Market Overview: Rising Demand for Sustainable and High-Performance Films

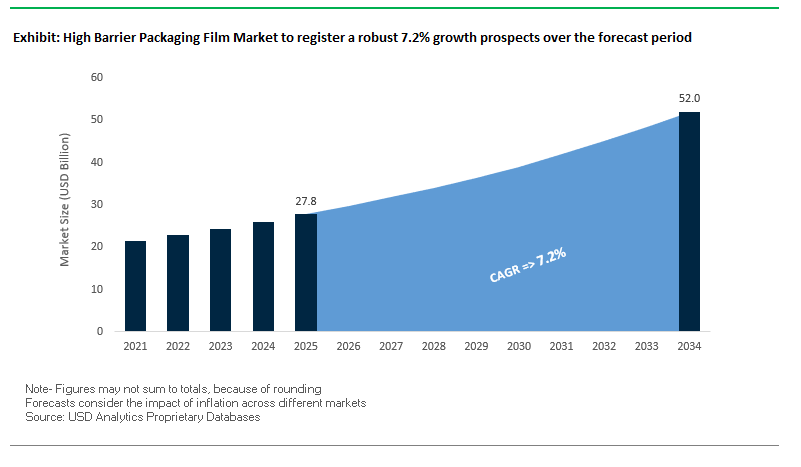

The Global High Barrier Packaging Film Market is valued at USD 27.8 billion in 2025 and is projected to reach USD 52 billion by 2034, growing at a CAGR of 7.2%. High barrier films are multi-layered protective packaging materials that safeguard products from oxygen, moisture, UV light, and contaminants. They are widely used across food & beverages, pharmaceuticals, pet food, and electronics, enabling extended shelf life, product integrity, and compliance with safety regulations.

The sector is undergoing a major transformation driven by consumer lifestyle changes, stricter regulatory frameworks, and sustainability targets. With the rising consumption of ready-to-eat meals, frozen foods, and convenience products, the demand for high barrier films has surged to preserve nutritional value and freshness while reducing food waste. The pharmaceutical industry also heavily relies on these films to protect sensitive drugs and single-dose medications from degradation.

Innovation is another key growth enabler. Mono-material recyclable films are gaining traction as companies move away from non-recyclable laminates. At the same time, smart packaging technologies such as QR codes, RFID tags, and time-temperature indicators are being integrated into high barrier films to enhance transparency, improve supply chain traceability, and strengthen consumer trust.

Key Insights for Industry Professionals:

- Market Value: USD 27.8B (2025) → USD 52B (2034).

- Growth Driver: Rising demand for convenience food and pharmaceutical packaging.

- Sustainability Push: Shift toward mono-material recyclable films replacing complex laminates.

- Technology Integration: Smart packaging features enabling real-time freshness monitoring.

- Strategic Focus: Lightweighting and bio-based materials for lower carbon footprint.

Market Analysis: Recent Developments Driving Innovation and Sustainability

The Global High Barrier Packaging Film Market has witnessed a series of strategic moves, acquisitions, and product innovations that underline its strong focus on circular economy practices, material science advancements, and consolidation among packaging leaders.

In January 2025, Jindal Films expanded its Brindisi, Italy plant with a new metallizer installation, boosting capacity for recyclable high barrier films. By March 2025, the pharmaceutical sector emphasized the adoption of flexible lid stock for single-dose medications, supporting safer dosage control and compliance with evolving healthcare regulations.

In June 2025, Mondi and Saga Nutrition launched a sustainable paper-based pet food solution, expanding the use of eco-friendly alternatives in high-performance barrier applications. The following month, Amcor and Berry Global Group completed their all-stock merger (July 2025), creating a new global packaging leader in flexibles and rigid containers. Parallelly, Amcor upgraded its Heanor, UK recycling facility (August 2025), adding capacity for 2,800 tonnes of recyclate annually, strengthening Europe’s circular packaging infrastructure.

At the same time, Ester Industries (September 2025) highlighted eco-friendly polyester films at the 12th Specialty Films & Flexible Packaging Summit in Mumbai, while LyondellBasell collaborated with Futamura Chemical and Iwatani Corporation (September 2025) to develop bio-based cosmetic film packaging.

Key Innovations and Growth Opportunities Driving the High Barrier Packaging Film Market

Commercialization of Recyclable High-Barrier Mono-Material Films

The high barrier packaging film market is undergoing a pivotal shift toward recyclable mono-material polyolefin films (PP or PE), moving away from complex, multi-layer laminates such as PET/ALU/PE or NY/EVOH/PE. This trend is driven by global sustainability initiatives, consumer demand for circular packaging, and regulations like the European Packaging and Packaging Waste Regulation (PPWR). These mono-material structures incorporate innovative coatings and additives to achieve ultra-high barrier performance, critical for protecting sensitive products including coffee, snacks, and sterilized medical devices. Companies like Mondi and ExxonMobil are leading the charge, offering high-barrier, recyclable PE/PP films engineered for existing production lines, enabling brands to transition seamlessly to sustainable packaging. Major consumer brands, including Nestlé, are piloting mono-material films for products like KitKat, signaling strong market adoption. This trend is reshaping the value chain, requiring close collaboration between resin producers, film converters, and brand owners to ensure high-performance, cost-effective solutions while meeting sustainability targets.

Adoption of Transparent Oxide Barrier Coatings to Replace Foil

The demand for product visibility combined with ultra-high barrier protection is driving the adoption of transparent aluminum oxide (AlOx) and silicon oxide (SiOx) coatings. Applied via vacuum deposition, these glass-like films offer exceptional oxygen and moisture barriers while allowing consumers to see the product, a critical factor for premium food items and microwavable packaging. Companies like Mitsubishi Chemical and leading film manufacturers are commercializing AlOx- and SiOx-coated PET films, providing a sustainable alternative to traditional aluminum foil laminates without compromising shelf life. Academic studies demonstrate that optimizing substrate materials and deposition parameters can maximize barrier performance, ensuring these films meet stringent industry requirements. The transparency of these films enhances product appeal, marketing effectiveness, and recyclability, creating a high-value growth avenue for both snacks, coffee, dried fruits, and other sensitive products.

Development of High-Barrier Films for Dry Pharmaceutical Blister Packaging

A significant growth opportunity exists in high-barrier polymer films replacing cold-formed aluminum (CFA) blisters for moisture-sensitive pharmaceuticals. Transparent polymer blisters allow visual inspection, reduce packaging weight by over 70%, and improve patient accessibility, especially for elderly or arthritic patients. Achieving a moisture vapor transmission rate (MVTR) below 0.1 g/m²/day is critical for drug stability, challenging but achievable with advanced polymer composites like poly(D,L-lactide) or PET with added barrier layers. By providing patient-friendly, lightweight, and sustainable packaging, manufacturers can enhance brand value and reduce costs—reports indicate potential material savings of up to 20% with smaller, more compact blister packs. This opportunity fosters closer collaboration between film producers and pharmaceutical companies, promoting innovation in sustainable, high-performance packaging.

Bio-Based and Compostable High-Barrier Films for Fresh Foods

The shift toward bio-based and compostable high-barrier films presents a key opportunity for modified atmosphere packaging (MAP) of fresh produce, meats, and cheeses. Polymers like PLA, PHA, or cellulose derivatives, enhanced with additives such as nanocellulose, can achieve the required oxygen and moisture barriers while being certified for industrial composting. This addresses consumer and corporate demand for truly sustainable packaging and creates a circular end-of-life pathway where traditional recycling is not feasible. Research from institutions like BARC, India, shows that bio-based films can match conventional plastics in mechanical and barrier performance, demonstrating their commercial viability. The development of compostable films opens a high-value growth avenue, enabling manufacturers to appeal to eco-conscious brands and integrate renewable raw materials into a sustainable supply chain, ultimately reducing reliance on petroleum-based plastics and promoting a circular economy.

Competitive Landscape: Global Leaders in High Barrier Packaging Films

The competitive landscape is shaped by large multinational corporations and innovative flexible packaging specialists, all aiming to deliver recyclable, high-performance films for diverse applications.

Amcor plc expands global footprint with sustainable packaging solutions

Amcor is a global leader with an extensive portfolio of AmLite Recyclable and AmPrima® recycle-ready films. In August 2025, Amcor upgraded its UK recycling site and expanded its healthcare packaging operations in Costa Rica. The July 2025 merger with Berry Global further cemented its dominance. Amcor’s strategic focus is to make all packaging recyclable or reusable by 2025, with an emphasis on mono-material solutions that deliver multi-layer performance.

Sealed Air Corporation strengthens CRYOVAC® brand in food packaging

Sealed Air is best known for its CRYOVAC® high barrier films, which extend shelf life and reduce food spoilage. Its innovations include Barrier Display Films (BDF) that balance durability, clarity, and protection. Sealed Air has also developed ultra-thin films to reduce plastic consumption while maintaining barrier strength. Its core strategy is to support food safety and minimize waste through high-performance yet sustainable packaging.

Huhtamaki Oyj drives circularity through blueloop™ solutions

Huhtamaki offers a broad range of flexible high barrier films for food, pet care, and pharmaceuticals. Its blueloop™ portfolio of sustainable flexible packaging is central to its 2030 circularity goals. In 2024, it launched new high-performance recyclable films aligned with its ambition of making all packaging recyclable, compostable, or reusable by 2030. Huhtamaki’s competitive edge lies in its global footprint and strong customer partnerships.

Berry Global Group, Inc. accelerates innovation through Amcor merger

Berry Global is a pioneer in circular polymers and recyclable film packaging. The July 2025 merger with Amcor established a new industry leader in flexible films. In late 2024, Berry partnered with VOID Technologies to launch recyclable pet food films. Its strength lies in combining circular material innovation with advanced processing technologies, ensuring long-term leadership in sustainable high barrier packaging.

ProAmpac delivers high-performance recyclable barrier films

ProAmpac specializes in flexible packaging solutions with a strong focus on recyclability and performance. Its innovations include ProActive Recyclable RP-1000HB and RT-4000 recyclable retort films, which balance oxygen resistance, heat tolerance, and recyclability. ProAmpac’s strategy is to deliver high barrier performance without compromising sustainability, making it a preferred partner for food, medical, and pet care industries.

High Barrier Packaging Film Market Share Insights

Oxygen Barrier Films Dominate Market Share by Barrier Type in High Barrier Packaging Film Industry

Oxygen barrier films hold the largest share of the high barrier packaging film industry at 50% in 2025, cementing their role as the most critical layer in extending product shelf life and preserving quality. Oxygen ingress is the leading cause of food spoilage, rancidity in oils, nutrient degradation, and microbial growth, making oxygen control the top priority for packaged foods, beverages, and sensitive pharmaceuticals. These films are integral to applications such as vacuum-sealed meats, coffee pouches, and pharmaceutical blister packs, where maintaining integrity directly impacts safety and consumer trust. Moisture barrier films, while slightly smaller in share, remain indispensable for products like baked goods, powdered foods, and nutraceuticals that are highly sensitive to water vapor transmission. Meanwhile, UV barrier films serve specialized but high-value niches by protecting light-sensitive products such as milk, juices, cosmetics, and biologics, where preventing vitamin degradation, discoloration, or potency loss is vital. Collectively, this segmentation reflects how oxygen barriers dominate as the primary safeguard against spoilage, while moisture and UV barriers provide essential complementary protection in specialized categories.

Food and Beverages Secure the Largest Market Share by Application in High Barrier Packaging Films

The food and beverages segment commands 70% of demand for high barrier films in 2025, reinforcing its status as the engine of this market. Packaging innovation in this sector focuses on minimizing food waste, extending shelf life, and ensuring food safety, with barrier films applied in Modified Atmosphere Packaging (MAP), vacuum packs, and aseptic packaging. This dominance is linked to rising global consumption of packaged snacks, meats, cheeses, dairy products, and ready-to-eat meals, all of which rely on precise oxygen and moisture control. Pharmaceuticals and healthcare represent the next most critical segment, accounting for 20% of the market, where high barrier films protect drug potency, sterility, and packaging compliance with global standards such as USP Class VI and FDA regulations. Cosmetics and personal care adopt barrier films to protect creams, fragrances, and serums from oxidation and volatilization, while industrial sectors utilize them for electronics and sensitive chemicals. This segmentation demonstrates how food and beverages anchor mass demand, pharmaceuticals drive regulatory-driven innovation, and cosmetics expand adoption through premium preservation needs.

United States High Barrier Packaging Film Market Accelerates with Sustainable and Innovative Solutions

The U.S. high barrier packaging film market is strongly influenced by a fragmented regulatory landscape, including California’s SB-54 Extended Producer Responsibility (EPR) law, which mandates a 25% plastic reduction by 2032 and establishes a $5 billion waste fund. This regulation indirectly drives the adoption of sustainable high barrier films as alternatives to traditional plastics. Technological advancements are prominent, with Amcor introducing its AmFiber Performance Paper, a recyclable high-barrier laminated paper compatible with flow wrap machinery, demonstrating the shift toward mono-material films for improved recyclability.

Corporate investments are reshaping the market, with Amcor’s planned acquisition of Berry Global Group expected to enhance R&D capabilities and scale sustainable packaging solutions. Key applications include food and beverage, pharmaceuticals, and e-commerce sectors, with online food delivery fueling the demand for robust, lightweight, and protective packaging. Sustainability remains a core focus, with eco-friendly materials, bio-based films, and recyclable paperboard meeting both regulatory requirements and consumer preferences.

Germany High Barrier Packaging Film Market Leads with Circular Economy and Regulatory Compliance

Germany’s high barrier packaging film market is driven by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates fully recyclable or reusable packaging by 2030 and restricts harmful chemicals like PFAS. Technological innovation is key, with firms such as Klöckner Pentaplast launching next-generation MAP trays like kp Elite® Nova, combining lightweight design with performance for high-value food products.

Leadership in the circular economy is supported by Germany’s Packaging Act (VerpackG), which incentivizes recyclable packaging designs and reusable containers through modulated fees. The market is particularly strong in food, beverage, and medical sectors, bolstered by a robust manufacturing base and strong export activities for specialty foods and pharmaceuticals. Companies continue to invest in R&D and production technologies to meet both regulatory standards and sustainability goals.

China High Barrier Packaging Film Market Expands Through Government Policies and Domestic Innovation

China’s high barrier packaging film market is being transformed by governmental initiatives aligned with the “dual carbon” goal, promoting sustainable materials and industrial upgrades. The revised national standard, GB/T 31268, effective November 2024, limits excessive packaging, directly impacting e-commerce and consumer goods packaging.

Technological advancements, including automation, AI integration, and “5G plus industrial internet,” are optimizing production processes and enhancing flexible manufacturing capacity. Corporate investments, such as Dow’s collaboration with Mengniu to launch mono-material PE yogurt pouches, highlight a focus on higher recyclability and circular economy practices. Domestic manufacturing expansion is a key trend, driven by growing demand for high-quality, sustainable packaging in food and beverage sectors.

India High Barrier Packaging Film Market Boosted by Circular Economy Initiatives and Domestic Manufacturing

India’s high barrier packaging film market is benefiting from government policies supporting a circular economy, including the draft Environment Protection (Extended Producer Responsibility for Packaging) Rules, 2024. The market sees strong adoption of automated printing systems and specialized film manufacturing to meet growing demand in frozen foods, snacks, and packaged vegetables.

Corporate investments are increasing, with UFlex pioneering aluminum-free laminates and bio-based films, signaling strong sustainability focus. Key applications include food processing, personal care, and e-commerce packaging, driven by the country’s expanding domestic market. The Make in India initiative further strengthens local manufacturing, innovation, and technological development, positioning India as a rising player in high barrier packaging films.

Japan High Barrier Packaging Film Market Focuses on High-Performance and Functional Packaging

Japan’s high barrier packaging film industry leverages advanced precision manufacturing and next-generation production ecosystems. Regulatory guidance from the Plastic Resource Circulation Act, effective April 2022, promotes sustainable material usage and reduces single-use plastics, driving adoption of eco-friendly high barrier films.

The market emphasizes high-performance and value-added films, with innovations such as IoT-enabled tracking, easy-open tear notches, and resealable closures to serve aging populations and single-person households. Companies like Toppan Inc. are advancing sustainable recycled BOPP films for mass production, reflecting Japan’s commitment to combining functionality with sustainability.

South Korea High Barrier Packaging Film Market Strengthened by Technical Innovation and Export Competitiveness

South Korea’s biaxially oriented film (BOPP) industry is undergoing strategic transformation, emphasizing technical innovation in optical, electronic, and new energy films. Leading companies such as SK Microworks and Kolon Industries are collaborating to maintain a competitive position against Chinese rivals in specialty films.

The market is largely driven by electronics and automotive sectors, with a shift from LCD to OLED displays increasing demand for high-performance display and optical films. South Korean manufacturers focus on value-added products, with ultra-thin films supporting electric vehicle applications. Strong export performance of cars, electronics, and semiconductors underscores the country’s global position in high-performance packaging solutions.

High Barrier Packaging Film Market Report Scope

High Barrier Packaging Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.8 Billion

|

|

Market Size (2034)

|

$52 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Material (PE, PP, PET, EVOH, PA, PVDC, Others), By Barrier Type (Oxygen Barrier, Moisture Barrier, UV Barrier), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial), By Packaging Format (Bags & Pouches, Lidding Films, Wraps, Blister Packs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Sealed Air Corporation, Berry Global Group, Inc., Sonoco Products Company, Klöckner Pentaplast, Mitsubishi Chemical Group Corporation, Toppan Inc., UFlex Ltd., Constantia Flexibles Group, Toray Industries, Inc., DuPont de Nemours, Inc., Innovia Films, Jindal Poly Films Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Barrier Packaging Film Market Segmentation

By Material

- PE

- PP

- PET

- EVOH

- PA

- PVDC

- Others

By Barrier Type

- Oxygen Barrier

- Moisture Barrier

- UV Barrier

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial

By Packaging Format

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in High Barrier Packaging Film Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Berry Global Group, Inc.

- Sonoco Products Company

- Klöckner Pentaplast

- Mitsubishi Chemical Group Corporation

- Toppan Inc.

- UFlex Ltd.

- Constantia Flexibles Group

- Toray Industries, Inc.

- DuPont de Nemours, Inc.

- Innovia Films

- Jindal Poly Films Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and multi-layered research methodology to deliver actionable insights on the Global High Barrier Packaging Film Market. The study combined primary research through interviews with key stakeholders, including packaging film manufacturers, converters, brand owners, and end-use companies in food & beverages, pharmaceuticals, and personal care, with secondary research involving company reports, regulatory documents, patent filings, and industry publications. Market sizing and forecasting were developed using historical data analysis, trend extrapolation, and econometric modeling, with particular attention to innovations in mono-material recyclable films, transparent oxide coatings, and bio-based high-barrier solutions. Regional market dynamics, covering the United States, Germany, China, India, Japan, and South Korea, were assessed for regulatory frameworks, sustainability initiatives, automation adoption, and circular economy practices. Competitive analysis examined leading players such as Amcor, Berry Global, Sealed Air, Mondi, Huhtamaki, and UFlex, focusing on R&D investments, strategic mergers, sustainable film development, and technology integration. This methodology ensures industry professionals receive a reliable, data-driven, and forward-looking perspective on market growth, material innovations, regulatory compliance, and opportunities in sustainable high-barrier packaging films.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.