Single-Use Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Single-Use Packaging Market to Reach $84.2 Billion by 2034 Amid Rising Demand for Hygiene, Convenience, and Sustainability

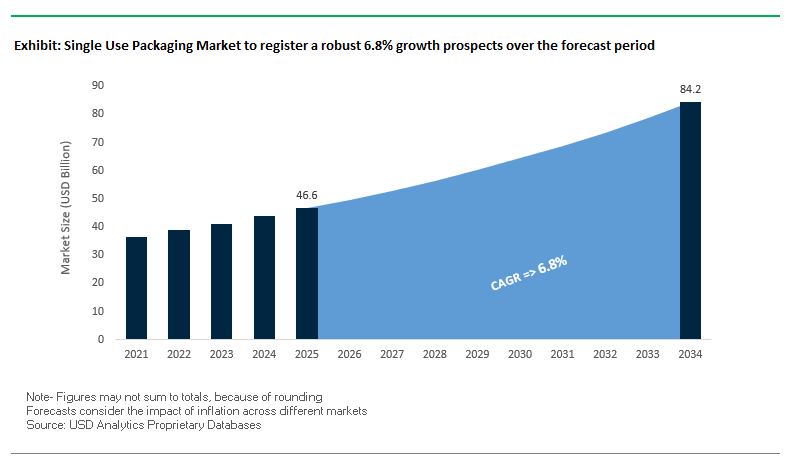

The global single-use packaging market is projected to grow from $46.6 billion in 2025 to $84.2 billion by 2034, reflecting a CAGR of 6.8%, driven by increasing consumer demand for hygiene, product safety, and on-the-go convenience across food, pharmaceutical, and personal care sectors. Single-use packaging is essential for protecting products, ensuring sterility, and maintaining freshness, while the industry simultaneously addresses environmental concerns and regulatory pressures.

Key Insights for Industry Professionals:

- Health and Safety Priorities: Single-use packaging provides a critical barrier against contamination, particularly important in food and pharmaceutical sectors.

- Innovation in Material Science: The market is moving toward bioplastics, paper, and paperboard alternatives, with paper-based solutions accounting for 38% of revenue in 2024.

- Consumer Convenience and E-Commerce Growth: Rising home delivery and online food services increase demand for durable, lightweight, and protective single-use formats.

- Regulatory and Environmental Pressures: Government bans and restrictions on plastics in regions like India and the EU are driving recyclable, compostable, and reusable solutions.

- Sustainability Integration: Companies are increasingly adopting circular economy principles, embedding eco-friendly packaging designs into product strategies.

Market Analysis: Recent Developments Highlight Industry Shifts Toward Sustainability, Innovation, and Strategic Collaborations

The single-use packaging market has experienced significant activity in sustainability initiatives, material innovations, and strategic partnerships, demonstrating a strong focus on efficiency, environmental responsibility, and market expansion. In August 2025, Klöckner Pentaplast was recognized for its kp 100% Tray2Tray® innovation, earning the German Packaging Award for new materials and underscoring the push for recyclable and eco-friendly packaging. The same month, Aquapak Polymers Ltd highlighted that 86% of FMCG brands are willing to pay a premium for sustainable packaging, reinforcing market alignment with consumer and industry sustainability expectations.

In July 2025, Amcor collaborated with Volpak and Menshen to launch an inverted pouch designed to enhance recyclability and reduce CO2 emissions, reflecting growing interest in innovative, eco-efficient packaging solutions. Earlier, in July 2024, Thermo Fisher Scientific introduced biobased films for single-use bioprocessing containers, certified by ISCC Plus, aiding biopharma manufacturers in operational efficiency while reducing environmental impact.

The market also witnessed strategic collaborations and circular economy initiatives, such as Chemco and Kandoi’s INR 450-crore JV in May 2025 for rPET projects, and the Danish-Indian 'From Beach to Big Bags' recycling initiative in March 2025, aimed at converting plastic waste into industrial-grade recycled polypropylene (rPP). Berry Global’s partnership with Mars in February 2025 to convert pantry jar packaging to 100% recycled plastic highlights a commitment to sustainability and reducing virgin plastic use. Additionally, the Lactips-Walki Group JDA in November 2024 and Constantia Flexibles’ Aluflexpack acquisition in October 2024 emphasize market consolidation and the adoption of innovative flexible packaging technologies.

Single Use Packaging Market: Regulatory Bans and Circular Innovation Driving the Future

Legislated Bans and Restrictions on Specific Material Formats

The single use packaging market is undergoing a structural transformation driven by global bans and restrictions on plastics that have low utility and high littering potential. India’s Plastic Waste Management (Amendment) Rules, 2021, implemented in July 2022, set a strong precedent by banning 19 categories of single-use plastics, including cutlery, straws, plates, and certain multilayer films. These restrictions have significantly impacted food service chains, quick-service restaurants (QSRs), and consumer goods companies, compelling them to transition to paper, compostable, or reusable formats to maintain compliance.

The regulatory crackdown is expanding worldwide. The European Union’s Directive on Single-Use Plastics, effective since July 2021, has eliminated plastic cutlery, plates, and straws across member states, while also imposing collection and recycling obligations on beverage bottles. More recently, in September 2025, South Australia introduced a ban on niche items like fish-shaped soy sauce bottles, signaling a growing focus on hard-to-recycle formats that contribute disproportionately to microplastic pollution. These cumulative policies are reshaping material demand in packaging supply chains and accelerating the replacement of banned products with paper, molded fiber, and biopolymer-based alternatives.

Corporate Investment in Reusable Packaging Infrastructure and Systems

Beyond material bans, corporations are proactively investing in reusable and refillable packaging systems as part of long-term circular economy strategies. Multinationals like Unilever are leading this transition with over 50 reuse and refill pilots globally, including in-store dispensing systems in Asia, refill pouches in Europe, and door-to-door services in South Asia. These initiatives reflect a fundamental shift away from single-use plastics, creating reusable loops designed to minimize waste while reducing reliance on fossil fuel-based polymers.

The growth of this segment is also driving the emergence of a “New Reuse Economy”, underpinned by reverse logistics networks for the collection, washing, and redistribution of reusable packaging. According to recent reports, multi-brand collection and sanitization hubs are being established in urban centers, designed to service multiple FMCG players and reduce costs through shared infrastructure. This systemic investment demonstrates how corporations are not merely replacing materials but building new business models and supply chain ecosystems that integrate sustainability as a core function.

Advanced Bio-Based and Marine-Biodegradable Polymers for Flexible Packaging

A major innovation opportunity for the single use packaging market lies in bio-based and marine-biodegradable polymers designed to close the loop on ocean plastic waste. Polyhydroxyalkanoates (PHAs) are gaining significant attention for their ability to biodegrade in marine environments, directly addressing the challenge of flexible packaging such as sachets and thin films, which are among the most problematic waste streams leaking into waterways.

Performance advancements are rapidly improving the commercial viability of these materials. Research published in scientific journals indicates that next-generation bio-based films are achieving low oxygen permeability and improved tensile strength, which are critical for food preservation and product protection. This combination of biodegradability and functional performance positions PHAs, polylactic acid (PLA), and blended bio-polymers as viable competitors to conventional plastics in sectors like foodservice, snacks, and personal care packaging. For industry players, this represents a first-mover advantage to capture regulatory and consumer-driven demand for sustainable flexible packaging solutions.

Digital Product Passports (DPPs) for Enhanced Traceability and EPR Compliance

The digitalization of packaging presents another powerful opportunity, with the EU’s Digital Product Passport (DPP) emerging as a regulatory driver of innovation. Introduced in July 2024 under the Ecodesign for Sustainable Products Regulation (ESPR), the DPP mandates that products carry a unique digital identifier (e.g., QR code or data carrier) linking to detailed information on material sourcing, recycled content, and disposal pathways.

For packaging producers and brands, DPPs provide a transparent framework to ensure Extended Producer Responsibility (EPR) compliance. A technical review highlights how DPPs allow companies to generate verifiable data on recycled content use and recovery rates, a critical step in proving adherence to EU PPWR and global EPR schemes. At the consumer level, this system empowers individuals to access instructions for proper disposal, thereby increasing recycling rates and reducing litter. For regulators and recyclers, DPPs create end-to-end traceability, enabling high-quality sorting, accurate reporting, and ultimately a data-driven circular economy for single-use packaging.

Competitive Landscape: Top Global Single-Use Packaging Companies Are Driving Sustainability, Innovation, and Market Consolidation

The single-use packaging industry is dominated by key global players that combine expertise in material science, sustainable innovations, and strategic acquisitions to deliver high-performance, eco-friendly packaging solutions.

Amcor PLC: Leading Global Innovations in Eco-Friendly and High-Performance Packaging

Amcor offers a broad portfolio of sustainable single-use packaging, including recyclable, reusable, and bio-based products for food, beverage, and healthcare applications. In July 2025, the company launched an inverted pouch with Volpak and Menshen to reduce CO2 emissions, and its Liquiflex AmPrima pouches in Europe offer up to 79% carbon footprint reduction. Amcor leverages a vertically integrated model, enabling efficient service across multiple industries while focusing on innovation, compliance, and market leadership.

Constantia Flexibles: Expanding Global Footprint Through Strategic Acquisition and Sustainable Packaging Solutions

Constantia Flexibles manufactures flexible packaging for pharmaceuticals and consumer goods, including blisters, pouches, trays, and containers. In October 2024, the company acquired Aluflexpack, enhancing its flexible packaging capabilities. Constantia emphasizes material innovation and sustainability, integrating eco-friendly solutions into its product portfolio to meet evolving market and regulatory requirements.

Berry Global Group, Inc.: Driving Circular Economy with Recycled and Reusable Packaging

Berry Global specializes in plastic packaging solutions for food, personal care, and healthcare sectors. In February 2025, Berry partnered with Mars to switch all pantry jar packaging for M&M'S, SKITTLES, and STARBURST to 100% recycled plastic, eliminating over 1,300 metric tons of virgin plastic annually. The company continues to invest in circular economy technologies, combining material innovation with a vertically integrated supply chain.

Huhtamaki Oyj: Pioneering Sustainable Food Packaging Through Innovative Fiber and Paper Solutions

Huhtamaki provides flexible, paperboard, and molded fiber packaging for food and beverage applications. The company recently launched Future Smart fiber lids, offering eco-friendly alternatives to traditional plastic lids. Huhtamaki emphasizes sustainability, material innovation, and a vertically integrated model to deliver high-performance packaging solutions globally.

Sealed Air Corporation: Innovating Protective Packaging Solutions with Circular Economy Principles

Sealed Air is a global leader in protective packaging, offering flexible films, foams, and paper-based materials. In August 2025, the company introduced Bubble Wrap® embossed paper, combining protection, sustainability, and recyclability. Sealed Air focuses on innovation, compliance, and circular economy adoption, leveraging brand recognition and manufacturing expertise to maintain global leadership.

Single Use Packaging Market Share Insights, 2025-2034

Pouches & Sachets Dominate Market Share by Product Type in the Single-Use Packaging Industry

Pouches and sachets command the largest share of the single-use packaging market at 30%, positioning themselves as the backbone of the global “sachet economy.” Their strength lies in affordability, lightweight structure, and minimal material usage, making them indispensable in both emerging and developed markets. In regions with lower incomes, sachets enable affordable access to branded products such as shampoos, condiments, and detergents, while in mature economies they cater to convenience-driven categories like snacks, nutraceuticals, and single-serve beverages. However, this dominance comes with environmental challenges: pouches and sachets are at the center of the plastic waste crisis, facing growing regulatory scrutiny and consumer pressure for eco-friendly alternatives. As a result, innovation in compostable polymers, recyclable mono-materials, and water-soluble formats is accelerating, positioning this segment as both the largest opportunity and the greatest challenge for the future of single-use packaging.

Food & Beverages Continue to Drive Market Share by End-Use in the Single-Use Packaging Industry

The food and beverages sector accounts for 60% of single-use packaging demand, making it the industry’s primary engine of growth and innovation. This dominance is tied to the essential role of packaging in ensuring food safety, extending shelf life, and enabling portion control. Single-use bottles, trays, cups, and flexible pouches are deeply embedded in global supply chains for packaged water, carbonated drinks, ready-to-eat meals, dairy products, and snacks. The sector’s reliance on barrier technologies to prevent oxygen and moisture ingress makes packaging indispensable, even as it becomes the main battleground for sustainability transformation. With governments tightening Extended Producer Responsibility (EPR) schemes and consumers demanding eco-friendly solutions, food and beverage brands are investing heavily in recyclable PET bottles, compostable coffee cups, and fiber-based trays. This balance between food security and environmental responsibility ensures that the sector not only sustains its share but also shapes the trajectory of sustainable single-use packaging innovation worldwide.

United States: Regulatory Bans and Smart Packaging Innovation

The United States single-use packaging market is undergoing a major transition as multiple states, including Maryland, Oregon, and Rhode Island, have enacted 2025 bans on single-use plastics such as foam containers and food service ware. These laws are compelling manufacturers to adopt plant-based plastics, paper-based flexible packaging, and recyclable mono-material solutions. Supporting this shift, the U.S. Environmental Protection Agency (EPA) has set an ambitious goal of increasing the national recycling rate to 50% by 2030, which is encouraging packaging companies to invest in advanced recycling infrastructure.

Industry players such as ProAmpac are introducing lightweight, recyclable solutions through portfolios like ProActive Recyclable®, targeting sectors such as snacks and food products. Meanwhile, the Association of Plastic Recyclers (APR) is shaping best practices by issuing guidance on washable inks and floatable films, enabling better recyclability for PET-based packaging. An important trend in the U.S. market is the integration of smart packaging features, including freshness indicators and QR-enabled traceability systems, which enhance consumer engagement, safety, and transparency while aligning with circular economy targets.

European Union: PPWR and ESPR Drive Circular Economy Standards

The European Union single-use packaging market is being redefined by the Packaging and Packaging Waste Regulation (PPWR), enforced in February 2025, which requires all plastic components of packaging to include minimum levels of post-consumer recycled content by 2030. This builds upon earlier mandates, including the Single Use Plastics Directive (SUPD) of July 2021, which banned items such as plastic cutlery and straws. Together, these frameworks are accelerating the shift toward mono-material flexible packaging and fully recyclable formats.

Complementing PPWR, the Ecodesign for Sustainable Products Regulation (ESPR), effective mid-2024, introduced the Digital Product Passport, requiring transparency on material composition, recyclability, and product origin. Another critical development is the ban on PFAS in food contact packaging from August 2026, which has triggered significant innovation in barrier coatings and alternative materials. Key industry responses include Huhtamaki’s recyclable paper cups, designed with less than 10% plastic content to comply with EU legislation. Additionally, industry consolidation, such as the Smurfit Kappa–WestRock merger, is enabling companies to expand their sustainable capacity across pan-European markets.

China: “Lazy Economy” and Stricter Regulations Accelerate Market Growth

The China single-use packaging market is shaped by both consumer demand for convenience and strict environmental regulations. Under the “14th Five-Year Plan”, the government is implementing strong controls on plastic pollution, including new June 2025 regulations requiring express delivery companies to adopt eco-friendly, reduced, or reusable packaging. A three-tiered system of laws, policies, and standards is in place to address waste from production to disposal, with results already visible in the food delivery and retail industries.

Consumer behavior is also critical, with the “Lazy Economy” driving premium demand for ready-to-eat meals, self-heating products, and luxury single-use formats. In response, manufacturers are leveraging advanced printing techniques, such as 3D platinum embossing and gold foil stamping, to enhance the visual appeal and security of packaging. Regulatory enforcement is intensifying, highlighted by Shanghai’s August 2025 policy, which fines restaurants and food delivery services using non-compliant disposable packaging, particularly targeting plastic-lined paper containers marketed as sustainable. This dual push of regulation and premiumization is accelerating innovation in sustainable single-use packaging solutions.

India: Traceability Mandates and Dairy Sector Demand Fuel Market Growth

The India single-use packaging market is expanding under the Plastic Waste Management (Amendment) Rules, 2024, which place heavy emphasis on Extended Producer Responsibility (EPR). From July 1, 2025, all plastic packaging in India must be traceable via barcodes or QR codes, ensuring accountability across the supply chain. While MSMEs are exempt, larger manufacturers and importers must comply with strict recycling and material-use obligations.

Growing retail and e-commerce sectors, coupled with government initiatives to boost dairy productivity, are fueling demand for affordable single-use packaging formats. These include portion packs for dairy, condiments, and processed foods. The market is therefore seeing strong interest in recyclable mono-material packaging, combined with lightweight formats designed for mass affordability. This blend of regulatory compliance and consumer demand is establishing India as one of the fastest-growing markets for traceable and sustainable single-use packaging.

Japan: Plastic Resource Circulation Strategy Accelerates Transition

The Japan single-use packaging market is undergoing a structural transition due to the Plastic Resource Circulation Strategy, which mandates that all plastic packaging must be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, targets the redesign of 12 single-use plastic categories, reinforcing the market’s shift toward compostable and paper-based alternatives.

Japan also aims to double renewable material use by 2030 and is strengthening waste-sorting enforcement to ensure higher recycling yields. Innovation is strong in this region, with companies such as Nippon Paper Industries developing advanced solutions like SHIELDPLUS paper, which incorporates a barrier layer against oxygen and odors. This material is a viable alternative for food-grade and sanitary single-use applications, positioning Japan as a hub for cutting-edge sustainable packaging materials.

Brazil: Reverse Logistics and Waste Reduction Targets Transform Market

The Brazil single-use packaging market is anchored by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and waste minimization. A pivotal reform came with Law No. 15,088, effective January 2025, banning the import of plastic and other waste materials to strengthen domestic sustainability initiatives. The government is also enforcing reverse logistics systems, requiring producers to manage the post-consumer recycling and disposal of their packaging.

An important development is a WWF-backed study, which showed that eliminating disposable plastics could cut Brazil’s waste generation by 3.2 million tons by 2040, while simultaneously strengthening its economy. These findings are pushing regulators and businesses to invest in eco-friendly single-use packaging while expanding domestic recycling infrastructure. With growing consumer awareness and strict regulations, Brazil is positioned as a leader in sustainable and circular single-use packaging adoption in Latin America.

Single Use Packaging Market Report Scope

Single Use Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$46.6 Billion

|

|

Market Size (2034)

|

$84.2 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Glass, Metal, Bioplastics), By Product Type (Bags, Pouches & Sachets, Bottles & Jars, Blister Packs, Cups & Lids, Trays & Clamshells, Tubes & Ampoules), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Household & Industrial, Retail & E-commerce)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamaki Oyj, Berry Global, Inc., Sealed Air Corporation, ProAmpac, Sonoco Products Company, Constantia Flexibles, Mondi Group, DS Smith Plc, WestRock Company, Winpak Ltd., Tetra Pak Inc., Greiner Packaging International GmbH, Klöckner Pentaplast, EPL Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Single Use Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

By Product Type

- Bags

- Pouches & Sachets

- Bottles & Jars

- Blister Packs

- Cups & Lids

- Trays & Clamshells

- Tubes & Ampoules

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Household & Industrial

- Retail & E-commerce

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Single Use Packaging Market

- Amcor plc

- Huhtamaki Oyj

- Berry Global, Inc.

- Sealed Air Corporation

- ProAmpac

- Sonoco Products Company

- Constantia Flexibles

- Mondi Group

- DS Smith Plc

- WestRock Company

- Winpak Ltd.

- Tetra Pak Inc.

- Greiner Packaging International GmbH

- Klöckner Pentaplast

- EPL Limited

* List Not Exhaustive

Methodology

USDAnalytics leverages a robust, multi-dimensional methodology to deliver actionable insights into the global Single-Use Packaging market. Our approach combines extensive secondary research from regulatory filings, industry reports, company disclosures, and sustainability databases with primary interviews of packaging engineers, R&D leaders, supply chain managers, and senior executives across food, beverage, pharmaceutical, and personal care sectors. Market sizing and growth forecasts are segmented by material type (Plastic, Paper & Paperboard, Glass, Metal, Bioplastics), product type (Bags, Pouches & Sachets, Bottles & Jars, Blister Packs, Cups & Lids, Trays & Clamshells, Tubes & Ampoules), and end-use industry (Food & Beverages, Healthcare, Personal Care, Household & Industrial, Retail & E-commerce), while also evaluating regional adoption trends in North America, Europe, Asia-Pacific, India, Brazil, and Japan. USDAnalytics further analyzes sustainability drivers, regulatory pressures, circular economy adoption, bio-based and marine-biodegradable polymers, and digital product passport integration for traceability and compliance. Competitive intelligence is built around strategic mergers, acquisitions, partnerships, and innovation by leading companies such as Amcor, Huhtamaki, Berry Global, and Constantia Flexibles, offering professional stakeholders a comprehensive understanding of growth opportunities, operational efficiency, and sustainable packaging strategies in the evolving single-use segment.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.