Paints and Coatings Market Size, Industry Consolidation, and Performance Coating Evolution

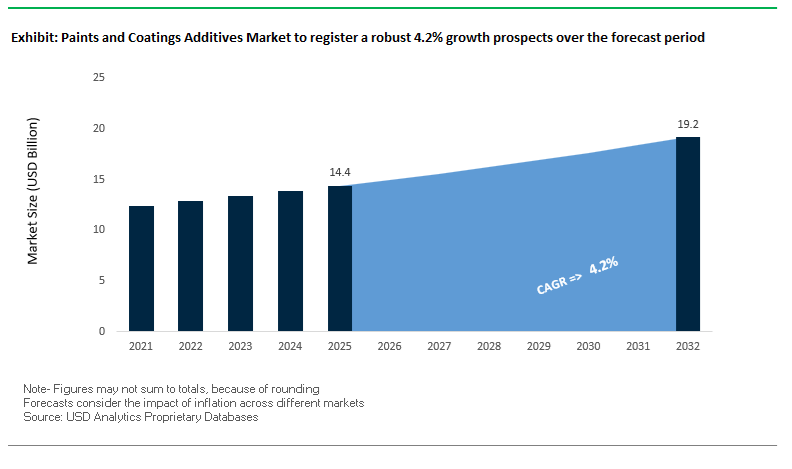

The global Paints and Coatings Market was valued at $206.9 billion in 2025 and is projected to grow at a CAGR of 4.2% through 2032, reaching $276 billion by 2032. This growth reflects sustained demand across construction, automotive, marine, aerospace, and industrial manufacturing, where coatings play a critical role in surface protection, durability, and functional enhancement.

A defining structural shift in the market is the increasing emphasis on high-performance, environmentally compliant coating systems, particularly waterborne, powder, and UV-curable technologies. Regulatory frameworks targeting VOC emissions, hazardous substances, and lifecycle sustainability are reshaping formulation strategies, pushing manufacturers toward low-emission, energy-efficient coating solutions. At the same time, the market is witnessing rising demand for coatings with advanced functionalities, including anti-corrosion, anti-fouling, UV resistance, and self-healing properties, particularly in infrastructure and energy applications.

Another key driver is the continued expansion of urbanization, infrastructure development, and industrial output, particularly in Asia-Pacific and Latin America. Decorative coatings remain volume-driven, but growth is increasingly concentrated in industrial and specialty coatings, where margins are higher and technical complexity is greater. Additionally, the emergence of smart coatings and digital monitoring systems is redefining value propositions, transforming coatings from passive materials into active performance systems capable of predictive maintenance and lifecycle optimization.

The market is also undergoing significant structural realignment, with major players optimizing portfolios, divesting non-core assets, and focusing on high-margin segments and regional growth opportunities. This consolidation trend is reshaping competitive dynamics and accelerating innovation across both product development and business models.

Market Analysis: Strategic Divestments, and Smart Coating Technologies Driving Market Transformation

Recent developments highlight a period of intense consolidation, strategic repositioning, and technological innovation in the global paints and coatings industry. The most significant event is the November 2025 merger agreement between AkzoNobel and Axalta Coating Systems, forming a coatings giant with an estimated enterprise value of $25 billion. Expected to close in late 2026, this merger will create a highly diversified entity spanning decorative, automotive, and industrial coatings, with dual headquarters in Amsterdam and Philadelphia.

In parallel, BASF’s €7.7 billion divestment of its global coatings division (October 2025) to Carlyle and the Qatar Investment Authority marks a strategic exit from downstream coatings, allowing BASF to concentrate on core chemical production and upstream value chains. Similarly, PPG Industries’ sale of its North American decorative business, rebranded as Pittsburgh Paints, reflects a broader industry trend toward portfolio rationalization and focus on high-performance coatings segments.

Strategic acquisitions and regional expansion remain key growth levers. Sherwin-Williams’ integration of Suvinil (January 2026) has strengthened its leadership in the Latin American decorative coatings market, while Kansai Nerolac’s amalgamation with Nerofix (February 2026) expands its footprint in construction chemicals and adhesives, diversifying beyond traditional paints.

Innovation in product technology is also accelerating. Jotun’s launch of smart coatings (January 2026) introduces real-time monitoring capabilities, enabling early detection of corrosion and reducing maintenance costs for offshore and industrial assets. Meanwhile, PPG’s AQUACRON WSP water-based shop primers (March 2026) address growing regulatory pressure by offering low-VOC, fast-drying, and corrosion-resistant solutions for structural steel applications.

Corporate restructuring is further shaping regional dynamics. AkzoNobel’s divestment of its Indian decorative business to JSW Group (October 2025) aligns with its strategy to streamline operations and improve profitability, while Hempel’s “Accelerate to Win” strategy (January 2026) underscores a sharpened focus on marine and energy coatings, sectors characterized by strong growth and high technical requirements.

Market Trend: Bio-Carbon Alkyd-Acrylic Hybrid Coatings Advancing Sustainable Architectural Paint Performance

The paints and coatings industry is undergoing a strategic shift toward bio-based formulations, with alkyd-acrylic hybrid coatings emerging as a leading solution in the architectural segment. This transition reflects a broader movement from basic low-VOC compliance toward measurable bio-carbon content and lifecycle sustainability. By integrating renewable fatty acids into acrylic polymer backbones, these hybrid coatings deliver a balance of durability, gloss retention, and environmental performance that traditional solvent-borne alkyd systems cannot achieve.

Modern bio-carbon hybrid resins are reaching biogenic carbon content levels of 35% to 50%, verified through ASTM D6866 testing. This represents a significant advancement over the historical benchmark of approximately 20% for green coatings, enabling manufacturers to differentiate products based on quantifiable sustainability metrics. At the same time, these systems maintain strong application performance. Advanced formulations achieve a Minimum Film Forming Temperature below 5°C without relying on coalescing solvents, allowing for zero-VOC labeling while preserving the leveling and flow characteristics associated with oil-based paints.

Durability is another key advantage driving adoption. In standardized scrub and abrasion testing, alkyd-acrylic hybrids demonstrate approximately 25% higher resistance compared to conventional 100% acrylic coatings. This enhanced surface hardness bridges the performance gap between waterborne coatings and traditional alkyd systems, making them suitable for high-traffic interior and exterior applications. The combination of sustainability, performance, and regulatory alignment is positioning bio-carbon hybrid coatings as a core innovation in architectural coatings.

Market Trend: Ultra-High Solids Epoxy Coatings Enhancing Industrial Protection Efficiency and Reducing VOC Emissions

Industrial coatings are rapidly transitioning toward ultra-high solids epoxy systems as manufacturers seek to reduce solvent usage, improve application efficiency, and comply with increasingly stringent environmental regulations. These coatings, with solids content exceeding 90%, are designed for high-build, single-coat applications that streamline maintenance processes and improve lifecycle performance in infrastructure, marine, and heavy equipment sectors.

Ultra-high solids epoxy coatings provide significant volumetric efficiency advantages. With nearly double the coverage per gallon compared to conventional 50% solids systems, these coatings reduce material consumption, transportation requirements, and storage needs by approximately 45%. This efficiency is particularly valuable in large-scale industrial projects where logistics and application speed are critical.

Application flexibility has also improved with the development of advanced surface chemistry. New-generation ultra-high solids epoxies incorporate chemically active additives that extend recoat windows up to 21 days without the need for mechanical surface preparation. This represents a substantial improvement over legacy system, which typically require recoating within 24 to 48 hours or necessitate additional surface treatment.

Environmental performance is a central driver of adoption. By utilizing reactive diluents instead of traditional solvents, these coatings maintain VOC levels below 100 g/L, enabling compliance with strict air quality regulations across global markets. The combination of high efficiency, extended service intervals, and low emissions is positioning ultra-high solids epoxy coatings as a preferred solution for industrial protective applications.

Market Opportunity: EPA NESHAP 2026 Revision Driving Demand for Low-HAP and Waterborne Coating Technologies

The 2026 revision of the US EPA National Emission Standards for Hazardous Air Pollutants for miscellaneous coating operations is creating a significant regulatory-driven opportunity in the paints and coatings industry. The updated rule eliminates exemptions for startup, shutdown, and malfunction conditions, requiring continuous compliance with HAP control efficiencies exceeding 95%.

This regulatory shift is forcing coating manufacturers and OEMs to transition toward low-HAP and waterborne coating systems that can maintain consistent emissions performance under all operating conditions. Coatings with total HAP content below 1% by weight are increasingly preferred, as they simplify compliance and reduce the need for costly emission control systems such as regenerative thermal oxidizers.

The introduction of mandatory electronic reporting through the Compliance and Emissions Data Reporting Interface is further increasing transparency and regulatory oversight. This is driving demand for pre-certified coating systems with verified emissions data, enabling manufacturers to streamline compliance processes and reduce audit complexity. As regulatory enforcement intensifies, suppliers offering compliant, high-performance coatings are expected to capture increased market share.

Market Opportunity: China VOC Phase 4 Regulations Accelerating Adoption of Low-VOC and Heavy-Metal-Free Coatings

China’s Phase 4 VOC Action Plan is creating a large-scale transformation in the paints and coatings market through the implementation of mandatory standards for both architectural and industrial coatings. The introduction of GB 30981.1-2025 and GB 30981.2-2025 establishes some of the most stringent VOC limits globally, driving a rapid transition toward environmentally compliant coating technologies.

Under these standards, water-based industrial coatings must maintain VOC levels below 200 g/L to qualify for green development incentives, particularly in key manufacturing regions such as the Yangtze River Delta. This requirement is accelerating the adoption of advanced waterborne and high-solids coatings that meet both performance and regulatory criteria.

The regulations also introduce strict limits on hazardous substances, including a maximum lead content of 90 mg/kg, aligning Chinese standards with European REACH requirements. This effectively eliminates legacy additive systems and creates a significant replacement market for compliant alternatives, benefiting suppliers with advanced formulation capabilities.

Enforcement mechanisms further reinforce this transition. High-VOC coatings are now subject to environmental consumption taxes, increasing their cost by 10% to 15% compared to low-VOC or powder-based alternatives. This economic pressure is driving rapid adoption of sustainable coatings across industrial and architectural applications, positioning China as a key growth driver in the global paints and coatings industry.

Paints and Coatings Market Share and Segmentation Insights

Topcoats Capture 35.4% Share Driven by Surface Protection, Aesthetics, and High Recoat Volumes

The paints and coatings market by product layer is dominated by topcoats, accounting for 35.4% of the global market share in 2025, due to their dual role in surface protection and visual enhancement. Topcoats act as the primary barrier against UV radiation, moisture, chemicals, and abrasion, while delivering the final gloss, color depth, and finish quality across automotive, architectural, and industrial coating systems. Their dominance is further reinforced by high demand in refinish, maintenance, and repaint applications, where only topcoats are reapplied over existing coatings, significantly increasing consumption volumes compared to primers or basecoats. As industries prioritize durability, weather resistance, and aesthetic performance, topcoats remain the most critical and widely used layer in the global coatings market.

Low-VOC Segment Holds 52.6% Share Driven by Environmental Regulations and Balanced Cost-Performance

In the paints and coatings market by VOC content, low-VOC coatings lead with a 52.6% market share in 2025, reflecting their status as the global regulatory standard. Stringent environmental regulations such as EPA (USA), REACH (EU), and China GB standards have mandated the adoption of coatings with VOC levels below 250 g/L for architectural and 420 g/L for industrial applications, making low-VOC formulations the baseline across major markets. These coatings—primarily waterborne acrylics, high-solids epoxies, and advanced polyurethane systems—offer an optimal balance between environmental compliance, application performance (flow, leveling, drying time), and cost efficiency. While zero-VOC coatings are gaining traction, their higher cost limits widespread adoption. As sustainability and regulatory pressures intensify, low-VOC coatings continue to dominate the global paints and coatings market.

Competitive Landscape of the Paints and Coatings Market

AkzoNobel Strengthens Market Leadership with Strategic Portfolio Optimization and Merger Plans

AkzoNobel N.V. continues to lead the global paints and coatings market through its focus on industrial excellence and margin expansion strategies. In Q1 2026, the company reported adjusted EBITDA of €345 million, achieving a 14.5% margin following an 80 bps increase, supported by a 9% revenue optimization after divesting assets in Pakistan and India. Its planned merger with Axalta is expected to create a major global coatings powerhouse, enhancing scale and efficiency. AkzoNobel’s 2026 “Rhythm of Blues” color innovation initiative targets key industries such as aerospace and automotive. Additionally, its shift toward 100% VOC-compliant waterborne and powder coatings reinforces its leadership in sustainable coatings.

PPG Expands Global Coatings Dominance Through Aerospace Investments and EV Innovations

PPG Industries, Inc. is a dominant player in the industrial coatings and specialty coatings market, leveraging its extensive R&D capabilities. In 2026, the company announced a $300 million investment to modernize aerospace manufacturing, targeting growth in aviation coatings and sealants. Its acquisition of Ozark Materials strengthens its infrastructure coatings portfolio, particularly in traffic safety applications. PPG is also expanding production of EV battery coatings, utilizing advanced cathode binder technologies to eliminate toxic solvents. With analysts forecasting an 8–12% EPS CAGR, supported by over $500 million in annual R&D investment, PPG continues to lead in high-performance coatings and next-generation mobility solutions.

Sherwin-Williams Drives Growth with Strong Financial Performance and Digital Coating Solutions

The Sherwin-Williams Company maintains a leading position in the North American paints and coatings market, supported by its extensive retail network and strong Performance Coatings Group. In Q1 2026, the company reported record net sales of $5.67 billion, reflecting 6.8% year-over-year growth, with significant contributions from its Consumer Brands segment. It reaffirmed full-year EPS guidance of $11.50–$11.90 despite challenging macroeconomic conditions. Sherwin-Williams is leveraging its “Success by Design” digital platform to automate coating specifications for large-scale infrastructure projects. Its strong cash flow and shareholder returns further highlight its financial resilience and leadership in architectural and industrial coatings.

Nippon Paint Accelerates APAC Growth Through Strategic Expansion and Strong Financial Gains

Nippon Paint Holdings Co., Ltd. is a major force in the Asia-Pacific paints and coatings market, driven by its aggressive growth strategy and strong regional presence. In FY 2025/2026, the company reported a 44.6% increase in operating profit in Japan, supported by recovery in automotive production and effective pricing strategies. Its China operations also delivered strong volume growth in decorative coatings, contributing significantly to overall revenue. Nippon Paint continues to expand through strategic acquisitions, including Cromology and JUB, while focusing on adjacent businesses such as construction chemicals and adhesives. This diversification strengthens its position in the global coatings ecosystem.

Axalta Drives Innovation in Mobility Coatings with AI and Advanced Color Technologies

Axalta Coating Systems Ltd. is a global leader in refinish and mobility coatings, positioning itself as an innovation-driven company ahead of its merger with AkzoNobel. In 2026, Axalta won three Edison Awards for technologies such as EcoNextJet™, Alesta® e-PRO, and TintMaster AI, highlighting its leadership in AI-powered coating solutions and EV safety coatings. Its TintMaster AI platform improves manufacturing efficiency by up to 29%, reducing waste and cycle times. The company’s global reach spans over 100,000 customers in 140 countries, with strong demand in automotive refinish and commercial coatings. Axalta’s focus on advanced color customization and high-performance coatings strengthens its competitive edge.

BASF Strengthens Coatings Innovation with Sustainable Dispersions and Advanced Color Technologies

BASF SE continues to lead innovation in the global paints and coatings market, leveraging its expertise in chemical engineering and material science. In 2026, the company expanded its dispersions production capacity in India to support growing demand for sustainable coatings in emerging markets. Its “Driving the Proxy” color trends showcase advanced interference pigments that deliver multi-dimensional surface aesthetics. BASF is also transitioning its architectural coatings portfolio toward low-VOC, low-odor dispersions aligned with green building standards. By leveraging its global innovation network, BASF is redefining coatings with functional, sustainable, and high-performance solutions across multiple industries.

China Paints and Coatings Market: Functional Innovation and Maritime Dominance

China has evolved into the global hub for advanced functional and maritime coatings, leveraging its leadership in shipbuilding, EVs, and semiconductor manufacturing. The country’s dominance in vessel construction is driving strong demand for anti-fouling and anti-corrosive marine coatings, aligned with both GB 4806.10-2025 standards and international environmental regulations.

Technological advancements include PACVD-compatible high-purity resins for semiconductor fabrication, supporting domestic FinFET node scaling. Innovations such as AkzoNobel’s radiative cooling coatings, capable of reducing surface temperatures by up to 10%, highlight China’s focus on thermal management in urban infrastructure. The rapid growth of the NEV sector is also fueling demand for digitally customized automotive coatings, supported by facilities like PPG’s Tianjin color design studio. Additionally, BASF’s new technical center in Jiangmen is strengthening China’s role as a regional innovation hub, while the scale-up of bio-based polyaspartic resins is advancing sustainability across industrial coatings.

United States Paints and Coatings Market: Regulatory Transformation and Infrastructure-Led Demand

The United States market is undergoing a structural shift toward low-VOC, PFAS-free, and circular-economy coatings, driven by federal funding and environmental regulations. The Infrastructure Investment and Jobs Act (IIJA) is generating massive demand for high-build epoxy and polyurethane coatings, particularly for bridges and rail systems requiring 20-year durability.

Technological innovation includes AI-optimized reflective coatings, which can reduce building surface temperatures by up to 20°C, significantly improving energy efficiency. Waterborne coatings now dominate nearly 67% of the architectural segment, supported by the rapid adoption of HEUR rheology modifiers. The market is also advancing in energy-curable coatings, with PPG’s DURANEXT portfolio eliminating traditional curing ovens. Additionally, the rise of cold-chain pharmaceutical logistics is boosting demand for antimicrobial and anti-fog coatings, reinforcing the U.S. position as a leader in high-performance, sustainable coating solutions.

Germany Paints and Coatings Market: Green Chemistry and Circular Economy Leadership

Germany leads Europe’s paints and coatings market through its focus on sustainability, circular economy integration, and advanced material innovation. Approximately 40% of coating plants are undergoing retrofits to meet stringent VOC thresholds, reflecting strong regulatory enforcement under EU Green Deal initiatives.

The country is driving innovation in bio-based polyols and polyurethane systems, supported by major investments such as Covestro’s €1.5 billion sustainability program. Germany’s expansion in offshore wind infrastructure is fueling demand for coatings capable of withstanding 25-year C5-M corrosive environments. Additionally, advancements in digital tracer technologies are enabling up to 99.5% accuracy in recycling systems, improving material recovery efficiency. The phase-out of chromate-based coatings in aerospace is also accelerating adoption of PACVD-based alternatives, reinforcing Germany’s leadership in sustainable and high-performance coatings.

India Paints and Coatings Market: Rapid Urbanization and Decorative Segment Expansion

India is the fastest-growing paints and coatings market globally, driven by large-scale infrastructure projects and housing initiatives such as Pradhan Mantri Awas Yojana (PMAY-U 2.0). The program’s massive funding is expected to significantly boost demand for architectural acrylics and decorative coatings.

Market dynamics include major consolidation activities, such as JSW Paints’ acquisition of Akzo Nobel India, signaling rapid industry evolution. Innovations in nanotechnology-based self-cleaning coatings are gaining traction in high-rise residential projects, particularly in urban areas with heavy dust exposure. Infrastructure development under the Smart Cities Mission is driving adoption of anti-carbonation coatings for bridges and transit systems. Additionally, the scaling of solar-reflective coatings, which reduce indoor temperatures by up to 5°C, aligns with India’s National Cooling Action Plan, reinforcing sustainable growth.

Japan Paints and Coatings Market: Advanced Materials and EV Synergies

Japan’s paints and coatings market is defined by its leadership in advanced material science and high-performance applications, particularly in electronics and automotive sectors. Innovations such as thermal-reflective coatings for EVs are improving energy efficiency by reducing cabin heat load and extending battery range.

The country is also pioneering photocatalytic coatings, such as ARITERAS KPC, which actively decompose organic pollutants, supporting cleaner indoor environments. Japan leads in biocide-free marine coatings, using hydrophilic resins to prevent fouling without toxic leaching. Regulatory frameworks like the Positive List System are driving the development of ultra-low-migration coatings for food and medical applications. Additionally, advancements in seismic-reinforcement coatings for aging infrastructure highlight Japan’s focus on safety and long-term durability.

Brazil Paints and Coatings Market: Industrial Expansion and Bio-Based Innovation

Brazil is emerging as a key regional player in paints and coatings, driven by growth in agriculture, industrial manufacturing, and aerospace sectors. Expansion projects, such as PPG’s powder coatings plant in Sumaré and WEG’s increased liquid paint capacity, are strengthening domestic production capabilities.

The market is benefiting from strong demand for protective coatings in agro-machinery and heavy transport equipment, as well as high-performance coatings for aerospace applications led by Embraer. Brazil’s leadership in bio-based binders derived from sugarcane is enabling sustainable coating formulations that meet global renewable content targets. Additionally, innovations in UV-resistant coatings are addressing the country’s high solar radiation conditions, ensuring durability in outdoor applications. The expansion of retail distribution channels is also driving adoption of premium decorative coatings among middle-income consumers.

South Korea Paints and Coatings Market: Semiconductor-Driven Precision and High-Tech Applications

South Korea’s paints and coatings market is heavily influenced by its dominance in semiconductors, electronics, and advanced display technologies. The country leads in anti-static (ESD) and EMI-shielding coatings, essential for protecting sensitive electronic components and cleanroom environments.

Technological advancements include thin-film encapsulation (TFE) coatings for OLED displays, enabling durability in foldable devices. South Korea is also pioneering low-voltage PACVD processes (<160V), allowing coatings to be applied on heat-sensitive substrates. Innovations in high-barrier retort coatings are supporting global food packaging applications, while bio-based solutions like Selektope-enabled marine coatings are improving environmental performance. Additionally, the influence of the K-Beauty industry is driving demand for premium tactile coatings with enhanced aesthetics and chemical resistance, reinforcing South Korea’s position in high-tech coatings innovation.

Paints and Coatings Market Report Scope

Paints and Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$206.9 Billion

|

|

Market Size (2032)

|

$276 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Cured, Solvent-free), By Resin Type (Acrylic, Epoxy, Polyurethane, Alkyd, Polyester, Vinyl, Fluoropolymers, Silicones and Silicates, Bio-based, Hybrid Resins), By End-Use Industry (Architectural and Decorative, Automotive and Transportation, General Industrial, Protective Coatings, Industrial Wood, Packaging, Coil and Extrusion, Electronics and Specialty), By Product Layer (Primers and Sealers, Basecoats, Topcoats, Clearcoats, Electrocoats), By Functional (Anti-Corrosive, Anti-Fouling, Intumescent, Self-Cleaning, Anti-Microbial, Thermal Barrier), By VOC Content (Conventional VOC, Low-VOC, Zero-VOC)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., BASF SE, Kansai Paint Co., Ltd., Asian Paints Limited, Jotun A/S, Masco Corporation, Hempel A/S, KCC Corporation, Berger Paints India Limited, Beckers Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paints and Coatings Market Segmentation

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Cured

- Solvent-free

By Resin Type

- Acrylic

- Epoxy

- Polyurethane

- Alkyd

- Polyester

- Vinyl

- Fluoropolymers

- Silicones and Silicates

- Bio-based

- Hybrid Resins

By End-Use Industry

- Architectural and Decorative

- Automotive and Transportation

- General Industrial

- Protective Coatings

- Industrial Wood

- Packaging

- Coil and Extrusion

- Electronics and Specialty

By Product Layer

- Primers and Sealers

- Basecoats

- Topcoats

- Clearcoats

- Electrocoats

By Functional

- Anti-Corrosive

- Anti-Fouling

- Intumescent

- Self-Cleaning

- Anti-Microbial

- Thermal Barrier

By VOC Content

- Conventional VOC

- Low-VOC

- Zero-VOC

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Paints and Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- RPM International Inc.

- Axalta Coating Systems Ltd.

- BASF SE

- Kansai Paint Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- Masco Corporation

- Hempel A/S

- KCC Corporation

- Berger Paints India Limited

- Beckers Group

*- List not Exhaustive