Market Overview: Kraft Paper and Flat-Bottom Bags Fuel Market Expansion

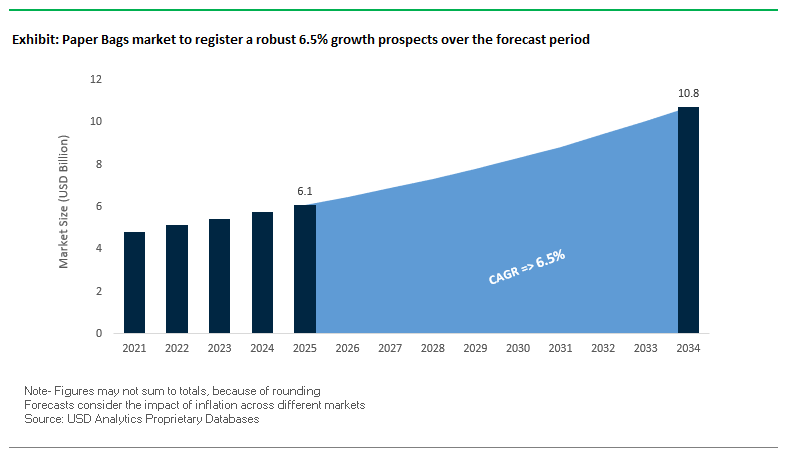

The global paper bags market is projected to reach USD 6.1 billion in 2025 and expand to USD 10.8 billion by 2034, registering a strong CAGR of 6.5%. This growth reflects the global shift away from single-use plastics, the rising need for eco-friendly and recyclable packaging, and strong demand from the retail, foodservice, and e-commerce industries. For industry professionals, the market outlook hinges on understanding how paper bag producers are innovating with barrier properties, automated production compatibility, and sustainability-driven product lines to align with both regulatory and consumer expectations.

Kraft paper dominates the sector, valued for its strength, durability, and recyclability, making it the preferred material across diverse industries. Flat-bottom paper bags are another high-demand segment, prized for their stability and capacity, especially in foodservice, grocery retail, and e-commerce delivery. The Asia-Pacific region leads in production and consumption, supported by government bans on plastic bags in China, India, and other markets. Overall, sustainability remains the key growth driver, with paper bags positioned as a mainstream alternative amid rising global environmental awareness.

Key Insights for Industry Professionals:

- Kraft paper leads as the dominant material for both industrial and retail applications.

- Flat-bottom bags capture significant demand from foodservice, retail, and e-commerce sectors.

- Plastic bans drive growth, with biodegradable and recyclable bags replacing single-use plastics globally.

- Asia-Pacific is the largest hub, driven by rapid urbanization and regulatory support.

Market Analysis: Recent Industry Developments Reshaping Market Dynamics

The paper bags industry is undergoing rapid transformation, led by major corporate acquisitions, material innovation, and sustainability-focused initiatives.

In August 2025, Mondi Group launched FunctionalBarrier Paper Ultimate, a high-barrier paper packaging solution, strengthening its position in sustainable packaging. In July 2025, IKEA Components announced it would replace plastic fitting bags with paper alternatives, reducing plastic use by 1,400 tons annually. The same month, Packaging Corporation of America (PCA) signed a USD 1.8 billion deal to acquire Greif’s containerboard business, boosting its access to raw materials. Also in July, Smurfit Westrock reported operational improvements tied to merger synergies in North America.

In April 2025, International Paper finalized its acquisition of a 66.3% stake in DS Smith, significantly reshaping the European and UK paper packaging landscape. Earlier, in March 2025, Mondi collaborated with Proquimia to launch paper-based pouches for dishwashing tabs, signaling diversification beyond traditional bag formats. In January 2025, Klabin introduced Wicket Paper Bags for diapers in Brazil, a fully recyclable alternative to plastic-based solutions. On the consumer goods side, PepsiCo’s April 2024 initiative to use paper outer bags for its Snack A Jacks multipacks cut virgin plastic usage by 65 tonnes annually.

Trends and Opportunities Reshaping the Paper Bags Market

Legislative Bans on Plastic Bags Driving Unprecedented Demand for Paper Alternatives

The paper bags market is being reshaped by sweeping government legislation banning single-use plastic bags, which has created a surge in demand for sustainable paper-based alternatives across retail, grocery, and foodservice sectors. India’s nationwide ban on single-use plastics, effective since 2022, and similar restrictions across China and the European Union, have positioned paper bags as the most viable large-scale substitute. Urban centers like Delhi and Mumbai have already reported a visible reduction in plastic consumption, with retailers rapidly switching to paper or cloth-based bags to comply with the law.

Corporates are also responding aggressively to align with these mandates and consumer expectations. IKEA Components announced it would replace plastic fitting bags with paper-based alternatives, a move projected to reduce plastic consumption by over 1,400 tons annually. Similarly, PepsiCo’s introduction of paper outer bags for multipack snacks will reduce virgin plastic use by 65 tonnes annually, reflecting the scale at which global brands are recalibrating packaging portfolios. These moves not only ensure compliance but also reinforce corporate ESG commitments. As bans expand globally, legislative pressure remains the single strongest catalyst behind the accelerated adoption of paper bags.

Innovation in Functional Coatings and Barrier Technologies for Non-Food Applications

Beyond traditional carry bags, the paper bags industry is undergoing a significant technological transformation as manufacturers develop functional coatings that improve moisture, grease, and air resistance. These advancements expand paper bags into non-traditional markets such as fast food, pet food, diapers, and industrial products, which were historically reliant on plastic or complex laminates.

Companies like Mondi are at the forefront, investing in production lines for their FunctionalBarrier Paper Ultimate, an ultra-high barrier paper that offers protection against oxygen and water vapor while remaining recyclable. Meanwhile, Klabin’s Wicket Paper Bag in Brazil is repulpable and recyclable, designed specifically for diapers a category long dominated by plastics. This expansion showcases the versatility of paper when paired with advanced coatings. Water-based, recyclable coatings are especially crucial, as they maintain recyclability while replacing unrecyclable plastic laminates. As brands seek functional yet sustainable alternatives, these innovations are opening entirely new market segments for paper bag adoption.

Development of High-Performance Recycled Fiber Content Bags

The circular economy shift is creating strong demand for paper bags with high post-consumer recycled (PCR) fiber content that do not compromise on tensile strength, printability, or load-bearing capacity. Retailers with strict sustainability mandates are prioritizing suppliers that can deliver paper bags made from recycled fibers at scale. For instance, Ecobags, highlighted by the UNFCCC, utilizes old newspapers and jute twine to produce biodegradable bags strong enough to carry 2.5 kilograms demonstrating both functionality and social impact by generating local livelihoods.

The Central Pollution Control Board (CPCB) in India has further accelerated this transition by mandating recycled content quotas from 2025, ensuring that PCR integration is not just a market preference but a regulatory requirement. Research shows that reverse logistics systems where packaging is collected, reprocessed, and reintroduced into supply chains are fueling the demand for high-quality recycled fibers. Manufacturers that successfully develop strong, visually appealing bags from high PCR content will gain a competitive edge, meeting corporate mandates while complying with evolving regulatory frameworks.

Integration of Digital Watermarking for Enhanced Sortation and Circularity

The integration of digital watermarking technologies offers a breakthrough opportunity for the paper bags market, addressing one of the biggest challenges in recycling: contamination in post-consumer waste streams. Through initiatives like HolyGrail 2.0, watermarks invisible to the naked eye are embedded into packaging and detected by high-resolution cameras at material recovery facilities (MRFs). This enables precise identification of paper bags, ensuring they are separated correctly and recycled into high-quality pulp.

Industrial trials under HolyGrail 2.0 demonstrated high detection efficiency even under real-world conditions, proving that watermarking is viable for scaling closed-loop recycling systems. This technology enhances recyclability by generating cleaner, higher-value fiber streams while simultaneously helping brands comply with Extended Producer Responsibility (EPR) regulations. It also provides a consumer engagement opportunity a scanned watermark can direct customers to sustainability information, instructions for proper disposal, or even brand storytelling platforms. By turning a paper bag into both a recycling enabler and a consumer touchpoint, watermarking positions paper packaging as a critical driver of the circular economy.

Competitive Landscape: Leading Companies in the Paper Bags Market

The global paper bags market is intensely competitive, with key players focusing on vertical integration, regulatory alignment, and material innovation to strengthen their global presence.

Mondi Group: Expanding High-Barrier Paper Packaging Capabilities

Mondi is a leader in kraft-based packaging solutions, offering paper bags for retail, food, and industrial applications. In August 2025, it invested €16 million to expand production of FunctionalBarrier Paper Ultimate in Poland. Mondi’s strategy revolves around its MAP2030 sustainability framework, targeting fully recyclable, compostable, or reusable packaging. Its vertical integration model, from forestry to bag conversion, ensures strong quality and supply chain reliability.

Smurfit Westrock plc: Optimizing Operations Post-Merger

Smurfit Westrock, formed from the Smurfit Kappa–WestRock merger, is a global leader in industrial and retail paper bags. In August 2025, it announced merger synergies that significantly improved operational efficiency, while in July 2025, it reported stronger North American performance. The company’s focus on footprint optimization and sustainability includes cutting 600,000 tons of non-strategic capacity, allowing it to realign with high-growth markets.

International Paper Company: Expanding Through Acquisitions

International Paper is a major producer of sustainable paper and corrugated bags. In April 2025, it acquired a 66.3% stake in DS Smith, strengthening its European presence. In August 2025, it announced the sale of its Global Cellulose Fibers division for USD 1.5 billion to streamline operations around packaging. International Paper’s strategy centers on sustainable forestry sourcing and consolidating its role as a leader in eco-friendly paper packaging.

Billerud AB: Investing in High-Performance Kraft Materials

Billerud focuses on sack and kraft papers for durable paper bag applications. Its ongoing investments in Michigan’s Escanaba and Quinnesec mills are key to its “Way Forward” strategy to expand U.S. operations. Known for lightweight yet strong papers, Billerud helps clients reduce material use without sacrificing durability. Its sustainability-driven model aligns with the EU Packaging and Packaging Waste Regulation (PPWR), making it a supplier of future-ready paper bag solutions.

DS Smith plc: Leveraging Circular Economy Expertise

DS Smith, now majority-owned by International Paper, brings a strong focus on circular packaging solutions. The company applies its “box-to-box in 14 days” model and Circular Design Metrics to optimize recyclability in paper bag manufacturing. DS Smith’s portfolio includes retail and e-commerce paper bags, positioning it as a key partner for sustainable logistics. Post-acquisition, DS Smith is expected to further integrate its circular design expertise with International Paper’s global scale.

Paper Bags Market Share Insights

Flat Bottom Bags Lead Paper Bags Market Share by Product Type

Flat bottom bags command the largest share of the global paper bags market at 30%, driven by their universal role in retail carryout across grocery chains, fashion outlets, and takeaway services. Their upright design and versatility make them the consumer-friendly option that has become synonymous with plastic bag bans worldwide. Sewn open-mouth bags follow closely, anchoring heavy-duty industrial and agricultural applications such as flour, cement, and animal feed, while pasted open-mouth and pinched bottom bags serve specialized needs for powders and premium products. Wicketed bags play a critical role in food and bakery automation, while pasted valve bags remain the niche choice for cement and building materials, where dust-free precision filling is vital. The leadership of flat bottom bags is further strengthened by advancements in durability, recycled content integration, and improved handle designs, ensuring their continued dominance in both retail and foodservice packaging markets.

Retail Sector Dominates Paper Bags Market Share by Application

Retail applications account for 35% of the global paper bags market, making this the largest and most visible end-use segment, fueled by legislative bans on single-use plastics and shifting consumer expectations for sustainable alternatives. Grocery stores, shopping malls, and fashion outlets rely heavily on paper bags not only as carryout solutions but also as branding tools with high-quality print surfaces. Food & beverages follow as a core driver, consuming paper bags for baked goods, produce, and food delivery, while agriculture depends on durable multi-wall bags for seed, fertilizer, and feed distribution. Building & construction remains a specialist segment dominated by pasted valve bags for cement and mortar, while chemicals, merchandise, and other industrial applications utilize paper bags with added protective linings for moisture and contamination resistance. The leadership of retail reflects the dual role of paper bags as both a regulatory-compliant packaging format and a visible symbol of brand commitment to sustainability.

United States: Rising Consumer Preference and E-Commerce Driving Sustainable Paper Bags

The U.S. paper bags market is witnessing strong growth due to evolving consumer preferences for eco-friendly packaging and governmental regulations aimed at reducing plastic waste. The implementation of state and local plastic bag bans and fees is a major catalyst for the shift from single-use plastics to recyclable and biodegradable paper bags. The boom in e-commerce and online retail further fuels demand, as businesses require durable and efficient packaging solutions for groceries, apparel, and other products.

Innovation is also transforming the market. Companies are developing reinforced handle paper bags, waterproof coatings, and advanced printing techniques to improve both durability and branding potential. These developments enable businesses to meet consumer expectations for sustainability and functionality, positioning paper bags as a preferred alternative for modern retail and e-commerce packaging solutions.

Germany: Regulatory Framework and Circular Economy Driving Eco-Friendly Paper Packaging

Germany’s paper bags market is influenced by stringent regulations such as the EU Packaging and Packaging Waste Regulation (PPWR) and the upcoming EU Deforestation Regulation (EUDR), effective end of 2025. These regulations enforce sustainable sourcing and recyclability standards, requiring manufacturers to implement due diligence systems for raw materials and ensure packaging is eco-friendly.

Germany’s leadership in the circular economy encourages high collaboration between manufacturers and end-users, with a strong focus on incorporating recycled content and developing packaging that aligns with national and EU sustainability targets. Technological innovation in production and eco-design also plays a pivotal role in delivering high-quality, sustainable paper bags suitable for diverse commercial applications.

China: Industrial Expansion and Automation Transforming Paper Bag Production

China’s paper bags industry is growing rapidly, driven by the country’s massive industrial expansion and increasing demand in food, retail, and e-commerce sectors. Manufacturers are investing heavily in automation and AI-powered machinery, such as fully automatic paper bag making machines capable of producing up to 1,200 bags per minute, meeting high-volume packaging requirements efficiently.

The governmental push for sustainability also contributes to growth. The new packaging regulations, effective June 2025, focus on reducing delivery waste, promoting recycled materials, and implementing reusable systems. These initiatives, combined with technological advancements, position China as a leading market for efficient, eco-friendly, and technologically advanced paper bag solutions.

India: Retail Growth and Sustainability Driving Demand for Paper Bags

India’s paper bags market is expanding rapidly due to governmental regulations like the Plastic Waste Management (Amendment) Rules, which phase out certain single-use plastics and promote sustainable alternatives. The surge in organized retail and e-commerce platforms is further increasing demand for durable, branded, and customizable paper bags for grocery and food delivery services.

Investments in domestic manufacturing are enhancing production capacity. Companies such as Bembi Group and VMG Paper Mills have expanded operations to meet growing market needs, while also integrating sustainable practices. This combination of regulatory support, retail growth, and investment in eco-friendly production strengthens India’s position as a fast-growing market for functional and environmentally responsible paper bag packaging.

Brazil: Legislative Push and Innovation Advancing Sustainable Paper Packaging

The Brazilian paper bags market is benefiting from strict legislation limiting single-use plastics, including the National Solid Waste Policy, which encourages reusable and eco-friendly packaging. The industry is embracing sustainability and innovation, exemplified by Klabin’s Wicket Paper Bag, a 100% recyclable and repulpable solution designed for products like diapers.

Strategic partnerships and collaborations, supported by studies from WWF-Brazil, further reinforce the market’s shift toward paper-based packaging. By reducing environmental pollution and promoting the circular economy, Brazil’s paper bags industry is advancing eco-friendly packaging solutions that align with both consumer expectations and government mandates.

Japan: Advanced Recycling and Functional Innovation Driving Paper Bag Adoption

Japan’s paper bags industry is distinguished by one of the world’s highest rates of waste paper and plastic collection and utilization, supported by the Plastic Resource Circulation Act. This robust recycling infrastructure enables the production of eco-friendly, circular packaging solutions.

Innovation in functionality is a key market driver. Companies like Oji Holdings are producing home delivery paper bags that are low-cost, water-repellent, and customizable with original designs, enhancing usability and brand visibility. Additionally, Rengo Co., Ltd. has introduced innovative solutions like the S-Lock Tray for fruit, optimizing material use while improving assembly efficiency. These developments highlight Japan’s focus on functional, sustainable, and technologically advanced paper bag solutions.

Paper Bags Market Report Scope

Paper Bags market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2034)

|

$10.8 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Flat Bottom Bags, Sewn Open Mouth Bags, Pinched Bottom Open Mouth Bags, Pasted Valve Bags, Pasted Open Mouth Bags, Wicketed Bags), By Material Type (Brown Kraft Paper, White Kraft Paper, Recycled Paper), By Application (Retail, Food & Beverages, Chemicals, Building & Construction, Agriculture, Merchandise, Other Applications), By End-Use Industry (Retail Stores, Food Service, E-commerce, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, International Paper, Smurfit Kappa Group plc, DS Smith Plc, Oji Holdings Corporation, Stora Enso, Novolex, Packaging Corporation of America (PCA), Huhtamäki Oyj, Klabin S.A., Rengo Co., Ltd., Segezha Group, BWAY Corp., WestRock, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Bags Market Segmentation

By Product Type

- Flat Bottom Bags

- Sewn Open Mouth Bags

- Pinched Bottom Open Mouth Bags

- Pasted Valve Bags

- Pasted Open Mouth Bags

- Wicketed Bags

By Material Type

- Brown Kraft Paper

- White Kraft Paper

- Recycled Paper

By Application

- Retail

- Food & Beverages

- Chemicals

- Building & Construction

- Agriculture

- Merchandise

- Other Applications

By End-Use Industry

- Retail Stores

- Food Service

- E-commerce

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Bags Market

- Mondi Group

- International Paper

- Smurfit Kappa Group plc

- DS Smith Plc

- Oji Holdings Corporation

- Stora Enso

- Novolex

- Packaging Corporation of America (PCA)

- Huhtamäki Oyj

- Klabin S.A.

- Rengo Co., Ltd.

- Segezha Group

- BWAY Corp.

- WestRock

- Greif, Inc.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global paper bags market, providing a detailed examination of recent breakthroughs, strategic developments, and market dynamics shaping the future of eco-friendly packaging. The analysis reviews key trends, including the rise of kraft paper and flat-bottom bag adoption, legislative bans on single-use plastics, and innovations in high-performance recycled fibers and barrier coatings. It highlights the transformative role of automation, digital watermarking, and circular economy initiatives in driving efficiency, sustainability, and regulatory compliance. The report further explores competitive strategies, mergers and acquisitions, and technological advancements by leading players, offering insights into material innovation, market penetration, and end-use sector growth. This report is an essential resource for industry professionals seeking to understand regional market trends, product innovations, and regulatory impacts, enabling informed decisions for strategic planning, investment, and supply chain optimization in the evolving paper bags landscape.

Scope Highlights:

- Segmentation: By Product Type (Flat Bottom Bags, Sewn Open Mouth Bags, Pinched Bottom Open Mouth Bags, Pasted Valve Bags, Pasted Open Mouth Bags, Wicketed Bags), By Material Type (Brown Kraft Paper, White Kraft Paper, Recycled Paper), By Application (Retail, Food & Beverages, Chemicals, Building & Construction, Agriculture, Merchandise, Other Applications), By End-Use Industry (Retail Stores, Food Service, E-commerce, Industrial Goods)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies, including Mondi Group, International Paper, Smurfit Kappa, DS Smith, Oji Holdings, and others

Methodology

The USDAnalytics study utilizes a combination of primary and secondary research methodologies to deliver an in-depth analysis of the paper bags market. Primary research involved interviews with industry stakeholders, including manufacturers, distributors, and retailers, to obtain firsthand insights into market trends, regulatory impacts, and technological adoption. Secondary research incorporated analysis of company reports, government regulations, trade journals, and industry publications to establish historical market data and forecast growth trajectories. Quantitative modeling techniques were applied to assess market size, product segmentation, and regional distribution, while qualitative assessments examined competitive strategies, innovation adoption, and sustainability initiatives. The methodology ensures a comprehensive understanding of market dynamics, enabling accurate forecasting and actionable insights for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.