Wood Packaging Market Overview: Pallets and Circular Models Driving Growth

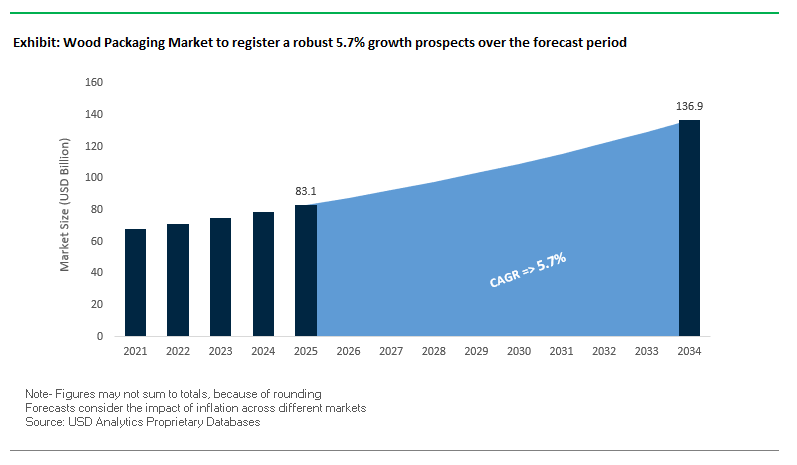

The Global Wood Packaging Market is projected to reach $83.1 billion in 2025 and expand to $136.9 billion by 2034, growing at a CAGR of 5.7%. Wood packaging plays a vital role in global logistics, supply chain efficiency, and safe product transport, with pallets accounting for the largest share. Pallets are the backbone of distribution networks due to their strength, reusability, and cost-effectiveness, making them indispensable for food, beverages, pharmaceuticals, and industrial goods.

The market is undergoing a transformation toward sustainability and circular economy models. Companies are increasingly adopting share-and-reuse platforms to reduce waste and optimize asset use. This shift is backed by regulatory recognition, such as the EU Packaging and Packaging Waste Regulation (PPWR), which in 2024 exempted wooden pallets from reuse requirements, acknowledging their sustainability contribution. Beyond logistics, wood packaging is finding a niche in premium e-commerce shipments, where crates and specialty wooden boxes enhance the unboxing experience for high-value goods.

Key Insights for Industry Professionals

- Wood pallets dominate global demand, ensuring efficiency and durability in supply chains.

- Circular business models such as share-and-reuse are reshaping the wood packaging industry.

- EU PPWR exemption for wood pallets highlights the sustainability role of reusable wooden platforms.

- Premium wooden crates are emerging in e-commerce to create memorable unboxing experiences.

Market Analysis: Recent Developments in Global Wood Packaging

The wood packaging industry is experiencing both strategic mergers and innovations that align with sustainability and operational efficiency. In August 2025, Brambles Ltd., a global leader in reusable pallets, reported strong annual results with an increased focus on free cash flow generation and launched a new share buy-back program, underscoring its financial stability. In the same month, Rehrig Pacific Company entered the wood pallet services segment by launching Rehrig Penn Inc., expanding its service offerings in pallet retrieval and management.

Also in August 2025, Nefab Group acquired FARUSA Emballage through its Danish subsidiary, strengthening its Nordic market position and extending its engineered packaging solutions. Earlier, in January 2025, the Smurfit Kappa–WestRock merger was completed, creating Smurfit WestRock, a giant in paper-based packaging with capabilities extending into paper pallets and eco-friendly pallet wraps. Shortly after, the new entity introduced an all-paper stretch wrap, a recyclable alternative to polyethylene, signaling a strong push toward sustainable palletization.

Looking back to November 2024, Nefab unveiled its award-winning EdgePak Collar, a lightweight and recyclable alternative to wooden pallet collars, further reinforcing its innovation leadership. That same period saw a report highlighting a slowdown in overall M&A activity in the packaging sector, although large strategic deals like Smurfit–WestRock and Amcor–Berry illustrated continued consolidation momentum.

Wood Packaging Market: Emerging Trends and Growth Opportunities

Strategic Shift to Pallet Pooling and Managed Services

The wood packaging market is undergoing a fundamental transformation as manufacturers and retailers increasingly transition from owning pallet assets to leveraging third-party pooling and managed services. This shift is driven by the need to reduce capital expenditure, improve logistics efficiency, and align with sustainability goals. Pallet pooling converts heavy upfront capital investments into predictable operational costs through usage-based models, offering companies greater financial flexibility. For instance, LEAP India provides a scalable pooling system that allows businesses to adjust pallet requirements based on seasonal demand, avoiding the burden of excess inventory.

Sustainability is another critical driver of this transition. Shared-use pallets extend asset lifecycles by undergoing repeated inspections, repairs, and redistribution. Providers like 48forty highlight quantifiable ESG benefits, including reductions in landfill waste and lower carbon footprints, helping brands meet corporate sustainability pledges. Additionally, outsourcing pallet management allows companies to focus on their core business operations while specialized pooling providers handle logistics recovery and refurbishment. This business model, rooted in asset-sharing, is attracting major institutional investors such as Morgan Stanley, underscoring the long-term growth prospects of sustainable pallet management services.

Regulatory Scrutiny Driving Standardization and Phytosanitary Compliance

Global enforcement of the ISPM 15 standard is intensifying, making phytosanitary compliance a critical non-negotiable factor in international wood packaging. Developed by the International Plant Protection Convention (IPPC), ISPM 15 mandates debarking, heat treatment, or methyl bromide fumigation of wood packaging materials (WPM) to prevent the spread of invasive pests and diseases. Countries such as the United States and New Zealand impose strict adherence, requiring stamped certification to verify compliance.

Failure to meet ISPM 15 standards results in shipment rejections at borders, causing costly delays and disruptions in supply chains. The U.S. Animal and Plant Health Inspection Service (APHIS) provides comprehensive enforcement guidance, emphasizing accountability through traceability to the treatment provider and manufacturer. For manufacturers, global harmonization of these rules requires robust internal certification systems and frequent audits to ensure consistent compliance. This increasing scrutiny is pushing wood packaging companies to adopt more advanced process control, documentation, and certification practices, effectively embedding regulatory compliance into their competitive strategy.

Development of Embedded Tracking and IoT Integration

The integration of IoT technologies into wood packaging represents a high-value opportunity to transform pallets and crates from passive transport assets into active supply chain intelligence hubs. Embedding RFID tags and IoT sensors into wooden pallets enables real-time tracking of shipments, reducing losses, theft, and inefficiencies. Research into intelligent RFID use in supply chains shows that these solutions deliver near-instantaneous tracking and significantly higher inventory accuracy compared to manual methods.

Beyond location monitoring, IoT-enabled pallets can measure critical environmental conditions such as temperature, humidity, shock, and tilt data essential for sensitive goods in the food and pharmaceutical sectors. Real-world applications have demonstrated reductions in product damage and improved compliance with cold-chain standards. Moreover, the data captured by smart pallets fuels predictive analytics, enabling companies to identify supply chain bottlenecks, optimize routes, and reduce dwell times. This results in measurable operational savings while unlocking new value streams, positioning IoT-enabled pallets as a key innovation in next-generation wood packaging logistics.

Innovation in Engineered and Alternative Wood Components

The growing demand for sustainable and high-performance materials is creating opportunities for engineered wood solutions and the use of alternative raw fibers in wood packaging. Engineered wood products such as laminated veneer lumber (LVL) and oriented strand board (OSB) are gaining traction due to their superior strength, resistance to warping, and ability to be tailored for specific load requirements. Unlike solid hardwood, engineered solutions maximize raw material utilization, thereby reducing waste and improving consistency in pallet and crate performance.

Alternative materials like bamboo and agricultural residues are also emerging as viable substitutes. Bamboo, with its tensile strength surpassing steel and rapid growth cycle of three to five years, is being recognized as a renewable and robust replacement for traditional wood in packaging. Simultaneously, agricultural waste such as rice straw, wheat straw, and sugarcane bagasse is being processed into biodegradable fibers and composites, offering an innovative way to reduce dependence on virgin timber while addressing agricultural residue management challenges. Together, engineered wood and alternative fibers position the industry to reduce environmental impact, meet evolving regulatory expectations, and diversify raw material supply chains for long-term resilience.

Competitive Landscape: Leading Companies in Global Wood Packaging

The global wood packaging market is highly consolidated, with major players leveraging circular economy models, engineered innovations, and global networks to expand their market reach.

Brambles Ltd.: Scaling Circular Economy through CHEP and IFCO

Brambles dominates the global wood packaging sector through its CHEP and IFCO brands, managing over 348 million pallets, crates, and containers worldwide. In late 2024, the company strengthened its financial position with a US$400 million share buy-back program. Its BXB Digital platform enhances supply chain efficiency by providing real-time asset tracking, while its circular share-and-reuse model ensures sustainability and cost efficiency for global customers.

Nefab Group: Driving Innovation with Sustainable Engineered Solutions

Nefab specializes in engineered wood and multi-material packaging solutions, offering crates, boxes, and pallets tailored to industrial requirements. The company focuses on lightweight plywood-based solutions and no-nail assembly systems, enhancing safety and reducing carbon emissions. In August 2025, it expanded further by acquiring FARUSA Emballage, strengthening its Nordic presence and expertise in heavy-duty industrial packaging. Nefab’s EdgePak Collar remains a flagship innovation in recyclable pallet solutions.

Millwood, Inc.: Expanding Vertically Integrated Pallet Solutions

Millwood operates more than two dozen locations, offering new and recycled pallets, lumber, and packaging management systems. Its vertically integrated model ensures control over its supply chain, from raw lumber to finished products. With the Millwood Lab, customers can test load-handling designs for customized solutions. Its strategic focus is on reducing waste through comprehensive logistics and packaging management services, making it a strong U.S. player in wood pallet innovation.

Rehrig Pacific Company: Expanding into Wood Pallet Services

Rehrig Pacific has long been known for plastic and wood packaging solutions in beverages, dairy, and retail. In August 2025, it launched Rehrig Penn Inc. to strengthen its role in wood pallet management services. By integrating supply chain expertise with both wood and plastic solutions, Rehrig is blurring material boundaries and offering flexible, customer-focused logistics models. Its strength lies in delivering integrated and sustainable pallet solutions tailored to customer needs.

Wood Packaging Market Share Insights

Wooden Pallets Dominate Market Share by Product Type in the Wood Packaging Industry

Wooden pallets account for nearly 65% of the global wood packaging market, cementing their role as the fundamental unit load base across global logistics and supply chains. Their dominance is reinforced by the rise of pallet pooling and rental networks such as CHEP and Loscam, which have embedded pallets into a mature circular economy model where reuse, repair, and refurbishment ensure sustainability and cost efficiency. Unlike alternative materials, wooden pallets balance strength, affordability, and scalability, making them indispensable for both industrial and consumer goods transportation. Their ability to adapt to automation-driven warehouses and global shipping standards ensures long-term relevance, even as composite and paper-based alternatives emerge in niche markets.

Industrial Sector Leads Market Share by End-Use Industry in the Wood Packaging Market

The industrial sector represents the largest share of demand within the wood packaging industry, accounting for approximately 28% of usage in 2025. This dominance is tied to the sector’s need for robust, custom-engineered wooden crates and pallets capable of transporting heavy-duty equipment, aerospace components, and machinery across long, complex supply chains. Unlike consumer-driven sectors, the industrial segment prioritizes durability, shock resistance, and compliance with international standards such as ISPM-15, which regulate wood packaging in cross-border trade. Its steady growth reflects the resilience of industrial activity, where the protection of high-value assets far outweighs cost concerns, keeping wood packaging at the forefront despite increasing competition from engineered plastics and metals.

United States: Sustainable and Technology-Enhanced Wood Packaging Driving Logistics Efficiency

The U.S. wood packaging market is experiencing growth fueled by rising sustainability awareness among consumers and corporations, driving demand for reusable, recyclable, and FSC-certified wood packaging solutions. These solutions are increasingly preferred due to their lower carbon footprint compared to non-biodegradable alternatives. Technological advancements, such as heat treatment and pressure impregnation, are improving durability and pest resistance, helping meet phytosanitary standards. Additionally, the integration of RFID tags for tracking and monitoring is enhancing the value of wood packaging in logistics and supply chain management.

Government initiatives like the USDA Forest Service Wood Innovations Grant Program are providing funding to expand timber markets, promote sustainable wood use, and drive economic growth in the packaging sector. Key applications include wooden pallets and crates for the food and beverage, automotive, and manufacturing industries, where durable, reusable, and cost-effective packaging is critical. Regulatory compliance with APHIS ISPM 15 standards ensures that all imported wood packaging is treated and certified to prevent the spread of wood-boring pests, maintaining both domestic and international safety standards.

Germany: Circular Economy and Regulatory Compliance Accelerating Reusable Wood Packaging

Germany’s wood packaging market is strongly influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), creating demand for eco-friendly and fully recyclable packaging. The country emphasizes a circular economy, with reusable packaging, particularly wooden pallets, being a major focus. Regulations such as the Verpackungsgesetz (Packaging Act), along with quality standards from the European Pallet Association (EPAL), ensure durable, standardized pallets are widely adopted.

Technological innovation in Germany includes integrating wood packaging into automated logistics and supply chains, improving efficiency and sustainability. The PPWR 2025 regulation also sets ambitious targets for full recyclability by 2030, along with reuse and refill mandates, driving German companies to invest in innovative pallet design, lightweighting, and automated production techniques. These efforts strengthen Germany’s position as a leader in sustainable wood packaging for industrial and commercial logistics.

China: Eco-Friendly Policies and Automation Boost Wood Packaging Demand

China’s wood packaging market is benefiting from government policies targeting the dual carbon goal of achieving carbon peak and carbon neutrality, encouraging the adoption of eco-friendly and reusable materials. Manufacturers are increasingly investing in automation and AI technologies, combining 5G and industrial internet solutions to optimize production efficiency and achieve flexible manufacturing capacity.

Sustainability policies, including restrictions on non-degradable plastics in express delivery by 2025, are driving demand for paper-based and wood packaging alternatives. Rapid e-commerce growth is boosting the need for durable and reliable wood packaging to secure long-distance shipping. Industry innovations, such as lightweight, efficient pallet and crate designs, are reducing material use and enhancing logistics efficiency, reflecting China’s commitment to sustainable, high-performance wood packaging solutions.

India: Government Initiatives and Rubberwood Adoption Driving Growth in Wood Packaging

India’s wood packaging market is witnessing rapid expansion supported by initiatives such as Make in India and Zero Effect Zero Defect, which promote quality domestic production and industrial infrastructure development. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, incentivizes manufacturers to adopt standardized and high-quality packaging solutions, including wood pallets and crates for bulk transport.

Rising disposable income and urbanization are driving demand for convenient, durable packaging solutions, making wood packaging increasingly important for logistics and supply chains. Indian companies heavily rely on rubberwood, known for its strength and durability, to produce reusable and reliable wood packaging cases. Regulatory frameworks, including the Plastic Waste Management (Amendment) Rules and Food Safety and Standards (Packaging and Labelling) Regulations, are further steering the market toward sustainable, eco-friendly alternatives in wood packaging for diverse industrial applications.

Wood Packaging Market Report Scope

Wood Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$83.1 Billion

|

|

Market Size (2034)

|

$136.9 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Wooden Pallets, Wooden Boxes & Crates, Wooden Containers, Wooden Bins & Cases, Other Product Types), By Material Type (Plywood, OSB, Lumber, Other Materials), By End-Use Industry (Food & Beverages, Industrial, Automotive, Chemicals, Logistics & Transportation, Other End-Use Industries), By Packaging Format (Primary Packaging, Secondary Packaging, Tertiary Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Brambles Limited, PalletOne Inc., UFP Industries, Inc., Greif, Inc., Nefab AB, Schoess, Saurashtra Pallets and Packaging Pvt. Ltd., Chep, Shur-Way Group, Durex, Rowlinson Packaging Ltd, Pallet Logistics of America, Pelheat Ltd, Conitex Sonoco, Edwards Wood Products, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wood Packaging Market Segmentation

By Product Type

- Wooden Pallets

- Wooden Boxes & Crates

- Wooden Containers

- Wooden Bins & Cases

- Other Product Types

By Material Type

- Plywood

- OSB

- Lumber

- Other Materials

By End-Use Industry

- Food & Beverages

- Industrial

- Automotive

- Chemicals

- Logistics & Transportation

- Other End-Use Industries

By Packaging Format

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Wood Packaging Market

- Brambles Limited

- PalletOne Inc.

- UFP Industries, Inc.

- Greif, Inc.

- Nefab AB

- Schoess

- Saurashtra Pallets and Packaging Pvt. Ltd.

- Chep

- Shur-Way Group

- Durex

- Rowlinson Packaging Ltd

- Pallet Logistics of America

- Pelheat Ltd

- Conitex Sonoco

- Edwards Wood Products, Inc.

* List Not Exhaustive

Methodology

USDAnalytics has conducted a comprehensive, data-driven analysis of the global Wood Packaging Market using a robust combination of primary and secondary research techniques. Our methodology includes in-depth interviews with key stakeholders such as pallet manufacturers, logistics providers, industrial end-users, and sustainability experts, complemented by secondary research from company reports, press releases, regulatory frameworks, and trade publications. Market sizing, CAGR projections, and forecast models are based on historical demand trends, the rising adoption of circular economy and share-and-reuse pallet models, and innovations in engineered wood, alternative raw materials, and IoT-enabled tracking solutions. The analysis also accounts for regional regulatory impacts, including ISPM 15 compliance and EU PPWR mandates, as well as emerging applications in premium e-commerce, industrial logistics, and automation-driven warehouses. Segmentation spans product type, material type, packaging format, and end-use industry, while strategic insights capture mergers, acquisitions, and technological advancements shaping the competitive landscape. This methodology ensures USDAnalytics delivers actionable intelligence and strategic guidance for industry professionals seeking to navigate the evolving wood packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.