Returnable Transport Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Returnable Transport Packaging Market to Reach $16.2 Billion by 2034 as Cost-Efficiency and Sustainability Drive Adoption

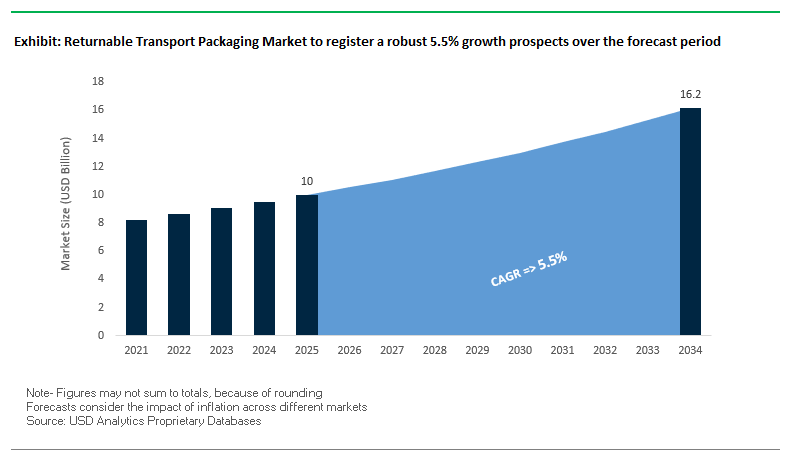

The global returnable transport packaging (RTP) market is projected to grow from $10 billion in 2025 to $16.2 billion by 2034, reflecting a CAGR of 5.5%. Growth is fueled by durable, reusable packaging solutions that optimize logistics, reduce waste, and align with sustainability goals. Industrial, retail, and consumer goods companies increasingly adopt RTP to reduce product damage, improve operational efficiency, and minimize environmental impact.

Key Insights for industry professionals and buyers:

- Cost-Efficiency Over Time: Although initial investment is higher, RTP delivers ROI within 12–18 months and can be up to 60% more cost-effective than single-use packaging over its lifecycle.

- Reduced Product Damage: Durable RTP containers can cut product damage by up to 98%, ensuring valuable goods are protected throughout the supply chain.

- Increased Supply Chain Efficiency: Standardized, durable RTP dimensions support automated handling, reducing manual labor and optimizing warehouse logistics.

- Lower Carbon Footprint: Life-cycle analysis shows up to 60% reduction in CO2 emissions compared to single-use options, supporting corporate sustainability commitments.

- Enhanced Operational Reliability: RTP solutions provide consistent performance, enabling closed-loop operations and reducing reliance on disposable packaging materials.

Returnable transport packaging is a strategic tool for cost reduction and environmental compliance, offering tangible benefits across supply chains while supporting corporate sustainability initiatives.

Market Analysis: Strategic Partnerships and Technological Innovations Are Shaping the Returnable Transport Packaging Market

The RTP market is undergoing rapid transformation through strategic collaborations, acquisitions, and automation. In August 2025, Rehrig Pacific Company partnered with AutoStore, becoming its official U.S. bin manufacturing partner and highlighting the integration of robotic warehouse automation with reusable packaging solutions. During the same month, Nefab Denmark acquired FARUSA Emballage, expanding its sustainable packaging portfolio in the Nordic region. Rehrig Pacific also launched Rehrig Penn Inc. in August 2025 to provide pallet management services, extending its service offerings beyond core plastic manufacturing.

Sustainability-focused innovations continue to influence market dynamics. In June 2025, Schoeller Allibert partnered with Transoplast as a Platinum Partner in the Netherlands, reinforcing its European distribution network. Automated logistics solutions are gaining prominence, exemplified by SSI SCHAEFER’s completion of a semi-automated warehouse for Rossmann in April 2025, which demonstrates the adoption of RTP in optimized intralogistics systems. In March 2025, Schoeller Allibert’s science-based emissions reduction targets were validated by the SBTi, emphasizing the industry’s commitment to environmental stewardship.

Innovative product launches also reflect market evolution. GWP Correx introduced the Rapitainer in November 2024, replacing single-use corrugated boxes with reusable plastic containers. In October 2024, Tri-Wall Circular launched YOYOBin Adjustable, a modular, foldable RTP solution for the automotive sector, addressing both efficiency and sustainability goals.

Returnable Transport Packaging Market: Trends and Opportunities Transforming Circular Logistics

Strategic Shift from Asset Ownership to Pooling and As-a-Service Models

A defining trend in the returnable transport packaging (RTP) market is the transition from asset ownership to pooling and pay-per-use service models. Traditionally, companies bore the full cost of purchasing, maintaining, and managing RTP assets, including pallets, crates, and containers. However, leading providers such as CHEP and Tosca are disrupting this model by offering scalable pooling services. A case study on a major U.S. retailer adopting Tosca’s pooling solutions revealed substantial supply chain cost reductions by eliminating capital expenditures on RTP assets and outsourcing asset management responsibilities. Beyond upfront cost savings, pooling shifts the operational burden—including cleaning, retrieval, repair, and storage—onto the service provider. According to industry analyses, this model reduces “hidden costs” of asset ownership while increasing asset utilization rates, freeing businesses to focus on their core supply chain activities. As regulatory frameworks like the EU Packaging and Packaging Waste Regulation (PPWR) push for more reuse and circularity, pooling-as-a-service models are expected to become the dominant operating framework across industries.

Integration of IoT and RFID for Real-Time Asset Visibility and Optimization

Another transformative trend is the integration of IoT sensors and RFID tags into RTP systems, which is driving real-time visibility and optimized reverse logistics. A 2024 RFID study highlighted that implementation of automated tracking systems reduced asset loss from 15% to as low as 1.5%, representing a drastic improvement in return rates. This directly enhances the economic and environmental efficiency of RTP systems by extending asset lifespans and reducing replacement needs. Going further, IoT-enabled RTP is revolutionizing logistics by providing live data on asset location, dwell times, and fill levels. A 2025 research paper demonstrated how such data allows logistics managers to optimize return routes, minimize empty mileage, and improve turnaround times in reverse logistics chains. By enabling predictive maintenance and supply chain automation, these digital tools transform RTP into data-driven assets, ensuring higher efficiency, transparency, and cost savings across the value chain.

Development of Lightweight, High-Strength Composite and Hybrid Materials

One of the most promising opportunities in RTP lies in the adoption of next-generation composite and hybrid materials. Traditional RTP solutions built from wood, steel, or conventional plastics often create trade-offs between weight and durability. However, innovations in carbon fiber-reinforced composites and advanced polymers offer a new benchmark. A composites industry analysis found that these materials are 70% lighter than steel and 40% lighter than aluminum, delivering significant reductions in transportation emissions and fuel consumption. At the same time, lightweight composites exhibit superior durability and impact resistance, allowing RTP assets to withstand demanding supply chain conditions with fewer repairs or replacements. An article on lightweight pallets further emphasized that such innovations not only lower operating costs but also extend asset lifespans, reinforcing circular economy objectives. By cutting emissions while improving long-term durability, high-performance composites represent a high-value growth segment for RTP manufacturers.

Expansion into New Vertical Markets with Stringent Hygiene and Traceability Needs

The RTP market is also expanding into new verticals that demand higher hygiene, traceability, and specialized protection standards. The pharmaceutical and biotechnology industries are emerging as critical growth areas, with RTP systems engineered to feature tamper-evident seals, sterilizable materials, and RFID-enabled traceability to comply with stringent regulatory requirements for safety and product integrity. Similarly, the aerospace and electronics sectors are adopting RTP solutions designed for high-value, sensitive components. A case study from a specialty packaging company demonstrated the use of static-dissipative RTP systems to prevent electrostatic discharge (ESD) in electronic components while ensuring efficient reverse logistics for reusable containers. These industry-specific adaptations highlight the versatility of RTP in addressing specialized market demands. As global supply chains evolve, the ability of RTP providers to deliver hygienic, traceable, and high-performance reusable packaging will unlock significant opportunities in regulated and high-value sectors.

Competitive Landscape: Leading Returnable Transport Packaging Companies Are Advancing Sustainability, Automation, and Supply Chain Optimization

The global RTP market is competitive, with top players focusing on durable, eco-friendly solutions, integrated services, and operational efficiency. Companies are investing in automation, circular business models, and global expansion to maintain leadership positions.

Schoeller Allibert: Championing Circular Economy and Durable Plastic Solutions in RTP

Schoeller Allibert manufactures returnable plastic crates, foldable large containers (FLCs), pallets, and dollies. Leadership transitions in August and October 2024 brought Alejandro Cabal Uribe as CEO and Kenneth Lynard as CFO. The company has earned an EcoVadis gold rating and had its science-based emissions reduction targets validated by SBTi. Schoeller Allibert’s innovations include pallet boxes made from recycled fishing nets, demonstrating a commitment to circular business models and sustainability-driven solutions.

Rehrig Pacific Company: Integrating Reusable Packaging with Robotic Warehouse Automation

Rehrig Pacific produces sustainable pallets, crates, and roll-out carts. In August 2025, it launched Rehrig Penn Inc., expanding its service offerings, and partnered with AutoStore, entering warehouse automation. The company’s state-of-the-art manufacturing facility in Buckeye, Arizona, opened in October 2024, can be expanded to 500,000 sq. ft. Its high-pressure injection molding expertise ensures durable, reliable RTP products, widely used in beverage, dairy, and retail sectors.

Myers Industries, Inc.: Delivering Long-Lasting Reusable Packaging for Industrial Applications

Myers Industries offers durable RTP products and Akro-Mils platform trucks. Through its Focused Transformation program, the company aims to streamline operations and achieve $20 million in annualized cost savings by 2025. Its rotational molding expertise produces containers that last 10+ years, and the company recycles 99% of manufacturing scrap, reflecting a strong circular economy focus.

SSI SCHAEFER: Pioneering Automated Intralogistics Systems to Optimize RTP Operations

SSI SCHAEFER provides automated storage/retrieval systems, conveyors, and AGVs critical to RTP operations. In April 2025, it completed a semi-automated warehouse for Rossmann, while the July 2025 launch of WAMAS Emulation Center enables digital replication of warehouses for risk-free process optimization. Its solutions enhance efficiency, reduce labor costs, and align with sustainable intralogistics practices.

Nefab AB: Strengthening RTP Solutions Through Strategic Acquisitions and Fiber-Based Innovations

Nefab offers returnable packaging for automotive, telecom, and industrial sectors. In August 2025, Nefab acquired FARUSA Emballage, and in April 2025, Embalajes Echeberria, expanding its sustainable packaging portfolio. Its FiberFlute product provides an eco-friendly, shock-absorbing alternative to foam. Nefab’s global network ensures efficient, circular supply chains while meeting sustainability and performance requirements.

Returnable Transport Packaging Market Share Insights, 2025-2034

Pallets retain Market Share leadership by Product Type in the Returnable Transport Packaging (RTP) market

In the RTP sector, pallets once again dominate with 40% market share, reinforced by their global standardization (EUR-pallets, GMA pallets) and compatibility with automated warehouses and international freight networks. The segment is undergoing a material transition, with lightweight, hygienic, and long-life plastic pallets expanding adoption in food, pharmaceuticals, and retail. Crates & totes follow with 25%, fueled by e-commerce expansion where unit-level picking and fulfillment efficiency depend on reusable handling systems. Intermediate bulk containers (IBCs) hold a significant 15%, servicing chemicals, pharmaceuticals, and food industries with secure, cost-efficient bulk handling. Drums & barrels contribute 12%, sustaining share in hazardous and certified applications despite competitive pressure from IBCs. Collapsible bins capture 8%, providing a strong value proposition in reverse logistics by reducing empty return costs—a critical factor in closed-loop, long-distance supply chains. Overall, pallets remain the uncontested leader due to universality and pooling efficiency, but the growth trajectory points towards IBCs and collapsible bins as specialized solutions solving liquid handling and logistics cost optimization challenges.

Food & Beverages drive Market Share by End-Use in the Returnable Transport Packaging (RTP) market

The food & beverage sector leads with 28% of RTP demand, as hygiene, cold chain integrity, and traceability are mission-critical. Plastic crates, RPCs, and hygienic pallets dominate here, enabling efficient produce handling, contamination risk reduction, and regulatory compliance. Automotive follows with 22%, reflecting its reliance on durable, custom-engineered RTP for high-value components in JIT supply chains. E-commerce & retail, the fastest-growing segment, now accounts for 20%, leveraging totes, crates, and pallets for fulfillment operations, last-mile delivery pilots, and reverse logistics. Chemicals represent 10%, using RTP in the form of certified drums and IBCs for safe handling of hazardous goods under strict compliance regimes. Consumer goods capture 10%, driven by high-volume retail supply chains that benefit from standardization, durability, and reduced damages. Healthcare & pharmaceuticals hold 10%, demanding the highest-value RTP with tamper-evidence, clean-room compliance, and temperature-control features—despite smaller volumes, this segment commands premium unit economics. This breakdown shows that F&B remains the anchor of RTP adoption, but e-commerce is reshaping the industry by accelerating the shift toward trackable, reusable, and logistics-optimized packaging systems.

European Union: PPWR and Reuse Targets Reshaping Transport Packaging Strategies

The European Union returnable transport packaging market is being reshaped by the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This regulation sets clear reuse obligations for multiple industries, directly influencing the logistics and retail sectors. One of the most critical targets is the mandated reduction of packaging waste per capita—by 5% in 2030, 10% in 2035, and 15% in 2040, compared to 2018 benchmarks. These ambitious goals are accelerating the transition away from single-use solutions toward returnable crates, pallets, and bulk containers.

Germany remains a front-runner with its reusable packaging obligation, effective since January 2023, which requires foodservice and catering businesses to provide reusable alternatives at the same cost as disposables. Across the EU, Deposit Return Systems (DRS) are gaining traction to streamline reverse logistics and improve packaging collection efficiency. Pilot initiatives such as “Mehrweg Modell Stadt” in Germany are testing cross-provider networks for reusable cups and containers, providing replicable models for other member states. Complementary policies like the Ecodesign for Sustainable Products Regulation (ESPR) and its Digital Product Passport are reinforcing compliance and supply chain transparency. These multi-layered regulations make Europe a benchmark region for scaling returnable transport packaging solutions.

United States: EPR Laws and Circular Economy Partnerships Driving Growth

In the United States, the returnable transport packaging market is expanding under a mix of federal and state-led initiatives. Extended Producer Responsibility (EPR) laws, now passed in seven states, are reshaping how packaging waste is managed. For instance, Maryland’s EPR law mandates that Producer Responsibility Organizations (PROs) must cover at least 90% of packaging waste management costs by 2030, placing significant responsibility on manufacturers to adopt returnable and recyclable formats.

Alongside regulations, industry innovation is advancing. The EPA and DOE are promoting sustainable packaging practices, with the DOE’s Building Technologies Office and EPA’s GreenChill program supporting energy efficiency in logistics and cold storage. Companies are making large-scale investments in recycling infrastructure and local manufacturing, backed by federal funding from the Infrastructure Investment and Jobs Act. Market trends highlight a growing preference for mono-material designs and premium returnable packaging formats, including high-margin crates and pallets designed for automotive, electronics, and food sectors. Collaborations under the U.S. Plastics Pact further align industry players toward national circular economy targets, ensuring the returnable transport packaging sector continues to scale.

China: Regulatory Push and E-Commerce Driving Reusable Transport Solutions

The China returnable transport packaging market is evolving rapidly under strong regulatory measures and the fast-growing logistics sector. As of June 1, 2025, new government rules require express delivery companies to prioritize reusable and eco-friendly packaging, directly fueling demand for returnable circulation boxes, crates, and pallets. The National Development and Reform Commission (NDRC) and Ministry of Ecology and Environment (MEE) are reinforcing these initiatives under the 14th Five-Year Plan, which focuses on curbing plastic pollution and promoting sustainable logistics.

Key logistics players like JDL Express and SF Express are deploying reusable inter-station transport boxes, phasing out single-use cardboard, and cutting down on packaging waste. The policy aligns with the Dual Circulation strategy, which emphasizes domestic demand, e-commerce growth, and logistics efficiency. The government is also incentivizing remanufacturing and green technologies through tax benefits, encouraging companies to invest in durable, recyclable, and eco-designed transport packaging systems. Combined with large-scale e-commerce demand, these shifts position China as a global leader in returnable transport packaging innovation.

India: EPR Regulations and Traceability Enhancing Returnable Packaging Models

The India returnable transport packaging market is expanding on the back of stricter regulatory frameworks under the Plastic Waste Management (Amendment) Rules, 2024. These rules enforce Extended Producer Responsibility (EPR) for producers, importers, and brand owners, while exempting smaller MSMEs. Importantly, starting from July 2025, plastic products used in packaging and logistics must be traceable through barcodes, QR codes, or unique identifiers, enabling accountability and enforcement across the supply chain.

The Indian Standards framework mandates disclosure of recycled content under IS 14534: 2023, creating opportunities for suppliers of returnable transport packaging to integrate high recycled content plastics and paper-based crates. Rising demand from the FMCG and processed food sectors, which rely on efficient and hygienic logistics, is driving adoption of reusable packaging in storage and last-mile delivery. At the same time, innovations in bioplastic-based reusable solutions—such as packaging derived from agricultural waste like ghee residue—are shaping a sustainable alternative market. These developments underscore India’s growing importance as a high-potential market for returnable transport packaging.

Japan: Plastic Resource Circulation Strategy Accelerating Reuse Adoption

The Japan returnable transport packaging market is guided by the country’s Plastic Resource Circulation Strategy, which mandates that all plastic packaging and goods be reusable or recyclable by 2025. This regulatory milestone is spurring investments in returnable crates, pallets, and containers, particularly for logistics, retail, and automotive supply chains. The government is also targeting to double renewable material use by 2030, reinforcing the shift toward bio-based and recyclable transport packaging formats.

Japanese companies are leading innovation in returnable solutions integrated with renewable or hybrid paper-plastic materials. For example, Nippon Paper Industries’ SHIELDPLUS barrier paper is influencing the development of recyclable crates and packaging liners. In parallel, the country is promoting waste sorting and circular economy models that ensure efficient collection and reuse of packaging materials. With major corporations like Shiseido also pushing refillable systems in consumer products, Japan is positioning itself as a technology-driven hub for scalable, returnable transport packaging.

Returnable Transport Packaging Market Report Scope

Returnable Transport Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10 Billion

|

|

Market Size (2034)

|

$16.2 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (Plastics, Wood, Metal, Glass, Paper & Paperboard), By Product Type (Pallets, Crates & Totes, Drums & Barrels, IBCs, Collapsible Bins), By End-Use Industry (Automotive, Food & Beverages, Consumer Goods, E-commerce & Retail, Healthcare & Pharmaceuticals, Chemicals), By Circulation Model (Closed-Loop Systems, Open-Loop Systems, Pooling Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Brambles Ltd. (CHEP), Schoeller Allibert, Orbis Corporation, DS Smith Plc, Smurfit Kappa Group Plc, Menasha Corporation, Myers Industries, Inc., Nefab Group, Rehrig Pacific Company, Schutz Container Systems, Inc., Buckhorn Inc., IPL Plastics Inc., CABKA Group, Georg Utz AG, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Returnable Transport Packaging Market Segmentation

By Material

- Plastics

- Wood

- Metal

- Glass

- Paper & Paperboard

By Product Type

- Pallets

- Crates & Totes

- Drums & Barrels

- IBCs

- Collapsible Bins

By End-Use Industry

- Automotive

- Food & Beverages

- Consumer Goods

- E-commerce & Retail

- Healthcare & Pharmaceuticals

- Chemicals

By Circulation Model

- Closed-Loop Systems

- Open-Loop Systems

- Pooling Services

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Returnable Transport Packaging Market

- Brambles Ltd. (CHEP)

- Schoeller Allibert

- Orbis Corporation

- DS Smith Plc

- Smurfit Kappa Group Plc

- Menasha Corporation

- Myers Industries, Inc.

- Nefab Group

- Rehrig Pacific Company

- Schutz Container Systems, Inc.

- Buckhorn Inc.

- IPL Plastics Inc.

- CABKA Group

- Georg Utz AG

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and integrated research methodology to provide comprehensive insights into the global returnable transport packaging (RTP) market, combining extensive secondary research with primary data collection. Our approach begins with the aggregation of verified data from company filings, industry reports, regulatory documents, trade publications, and sustainability disclosures to identify trends in reusable transport packaging, pooling services, and closed-loop logistics systems. Primary research involves interviews with packaging manufacturers, logistics providers, distributors, and end-users across automotive, food & beverage, e-commerce, and industrial sectors to assess operational efficiency, lifecycle benefits, and adoption challenges. USDAnalytics applies advanced quantitative modeling and market forecasting techniques to project market growth, incorporating variables such as technological innovations (IoT, RFID), material advancements, regulatory impacts (PPWR, EPR, Plastic Waste Management Rules), and regional dynamics. The methodology also evaluates strategic partnerships, mergers & acquisitions, and service models including pooling and pay-per-use frameworks. By combining cost-benefit analysis, environmental impact assessment, and supply chain optimization, USDAnalytics delivers actionable, data-driven insights that support strategic decision-making, investment planning, and operational improvements for industry professionals navigating the evolving RTP landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.