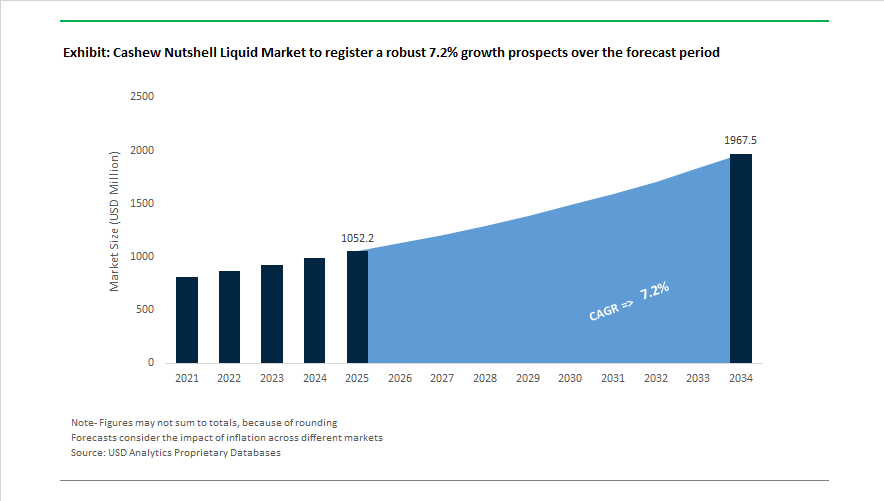

The Cashew Nutshell Liquid (CNSL) market is projected to grow from USD 1,052.2 Million in 2025 to USD 1,967.2 Million by 2034, reflecting a CAGR of 7.2% driven by the rapid industrialization of bio-based phenolic chemistry, renewable polyols, and high-performance resins. Industrial momentum accelerated during 2024 when Cardolite Corporation launched LITE 514HP, a BPA-free, high-bio-content epoxy resin and modifier that strengthened CNSL’s position in corrosion-resistant coatings and structural adhesives. During the same 2024 to 2025 period, Palmer International operationalized its new facility at the TexAmericas Center in Texas after a USD 10 million investment, expanding capacity for CNSL-based friction materials used in automotive brake systems. Export data for FY 2024 to 2025 confirmed India’s expanding role, with 971.69 metric tons of CNSL shipped globally, underscoring Asia’s dominance in raw material processing and value-added chemical derivatives.

Market dynamics shifted significantly in 2025 as advanced purification and downstream diversification accelerated. Cardolite introduced the NX-2024 and NX-2025 low-odor cardanol diluents, enabling broader penetration into indoor flooring and consumer adhesives where volatile odor constraints previously limited CNSL adoption. Late 2025 marked a major technological milestone when producers such as GHW in Vietnam implemented vacuum distillation and supercritical extraction, achieving cardanol purity levels above 95% , enabling CNSL to compete with petroleum phenols in pharmaceutical intermediates and specialty surfactants. In May 2025, COIM USA acquired a Palmer International asset, integrating CNSL-derived renewable polyols into polyurethane systems targeting construction insulation and lightweight automotive components. Cardolite also launched CNSL-based polyols for EV battery adhesives in 2025, leveraging natural hydrophobicity for moisture resistance and thermal management in electric vehicle battery packs.

Bioenergy and sustainability mandates are expanding CNSL’s application scope beyond specialty chemicals. Oilfield service companies adopted CNSL-derived demulsifiers in late 2025 due to their lower toxicity and strong emulsion-breaking performance. In January 2026, maritime research positioned pyrolyzed CNSL blends as a promising marine biofuel candidate aligned with 2050 decarbonization goals, though VPS issued bunker fuel testing guidelines the same month to control contamination risks. Vietnam’s June 2026 biofuel transition policy is expected to redirect domestic CNSL supply toward fuel blending, tightening feedstock availability for chemical-grade exports. Regional capacity additions such as Indonesia’s Kabil Industrial Park investments in 2024 strengthened integrated extraction infrastructure, while global end-use markets continue shifting toward bio-based epoxy resins, CNSL polyols, renewable phenolic modifiers, and high-purity cardanol intermediates that are redefining the competitive landscape of the cashew nutshell liquid industry.

Trends and Opportunities Reshaping the Cashew Nutshell Liquid Market

Strategic Investment in Hydrogenated and Polymerized CNSL for High-Temperature Industrial Resins

The Cashew Nutshell Liquid Market is undergoing a structural transition driven by capital allocation toward hydrogenated and polymerized derivatives, positioning CNSL as a competitive alternative to petroleum-based alkylphenols in performance coatings, epoxy systems, and polyurethanes. Producers such as Cardolite Corporation are central to this shift. Their NX-202X series expansion in 2024–2025 introduced hydrogenated cardanol grades with Gardner color below 1, enabling formulators to substitute fossil-derived phenols in applications where visual clarity, odor neutrality, and high heat tolerance are mission-critical.

Hydrogenated cardanol offers thermal stability tolerance approaching 400°C, enabling its use in corrosion-resistant marine coatings, protective pipeline linings, and industrial epoxy curing agents that require deflection resistance under extreme temperature cycling. Additionally, polymerized CNSL intermediates are allowing producers to enter polyurethane and composite markets—segments previously dominated by palm-oil-based or fossil-based feedstocks. The long hydrophobic side chain inherent to the CNSL molecule provides a natural moisture-barrier effect, making CNSL-derived polyols increasingly relevant for electric vehicle battery enclosures, aerospace composite laminates, and moisture-prone structural adhesives. Moving forward, the business narrative is shifting from “bio-based alternative” toward “performance-driven incumbent,” allowing CNSL producers to compete based on durability and high-specification outcomes rather than solely sustainability credentials.

CNSL-Derived Surfactants Gaining Ground in Enhanced Oil Recovery and Agrochemical Formulations

Cardanol’s amphiphilic chemistry is increasingly being commercialized as next-generation biosurfactants tailored for extreme reservoir and agricultural environments. Recent technical work (December 2025) demonstrates that CNSL-based anionic surfactants, specifically PALA and CALA derivatives, can achieve a Hydrophilic-Lipophilic Balance of 13.7 and critical micelle concentrations as low as 4.10 × 10⁻⁶ M. These parameters translate into practical field performance: more efficient oil-water phase separation, improved wetting on low-permeability rock, and enhanced demulsification efficiencies during crude processing.

With Enhanced Oil Recovery operations prioritizing decarbonized chemical flooding, CNSL surfactants present a reduced-toxicity footprint and can be delivered into production sites without the environmental burdens associated with petroleum-based surfactants. In agrochemicals, they are improving pesticide efficacy through better leaf surfacing and droplet spread, enabling manufacturers to reduce active ingredient dosages while maintaining yield-impacting performance—aligning with farm-level cost pressures and emerging pesticide-residue regulations.

Friction Modifiers Enabling Full Compliance with Copper-Free Brake Pad Legislation

The adoption of CNSL-based friction dust represents one of the largest guaranteed-demand applications across the Cashew Nutshell Liquid Market because of non-discretionary regulatory pressure. Beginning January 1, 2025, the Washington State Better Brakes Law (RCW 70.285) and California SB 346 enforce copper content limits of 0.5% in all brake pads sold within the jurisdictions. This has forced both original-equipment and aftermarket suppliers across North America to adopt polymerized cashew friction dust to maintain coefficient stability and meet heavy-duty fleet braking standards.

From a functional standpoint, CNSL friction dust contributes damping properties, helping to reduce brake squeal, rotor scoring, and dust pollution. As electric vehicle fleets expand, brake pad frequency decreases due to regenerative braking, meaning more demanding thermal shock cycles and moisture exposure during low-use intervals. CNSL friction dust’s resistance to oxidative degradation positions it as a friction modifier suited for EV fleet duty cycles, creating procurement stickiness for manufacturers who adopt CNSL-based systems.

CNSL as a Precursor for Carbon Aerogels and Battery-Grade Carbon Foams

Beyond legacy resin applications, the most transformational future-growth avenue lies in CNSL’s role as a renewable precursor for high-value carbon materials. Because cardanol exhibits a high carbon yield during pyrolysis, CNSL is being commercialized as a feedstock for carbon aerogels and foams—materials central to energy storage, thermal insulation, and lightweight structural components.

Industrial pilot lines are now producing CNSL-derived aerogels that form 3D porous carbon matrices suited for supercapacitor electrodes, where surface area and electrolyte diffusion dictate energy efficiency. In lithium-sulfur battery development, CNSL carbon foams are being tested as sulfur-immobilizing separators, improving cycle stability and conductivity—addressing a critical barrier that previously prevented Li-S chemistries from entering commercial deployment. If performance continues to validate at scale, CNSL feedstock producers could expand from resin suppliers into strategic materials vendors for the battery sector, unlocking multi-year offtake agreements and technology licensing models.

Cashew Nutshell Liquid (CNSL) Market Share and Segmentation Insights

Market Share by Product Type: Cardanol Anchors Value While Refined and Crude CNSL Support Volume

Cardanol holds 44% of CNSL-derived product demand in 2025, serving as a renewable meta-alkylphenol feedstock for phenolic resins, epoxy curing agents, friction materials, and specialty surfactants. Its ability to replace petrochemical phenol in coatings and automotive brake systems positions it as the most commercially valuable CNSL derivative. Refined cashew nutshell liquid ranks second, offering a cost-effective blend rich in cardanol and cardol for direct use in industrial coatings and polymer modification, albeit with lower compositional consistency. Crude CNSL remains a traded commodity exported primarily from India, Vietnam, and West Africa to downstream processors in China, Europe, and the US, with pricing influenced by cashew harvest cycles. Anacardic acid represents a niche but high-value stream for bioactive skincare and pharmaceutical applications, supported by clean-label trends, while cardol remains the smallest segment due to separation complexity, supplying specialty surfactants and high-temperature lubricant additives.

Market Share By Product Type, 2025.png)

Market Share by End Use Industry: Construction Leads as Automotive and Bio-Based Chemicals Expand

Building and construction account for 34% of CNSL consumption in 2025, driven by cardanol-based epoxy coatings, concrete sealers, and corrosion-resistant flooring systems that deliver low VOC emissions and renewable carbon content aligned with green building certifications. Automotive and transportation follow, utilizing CNSL derivatives in brake pads and clutch facings for stable friction performance, as well as reactive diluents in primers and structural adhesives supporting lightweight vehicle assembly and emerging EV battery enclosure coatings. Industrial chemicals form a significant downstream channel, converting CNSL into phenolic resins, foundry binders, abrasive wheels, and polyurethane polyols. Marine and aerospace remain specialized, high-performance markets for anti-corrosive coatings in ship hulls, offshore platforms, and aircraft components. Healthcare and pharmaceuticals represent the fastest-growing niche, leveraging anacardic acid in anti-acne, antibacterial, and oral care formulations, where natural origin and bioactivity command premium pricing despite modest volumes.

Competitive Landscape of the Cashew Nutshell Liquid (CNSL) Market

The global cashew nutshell liquid (CNSL) market in 2026 is defined by rapid growth in bio-based resins, cardanol derivatives, phenalkamine curing agents, friction materials, and sustainable polyurethane inputs. Competitive differentiation centers on molecular functionalization, vacuum-distilled cardanol purity, waterborne zero-VOC technologies, and vertically integrated cashew shell sourcing. Market leaders are scaling USDA-certified bio-based epoxies, corrosion-resistant coatings, EV brake binders, and nonyl-phenol-free surfactants, while ESG compliance, EUDR traceability, and circular bio-economy practices increasingly shape procurement decisions. Demand is accelerating across protective coatings, composites, automotive friction materials, bio-lubricants, and green construction, positioning CNSL as a strategic renewable feedstock in the global specialty chemicals value chain.

Bio-based epoxy curing leadership and molecular engineering excellence from Cardolite Corporation

Cardolite dominates the 2026 CNSL market through advanced cardanol refining and high-performance bio-based derivatives. Its Ultra LITE and NX series anchor a portfolio of USDA-certified phenalkamines, polyols, and reactive diluents engineered for fast cure and superior moisture resistance in coatings and composites. In late 2025, Cardolite launched Waterborne Phenalkamines delivering zero-VOC performance while retaining heavy-duty corrosion protection. A core differentiator is molecular functionalization, modifying cardanol at multiple structural points to create tailored monomers for adhesives and polyurethane systems. Strategically, Cardolite is positioning CNSL polyols as hydrophobic alternatives to petro-based polyethers, reinforcing its role in sustainable performance materials.

Integrated cashew shell valorization and ESG traceability driven by Olam Food Ingredients

OFI enters 2026 as the architect of the integrated CNSL supply chain, leveraging its scale as a global cashew processor. Expanded shell-processing capacity in Côte d’Ivoire and Vietnam enables in-house CNSL extraction with full traceability. Through its AtSource digital platform, OFI provides real-time ESG metrics aligned with EUDR and global sustainability frameworks. Following its parent’s stake sale to SALIC, OFI refocused capital on waste valorization, converting shells into CNSL and bio-char. The company is a dominant supplier of technical-grade CNSL for automotive friction materials, reinforcing its leadership in sustainable sourcing and large-volume industrial applications.

High-purity vacuum-distilled cardanol scale from Cat Loi Cashew Oil Production & Export J.S.C.

Cat Loi stands out in 2026 as a major Vietnamese producer of vacuum-distilled CNSL, supplying Asian and European coatings markets. Specializing in refined cardanol exceeding 95% purity, the company uses advanced distillation to maximize active content while minimizing polymeric residues, making its products ideal for premium paint resins. Strategic upgrades in 2025/2026 introduced emission-reducing scrubbers, improving environmental performance versus traditional roasting extraction. Located at the center of Vietnam’s cashew belt, Cat Loi combines logistics efficiency with competitive pricing. Its CNSL derivatives are widely exported for maritime coatings, valued for salt-water corrosion resistance and anti-fouling durability.

Green solvent extraction and bioactive CNSL innovation by Mane Kancor Ingredients

Mane Kancor applies specialty extraction expertise to CNSL, focusing on cold-pressed grades rich in anacardic acid for niche pharmaceutical and bio-pesticide uses. In early 2026, the company introduced low-heat extraction to preserve sensitive bioactives, expanding CNSL into higher-value functional ingredients. Backed by MANE’s global R&D network, Kancor is also developing CNSL-based aroma and fixative chemicals that bridge industrial resins with specialty fragrance applications. With ₹150 crore invested in Indian processing expansion, Kancor’s 2026 strategy centers on “Ingredients of the Future,” including CNSL bio-surfactants produced via sustainable green solvent platforms.

EV-ready friction materials and customized CNSL binders from Palmer International

Palmer International anchors the Americas’ CNSL market with high-performance friction dust and brake resin systems for EVs and rail. Its products enable superior heat dissipation and low-noise operation in heavy-duty braking environments. Responding to 2026 US reshoring trends, Palmer strengthened domestic processing to mitigate raw material volatility. A defining strength is technical customization, producing friction particles with precise mesh sizes and thermal profiles tailored to OEM specifications. Palmer dominates North American rail and transit applications, where CNSL-based binders outperform synthetic phenolics in wear resistance and NVH reduction, reinforcing its position in advanced mobility materials.

Circular bio-materials integration and refined CNSL logistics by GHW (Vietnam) Co., Ltd.

GHW advances CNSL adoption through biorefinery integration, co-producing bio-lubricants for industrial machinery markets transitioning away from mineral oils. Recognized in late 2025 for circular bio-economy practices, GHW converts de-oiled shell residue into biomass pellets for industrial boilers. The company expanded refined CNSL capacity in 2026 to meet rising demand for cardanol in nonyl-phenol-free surfactants. With both technical and refined grades available, GHW supports coatings and specialty chemical customers worldwide. Its global logistics network enables flexible shipping via flexi-bags or ISO tanks, preserving CNSL purity across long-haul routes to the US and EU.

Côte d’Ivoire: Local Processing Acceleration and ISO-Tank Export Logistics Transform CNSL Manufacturing

Côte d’Ivoire is rapidly repositioning itself from a raw cashew exporter to a global cashew nutshell liquid (CNSL) manufacturing hub through large-scale industrial processing and policy-driven value addition. In September 2025, a $27 million (CFA 15 billion) processing facility was inaugurated in Kpouèbo with backing from Robust International. The plant has a capacity of 120 tons of raw nuts per day (37,440 tons annually) and is specifically engineered for high-quality CNSL extraction using improved thermal recovery systems. This milestone significantly increases domestic availability of technical CNSL (TCNSL) for export into epoxy resins, friction materials, and phenolic intermediates.

Through the Cotton, Cashew, and Shea Council (CCA-K), the government has set a strategic target to locally process 50% of its 1.5 million-ton harvest by the end of 2025. By May 2025, industrial processors had already secured 650,000 tons of raw nuts—exceeding initial procurement targets by 62% —indicating strong feedstock availability for CNSL distillation and cardanol production. Tax holidays for “Secondary and Tertiary Processing” specifically incentivize the upgrading of technical CNSL into high-value cardanol, potentially increasing export revenues by 15–20% . Logistics have improved following investments by Maersk under the West African Cashew Campaign, enabling bulk CNSL shipment in ISO tanks and reducing transit times to European chemical hubs by approximately 12 days. New facilities incorporate smoke scrubbers and closed thermal extraction systems, addressing carbon footprint concerns associated with traditional open-pan extraction.

India: Cardanol Export Specialization and Polyol Innovation Strengthen CNSL Derivatives Market

India’s cashew nutshell liquid industry is moving up the value chain through integration, mechanization, and derivative innovation. In late 2025, Oriental Aromatics Ltd consolidated its terpene and CNSL divisions to focus on high-purity isoborneol and CNSL derivatives for pharmaceutical and fragrance applications. This integration supports specialty chemical positioning rather than commodity-grade exports.

Public sector expansion is also visible. Gujarat State Fertilizers & Chemicals Ltd launched an R&D initiative in June 2025 to develop CNSL-based polyols for rigid polyurethane foams targeting India’s growing construction sector. According to APEDA FY25 data, India shifted export emphasis toward refined cardanol, shipping over 7,500 MT to key markets such as the Republic of Korea, the United Kingdom, and Germany within the first three quarters. To secure long-term raw material supply, the Directorate of Cashew nut & Cocoa Development approved expansion of cashew cultivation by 120,000 hectares by 2026. Financially, the Ministry of Commerce and Industry allocated ₹60 crore ($8 million) under a Medium Term Framework to modernize CNSL extraction units, enhancing yield efficiency and operator safety. Academic institutions are advancing CNSL-based bio-pesticides and surfactants, targeting commercial rollout by 2026 as sustainable substitutes for petroleum-derived agrochemicals.

Vietnam: High-Purity Cardanol Refining and Wind Energy Integration Drive CNSL Premiumization

Vietnam remains the dominant supplier of technical CNSL (TCNSL), with companies such as GHW (Vietnam) and Kimmy LLC contributing to broader cashew export revenues exceeding $2.36 billion in the first half of 2025. The country’s competitive advantage lies in refining capabilities; upgraded vacuum distillation columns now enable production of Gardner 1 color grade cardanol, suitable for electronics and semiconductor packaging markets requiring ultra-low color specifications.

Western wind-energy blade manufacturers have established direct sourcing agreements with Vietnamese processors for high-purity cardanol used in bio-based epoxy resins, reducing reliance on petroleum-derived phenolics. Vietnam has also emerged as a marine coating innovation hub, where phenalkamine curing agents derived from CNSL reduced dry-dock turnaround time by 25% in high-humidity shipyard conditions. The 2025 “Golden Cashew Rendezvous” policy forum introduced regulatory measures favoring export of refined derivatives over raw shells, targeting $4.5 billion in total sector exports by 2026. This strategic pivot strengthens Vietnam’s leadership in value-added CNSL derivatives rather than primary raw materials.

United States: Bio-Based Epoxy Modifiers, Marine Biofuels, and Friction Material Substitution Expand CNSL Applications

The United States CNSL market is shaped by consolidation, infrastructure mandates, and renewable material innovation. Cardolite Corporation continues to dominate high-performance phenalkamine curing agents and expanded its Ultra LITE technology in early 2026, delivering shelf-stable epoxy modifiers for coatings and composites. The U.S. International Trade Commission’s 2025 ruling on epoxy resin imports created favorable conditions for bio-based additives under “Build America, Buy America” requirements, accelerating integration of CNSL-derived phenolics into infrastructure coatings.

In marine fuels, a collaboration involving Lloyd's Register and Wärtsilä validated the FSI.100 CNSL-based biofuel as a 30% blend component in marine gasoil during 2024–2025 sea trials. Automotive friction material manufacturers are replacing copper and antimony with CNSL-based bio-phenolics to comply with heavy metal emission caps in California and Washington. Venture capital investment has also surged into CNSL-derived graphene oxide research, leveraging cashew shells as a sustainable carbon precursor for advanced energy storage and composite materials.

Brazil: Zero-Waste Electrochemical Conversion and Bio-Resin Diversification Strengthen Domestic CNSL Value Chain

Brazil’s CNSL industry is evolving through renewable feedstock innovation and construction-grade bio-resin applications. Peer-reviewed research published in 2025–2026 demonstrated electrochemical synthesis of citric, malonic, and acetic acids directly from CNSL effluents, enabling zero-waste processing models and circular chemical valorization. Government-backed crop diversification policies are promoting replacement of aging cashew plantations with high-yielding CNSL-rich varieties in northeastern states, revitalizing domestic raw shell supply.

Brazilian firms are specializing in CNSL-based particleboard adhesives achieving Class E1 formaldehyde emission compliance while increasing biodegradability of panels by approximately 30% . Petrobras has explored integration of cashew-derived oils into renewable diesel pilot programs, aligning agricultural byproducts with low-carbon fuel strategies. These initiatives collectively position Brazil as a diversified CNSL innovation center spanning bio-resins, green chemistry, and renewable fuels.

Netherlands: Rotterdam Bio-Based Throughput and Non-Isocyanate Polyurethane Innovation Expand Cardanol Markets

The Netherlands has solidified its role as Europe’s primary entry point for cardanol and CNSL derivatives, with the Port of Rotterdam recording a 15% increase in bio-based chemical throughput in 2025. This gateway status enhances supply chain efficiency for European epoxy resin, surfactant, and coatings manufacturers reliant on imported CNSL intermediates.

Dutch formulators are leading development of CNSL-derived ethoxylates as biodegradable substitutes for nonylphenol ethoxylates in professional cleaning products. Leveraging EU Green Deal funding, chemical companies in the Netherlands are advancing 100% bio-based non-isocyanate polyurethane (NIPU) coatings where CNSL functions as the primary polyol component. This circular economy alignment strengthens Europe’s transition toward fossil-free coatings and surfactants, reinforcing the Netherlands’ strategic importance in the global cashew nutshell liquid industry.

Cashew Nutshell Liquid Market Report Scope

Cashew Nutshell Liquid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1052.2 Million

|

|

Market Size (2034)

|

$1967.2 Million

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Product Type (Crude Cashew Nutshell Liquid, Refined Cashew Nutshell Liquid, Cardanol, Cardol, Anacardic Acid), By Grade (Technical Grade, Refined Grade), By Extraction Technology (Mechanical Extraction, Solvent Extraction, Supercritical Extraction, Thermal Treatment), By Application (Friction Materials, Resins and Coatings, Adhesives and Sealants, Surfactants and Plasticizers, Bio Fuels, Other Applications), By End Use Industry (Automotive and Transportation, Building and Construction, Industrial Chemicals, Marine and Aerospace, Healthcare and Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cardolite Corporation, Kraton Corporation, Kolon Industries, Mangalam Organics, Gujarat State Fertilizers and Chemicals, Indo Amines, Catay Specialty Chemicals, Palmer International, Olam International, Robust International, Haoyi New Material, Henglong Chemical, Kanchi Karpooram, Nexira, Sonas Cosmetics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cashew Nutshell Liquid Market Segmentation

By Product Type

- Crude Cashew Nutshell Liquid

- Refined Cashew Nutshell Liquid

- Cardanol

- Cardol

- Anacardic Acid

By Grade

- Technical Grade

- Refined Grade

By Extraction Technology

- Mechanical Extraction

- Solvent Extraction

- Supercritical Extraction

- Thermal Treatment

By Application

- Friction Materials

- Resins and Coatings

- Adhesives and Sealants

- Surfactants and Plasticizers

- Bio Fuels

- Other Applications

By End Use Industry

- Automotive and Transportation

- Building and Construction

- Industrial Chemicals

- Marine and Aerospace

- Healthcare and Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Cashew Nutshell Liquid Industry

- Cardolite Corporation

- Kraton Corporation

- Kolon Industries

- Mangalam Organics

- Gujarat State Fertilizers and Chemicals

- Indo Amines

- Catay Specialty Chemicals

- Palmer International

- Olam International

- Robust International

- Haoyi New Material

- Henglong Chemical

- Kanchi Karpooram

- Nexira

- Sonas Cosmetics

*- List not Exhaustive