Market Overview: Rising Demand for Sustainable and High-Performance Packaging

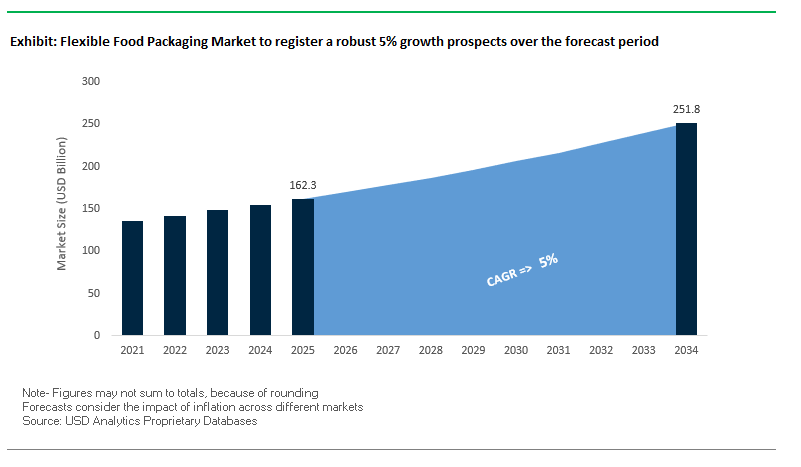

The Global Flexible Food Packaging Market is projected to expand from USD 162.3 billion in 2025 to USD 251.8 billion by 2034, growing at a CAGR of 5%. Flexible packaging has become a cornerstone of the modern food supply chain due to its ability to provide convenience, extended shelf life, reduced food waste, and lightweight efficiency. The market is undergoing a major transformation, driven by sustainability initiatives, high-performance barrier films, and the rise of e-commerce and food delivery channels.

A central trend is the sustainable shift toward recyclable, compostable, and PCR (post-consumer recycled)-content packaging. Consumer preference for eco-friendly packaging is now influencing every level of the supply chain, from material innovation to retail strategies. High-performance barrier films are also a defining feature, as they protect food from oxygen, light, and moisture, ensuring freshness and safety across categories such as fresh produce, dairy, snacks, and frozen meals.

The industry is equally shaped by its focus on lightweight materials, which significantly reduce both production emissions and logistics costs. With the rapid growth of e-commerce, flexible packaging is increasingly valued for its durability, low weight, and ability to minimize shipping damage. Brands are also adopting visually engaging designs, smart labeling, and interactive features to differentiate products on both retail shelves and online platforms.

Key Insights for Industry Professionals:

- Market value to rise from USD 162.3B (2025) → USD 251.8B (2034), CAGR 5%.

- Sustainable packaging with recyclable and compostable formats is a priority.

- Barrier films ensure shelf life extension and food safety.

- Lightweight packaging reduces costs and carbon footprint.

- E-commerce growth is fueling demand for protective, durable packaging.

Market Analysis: Recent Developments Driving Flexible Food Packaging

The Flexible Food Packaging Industry is witnessing accelerated innovation and strategic expansion, with companies focusing on sustainability, acquisitions, and advanced material technologies to secure leadership.

In September 2025, Henkel Adhesive Technologies announced it would showcase new recyclable and CO₂-reducing adhesive solutions at Labelexpo Europe, reflecting the demand for eco-friendly materials in flexible packaging. The following month, ProAmpac (August 2025) revealed its acquisition of PAC Worldwide, reinforcing its role in e-commerce fulfillment and protective packaging, both of which intersect with food packaging requirements.

Meanwhile, Sealed Air (August 2025) reported steady food packaging volumes but disclosed a strategic pivot toward retail channels to adapt to consumer purchasing shifts. In the same month, Mondi introduced its Ad/Vantage kraft paper, offering a sustainable paper alternative that could reduce plastic use in food packaging.

Two landmark mergers also reshaped the market in July 2025: the Amcor–Berry Global combination formed a dominant player in flexible and rigid packaging, while the Smurfit Kappa–WestRock merger created a global leader in paper-based packaging, influencing paper-based flexible formats. Also in July, Huhtamaki unveiled a recyclable and compostable ice cream packaging solution, strengthening its sustainable product pipeline.

Emerging Trends and Strategic Opportunities in the Flexible Food Packaging Market

Strategic Investment in Monomaterial Polyolefin-Based Structures

A defining trend in the flexible food packaging market is the industry’s rapid pivot toward monomaterial polyethylene (PE) and polypropylene (PP) structures. Traditional multi-layer laminates, which combine plastics, foils, and coatings, have long been incompatible with recycling streams, contributing to low global recovery rates for flexible packaging. The Ellen MacArthur Foundation highlights flexible packaging as the fastest-growing plastic segment but one of the least recycled due to its complex construction.

Major players are making bold moves to address this. Nestlé has committed up to CHF 2 billion to scale food-grade recycled plastics and accelerate innovation in recyclable packaging solutions. Packaging converters like Mondi are launching high-barrier mono-material packaging that balances performance—such as oxygen and moisture protection—with recyclability. These advances represent a major growth avenue, as food and beverage brands seek compliant packaging that aligns with EPR mandates and circular economy pledges.

The transition is also reshaping supply chains. To scale mono-material solutions, collaboration is intensifying between resin producers, converters, and CPG brands. Closed-loop partnerships are emerging to ensure high-quality recycled content and to optimize machinery for new material structures. For manufacturers, this shift not only delivers compliance but also creates long-term differentiation in a market prioritizing recyclability and circularity.

Integration of Advanced Digital Watermarking for Smart Sorting

Another trend accelerating change is the integration of digital watermarking technologies, such as those pioneered by the HolyGrail 2.0 initiative. Sorting challenges have long plagued flexible packaging due to contamination, multilayer complexity, and equipment tangling at material recovery facilities (MRFs). Digital watermarks provide an invisible code embedded in packaging that can be read by high-speed cameras, dramatically improving sortation accuracy.

Industrial-scale trials under HolyGrail 2.0, involving more than 130 companies across the packaging value chain, have shown detection rates of 99% and purity levels above 93%. This is a breakthrough for producing clean, segregated recycled streams, particularly separating food-grade from non-food-grade plastics. For CPG brands, this translates into higher recovery of valuable post-consumer material and stronger compliance with recycling targets.

The adoption of watermarking also creates a data-driven, interconnected value chain. Flexible packaging manufacturers, technology providers, and recyclers must collaborate closely to ensure seamless integration. For converters and brands, digital watermarks offer a way to future-proof packaging against rising EPR costs while enabling consumer engagement through scannable codes. This positions smart-sorting technologies as both a compliance enabler and a marketing tool in a circular economy.

Development of US Recycling Infrastructure Driven by Extended Producer Responsibility (EPR)

The passage of Extended Producer Responsibility (EPR) laws in U.S. states such as California, Maine, Oregon, and Colorado is creating a once-in-a-generation opportunity for the flexible food packaging sector. These laws mandate that producers bear financial and operational responsibility for packaging end-of-life, incentivizing the use of recyclable materials.

Maine’s 2021 EPR law for packaging marked the first U.S. milestone, and momentum is building across states. According to the Sustainable Packaging Coalition, these policies are accelerating investment in advanced sorting and recycling infrastructure. For brands and converters, the incentive is clear: designing recyclable flexible packaging reduces compliance fees and strengthens ESG positioning.

This policy-driven shift opens a high-value growth avenue for packaging manufacturers offering recyclable mono-material solutions and for recyclers scaling advanced processing facilities. The impact on the value chain is profound, requiring closer collaboration between brands, converters, and recycling organizations to ensure alignment on material compatibility and infrastructure readiness. For forward-looking players, EPR creates a competitive edge by embedding recyclability into product design and supply chain planning.

Adoption of High-Barrier Bio-Based & Compostable Films for Selective Applications

A parallel opportunity is the commercialization of bio-based and certified compostable films with advanced barrier properties, particularly for applications where food contamination limits recyclability. Examples include fresh produce wraps, salad bags, and tea bags, where compostable alternatives provide both functionality and sustainable disposal pathways.

R&D breakthroughs are enhancing the viability of these films. Studies on bacterial cellulose and modified biopolymers demonstrate oxygen barrier improvements and up to 84% reductions in water vapor permeability, while maintaining full biodegradability within 30 days in soil. Companies specializing in bioplastics are launching compostable solutions based on renewable feedstocks, with performance suitable for diverse food packaging uses.

The opportunity lies in targeting niches where compostable packaging provides a clear environmental and functional advantage, reducing food waste and eliminating reliance on single-use plastics. With consumer demand for plastic-free packaging surging and regulators tightening restrictions on difficult-to-recycle formats, compostable high-barrier films are positioned as a premium growth segment within the broader flexible food packaging market.

Competitive Landscape: Key Companies Defining Flexible Food Packaging

The Global Flexible Food Packaging Market is shaped by leading companies that are expanding their presence through strategic mergers, acquisitions, and innovation in sustainable packaging.

Amcor plc prioritizes global expansion and recyclable packaging solutions

Amcor is a global leader with a strong focus on sustainable innovation. In August 2025, it expanded its healthcare packaging operations in Costa Rica and launched an upgraded recycling facility in the UK, showcasing its operational and environmental commitments. Its AmPrima® recycle-ready solutions provide the performance of multi-layer laminates while being designed for recyclability. Amcor’s portfolio spans barrier films, vacuum bags, and flexible pouches, making it central to the global FMCG and food ecosystem.

Huhtamaki Oyj focuses on compostable and recyclable packaging innovation

Huhtamaki is at the forefront of sustainable innovation. In July 2025, it launched a new recyclable and compostable ice cream package, reinforcing its commitment to circular packaging solutions. Its blueloop™ portfolio is dedicated to flexible food packaging designed for recyclability. Huhtamaki’s products range from flexible films for ready meals to fiber-based on-the-go containers, making it a versatile leader in both consumer and foodservice markets.

Sealed Air Corporation pivots toward retail-focused sustainable packaging

Sealed Air, through its Cryovac® brand, is a trusted name in the protein and dairy sectors, offering barrier shrink films and vacuum bags that extend shelf life and reduce waste. In August 2025, it announced a strategic pivot to retail-focused channels, addressing shifting consumer purchasing trends. Sealed Air’s emphasis is on sustainability, automation, and recycled-content packaging, ensuring efficiency in e-commerce and omnichannel supply chains.

ProAmpac strengthens e-commerce and food packaging portfolio through acquisitions

ProAmpac is a fast-growing player with strong expertise in custom-engineered flexible packaging. In August 2025, it acquired PAC Worldwide, a move that strengthens its position in e-commerce protective and food packaging solutions. Its ProActive Recyclable® films offer sustainable drop-in replacements for conventional laminated structures, catering to snacks, frozen food, and pet food markets. ProAmpac’s strategy is built on combining sustainability and high-performance materials.

Constantia Flexibles expands sustainable packaging capabilities with Aluflexpack acquisition

Constantia Flexibles has reinforced its market position by acquiring Aluflexpack in August 2025, expanding its footprint in high-value packaging segments. Its Ecolutions® portfolio delivers recyclable mono-materials and high-barrier films that ensure food protection while supporting circular economy targets. With over €100 million invested in facility upgrades, Constantia is positioning itself as a leader in next-generation sustainable packaging solutions for food, pharma, and pet food sectors.

Flexible Food Packaging Market Share Insights

Pouches Retain the Largest Market Share by Packaging Type in Flexible Food Packaging

Pouches account for 35% of the flexible food packaging industry, positioning them as the most dynamic and adaptable format. Their high barrier properties, material efficiency, and consumer-friendly features allow them to replace rigid packaging across categories from snacks to pet food. Stand-up pouches, retort pouches, and spouted formats are increasingly utilized to deliver both convenience and sustainability advantages, with reduced plastic weight and improved recyclability. Their dominance is reinforced by rapid advances in mono-material structures and compostable films, enabling compliance with tightening sustainability regulations. As brands seek to balance cost reduction, shelf impact, and environmental responsibility, pouches will continue to lead market share in flexible packaging.

Snacks & Savories Hold the Largest Market Share by End-Use in Flexible Food Packaging

Snacks and savories represent 25% of demand in the flexible food packaging market, reflecting their high consumption frequency, global retail penetration, and rapid product innovation cycles. This segment requires advanced packaging that delivers moisture and oxygen barriers to maintain crispness and flavor integrity while also enabling strong shelf visibility. Flexible packaging formats such as metallized pouches and laminated films have become indispensable in snack applications, where visual appeal and extended freshness directly influence purchasing decisions. Moreover, the rise of portion-controlled packs, resealable zippers, and single-serve snack sizes further amplifies demand for flexible packaging. This consistent innovation ensures that snacks and savories remain the largest and most influential end-use driver in the market.

United States Flexible Food Packaging Market Driven by EPR Regulations and Smart Packaging Innovations

The U.S. flexible food packaging market is witnessing strong growth, propelled by federal and state-level regulations, including Extended Producer Responsibility (EPR) laws, which shift recycling and waste management costs from taxpayers to manufacturers. These regulations are incentivizing companies to develop mono-material pouches and other sustainable formats that reduce material complexity and enhance recyclability. Technological advancements, such as smart packaging with integrated QR codes and NFC chips, are improving supply chain traceability and consumer engagement by providing detailed product information and interactive experiences.

Corporate investments are fueling market expansion, with Sonoco Products Co. announcing a $30 million facility expansion in August 2025 to increase sustainable adhesive packaging production with a focus on flexible food formats. Key applications are concentrated in e-commerce, direct-to-consumer (DTC), and food & beverage sectors, where lightweight and robust packaging ensures product protection during shipping. Sustainability remains a strategic priority, with bio-based films and recyclable paperboard gaining adoption to meet consumer demand for environmentally responsible packaging solutions.

Germany Flexible Food Packaging Market Strengthened by Regulatory Compliance and Circular Economy Leadership

Germany’s flexible food packaging market operates under strict regulatory mandates, including the EU Packaging and Packaging Waste Regulation (PPWR) enforced in February 2025. This regulation requires all packaging to be fully recyclable or reusable by 2030, with strict limits on recycled content and chemicals such as PFAS in food-contact materials. The country’s Extended Producer Responsibility (EPR) system drives innovation in recycling and sorting, encouraging manufacturers to design packaging that is easier to recycle while meeting consumer demand for reusable containers and trays.

Technological innovations are gaining prominence, including digital product passports and watermarks that improve material transparency and recycling efficiency. Industry recognition, such as the German Packaging Award 2025, highlights sustainable flexible packaging innovations. Corporate developments, such as Amcor showcasing its CleanStream technology with mechanically recycled polypropylene at Fachpack Expo 2025, demonstrate strong market momentum. The market’s key applications are retail and food service sectors, where high-barrier films ensure extended shelf life for premium products.

China Flexible Food Packaging Market Expanding Through Green Policies and Technological Advancements

China’s flexible food packaging market is being accelerated by the government’s “dual carbon” goal and initiatives like the March 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement, which encourage the use of sustainable materials and recycling practices. Regulatory reforms effective September 2023, limiting packaging layers and void ratios, directly impact e-commerce packaging, a major channel for flexible food products.

Technological investments, including AI, 5G-enabled industrial internet, and automation, are optimizing production efficiency and flexible manufacturing capacities. Domestic manufacturing is expanding to reduce reliance on imported technologies, with local companies meeting the growing demand for high-quality, circular packaging. Key applications include ready-to-eat foods, e-commerce deliveries, and the food and beverage sector, with online grocery deliveries forecasted to drive substantial growth in flexible packaging volumes.

India Flexible Food Packaging Market Propelled by Circular Economy Initiatives and Local Manufacturing

India’s flexible food packaging market is benefiting from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which ensure safe, food-grade materials and prohibit the use of recycled plastics for food contact. Technological adoption of automated production systems is increasing, enabling cost-effective and efficient solutions across various applications.

Corporate investments are on the rise, exemplified by the launch of ProDairy, a recyclable single-coated paper cup for yogurt, reducing plastic content below 10%. Demand is being driven by the expanding food and beverage and personal care sectors, along with the growth of e-commerce and consumer preference for sustainable packaging. The domestic food processing industry and “Make in India” initiative are fostering local manufacturing and innovation, supporting the development of modern, high-performance flexible food packaging solutions.

Japan Flexible Food Packaging Market Innovating Through High-Performance Films and Cross-Industry Collaborations

Japan’s flexible food packaging market is a leader in precision manufacturing and sustainable packaging, with innovations such as Toppan Inc.’s recycled BOPP film developed in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc. in September 2024. Regulatory guidance from the Plastic Resource Circulation Act, effective April 2022, promotes environmentally conscious design and reduces single-use plastics, aiming to introduce 2 million tonnes per year of bio-based plastics by 2030.

High-performance films with superior barrier properties, IoT-enabled tracking, and digital printing are driving innovation. Functional enhancements like easy-open tear notches and resealable closures are addressing demographic shifts, including aging populations and single-person households. Cross-industry collaborations, such as LyondellBasell’s partial incorporation of bio-based PP into Shiseido’s packaging, illustrate the trend of integrating sustainable materials across sectors while advancing flexible food packaging technologies.

Flexible Food Packaging Market Report Scope

Flexible Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$162.3 Billion

|

|

Market Size (2034)

|

$251.8 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Packaging Type (Pouches, Bags, Films, Wraps, Others), By Material Type (Plastics, Paper & Paperboard, Foils, Bioplastics), By End-Use Industry (Bakery & Confectionery, Dairy Products, Meat, Poultry, & Seafood, Ready-to-Eat Meals, Snacks & Savories, Pet Food, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, International Paper Company, DS Smith plc, WestRock Company, Sonoco Products Company, Sealed Air Corporation, Crown Holdings Inc., Ardagh Group, Ball Corporation, Billerud AB, Graphic Packaging Holding Company, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Food Packaging Market Segmentation

By Packaging Type

- Pouches

- Bags

- Films

- Wraps

- Others

By Material Type

- Plastics

- Paper & Paperboard

- Foils

- Bioplastics

By End-Use Industry

- Bakery & Confectionery

- Dairy Products

- Meat, Poultry, & Seafood

- Ready-to-Eat Meals

- Snacks & Savories

- Pet Food

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Food Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- International Paper Company

- DS Smith plc

- WestRock Company

- Sonoco Products Company

- Sealed Air Corporation

- Crown Holdings Inc.

- Ardagh Group

- Ball Corporation

- Billerud AB

- Graphic Packaging Holding Company

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-faceted methodology to deliver an authoritative analysis of the Global Flexible Food Packaging Market. Our approach combined primary research, including interviews with packaging manufacturers, supply chain experts, and sustainability professionals, with comprehensive secondary research from corporate reports, trade publications, regulatory filings, and industry journals. Quantitative forecasting models were developed to assess market growth by packaging type, material, and end-use industry, while qualitative insights evaluated emerging trends such as mono-material recyclable structures, high-barrier compostable films, digital watermarking, and smart labeling for e-commerce. Regional dynamics, including U.S. EPR mandates, EU packaging regulations, and China’s green policies, were carefully analyzed, alongside strategic corporate developments like mergers, acquisitions, and innovative product launches. USDAnalytics also assessed technological adoption, material innovations, and sustainability initiatives, ensuring that industry professionals gain actionable intelligence for strategic decision-making, operational planning, and product development in the rapidly evolving flexible food packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.