Rigid Plastic Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Rigid Plastic Packaging Market to Reach $672.4 Billion by 2034 Driven by Sustainability, Lightweighting, and E-commerce Demand

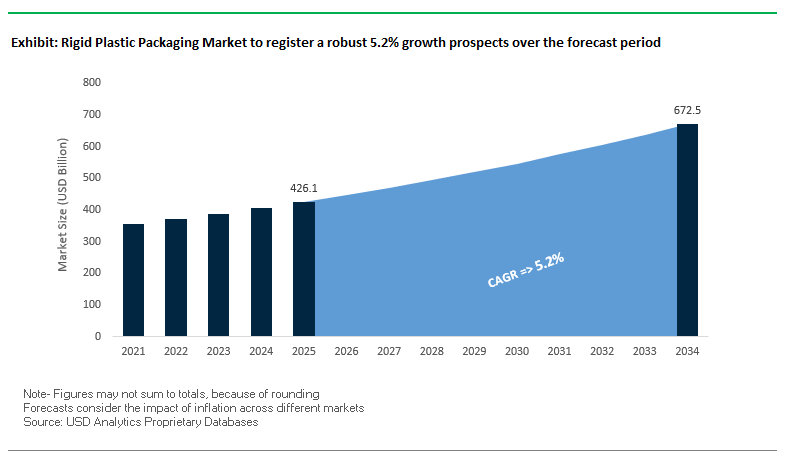

The global rigid plastic packaging market is projected to grow from $426.1 billion in 2025 to $672.4 billion by 2034, at a CAGR of 5.2%. This growth is fueled by stringent sustainability regulations, innovations in lightweighting, PET dominance in beverages, and the rapid rise of e-commerce. Industry professionals can leverage insights from recycled content adoption, design versatility, and supply chain efficiency to inform investment and production decisions.

Key Insights for decision-makers and buyers:

- Recycled Content Targets: Major manufacturers are integrating 25% or more recycled plastic to comply with the EU Packaging and Packaging Waste Regulation (PPWR).

- PET Dominance: PET bottles and containers account for over 40% of North America’s food and beverage rigid packaging, valued for clarity, durability, and recyclability.

- Lightweighting Innovations: Material and design advances reduce plastic content by over 16%, lowering costs while maintaining product integrity.

- E-commerce Influence: Robust and standardized rigid containers facilitate automated handling, reduce transit damage, and improve supply chain efficiency.

- Circular Economy Momentum: Companies are exploring plant-based polymers and reusable plastic solutions, aligning with long-term sustainability goals.

- Premium Branding and Customization: Opportunities exist for enhanced printability, labeling, and consumer engagement in high-value markets.

The rigid plastic packaging market represents a strategic convergence of sustainability, efficiency, and innovation, making it a focal point for global packaging investment and operational strategies.

Market Analysis: Strategic Mergers, Sustainable Innovations, and Facility Expansions Are Shaping the Rigid Plastic Packaging Market

The rigid plastic packaging industry has experienced robust activity through mergers, acquisitions, and sustainable product launches. In August 2025, Amcor and Flügger introduced a paint container with 50% recycled material, showcasing commitment to circular packaging. In July 2025, the Amcor-Berry Global merger created a diversified global leader in rigid plastic solutions, enhancing product range and geographic footprint.

Sustainability-focused developments have accelerated industry transformation. In February 2025, Amcor Rigid Packaging partnered with Avantium NV to explore plant-based polyethylene furanoate, advancing bioplastic adoption. Simultaneously, the February 2025 merger between IPL and Schoeller Allibert formed a $1.4 billion reusable packaging powerhouse, reflecting a shift toward reusable plastic solutions.

Facility investments and portfolio optimization demonstrate strategic growth. April 2025 saw Sonoco divest its Thermoformed and Flexibles Packaging business for US$1.8 billion, focusing on core rigid packaging. That month, ALPLA expanded injection molding capabilities via an Italian acquisition, reinforcing global production capacity. Earlier, in November 2024, Sonoco acquired Eviosys, advancing its European rigid packaging offerings. These moves underscore the dual focus on sustainability and operational excellence driving the market forward.

Rigid Plastic Packaging Market: Trends and Opportunities Transforming Circularity

Mandated Incorporation of Post-Consumer Recycled (PCR) Content

One of the most powerful forces driving transformation in the rigid plastic packaging market is the legally binding incorporation of post-consumer recycled (PCR) content. The European Union’s Packaging and Packaging Waste Regulation (PPWR), finalized in March 2024, establishes strict recycled content thresholds for plastic packaging across all member states. By 2030, single-use plastic beverage bottles must contain at least 30% recycled content, rising further to 65% by 2040. These requirements not only apply to packaging manufactured in the EU but also to imports, effectively raising the global compliance bar. Parallel regulatory momentum is evident in Asia: India’s Plastic Waste Management (Amendment) Rules, April 2025, mandate a minimum of 30% recycled content for rigid plastics (Category I) by FY 2025–26, with targets climbing to 60% by FY 2028–29. Together, these regulations are creating powerful demand signals for recycled resins, compelling brand owners and converters to accelerate sourcing strategies and invest in high-quality PCR integration to maintain compliance and brand reputation.

Strategic Vertical Integration and Investment in Advanced Recycling

A second defining trend is the vertical integration of advanced recycling infrastructure by brand owners and packaging producers. This strategy ensures a secure and high-quality feedstock supply at a time when global demand for recycled resins far outpaces availability. The Circular Plastics Australia partnership—a joint venture between Pact Group, Cleanaway, Asahi Beverages, and Coca-Cola Europacific Partners—serves as a strong example. By pooling resources, these companies are doubling the production of food-grade rPET in Australia from 30,000 tonnes to over 60,000 tonnes annually, ensuring a robust closed-loop system for beverage bottles. Similarly, a Lux Research report (Jan 2025) highlights how advanced recycling operators are integrating upstream to capture guaranteed feedstocks, reducing dependence on volatile waste collection markets. This shift underscores a growing industry recognition that controlling recycling capacity and feedstock access is as critical as packaging production itself, positioning vertically integrated firms as leaders in the race toward circular rigid plastic packaging.

Adoption of Monomaterial and Polymer-Barrier Solutions

One of the most significant opportunities lies in the transition from composite to monomaterial rigid plastic packaging. Traditional multi-layer structures hinder recyclability, but innovations are delivering monomaterial formats with high-performance barrier properties. A June 2025 article spotlighted Zotefoams’ “ReZorce” packaging, a monomaterial barrier solution recognized for replacing non-recyclable composites while retaining structural and functional performance. Similarly, NUREL’s “Enoxite®” barrier polymer portfolio offers ultra-high oxygen resistance as an internal layer in recyclable PE and PP trays. These advances make rigid plastic containers suitable for sensitive food applications like dairy and ready meals while remaining fully recyclable. By solving the recyclability-versus-performance trade-off, monomaterial barrier packaging positions itself as a game-changing enabler for brands striving to meet regulatory recycled content targets without compromising product protection or shelf life.

Integration of Digital Watermarking for Intelligent Sorting

The second major opportunity is the integration of digital watermarking technologies for advanced waste stream sorting. The HolyGrail 2.0 initiative, led by the European Brands Association with support from the Alliance to End Plastic Waste, has proven that watermarking rigid plastic packaging can dramatically enhance sorting accuracy. Trials conducted with post-consumer waste achieved detection accuracy between 87.9% and 93.8%, even in highly mixed waste streams. Beyond simple separation, this technology enables SKU-level sorting, where watermarks encode information such as polymer type, food versus non-food use, and brand. A technical report from April 2025 confirmed that this granular data makes it possible to create high-purity recycling streams, unlocking the production of higher-quality recyclate essential for food-contact and premium applications. As regulations tighten, watermarking stands out as a critical digital enabler that not only improves recycling yields but also builds transparency and traceability across the rigid plastic packaging value chain.

Competitive Landscape: Global Leaders Are Driving Innovation, Sustainability, and Operational Efficiency in Rigid Plastic Packaging

The rigid plastic packaging sector is highly competitive, with top companies leveraging innovation, sustainability, and mergers to capture market share. These leaders address food, beverage, healthcare, and consumer goods markets with durable, recyclable, and high-performance packaging solutions.

Amcor plc: Leading the Way with Sustainable and Lightweight Rigid Plastic Packaging

Amcor provides a broad portfolio of rigid plastic containers including PET bottles and jars, serving beverages, food, and personal care markets. The July 2025 merger with Berry Global expanded its global presence. Amcor has identified $20 billion in core consumer packaging solutions and is exploring alternatives for $2.5 billion in non-core assets. Innovations include AmFiber Performance Paper and a new sports closure for children’s drinks, highlighting sustainability and functional packaging.

Berry Global Group, Inc.: Expanding Circular Economy Initiatives Through Agile Manufacturing and Diversification

Berry Global offers rigid plastic containers, bottles, and jars across multiple sectors. Post-July 2025 merger with Amcor, the company enhanced its global footprint. Berry Global aims to integrate 30% circular plastics in FMCG packaging by 2030. Its core strengths include agile manufacturing capabilities, a diverse product portfolio, and a strong presence in healthcare. Capital investments include $20 million in a Kentucky facility, strengthening production capabilities.

Silgan Holdings Inc.: Strengthening European Footprint Through Strategic Acquisitions and Operational Efficiency

Silgan Holdings specializes in rigid plastic and metal containers, closures, and packaging solutions. In August 2025, the company completed a European acquisition, expanding its regional presence and capabilities. Silgan’s strategy emphasizes operational efficiency, consistent dividend payouts, and the “Fit to Win” initiative. Key offerings include custom-designed bottles, containers, and metal packaging for food and consumer applications.

Sonoco Products Company: Focusing on Core Rigid Packaging Capabilities and Sustainable Growth

Sonoco provides rigid plastic packaging, paper-based containers, and composite cans. Strategic divestitures, such as the April 2025 sale of Thermoformed and Flexibles Packaging, allow focus on core strengths. In July 2025, Sonoco announced a $30 million investment to expand adhesives and sealants capacity. Its portfolio emphasizes durable, eco-friendly packaging solutions, aligned with the “Better Packaging. Better Life.” initiative.

Sealed Air Corporation (SEE): Driving Automation, Digital Integration, and Net Positive Circular Packaging Solutions

SEE offers rigid plastic solutions under CRYOVAC® and LIQUIBOX® brands. Its “Net Positive Circular Ecosystem” strategy aims for 100% recyclable or reusable packaging by 2025. SEE integrates automation and digital solutions to create value, planning to double its automation portfolio by 2027, with 80% of sales expected to be digital. In August 2025, Kristen Actis-Grande was appointed CFO, reinforcing leadership stability.

Rigid Plastic Packaging Market Share Insights, 2025-2034

Bottles & Jars lead Market Share by Product Type in the Rigid Plastic Packaging Industry

Rigid plastic bottles and jars hold the largest share at 40%, making them the foundation of the global rigid plastic packaging industry. Their dominance is driven by sheer volume across beverages, sauces, condiments, shampoos, lotions, and household chemicals. Lightweight PET and HDPE have largely displaced glass, offering cost-effective, durable, and shatter-resistant solutions. Sustainability is now reshaping this category, with leading producers racing to incorporate recycled PET (rPET) and recycled HDPE (rHDPE) to meet circular economy targets. While trays, closures, and specialty containers grow steadily, bottles and jars remain the indispensable format for high-frequency consumer goods, ensuring their continued leadership despite rising environmental scrutiny.

Food & Beverages command Half of the Market Share by End-Use in the Rigid Plastic Packaging Industry

The food and beverages sector represents 50% of rigid plastic packaging demand, cementing its role as the largest and most indispensable application. The dominance stems from rigid plastic’s ability to deliver oxygen and moisture barriers, tamper evidence, resealability, and light weight, which are critical for preserving shelf life, ensuring food safety, and reducing logistics costs. From carbonated soft drinks to ready-to-eat meals, rigid plastics provide unmatched versatility at scale. Regulatory mandates and consumer expectations are pushing this segment toward recycled content integration and design-for-recyclability, but its fundamental reliance on plastic’s durability and cost-efficiency ensures that food and beverages will remain the market’s anchor end-use sector well into the future.

European Union: PPWR and ESPR Regulations Driving Rigid Plastic Packaging Transition

The European Union rigid plastic packaging market is being reshaped by the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. This regulation requires all plastic components in packaging to contain minimum percentages of recycled content recovered from post-consumer waste by January 2030, creating a strong push for circularity. It also establishes sector-specific reuse targets, promoting the adoption of rigid plastic bottles, crates, and pallets designed for multiple life cycles.

The Ecodesign for Sustainable Products Regulation (ESPR), effective since mid-2024, introduces the Digital Product Passport, ensuring full traceability of materials. Meanwhile, restrictions on PFAS in food contact packaging (effective August 2026) are driving the adoption of safer barrier technologies in rigid plastic containers. At the industry level, companies are innovating rapidly; for example, Amcor and Flügger’s launch of a paint container with 50% recycled content reflects the EU’s focus on blending sustainability with functional durability. Deposit Return Systems (DRS) are also expanding, providing high-quality recycled inputs essential for this sector.

United States: EPR Laws and Corporate Innovation Accelerating Rigid Plastic Packaging Adoption

In the United States rigid plastic packaging market, Extended Producer Responsibility (EPR) laws are gaining momentum, with seven states, including Maryland, mandating that Producer Responsibility Organizations (PROs) cover 90% of packaging waste management costs by 2030. These frameworks are driving systemic investment in circular packaging supply chains.

Corporate innovation is accelerating the transition. Berry Global has introduced a customizable rectangular bottle made with up to 100% post-consumer recycled (PCR) plastic, addressing sustainability needs in beauty, home, and personal care. Chlorophyll Water became the first U.S. bottled water brand to achieve Clean Label Project Certification by shifting to 100% rPET bottles. Likewise, Fresh Del Monte Produce’s partnership with Arena Packaging to use reusable plastic containers (RPCs) for bananas highlights how rigid formats help reduce food waste and emissions. Additionally, the U.S. market is preparing for closure-retention mandates, fueling the demand for rigid bottles with tethered caps, a trend merging regulatory compliance and consumer convenience.

China: Policy Reforms and Premium Food Demand Driving Rigid Plastic Packaging Market

The China rigid plastic packaging market is underpinned by strict environmental regulations and fast-evolving consumer demand. The NDRC and MEE are executing the “14th Five-Year Plan” with strong measures against plastic pollution, while new rules effective June 1, 2025 require express delivery companies to adopt eco-friendly, reduced, and reusable packaging. This is propelling demand for rigid packaging solutions in e-commerce and logistics.

At the same time, multinational brands are aligning with these initiatives. For instance, Coca-Cola in Hong Kong now produces bottles entirely from 100% rPET sourced in China, a clear example of closed-loop recycling in rigid plastics. Rising consumer appetite for premium food and beverage products is further accelerating the shift to high-quality rigid packaging solutions. Alongside, tax incentives supporting remanufacturing and green technology adoption are encouraging local players to expand their rigid plastic packaging portfolios.

India: EPR Mandates and Cold Chain Expansion Strengthening Rigid Plastic Packaging Market

The India rigid plastic packaging market is advancing under the Plastic Waste Management (Amendment) Rules, 2024, which enforce Extended Producer Responsibility (EPR) across producers, importers, and brand owners. Effective from April 1, 2025, PIBOs must include at least 30% recycled content in rigid plastics (Category I), significantly altering procurement and manufacturing strategies.

The FSSAI’s ongoing work on rPET food packaging guidelines is expected to boost safe applications of recycled content in beverages and dairy sectors. Parallelly, the government’s ethanol-blended fuel program is fueling demand for HDPE jerrycans and rigid fuel containers, while the PM Gati Shakti plan is spurring demand for PET preforms and rigid cold-chain containers. With high adoption of injection molding and thermoforming, India’s packaging manufacturers are scaling output for pharmaceuticals, dairy, and personal care industries, positioning rigid plastics as a backbone of the country’s packaging ecosystem.

Japan: Circular Economy and Bio-Based Innovation in Rigid Plastic Packaging

The Japan rigid plastic packaging market is guided by the Plastic Resource Circulation Strategy, which mandates that all packaging must be reusable or recyclable by 2025. Complementing this, the government aims to introduce 2 million tons of bio-polypropylene (bio-PP) annually by 2030, enhancing renewable inputs in rigid formats.

Collaboration is strong across the value chain. Companies such as LyondellBasell and Shiseido, in partnership with Futamura Chemical and Iwatani, are integrating bio-based PP into cosmetic rigid packaging. In parallel, the Plastic Resource Circulation Promotion Law (2025) enforces redesign of 12 single-use plastics, expanding opportunities for rigid alternatives like bio-PP containers. On the production front, Coca-Cola Bottlers Japan Inc. (CCBJI) has introduced an aseptic line at its Tokai Plant in Aichi Prefecture, capable of producing 600 PET bottles per minute, meeting surging domestic demand with recyclable rigid formats.

Brazil: Reverse Logistics and Waste Import Ban Reinforcing Rigid Plastic Packaging Market

The Brazil rigid plastic packaging market is shaped by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and reduction. A major development is Law No. 15,088 (January 2025), banning the import of solid waste, including plastics, to promote sustainable domestic waste management.

Brazil’s government is strengthening reverse logistics systems, making producers accountable for post-consumer rigid packaging recovery and recycling. These frameworks are pushing local companies to integrate recycled content into rigid bottles, trays, and containers. The food and retail industries are also increasing their use of MAP (Modified Atmosphere Packaging) and vacuum-sealed rigid trays to extend shelf life and reduce waste. Together, these measures are driving Brazil toward a more sustainable and self-sufficient rigid plastic packaging market.

Rigid Plastic Packaging Market Report Scope

Rigid Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$426.1 Billion

|

|

Market Size (2034)

|

$672.4 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material (Plastics), By Product Type (Bottles & Jars, Trays & Containers, Caps & Closures, IBCs, Drums & Pails, Blisters & Clamshells), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Cosmetics & Personal Care, Industrial, E-commerce, Chemicals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Silgan Holdings Inc., Sonoco Products Company, Ball Corporation, DS Smith Plc, Mondi Group, Greif, Inc., Crown Holdings, Inc., Huhtamaki Oyj, Pactiv Evergreen Inc., Orbis Corporation, Plastipak Holdings, Inc., Alpha Packaging, ProAmpac

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Plastic Packaging Market Segmentation

By Product Type

- Bottles & Jars

- Trays & Containers

- Caps & Closures

- IBCs

- Drums & Pails

- Blisters & Clamshells

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Cosmetics & Personal Care

- Industrial

- E-commerce

- Chemicals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Plastic Packaging Market

- Amcor plc

- Berry Global, Inc.

- Silgan Holdings Inc.

- Sonoco Products Company

- Ball Corporation

- DS Smith Plc

- Mondi Group

- Greif, Inc.

- Crown Holdings, Inc.

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Orbis Corporation

- Plastipak Holdings, Inc.

- Alpha Packaging

- ProAmpac

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, multi-faceted research methodology to deliver actionable insights into the global rigid plastic packaging market. Our approach combines exhaustive secondary research, including corporate reports, regulatory filings, sustainability disclosures, industry journals, and market intelligence studies, with primary interviews of key stakeholders such as manufacturers, brand owners, recyclers, and distributors across food & beverages, healthcare, personal care, cosmetics, chemicals, and e-commerce sectors. Market sizing and forecasting incorporate analysis of materials (PET, HDPE, bio-based plastics), product types (bottles, jars, trays, closures, drums), and regional regulatory influences including EU PPWR and ESPR, U.S. EPR frameworks, China’s green packaging mandates, India’s Plastic Waste Management rules, Japan’s Circular Economy initiatives, and Brazil’s PNRS. USDAnalytics also evaluates sustainability trends, lightweighting innovations, digital watermarking for traceability, vertical integration of recycling infrastructure, and monomaterial polymer barrier solutions. This integrated methodology ensures industry professionals gain a comprehensive understanding of market dynamics, competitive strategies, emerging technologies, and investment opportunities driving growth and circularity in the rigid plastic packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.