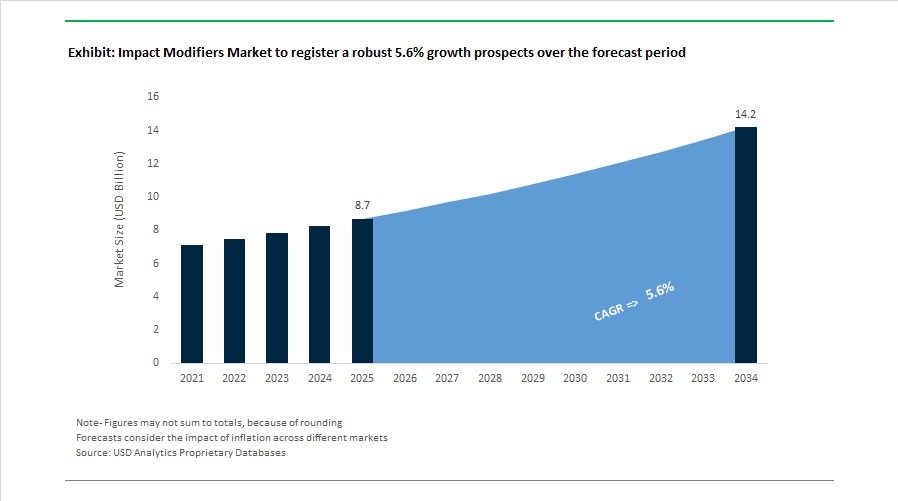

Impact Modifiers Market to Reach $14.2 Billion by 2034 at 5.6% CAGR Amid Recycling Mandates and EV Lightweighting

The Impact Modifiers Market is projected to expand from $8.7 billion in 2025 to $14.2 billion by 2034, registering a steady CAGR of 5.6%. Growth is being shaped by regulatory pressure on recycled plastics, rapid electrification of mobility, and the increasing performance requirements of lightweight polymers across packaging, automotive, electronics, and construction. Impact modifiers, including acrylic impact modifiers (AIM), MBS, CPE, ABS modifiers, and core-shell tougheners, are becoming essential for enhancing toughness, low-temperature resistance, and durability in both virgin and post-consumer recycled (PCR) resins.

In February 2025, the EU Packaging and Packaging Waste Regulation entered into force, mandating that all packaging be recyclable by 2030 and establishing strict recycled content thresholds. This regulation triggered a structural surge in demand for impact modifiers capable of restoring mechanical strength and drop-test performance in recycled polyethylene, polypropylene, and PET streams. In May 2025, Dow introduced its Decarbia reduced-carbon silicone elastomer platform, integrating lower-carbon feedstocks into hybrid modifier systems used in industrial coatings and personal care packaging. Throughout 2024 and 2025, Kaneka expanded its Kane Ace MX liquid core-shell toughener range, targeting epoxy resin systems for electric vehicle battery enclosures and lightweight structural composites. In 2025, LG Chem signed an MoU with EL Electric to co-develop flame-retardant EV charging cables using ultra-high molecular weight PVC and proprietary impact-modifying technologies, achieving 30% greater flexibility and enhanced thermal resistance.

Battery manufacturing expansion has reinforced regional demand for high-performance impact-modified plastics. By early 2025, LG Energy Solution confirmed investments exceeding $4.5 billion to add 70 GWh of battery capacity in the United States, with parallel cathode material expansions by LG Chem. These investments accelerated the use of impact-modified polypropylene, ABS, and PVC compounds in battery housings and electrical safety components. In December 2025, Mitsubishi Chemical announced plans to double carbon fiber capacity through 2027, indirectly stimulating demand for impact-modified epoxy and advanced resin systems used in aerospace and performance automotive composites.

Strategic portfolio restructuring and innovation intensified in 2026. In January 2026, Dow launched its “Transform to Outperform” strategy targeting $2 billion in EBITDA improvement, emphasizing modernization of specialty plastics and additives. In January 2026, Arkema finalized the divestment of its global MBS and acrylic impact modifier operations to Praana, reshaping competitive dynamics in Europe and Asia. At PlastIndia 2026 in February, Milliken introduced next-generation DeltaMax performance modifiers designed to balance melt flow and impact strength in virgin and recycled polypropylene, enabling thinner-wall packaging and lower processing temperatures. During the same event, BASF showcased its Tinuvin NOR stabilizer and modifier platform engineered for agricultural plastics requiring extreme UV and heat resistance. In January 2026, Sony and global partners launched a renewable plastics supply chain aimed at achieving virgin-equivalent drop performance in recycled electronics plastics through advanced impact modification technologies.

Impact Modifiers Market Trends and Opportunities

Accelerated Adoption of Acrylic Impact Modifiers for Long-Life Weatherable PVC

The global impact modifiers market is undergoing a decisive shift in outdoor construction applications, with Acrylic Impact Modifiers emerging as the default solution for weatherable PVC profiles. Regulatory pressure and buyer expectations have converged around a 30-year service life benchmark for windows, siding, and fencing across North America and Europe. This has materially weakened the position of traditional Chlorinated Polyethylene and MBS modifiers, which exhibit inferior UV stability and long-term color retention under accelerated weathering.

Tier-1 suppliers are actively reshaping portfolios to align with this structural demand shift. In late 2025, Arkema’s proposed divestment of its MBS business signaled a strategic retreat from indoor-grade modifiers and a capital redeployment toward specialty acrylic copolymers optimized for outdoor exposure. Production audits from 2025 further validate this transition. Modern all-acrylic core-shell modifiers maintain ductile fracture behavior in rigid PVC even after 10,000 hours of accelerated weathering, meeting zero-maintenance durability claims increasingly required by residential building codes and green construction certifications.

Beyond durability, AIM adoption is being reinforced by processing economics. High-efficiency acrylic modifiers now act as dual-function additives, improving PVC melt strength by approximately 15–20%. This enables higher extrusion throughput, reduces scrap rates, and lowers energy consumption per linear meter of profile, directly improving margins for window and siding manufacturers facing rising labor and electricity costs.

Functionalized Impact Modifiers Enabling Paint-Ready Automotive Thermoplastics

Automotive lightweighting strategies are accelerating the substitution of steel with polypropylene and polyamide in exterior body panels. This structural shift is driving demand for functionalized impact modifiers that provide both toughness and surface adhesion. By grafting reactive groups such as maleic anhydride onto elastomeric modifiers, OEMs and Tier-1 suppliers are eliminating primer layers traditionally required for painting plastic substrates.

This trend is particularly pronounced in electric vehicles, where Class A surface finishes are no longer optional. Automotive color and coating roadmaps for 2025–2026 show increased adoption of multi-layer metallic and high-chroma finishes, which require consistent paint adhesion across complex geometries. Functionalized impact modifiers now deliver up to 30% stronger adhesive bonding between thermoplastics and structural adhesives, improving paint durability and crash performance simultaneously.

From a circularity perspective, these modifiers are also enabling recyclability. Chemical recycling pilots conducted in 2025 demonstrated that functionalized elastomer-modified polypropylene components can be reprocessed with minimal loss of mechanical performance. This aligns with OEM targets to reintegrate automotive shredder residue into high-value interior and exterior components, shifting impact modifiers from a cost add-on to a strategic enabler of circular automotive platforms.

Bio-Based Toughening Agents for Brittle Biopolymers

A major opportunity frontier is opening in bio-based impact modifiers designed for inherently brittle polymers such as polylactic acid and polyhydroxyalkanoates. As the European Commission advances regulations to phase out non-degradable fossil-based packaging by 2028, biopolymers are moving from niche to mainstream. However, their limited low-temperature impact resistance remains a structural barrier to adoption.

By late 2025, the dedicated market for PLA impact modifiers had reached an estimated valuation of $750 million, with growth driven by packaging, disposable consumer goods, and agricultural films. New-generation bio-based modifiers are engineered to improve toughness without compromising compostability certifications. Innovations in PHA-based rubber phases introduced in 2025 have enabled rigid biopolymer blends to achieve impact performance comparable to modified polypropylene while remaining fully soil and marine degradable.

Public funding is accelerating commercialization. European bioeconomy programs have earmarked over €170 million for 2026 to support bio-based chemical scale-up, with a strong emphasis on closing the mechanical performance gap of bioplastics. This positions bio-based impact modifiers as one of the highest-margin segments within the broader impact modifiers market over the next five years.

Non-Migrating Impact Modifiers for Food Contact and Medical Compliance

Regulatory tightening around Food Contact Materials and medical devices is creating a structurally attractive opportunity for non-migrating, permanently bound impact modifiers. The 2025 update to EU food contact regulations introduces unprecedented scrutiny of Non-Intentionally Added Substances, effectively disqualifying low-molecular-weight modifiers that can leach into food simulants.

In parallel, intensified FDA inspections in 2025 have raised the compliance bar for medical container-closure systems and device housings. Manufacturers are now required to fully characterize potential extractables and leachables, driving rapid adoption of high-molecular-weight acrylic and core-shell modifiers with cross-linked rubber domains. These systems remain locked within the polymer matrix, delivering impact resistance without migration risk.

Medical-grade impact modifiers are now being specified as part of risk mitigation strategies rather than optional enhancements. Adoption rates for locked-in acrylic modifiers in transparent medical housings increased by approximately 25% in 2025, as OEMs prioritize regulatory certainty alongside mechanical performance. This shift is transforming compliance-driven markets into premium, defensible revenue streams for advanced impact modifier suppliers.

Impact Modifiers Market Share and Segmentation Insights

Acrylic Impact Modifiers Lead the Market Through Weather-Resistant PVC Performance in Construction

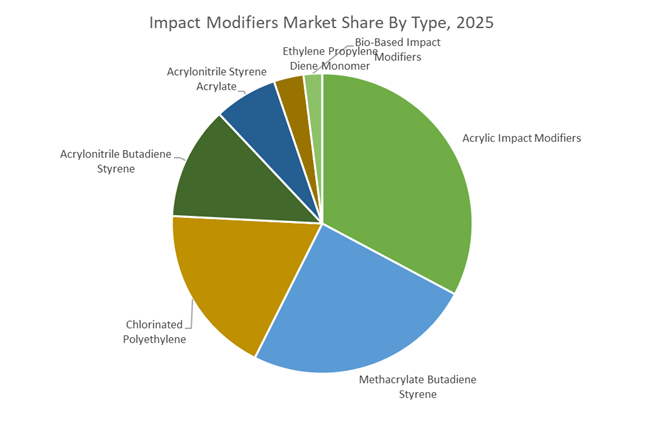

Acrylic impact modifiers accounted for 32.80% of the Impact Modifiers Market share in 2025, making them the most widely used modifier type in polymer performance enhancement. Acrylic-based modifiers are extensively used to improve the impact resistance, durability, and processing stability of polyvinyl chloride (PVC) compounds, particularly in rigid PVC products used across the construction industry. Their dominance stems from the ability to provide excellent weatherability, ultraviolet resistance, and long-term color stability, which are essential for outdoor applications such as window profiles, vinyl siding, fencing, decking, and exterior cladding systems. Unlike many alternative modifiers, acrylic impact modifiers maintain performance without yellowing or degradation during long-term exposure to sunlight and environmental conditions. In 2025, demand is strongly influenced by the continued global expansion of PVC-based building materials, particularly in residential construction and renovation markets. New formulation developments allow manufacturers to produce thinner and lighter PVC profiles while maintaining structural strength and impact resistance, improving material efficiency and lowering production costs for construction products.

Polyvinyl Chloride Applications Dominate Impact Modifier Consumption

Polyvinyl Chloride (PVC) represented 58.60% of the Impact Modifiers Market share in 2025, making it the largest application segment within the global polymer additives industry. PVC is inherently rigid and brittle in its unmodified state, requiring the addition of impact modifiers to enhance toughness, flexibility, and resistance to cracking during installation and long-term use. As a result, nearly all rigid PVC products incorporate impact modifier formulations to achieve the mechanical performance required for commercial applications. Major PVC-based products include pipes and fittings, window profiles, siding, cable insulation, and industrial components, with construction and infrastructure development driving the majority of global consumption. In 2025, an important technological shift shaping this segment is the global transition away from lead-based stabilizers in PVC formulations, replaced by environmentally compliant calcium-zinc stabilizer systems. This regulatory transition has required polymer additive manufacturers to develop new impact modifier formulations compatible with modern stabilizer chemistry, ensuring consistent processing performance, mechanical strength, and long-term durability in next-generation PVC materials used in building and infrastructure applications.

Competitive Landscape in Impact Modifiers Market

Arkema Expands Specialty Acrylic Modifier Platform

Arkema S.A. continues to anchor its position through its Specialty Materials segment, reporting 2025 sales of €9.07 billion and EBITDA of €1.25 billion. Its Biostrength® and Durastrength® acrylic impact modifiers are engineered to improve PVC weatherability, impact resistance, and long-term durability in exterior construction applications. In early 2026, Arkema completed three capacity expansions across the U.S. and Asia, expected to contribute €50 million in incremental EBITDA during 2026. Strategic focus centers on decarbonization and circularity, with a €600 million capex plan supporting bio-based feedstocks and recyclable additive solutions. The company targets a 16.5% EBITDA margin by 2027, positioning impact modifiers as a value-accretive segment within its broader performance polymer portfolio.

Dow Drives Efficiency and North American Supply Resilience

Dow Inc. is reinforcing its position in acrylic and MBS modifiers through operational restructuring under its “Transform to Outperform” initiative, targeting $2 billion in operating EBITDA improvement by 2028. The PARALOID™ portfolio remains a benchmark in transparent packaging, electronics housings, and low-temperature applications requiring clarity and toughness. Dow expects approximately $500 million in EBITDA gains in 2026 from efficiency programs despite one-time restructuring costs between $1.1 billion and $1.5 billion. Strategically, the company is emphasizing domestic production in North America to mitigate tariff exposure and supply volatility. This localized manufacturing model strengthens its competitive advantage in packaging and building materials where reliability and lead-time performance are critical.

Kaneka Advances Core-Shell Technology and Bioplastic Integration

Kaneka Corporation retains technological leadership in multilayer core-shell impact modifier technology through its KANE ACE™ line. These engineered polymer particles enhance the toughness of PVC, PMMA, and PBT while maintaining heat resistance and transparency. In February 2026, Kaneka expanded its Green Planet™ biodegradable polymer adoption across sports and food service brands, reinforcing its strategy of linking impact modification with sustainable polymers. Its European operations in Belgium and Germany support consolidation of strong market share in the acrylic-modifier niche. Kaneka is diversifying applications into healthcare materials and solar-related components, broadening demand beyond traditional construction and packaging sectors.

LG Chem Aligns Impact Modifiers with EV Infrastructure Growth

LG Chem Ltd. is integrating its petrochemical backbone with AI-driven operational reforms under its AX and OKR transformation framework. The company has commercialized high-performance PVC compounds and modifiers tailored for EV charging cables and infrastructure, delivering approximately 30% greater flexibility compared to standard formulations. Its Tianjin site achieved UL Solutions’ Zero Waste to Landfill Platinum certification in early 2026, reinforcing sustainability positioning. By coupling ultra-high molecular weight PVC with proprietary modifiers, LG Chem is targeting flame-retardant and high-durability applications in electrification and smart-grid infrastructure.

Mitsubishi Chemical Repositions Around Bio-Engineered Polymers

Mitsubishi Chemical Group is simplifying its portfolio under its “Grow UP 2026” strategy, targeting a 10% operating margin in core segments. DURABIO™, a plant-derived engineering plastic adopted in automotive interior AI speaker components, illustrates its pivot toward specialty, bio-derived materials. The company is exiting legacy carbon businesses and reallocating resources toward green chemicals and circular polymer initiatives. A February 2026 memorandum with MUFG Bank advances recycling proof-of-concept programs to close commercial polymer loops. Impact modification capability remains integral to ensuring mechanical durability in plant-derived engineering plastics.

BASF Scales Asian Capacity While Tightening Cost Discipline

BASF SE is executing its “Winning Ways” strategy with a €1.7 billion cost-reduction run rate achieved by end-2025 and a target of €2.3 billion by end-2026. The Zhanjiang Verbund site in China, operational since late 2025, serves as the primary growth engine for impact modifiers and performance materials across Asia. BASF projects 2026 Group EBITDA before special items between €6.2 billion and €7.0 billion, with free cash flow potentially reaching €2.3 billion. A €1.5 billion share buyback program (November 2025–June 2026) underscores balance sheet strength. Within impact modifiers, BASF is prioritizing localized production, integration advantages from its Verbund model, and high-performance additive formulations tailored for recyclable and flame-retardant polymer systems.

United States Impact Modifiers Market: Strategic Asset Retention and Performance-Driven Formulation Shifts

The United States impact modifiers industry is undergoing targeted consolidation and performance-led innovation, shaped by construction resilience, automotive electrification, and sustainability-linked regulation. In December 2025, Arkema executed a major global divestment of its plastic additives portfolio to the Indian industrial group Praana, while deliberately retaining its Mobile, Alabama facility. This decision underscores the strategic importance of North American Acrylic Impact Modifier production, particularly for U.S. construction materials and automotive polymers that require consistent supply, localized technical support, and compliance with ASTM performance standards. Retention of AIM capacity also reflects steady domestic demand for weatherable PVC profiles, vinyl siding, and window systems, where acrylic-based modifiers are increasingly preferred for long-term UV resistance and color stability.

Regulatory and technology-driven demand vectors are reinforcing this position. The EPA’s 2026 recycled content guidelines for federally funded infrastructure projects have accelerated adoption of compatibilizer–impact modifier hybrids that restore toughness and elongation in post-consumer resin blends used in structural plastics. In parallel, U.S. manufacturers reported a 14% increase in development activity for ultra-clean impact modifiers formulated for fluoropolymer piping in sub-2nm semiconductor fabrication facilities, where particulate control and mechanical integrity are critical. At the innovation frontier, Dow Inc. released performance data for PARALOID EXL-3691J in late 2025, an MBS-based modifier designed to preserve impact strength of PC and PC/ABS blends under extreme cold conditions, directly targeting electric vehicle battery housings in North America.

India Impact Modifiers Market: Global Manufacturing Hub Formation and Recycled Plastics Enablement

India has emerged as a pivotal center in the global impact modifiers value chain, driven by cross-border acquisitions, regulatory mandates on recycled plastics, and infrastructure-led polymer demand. In December 2025, the Indian industrial group Praana, parent of Galata Chemicals and Sterling Specialty Chemicals, announced its agreement to acquire Arkema’s global MBS business along with its Asian and European AIM operations. Expected to close in the first quarter of 2026, this transaction structurally repositions India as a global manufacturing and export hub for impact modifiers, with access to established technologies, customer relationships, and formulation expertise across mature markets.

Domestic regulation and infrastructure spending are amplifying demand. Amendments to India’s Plastic Waste Management Rules for the 2025–26 fiscal year mandate 30% recycled content in Category I rigid packaging, creating a sizable secondary market for modifiers that compensate for brittleness and molecular degradation in recycled polymers. Concurrently, large-scale national highway upgrades and associated electrical conduit and HVAC installations have driven a 22% increase in local demand for chlorinated polyethylene and high-efficiency ABS modifiers. This momentum is further supported by the expansion of production-linked incentive schemes under the 2026 Union Budget, which explicitly targets high-end polymer additives to reduce reliance on imports from East Asia.

South Korea Impact Modifiers Market: Automotive Surface Quality and EV Safety Focus

South Korea’s impact modifiers industry is increasingly aligned with automotive aesthetics, electric vehicle safety, and export-oriented specialty plastics. In October 2025, LG Chem showcased its Impact Ready portfolio at K 2025 in Germany, highlighting ASA and high-gloss ABS modifiers engineered for 2026 automotive platforms. These materials deliver high heat resistance and weatherability while eliminating secondary painting processes, supporting lightweighting and cost efficiency for OEMs. Earlier in 2025, LG Chem became the first Korean member of the Global Impact Coalition, a CEO-led initiative focused on net-zero chemical innovation using AI-guided molecular design to reduce the carbon intensity of impact modifiers.

Safety-driven innovation is also gaining prominence. In late 2025, South Korean producers launched flame-retardant engineering plastic modifiers designed to delay thermal runaway in electric vehicle battery packs, addressing regulatory scrutiny and OEM risk management priorities. Alongside this, the development of ultra-high molecular weight PVC modified with high-modulus compounds for flexible EV charging cables has become a core export focus, reinforcing South Korea’s position in advanced polymer modification for mobility infrastructure.

Japan Impact Modifiers Market: Supply Chain Stabilization and Bio-Based Integration

Japan’s impact modifiers market is characterized by supply chain discipline, advanced core-shell technologies, and early integration of bio-based polymers. Between July 2024 and mid-2025, Kaneka Corporation implemented price and supply realignments for its Kane Ace series, stabilizing global availability and enabling reinvestment into core-shell modifier technology for ultra-transparent PVC applications. These developments are particularly relevant for medical, electronics, and premium packaging uses where optical clarity and impact resistance must coexist.

In parallel, Kaneka achieved an industry-first milestone in 2025 by integrating its biodegradable polymer PHBH with specialized impact modifiers for pharmaceutical packaging and bio-based banding films. This innovation aligns with Japan’s broader decarbonization agenda, exemplified by Kaneka’s selection for Saitama City’s sustainable urban development project in November 2025. Complementing these initiatives, Mitsubishi Chemical Group announced a phased doubling of carbon fiber capacity in Japan and the United States through 2027, intensifying R&D demand for advanced toughening agents used in aerospace and hypercar composite structures.

China Impact Modifiers Market: Infrastructure Demand and Export-Led Scale

China’s impact modifiers industry continues to scale through policy-backed specialty chemical growth and infrastructure-intensive end-use demand. Under the Ministry of Industry and Information Technology Green Growth Blueprint for 2025–2026, the specialty chemical sector is guided toward a minimum annual expansion target, with high-end polymer additives identified as a priority segment. This policy framework has reinforced investment in advanced impact modifiers for engineering plastics used in transport, energy, and urban infrastructure.

Urban rail expansion in 2025 has been a major consumption driver, with extensive use of modified engineering plastics in electrical and safety-critical components required to meet seismic resistance and fracture toughness codes. Despite persistent trade tensions, Chinese MBS producers increased exports to Southeast Asia by 18% in 2025, filling supply gaps created by European capacity rationalization. This export momentum highlights China’s cost-competitive scale and growing technical capability in impact modifier production.

Impact Modifiers Industry: Country-Level Strategic Snapshot

Impact Modifiers Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Industry Shift

|

|

United States

|

Asset retention and recycled content mandates

|

Construction PVC, EV battery housings, semiconductors

|

Shift toward acrylic and hybrid modifiers

|

|

India

|

Global acquisitions and recycling regulation

|

Rigid packaging, infrastructure plastics

|

Emergence as global manufacturing hub

|

|

South Korea

|

Automotive quality and EV safety

|

ASA, ABS, flame-retardant plastics

|

Export-oriented specialty modifiers

|

|

Japan

|

Supply stabilization and bio-based innovation

|

Transparent PVC, pharma packaging, composites

|

Core-shell and biodegradable integration

|

|

China

|

Policy-led growth and infrastructure demand

|

Rail systems, engineering plastics

|

Export expansion and scale efficiency

|

Impact Modifiers Market Report Scope

Impact Modifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.7 Billion

|

|

Market Size (2034)

|

$14.2 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Type (Acrylic Impact Modifiers, Acrylonitrile Butadiene Styrene, Methacrylate Butadiene Styrene, Chlorinated Polyethylene, Ethylene Propylene Diene Monomer, Acrylonitrile Styrene Acrylate, Bio-Based Impact Modifiers), By Application (Polyvinyl Chloride, Polyamide, Polybutylene Terephthalate, Polycarbonate & Blends, Engineering Plastics, Thermosetting Resins), By End-User Industry (Construction, Automotive, Packaging, Consumer Goods, Sports & Leisure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Arkema S.A., Kaneka Corporation, LG Chem Ltd., Mitsubishi Chemical Group Corporation, Praana Group, BASF SE, Shandong Gaoxin Chemical Co., Ltd., Wacker Chemie AG, Evonik Industries AG, Formosa Plastics Corporation, Sundow Polymers Co., Ltd., Clariant AG, ADEKA Corporation, Songwon Industrial Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Impact Modifiers Market Segmentation

By Type

- Acrylic Impact Modifiers

- Acrylonitrile Butadiene Styrene

- Methacrylate Butadiene Styrene

- Chlorinated Polyethylene

- Ethylene Propylene Diene Monomer

- Acrylonitrile Styrene Acrylate

- Bio-Based Impact Modifiers

By Application

- Polyvinyl Chloride

- Polyamide

- Polybutylene Terephthalate

- Polycarbonate & Blends

- Engineering Plastics

- Thermosetting Resins

By End-User Industry

- Construction

- Automotive

- Packaging

- Consumer Goods

- Sports & Leisure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Impact Modifiers Industry

- Dow Inc.

- Arkema S.A.

- Kaneka Corporation

- LG Chem Ltd.

- Mitsubishi Chemical Group Corporation

- Praana Group

- BASF SE

- Shandong Gaoxin Chemical Co., Ltd.

- Wacker Chemie AG

- Evonik Industries AG

- Formosa Plastics Corporation

- Sundow Polymers Co., Ltd.

- Clariant AG

- ADEKA Corporation

- Songwon Industrial Co., Ltd.

*- List not Exhaustive