Plastic Pallets Market Size, Overview, and Growth Outlook (2025–2034)

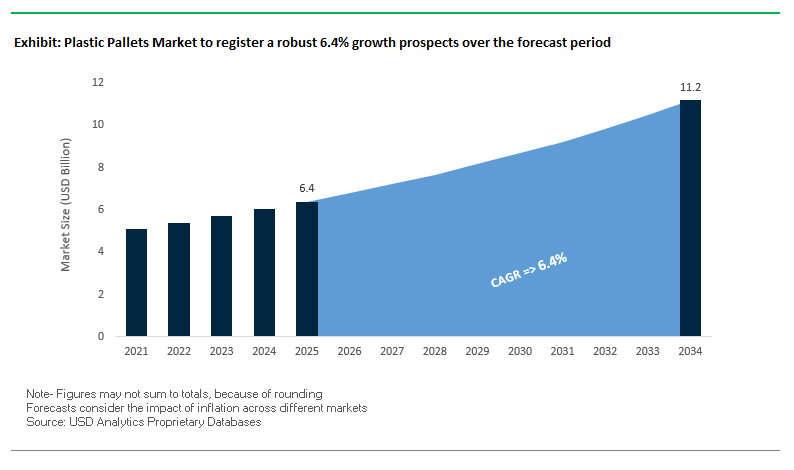

Plastic Pallets Market Set to Grow from $6.4 Billion in 2025 to $11.2 Billion by 2034 with 6.4% CAGR Driven by Reusability and Hygiene Benefits

The global plastic pallets market is expected to expand from $6.4 billion in 2025 to $11.2 billion by 2034, at a CAGR of 6.4%, driven by growing adoption in food & beverage, pharmaceuticals, cold chain logistics, and industrial sectors. Plastic pallets offer durability, hygiene, lightweight advantages, and compliance with international shipping standards, positioning them as an attractive alternative to traditional wooden pallets for global supply chains.

Key Insights for industry professionals and buyers:

- Durability and Long-Term Cost Efficiency: Plastic pallets can be reused over 100 cycles, spreading upfront costs over extended use.

- Hygienic Advantages for Sensitive Industries: Non-porous surfaces inhibit bacteria and fungi, making them ideal for food, pharma, and cold chain logistics.

- Lightweighting Reduces Transportation Costs: Lower pallet weight translates to fuel savings, reduced emissions, and cost-efficient air freight logistics.

- Exemption from ISPM 15 Regulations: Plastic pallets eliminate fumigation and heat-treatment requirements for international shipping.

- Sustainability and Circular Economy Alignment: Many plastic pallets leverage post-consumer recycled materials, supporting ESG goals and environmental stewardship.

Market Analysis: Plastic Pallets Industry Experiences Rapid Technological and Sustainability Advancements

The plastic pallets market has witnessed strategic expansions, innovative technology deployment, and sustainability-focused initiatives. In August 2025, Rehrig Pacific Company launched Rehrig Penn Inc., expanding its services to wood pallet management, signaling diversification beyond plastic solutions. That same month, Cabka N.V. reported positive H1 2025 results, with operational efficiencies and cost savings realized through its Shift program. In July 2025, Schoeller Allibert partnered with Transoplast, positioning Transoplast as a primary distributor for its reusable transport packaging solutions, strengthening European and global reach.

Technological innovation continues to redefine the market. April 2025 saw Rehrig Pacific introduce Vision® Object Recognition (VOR), an AI-powered system for real-time asset tracking, enhancing supply chain visibility. Similarly, June 2025 coverage in Fortune magazine highlighted Rehrig Pacific's long-term innovation and leadership. In March 2025, the Science Based Targets initiative (SBTi) validated Schoeller Allibert's GHG emission reduction targets, confirming the company’s commitment to sustainable operations.

Capacity expansions and mergers are further shaping the industry. In November 2024, ORBIS Corporation expanded its Ohio manufacturing plant by 30%, increasing production of pallets and totes to shorten lead times. In May 2025, Schoeller Allibert merged with IPL, creating a global sustainable packaging solutions provider with enhanced product offerings and market presence.

Emerging Trends and Opportunities in the Plastic Pallets Market

Strategic Shift Towards Closed-Loop Pooling and Rental Models

The plastic pallets market is experiencing a significant transformation as businesses shift from traditional ownership models to closed-loop pooling and rental systems. Barilla’s December 2024 announcement of consolidating its pallet operations with CHEP is a prime example of this transition. By converting the majority of its Italian freight pallets to CHEP’s reusable, managed pallet platform, Barilla projects avoiding over 290 tons of waste and 3,700 tons of CO₂ emissions annually. This case demonstrates the direct alignment between pallet pooling and corporate sustainability metrics, with measurable waste and emissions reductions that support ESG commitments. Similarly, Nestlé MENA renewed a two-year partnership with CHEP, transitioning from white wood pallets to managed plastic pooling solutions. The “share and reuse” model not only ensures higher service quality and consistency but also advances Nestlé’s goal of achieving net-zero emissions by 2050. These strategic moves highlight how pooling platforms are becoming central to corporate circular economy strategies, reducing waste, improving efficiency, and enhancing supply chain resilience.

Integration of Advanced Tracking and IoT Technologies

The digitalization of supply chains is further accelerating the adoption of plastic pallets, as companies leverage IoT and real-time data to maximize logistics efficiency. FreightWaves documented how CHEP’s tracking capabilities enable customers to reduce empty miles, minimize inefficiencies, and lower costs by harnessing movement data from its widely deployed blue pallets. This demonstrates how plastic pallets are evolving from simple load carriers into active enablers of smarter logistics systems. At the same time, automation in warehouses is reinforcing the importance of plastic pallets due to their dimensional uniformity. Unlike wood pallets, which often vary in shape and can disrupt automated conveyors or robotic handling systems, plastic pallets deliver an engineered, consistent design that minimizes downtime and prevents costly interruptions. Their precision, combined with IoT integration, makes them foundational for highly automated and data-driven supply chains, particularly in industries such as food, beverage, and pharmaceuticals where efficiency and accuracy are paramount.

Development of High-Performance Hybrid and Composite Materials

Material innovation offers one of the strongest growth avenues in the plastic pallets market, particularly through the development of hybrid and composite solutions. Research from Lund University in Sweden highlighted the advantages of lighter plastic pallets compared to wood alternatives, with transport-phase carbon emissions reduced significantly in closed-loop systems. Lightweight pallets contribute to lower fuel consumption during transit, enhancing sustainability while cutting costs for shippers. Companies such as Rehrig Pacific Company have further emphasized the economic benefits of durable, reusable plastic pallets, which outperform wood in longevity and reliability. Their resilience against wear and consistent design make them highly compatible with automated warehouses, offering long-term cost efficiency. Future material development is likely to focus on balancing reduced weight with enhanced load-bearing capacity, unlocking opportunities to further optimize emissions, performance, and lifecycle economics.

Expansion Driven by Stringent International Phytosanitary Regulations (ISPM 15)

Global trade regulations are also creating structural opportunities for plastic pallets. The International Standard for Phytosanitary Measures No. 15 (ISPM 15) requires wood packaging used in global shipments to undergo heat treatment or fumigation to prevent pest transfer. Plastic pallets, however, are fully exempt from this requirement, offering exporters a cost-effective and time-efficient alternative. This advantage makes them particularly attractive for industries like food, pharmaceuticals, and medical devices that depend on compliance with international trade rules and hygienic transport. Beyond regulatory exemptions, plastic pallets are increasingly preferred in industries governed by strict hygiene standards. iGPS Logistics reports that unlike porous wooden pallets, plastic pallets are non-absorbent, resistant to bacteria, and easy to sanitize, enabling compliance with regulations such as the U.S. Food Safety Modernization Act (FSMA). Their hygienic properties and exemption from ISPM 15 are accelerating adoption across global supply chains, cementing their role as a strategic choice for exporters and regulated industries.

Competitive Landscape: Leading Plastic Pallet Manufacturers Are Driving Innovation, Sustainability, and Operational Efficiency

The global plastic pallets industry is dominated by companies emphasizing technology, durability, sustainability, and service expansion. Industry leaders are investing in AI tracking, post-consumer recycled materials, and international capacity growth to meet evolving logistics and environmental requirements.

ORBIS Corporation: Delivering Integrated Reusable Packaging Solutions with Strong Circular Economy Focus

ORBIS provides a comprehensive portfolio of rackable, stackable, and nestable plastic pallets, bulk containers, and material handling solutions. The company specializes in integrated reusable packaging programs, helping customers improve operational efficiency while minimizing environmental impact. In November 2024, ORBIS expanded its Ohio facility by 30%, increasing molding capacity and energy efficiency. Its strength lies in sustainable program design and use of repurposed plastics, offering long-lasting, high-performance solutions.

Rehrig Pacific Company: Leading the Market with AI-Powered Supply Chain Visibility and Diverse Pallet Offerings

Rehrig Pacific produces a wide range of heavy-duty, multi-use, and fire-retardant plastic pallets, with various sizes and colors. Its Vision® Object Recognition (VOR) AI technology enables real-time asset tracking across supply chains. In August 2025, Rehrig launched Rehrig Penn Inc. for wood pallet management, expanding service offerings. The company’s core strength is injection molding expertise, which ensures premium quality, reliability, and integration of recycled materials into durable reusable solutions.

Schoeller Allibert: Driving Global Expansion and Sustainable Packaging Leadership through Strategic Mergers

Schoeller Allibert produces plastic pallets, foldable containers, crates, and boxes for industries such as retail, agriculture, and automotive. In May 2025, it merged with IPL, creating a $1.4 billion international packaging provider. The company’s SmartLink technology enables real-time tracking, while the AgriMax solution supports citrus harvesting efficiency. Validation of GHG emission targets by SBTi emphasizes the company’s commitment to sustainability and industry leadership.

Cabka Group: Transforming Recycled Plastics into High-Quality Reusable Pallets

Cabka converts hard-to-recycle plastic waste into plastic pallets and reusable transport packaging solutions. Its Shift program, reported on track in August 2025, enhances operational efficiency and reduces costs. Cabka’s vertically integrated process uses up to 100% recycled materials, earning an EcoVadis Platinum Medal. The company aims to become a global leader in sustainable reusable transport packaging, emphasizing circular economy principles.

T.M. Fitzgerald & Associates: Providing High-Quality Custom Pallets for Industrial and Food Applications

T.M. Fitzgerald & Associates manufactures plastic pallets tailored for food, waste management, and industrial applications. Its strength is responsive customer service and customization, ensuring optimal product protection and hygiene. Products are widely used in commercial bakeries, farms, private industries, and government sectors, emphasizing durability, reliability, and application-specific solutions.

Plastic Pallets Market Share Insights, 2025-2034

Stackable Pallets Dominate Market Share by Pallet Type in the Plastic Pallets Industry

Stackable pallets represent the largest segment with 35% share, cementing their role as the workhorse of the plastic pallets industry. Their appeal lies in durability, cost-effectiveness, and universal suitability for cross-industry warehousing and transportation, making them the default pallet choice across FMCG, manufacturing, and retail. Rackable pallets follow with a significant share, driven by the accelerated adoption of automated storage and retrieval systems (AS/RS) and robotics in logistics centers, where superior load-bearing strength and dimensional stability are critical. Nestable pallets contribute 18% of the market, thriving in closed-loop and returnable systems by reducing reverse logistics costs by up to 80%, making them essential for beverage bottling, parcel services, and high-frequency distribution networks. Export pallets, with a lean but steady share, dominate in international shipping due to their lightweight, ISPM 15-compliant design, offering a competitive edge over wooden alternatives. Drum pallets, while smaller in share, are indispensable for chemicals, pharmaceuticals, and food where spill containment and load stability are non-negotiable. Display pallets capture retail-focused growth, designed for point-of-purchase use where functionality merges with merchandising aesthetics. Custom pallets remain a premium, low-volume niche, serving industries like pharmaceuticals and cleanrooms where specialized designs or materials are necessary. Collectively, pallet segmentation reflects a shift from standardization toward specialization aligned with automation, hygiene, and logistics efficiency.

Manufacturing Holds the Largest Market Share by End-Use Industry in Plastic Pallets

The manufacturing sector accounts for the largest end-use share at 40%, as plastic pallets are indispensable in production environments requiring dimensional accuracy, durability, and hygiene standards that wood cannot consistently deliver. Precision pallets are crucial for in-process handling, robotic systems, and outbound logistics in industries ranging from automotive to electronics. Logistics and warehousing follows closely, representing 30% of demand, fueled by the explosive rise of e-commerce and automated fulfillment centers that rely on rackable and nestable pallets to streamline throughput and reduce total cost of ownership (TCO). Food and beverage industries maintain a critical 15% share, where plastic pallets are mandated by food safety regulations due to their non-porous, easily sanitized surfaces that minimize bacterial growth—a key compliance factor under HACCP and FDA standards. Retail, while smaller at 8%, leverages plastic pallets for backroom storage and increasingly for floor-ready display pallets, enhancing merchandising efficiency. Chemicals and pharmaceuticals hold 7%, a specialized but high-margin segment demanding pallets with static control, chemical resistance, and cleanroom compatibility. This end-use segmentation illustrates that while manufacturing sets the volume baseline, the fastest-growing opportunities are in logistics automation and regulated industries where pallet performance, traceability, and sustainability converge.

United States: EPR Laws, Automation, and FDA Standards Driving Growth

The United States plastic pallets market is undergoing a structural transformation driven by regulation, automation, and sustainability initiatives. The Department of Energy’s “Strategy for Plastics Innovation” is a pivotal force, directing R&D into recyclable-by-design plastics and advanced recycling technologies that directly influence pallet composition. A growing number of states are introducing Extended Producer Responsibility (EPR) laws, which are expected to expand beyond packaging into durable goods such as plastic pallets. These laws will require manufacturers to manage end-of-life recycling, creating accountability across the supply chain.

At the same time, U.S. plastics manufacturers are investing heavily in automation, with over 1,600 robotic units added in 2023, significantly enhancing quality control and reducing production costs for molded pallets. Innovations center on post-consumer recycled (PCR) content pallets, aligning with brand sustainability goals and the U.S. Plastics Pact’s circular economy vision. In the food & beverage industry, the FDA’s strict food-contact regulations are pushing demand for hygienic pallets that prevent contamination. Collectively, these factors are positioning the U.S. as a leader in sustainable and automated pallet manufacturing.

European Union: PPWR and Circular Economy Targets Reshaping Pallet Design

In the European Union, the plastic pallets market is shaped by stringent sustainability regulations. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, enforces recyclability standards and mandates that packaging be reusable under defined conditions. From August 2026, the PPWR prohibits food packaging containing PFAS above threshold limits, with implications for pallet materials used in food transport. Looking further ahead, by January 2030, products with a recyclability grade below 70% will no longer qualify as recyclable, forcing pallet manufacturers to adopt “design for recycling” strategies.

The EU’s circular economy focus is stimulating demand for single-material, fully recyclable pallets while discouraging multi-material products. Government funding is flowing into projects that improve durability and reparability, helping companies extend pallet lifespans and reduce waste. The regulatory environment is fostering innovation in reusable pallet systems, ensuring compliance while meeting industry needs for efficiency and sustainability.

China: Domestic Recycling Expansion and Robotics Adoption Boosting the Market

China’s plastic pallets industry is strongly influenced by regulations introduced in June 2025, targeting delivery waste reduction through recycled materials and reusable packaging systems. Following the 2018 ban on plastic waste imports, China has built a domestic recycling infrastructure that underpins pallet manufacturing with locally sourced recycled materials. Regulatory agencies including the NDRC and MEE are working jointly to tighten control over plastic pollution, strengthening compliance for pallet producers.

Automation is a key differentiator, with companies like Shandong LingYue Packing Products pioneering unmanned production lines that integrate robotic palletizing. On the regulatory side, the positive list system for food-contact materials and new adhesive standards are shaping pallet production for food logistics. China’s engagement with international standards, particularly via the China Federation of Logistics and Purchasing’s involvement in ISO/TC 51, highlights its growing influence in global pallet standardization.

India: EPR Enforcement and Local Innovation Supporting Sustainable Pallets

India’s plastic pallets market is being reshaped by the Plastic Waste Management Rules (2016, amended in 2022), which impose strict Extended Producer Responsibility (EPR) requirements. Under this framework, manufacturers must collect and recycle plastic waste, extending responsibility to durable goods like pallets. National initiatives such as the Swachh Bharat Abhiyan are reinforcing this shift by promoting waste segregation and improved collection infrastructure.

The Food Safety and Standards Authority of India (FSSAI) is also driving sustainability by holding consultations on biodegradable and recyclable food packaging, influencing pallet adoption in the food sector. Local innovation is accelerating, with Indian manufacturers investing in eco-friendly pallet designs that balance durability with recyclability. As India’s logistics and industrial sectors expand, EPR obligations and innovation are combining to create a fast-evolving market for sustainable pallets.

Brazil: Heavy Investment and Regulatory Push Toward Recycling

Brazil’s plastic pallets market is benefiting from strong industry investment, with the Abiplast association forecasting R$10.5 billion ($1.8 billion) annually for factory expansions, sustainable packaging, and new recycling technologies. The National Solid Waste Policy seeks to achieve a 27% recycling rate for plastic packaging by 2024, creating downstream impacts for pallet production. The growth of e-commerce—up 26.9% in 2022—is increasing demand for efficient logistics solutions, including durable pallets.

Major companies like Braskem are expanding capacity, including the development of a new ethane import terminal, ensuring secure feedstock for plastic pallet production. Brazil’s active role in UN plastics negotiations further emphasizes its commitment to global plastic pollution solutions. With investment-driven capacity growth and regulatory recycling targets, Brazil is positioning itself as a leading Latin American hub for sustainable pallet innovation.

Canada: SUPPR Ban and USMCA Facilitating Trade in Pallet Solutions

Canada’s plastic pallets market is influenced by the Single-Use Plastics Prohibition Regulations (SUPPR), which aim to achieve zero plastic waste by 2030. By eliminating over 1.3 million tonnes of hard-to-recycle waste, these regulations are encouraging companies to adopt durable and reusable products such as pallets. Demand for rPET-based products is increasing, as companies align with EPR program requirements and consumer preferences.

Government support, such as the $2.9 million funding to Exxel Polymers, underscores Canada’s commitment to scaling up recycled plastics infrastructure. Furthermore, the USMCA trade agreement ensures seamless cross-border pallet trade and logistics integration with the U.S. and Mexico. This combination of federal regulation, investment support, and trade facilitation is shaping Canada’s role as a reliable supplier of sustainable pallet solutions in North America.

Plastic Pallets Market Report Scope

Plastic Pallets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$11.2 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Pallet Type (Nestable, Rackable, Stackable, Drum, Display, Export, Custom), By Material (HDPE, PP, LDPE, Recycled Content Plastics, Virgin Resins, Others), By Application (Food & Beverages, Chemicals & Pharmaceuticals, Automotive, Retail & Consumer Goods, Logistics & Warehousing, Agriculture), By End-Use Industry (Manufacturing, Transportation, Logistics, Retail)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cabka Group, Schoeller Allibert, Rehrig Pacific Company, ORBIS Corporation, TranPak Inc., Perfect Pallets, Inc., Monoflo International, Greystone Logistics Inc., Plastic Pallets and Containers, TMF Corporation, Buckhorn Inc., Craemer Group, RPP Containers, IQS Directory, WEBER Packaging GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Pallets Market Segmentation

By Pallet Type

- Nestable

- Rackable

- Stackable

- Drum

- Display

- Export

- Custom

By Material

- HDPE

- PP

- LDPE

- Recycled Content Plastics

- Virgin Resins

- Others

By Application

- Food & Beverages

- Chemicals & Pharmaceuticals

- Automotive

- Retail & Consumer Goods

- Logistics & Warehousing

- Agriculture

By End-Use Industry

- Manufacturing

- Transportation

- Logistics

- Retail

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Pallets Market

- Cabka Group

- Schoeller Allibert

- Rehrig Pacific Company

- ORBIS Corporation

- TranPak Inc.

- Perfect Pallets, Inc.

- Monoflo International

- Greystone Logistics Inc.

- Plastic Pallets and Containers

- TMF Corporation

- Buckhorn Inc.

- Craemer Group

- RPP Containers

- IQS Directory

- WEBER Packaging GmbH

* List Not Exhaustive

Methodology

USDAnalytics applies a robust, multi-layered research methodology to deliver a comprehensive analysis of the Plastic Pallets Market. Our approach integrates both primary and secondary research, including in-depth interviews with industry leaders, supply chain experts, and regulatory authorities, alongside meticulous review of company reports, press releases, patents, financial statements, and trade publications. We employ quantitative modeling and forecasting to estimate market size, growth trajectory, and segmental trends, analyzing key factors such as pallet type (stackable, rackable, nestable, export, drum, display, custom), material composition (HDPE, PP, LDPE, recycled content, virgin resins), applications (food & beverage, chemicals & pharmaceuticals, logistics, automotive, retail, agriculture), and end-use industries (manufacturing, transportation, warehousing, retail). USDAnalytics also evaluates technological innovations, sustainability initiatives, IoT-enabled tracking systems, and regulatory frameworks across major regions, including the U.S., EU, China, India, Canada, and Brazil. This comprehensive methodology ensures actionable insights for industry professionals, highlighting growth opportunities in reusable pallet systems, hybrid and composite materials, circular economy adoption, and automated warehouse integration. Our analysis emphasizes accuracy, market relevance, and forward-looking intelligence to guide strategic investment, production, and supply chain decisions in the global plastic pallets market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.