Market Overview: Anti Fog Lidding Film Market to Reach $1,617.5 Million by 2034 as Recyclable Mono-Materials, MAP-Compatible Barriers, and PCR Content Redefine Food Packaging

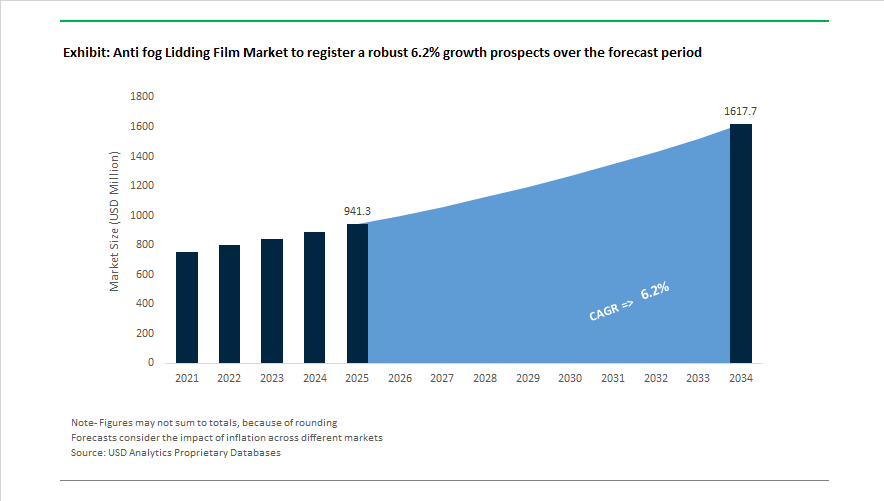

The global anti fog lidding film market is projected to expand from $941.3 Million in 2025 to $1,617.5 Million by 2034, advancing at a 6.2% CAGR. Growth is driven by rising demand for high-clarity food packaging, modified atmosphere packaging (MAP) films, recyclable mono-material lidding, and condensation-resistant tray seals across fresh produce, meat, dairy, ready meals, and premium pet food. Anti-fog lidding films maintain product visibility by preventing droplet formation under temperature fluctuations common in refrigerated retail chains. Market dynamics are shaped by the transition to mono-PET and mono-PP structures, PCR-integrated food-contact films, compostable bio-based lidding materials, and thinner co-extruded barrier films designed for high-speed automated filling lines. Sustainability mandates, extended shelf-life requirements, and reduced sealing energy consumption remain central to product development strategies.

Material innovation accelerated in August 2024 as Profol launched PVC-free high-clarity film technology. Recyclability milestones followed in March 2025 when Mondi introduced compostable lidding for organic produce, and in April 2025 when Jindal Films demonstrated recyclable mono-PP barrier lidding. In May 2025, Klöckner Pentaplast launched 30% PCR-content lidding films maintaining anti-fog performance. Energy-efficient processing innovations emerged in June 2025 as KM Packaging introduced low-temperature sealing mono-PET films. Retail-focused solutions expanded in July 2025 when Sealed Air unveiled Cryovac anti-fog films engineered for condensation control in open display refrigeration.

Barrier performance enhancements continued in August 2025 with Amcor launching high-barrier easy-peel MAP-compatible films, while Constantia Flexibles strengthened UK lidding capabilities through the acquisition of FFP Packaging Solutions. Specialty segment expansion appeared in December 2025 as Cosmo Films introduced high-heat-resistant BOPET lidding for premium pet food. Infrastructure investments were confirmed in February 2025 by Coveris, expanding sustainable extrusion capacity for thinner multi-layer films. Industry consolidation peaked in November 2025 when Amcor completed its acquisition of Berry Global, creating one of the largest global suppliers of anti-fog flexible packaging.

Trends and Opportunities Transforming the Anti Fog Lidding Film Market

Mono-material PET Lidding Becomes the Compliance Standard for Circular Food Packaging

The Anti Fog Lidding Film Market is being structurally reshaped by EU Packaging and Packaging Waste Regulation (PPWR) enforcement, which requires brands to transition from multi-material, low-recyclability laminates toward mono-material PET formats with built-in anti fog systems. Under the PPWR recyclability grading system (2025–2030), all EU-marketed packaging must achieve an A–C recyclability score by 2030. PET-only lidding films are the fastest route to compliance because they eliminate composite PE-PET separations during waste sorting. A relevant market example is Klöckner Pentaplast’s kp MonoSeal®, a mono-PET lidding substrate that reduces total packaging weight by 15%, features high-clarity anti fog finish, and is the first rigid PET film endorsed by Petcore Europe for circularity at industrial scale.

Another regulatory force is PFAS phase-out for food contact, effective August 2026, which enforces <25 ppb for any single PFAS in packaging. Because legacy anti-fog coatings often rely on fluorine chemistry, there is accelerated adoption of silicon-free and fluorine-free internal additives, often derived from bio-based surfactants and vegetable-oil esters. Financial pressure is also driving change. In the UK and EU, plastic taxes averaging £210 per tonne on non-recycled content are pushing converters to incorporate ≥30% PCR PET while relying on anti fog additives to preserve transparency, which is essential for supermarket merchandising and maintaining "fresh visual appeal" for salads and cut produce.

Barrier-Integrated Anti Fog Films Expand in Premium Fresh Food and MAP Segments

High-barrier anti fog lidding films are emerging as premium-price products because they directly reduce food waste in fresh-ready retail categories. Leading producers in 2025 are combining EVOH oxygen barriers with co-extruded permanent anti fog coatings, enabling up to 20% shelf-life extension for proteins, salads, herbs, or superfruits. This performance is especially relevant for Modified Atmosphere Packaging (MAP) applications. If fogging occurs, MAP gas cannot efficiently circulate, which leads to wilting of cut greens, pinking in plant-based meats, or accelerated spoilage. By eliminating droplet formation, anti fog surfaces enable full O₂/CO₂ mixture contact, maximizing respiration control and reducing shrink-related retail losses. Retailers including Tesco and Carrefour have stated that shoppers are 40% less likely to purchase a product when condensation prevents visual inspection, making fog-free clarity not only a packaging specification but a conversion KPI for high-turnover foods.

Market Opportunities Unlocking Long-Term Commercial Scale

Sterilization-Resistant Anti Fog Lidding Films for Medical Device Packaging

Outside food packaging, a major growth avenue lies in medical-grade sterile kits and diagnostic trays, where lidding films must maintain optical clarity during sterilization cycles. Regulatory frameworks are shifting away from legacy EtO sterilization toward Vaporized Hydrogen Peroxide (VHP) and Ozone gas. New PET-based lidding films tested in August 2025 showed zero anti fog degradation after three VHP cycles, which is crucial because printed instructions and reaction indicators must remain readable through the sealed film. Validation under ISO 11607-1:2019 and ASTM F1980-21 accelerated aging now requires that anti fog additives do not migrate or weaken the sterile barrier across a 3–5 year shelf-life, positioning medical-grade anti fog films as a specialized high-value SKU tied to hospital procurement budgets and expanding point-of-care diagnostic demand.

Smart Moisture-Regulating Lidding Films for Plant-Based Protein Packaging

The fastest-growing niche application is plant-based meat alternatives, which require controlled water vapor balance and visual transparency. Supply-chain temperature shifts cause “exudate” release that leads to visible milky fogging on standard films. Manufacturers are now piloting micro-perforated PET with integrated anti fog coatings, specifically engineered to manage moisture flux and prevent condensation buildup. Research published December 2025 confirms that fog-free films help maintain the pink-red "bloom" color of plant-based beef, improving consumer willingness to purchase. To align packaging ethics with vegan consumers, suppliers are introducing bio-based PET and PLA-based lidding films using vegetable-oil-derived sorbitan ester anti fog additives, enabling fully bio-based packaging systems for plant-based SKUs.

Anti-Fog Lidding Film Market Share and Segmentation Insights

Market Share by Material Type: Polyethylene Leads Volume While Bio-Based Films Accelerate Regulatory-Driven Adoption

Polyethylene (PE) accounts for approximately 32% of the global anti-fog lidding film market in 2025, retaining leadership due to low cost, excellent heat-sealing performance, and broad adoption in fresh produce and meat packaging. Polypropylene (PP) follows, gaining traction in microwavable trays where higher temperature resistance and improved clarity are required. Polyethylene terephthalate (PET) serves premium modified atmosphere packaging (MAP) applications, valued for rigidity and superior transparency in retail-ready displays. Ethylene vinyl alcohol (EVOH) is rarely used alone but plays a critical role as a high-oxygen barrier layer in multilayer anti-fog structures, extending shelf life for protein and fresh-cut foods. Polyamide supports mechanical strength in co-extruded films. Bio-based and compostable polymers represent the fastest-growing segment, driven by EU and North American single-use plastic regulations, pushing converters toward recyclable mono-material PE/PP and sustainable anti-fog formulations despite higher material costs.

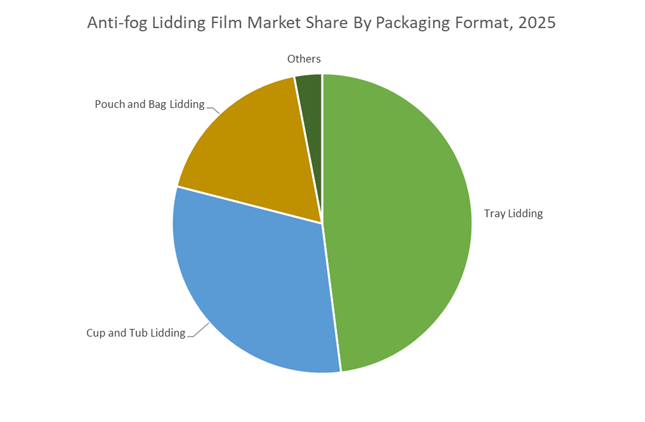

Market Share by Packaging Format: Tray Lidding Dominates as Fresh Food Visibility Becomes Mission-Critical

Tray lidding represents roughly 48% of anti-fog lidding film demand in 2025, making it the dominant packaging format across fresh red meat, poultry, and ready meals. Retailers increasingly specify high-clarity, anti-condensation films to maintain product visibility in chilled cabinets and reduce perceived spoilage. Cup and tub lidding ranks second, supported by dairy applications such as yogurt and cream, alongside single-serve coffee, where anti-fog performance is essential for brand presentation and impulse purchase. Pouch and bag lidding is an emerging growth area, fueled by stand-up pouches for fresh-cut produce and seafood, although penetration remains lower than rigid formats. Across all formats, the core technical requirement is consistent prevention of water droplet formation, which otherwise obscures contents and creates moisture conditions that accelerate bacterial growth. Rising e-grocery penetration and extended cold-chain distribution are further intensifying performance specifications.

Anti Fog Lidding Film Market Competitive Landscape

The global anti fog lidding film market is becoming increasingly competitive as food processors, healthcare packagers, and ready-meal brands accelerate adoption of recyclable mono-material films, high-clarity packaging, and smart anti-fog technologies. Market leaders are investing heavily in sustainable barrier coatings, PCR-enabled structures, and easy-peel sealing systems to meet tightening ESG regulations and rising consumer demand for transparent, shelf-ready packaging. Innovation is concentrated around mono-PE and mono-PP lidding films, EVOH-based barriers, digital traceability, and anti-fog solutions compatible with modified atmosphere packaging (MAP). Strategic M&A, R&D centers of excellence, and lifecycle assessment tools are reshaping supplier positioning across North America, Europe, and Asia-Pacific.

Global scale and mono-material innovation define Amcor plc’s leadership

Amcor has emerged as the world’s largest packaging company following its 2025 merger with Berry Global, bringing unmatched R&D scale to anti fog lidding film development. Its AmPrima™ Plus mono-PE lidding films deliver over 95% recycling stream compatibility while maintaining high-gloss clarity for refrigerated protein trays. In 2025–2026, Amcor launched a Global Centre of Excellence for medical and healthcare lidding and introduced the Lift-Off Winter Challenge to advance nature-based anti-fog barriers. Through its Amcor ASSET™ life cycle assessment platform, customers receive real-time carbon footprint data, directly supporting 2030 ESG targets across fresh food, medical packaging, and sustainable flexible film applications.

Case-ready protein dominance strengthens SEE’s smart lidding portfolio

SEE continues to lead the case-ready meat segment through its CRYOVAC® platform, combining shelf-life extension with advanced anti-fog technology. The 2025 launch of CRYOVAC® LID39ZAP introduced an ultra-thin 39-micron mono-PP lidding film capable of autoclave pasteurization without losing fog resistance. SEE differentiates with self-venting micro-perforations that enable microwave heating while preventing condensation. Its MultiSeal® FlexLOK™ resealable films retain anti-fog performance after repeated openings. Looking ahead, SEE is embedding QR codes and NFC tags directly into lidding films, advancing smart packaging and food traceability without compromising product visibility.

Recyclable-by-design solutions position Mondi Group at the sustainability frontier

Mondi is redefining anti fog lidding film through its re/loop portfolio, featuring PE-based structures with up to 30% post-consumer recycled content while maintaining high oxygen and WVTR barriers. Recognized with multiple WorldStar Awards in 2026, Mondi is also scaling paper-based lidding with aqueous anti-fog coatings that preserve repulpability. Its strategy includes transitioning away from PE where possible and integrating fiber-and-film hybrid packaging via its new Duino recycled containerboard mill. Mondi’s high-barrier technical films support chilled food, lamination, and recyclable MAP applications, reinforcing its leadership in circular flexible packaging.

Easy-peel engineering drives Constantia Flexibles’s dairy and pharma growth

Constantia Flexibles specializes in premium anti fog lidding for dairy desserts and pharmaceutical packaging, anchored by its AluPET® and EcoLam product lines. The company combines rotogravure and flexo printing with anti-fog windows to deliver both shelf impact and clarity. Recent asset acquisitions expanded its Asia-Pacific ready-meal footprint, addressing humid climate performance requirements. Constantia excels in easy-peel sealant chemistry, ensuring clean release across PE, PP, and PET trays. Its Alu-free microwave-safe lidding delivers aluminum-like puncture resistance with plastic transparency, positioning Constantia as a technical benchmark in high-barrier lidding films.

Digital recycling and ultra-thin films distinguish Wipak Group in Europe

Wipak is advancing carbon-neutral packaging ambitions with its GreenChoice portfolio of ultra-thin anti-fog lidding films, reducing material usage by up to 40%. In 2025, Wipak integrated Digimarc digital watermarking, enabling automated sorting of food-grade films at recycling facilities. The company also pioneers “paper-touch” outer layers paired with clear anti-fog windows for premium visual appeal. Through its co-creation R&D model, customers validate anti-fog performance directly on thermoforming lines before commercialization. Wipak’s focus on lightweighting, digital traceability, and tactile design reinforces its role as a sustainability-driven innovator.

Integrated MAP systems anchor Winpak Ltd.’s North American presence

Winpak delivers turnkey anti fog lidding solutions through its expanded MAPfresh® tray and lid program, supporting fresh meat and poultry processors with integrated modified atmosphere systems. Its 1 Mil and 2 Mil shrink lidding films provide drum-tight clarity for non-printed packs where product visibility drives sales. Winpak’s high puncture resistance technology addresses bone-in protein applications, maintaining fog-free performance under stress. In 2026, the company introduced EVOH-barrier eco films that eliminate PVDC coatings, aligning with environmental regulations while preserving shelf life. Winpak’s machinery-film integration model strengthens operational efficiency across North American protein packaging.

India Anti Fog Lidding Film Market: High-Heat Performance and Monomaterial Compliance Drive Domestic Leadership

India has emerged as a fast-scaling manufacturing hub for anti-fog lidding films, supported by industrial expansion and targeted government incentives. In late 2025, Cosmo Films commissioned a new high-performance production line dedicated to anti-fog transparent BOPET lidding films. These films are engineered to withstand sterilization-intensive processing while maintaining optical clarity, directly addressing demand from the pet food and ready-to-eat segments that require thermal stability and condensation control.

Policy support has further accelerated capacity build-out. Under the PLI Scheme 2.0, capital allocation toward high-tech polymer processing has strengthened India’s position in export-grade seafood and meat packaging. Complementing this, Vishakha Group expanded its multi-layer co-extrusion capabilities in 2025, introducing 9-layer and 11-layer high-barrier structures with integrated anti-fog functionality for dairy and fresh produce. Regulatory updates to India’s Plastic Waste Management Rules in 2025 have also shifted demand toward monomaterial PE anti-fog lidding, enabling full recyclability within existing domestic waste streams and reinforcing India’s alignment with circular packaging frameworks.

United States Anti Fog Lidding Film Market: Recycle-Ready Innovation and MAP Functionality Redefine Value

The United States anti fog lidding film market is advancing through sustainability-driven reformulation and enhanced consumer functionality. In 2025, Sealed Air expanded its CRYOVAC® range of recycle-ready anti-fog lidding films, including the Lid 1050 series designed for RIC4 store drop-off recycling. These developments directly respond to consumer and retailer pressure for visible, condensation-free packaging that remains compatible with established recycling pathways.

Technology integration in modified atmosphere packaging has also intensified. Multi-reseal solutions such as Multi-Seal® FlexLOK™ introduced in 2025 combine anti-fog performance with easy-open and reseal functionality, particularly for fresh protein packaging. Sustainability commitments are influencing manufacturing operations as well. Winpak Ltd. received Science Based Targets initiative approval in September 2025, shaping process optimization and material selection for its recycle-ready thermoforming lidding films. Across the U.S., converting facilities have increased investment in automation and predictive analytics to ensure consistent anti-fog coating application on thin-gauge polyester substrates.

Australia Anti Fog Lidding Film Market: Amcor’s Strategic Push Toward Nature-Based and PCR Films

Australia’s influence in the anti fog lidding film industry is closely linked to the global strategy of Amcor, which continues to steer material innovation across regions. In November 2025, Amcor launched the Lift-Off Winter 2025/26 Challenge, allocating funding to start-ups developing nature-based barrier additives and compostable adhesives suitable for anti-fog film formulations. This initiative signals a shift toward biologically derived performance enhancers that can meet food-contact and clarity requirements.

Material science advancements were further highlighted in Amcor’s FY25 Sustainability Report, which confirmed the commercialization of specialty film packs containing 100% post-consumer recycled content. This development lays the groundwork for integrating recycled resins into anti-fog lidding layers by 2026. Australian firms have also taken a leadership role in eliminating PFAS from food-contact materials, aligning anti-fog and grease-resistant layers with evolving global mandates to remove persistent chemicals from packaging supply chains.

China Anti Fog Lidding Film Market: Verbund Resin Supply and Export-Oriented Sustainability Standards

China’s role in the anti fog lidding film value chain is increasingly defined by integrated resin supply and export-focused sustainability compliance. The BASF Zhanjiang Verbund site, scaling through 2025–2026, has begun supplying high-purity polyethylene and polyamide resins optimized for high-clarity, low-condensation lidding applications serving East Asian food packaging markets. Localized resin availability strengthens supply security for converters focused on optical performance and seal integrity.

Export momentum is being driven by sustainability benchmarking. Jiangsu Qianrun New Material Technology expanded its low-OTR anti-fog lidding portfolio in 2025, targeting European buyers operating under stringent Green Deal requirements. These developments reflect China’s strategic emphasis on combining scale efficiency with compliance-ready film structures suitable for international food packaging standards.

Strategic Positioning in the Anti-Fog Lidding Film Industry

Anti-Fog Lidding Film Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Industry Implication

|

|

India

|

High-heat BOPET, monomaterial PE compliance

|

Export-ready, recyclable lidding for RTE and pet food

|

|

United States

|

Recycle-ready films and MAP reseal innovation

|

Consumer convenience with regulatory alignment

|

|

Australia / Global

|

Nature-based additives and PCR integration

|

Next-generation sustainable lidding platforms

|

|

China

|

Verbund resin supply and low-OTR exports

|

Scale efficiency with EU-compliant film structures

|

Anti-Fog Lidding Film Market Report Scope

Anti fog Lidding Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$941.3 Million

|

|

Market Size (2034)

|

$1617.5 Million

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polyamide, Ethylene Vinyl Alcohol, Bio Based and Compostable Polymers), By Sealing Type (Peelable, Weld Seal, Resealable), By Application (Fresh Produce, Meat Poultry and Seafood, Dairy Products, Ready to Eat Foods, Frozen Foods), By Packaging Format (Tray Lidding, Cup and Tub Lidding, Pouch and Bag Lidding), By Technology (Co Extrusion, Extrusion Coating, Solvent and Aqueous Coating, Nanotechnology Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group Inc, Sealed Air Corporation, Mondi plc, Huhtamaki Oyj, Constantia Flexibles, Winpak Ltd, Cosmo Films Ltd, Coveris Holdings SA, Sonoco Products Company, Wipak Group, Uflex Ltd, Jiangsu Qianrun New Material Technology, KM Packaging Services Ltd, Vishakha Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Fog Lidding Film Market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Polyamide

- Ethylene Vinyl Alcohol

- Bio Based and Compostable Polymers

By Sealing Type

- Peelable

- Weld Seal

- Resealable

By Application

- Fresh Produce

- Meat Poultry and Seafood

- Dairy Products

- Ready to Eat Foods

- Frozen Foods

By Packaging Format

- Tray Lidding

- Cup and Tub Lidding

- Pouch and Bag Lidding

By Technology

- Co Extrusion

- Extrusion Coating

- Solvent and Aqueous Coating

- Nanotechnology Coatings

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Fog Lidding Film Industry

- Amcor plc

- Berry Global Group Inc

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- Constantia Flexibles

- Winpak Ltd

- Cosmo Films Ltd

- Coveris Holdings SA

- Sonoco Products Company

- Wipak Group

- Uflex Ltd

- Jiangsu Qianrun New Material Technology

- KM Packaging Services Ltd

- Vishakha Group

*- List not Exhaustive