Market Overview: Growth Driven by Sustainability and Smart Packaging Innovation

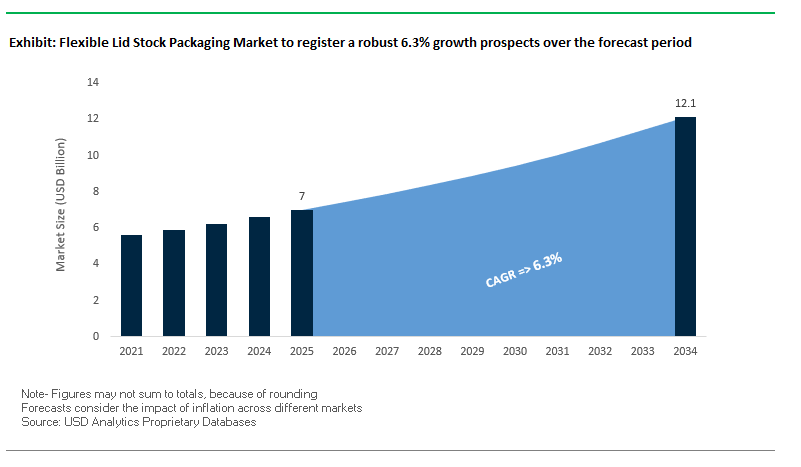

The Global Flexible Lid Stock Packaging Market is projected to grow from USD 7.0 billion in 2025 to USD 12.1 billion by 2034, expanding at a CAGR of 6.3%. This specialized packaging segment plays a critical role across food, beverage, dairy, and healthcare industries, ensuring product freshness, safety, and convenience. Flexible lid stock—typically made from multi-layer polymer films, aluminum laminations, or Tyvek® for medical use—is valued for its ability to provide superior barrier protection against oxygen, light, and moisture.

The market is experiencing rapid evolution as sustainability and convenience become dominant drivers. Peelable, easy-open lids are increasingly demanded by consumers, especially in single-serve formats such as ready meals, yogurt cups, and pharmaceutical blister packs. At the same time, smart packaging technologies—such as QR codes, NFC tags, and freshness indicators—are being integrated into lid stock, enabling traceability, product authentication, and consumer engagement.

Healthcare applications are also shaping demand. Medical-grade lid stock, including Tyvek® and sterile foil laminates, is being widely adopted for tamper-evident, hygienic packaging of devices and single-dose pharmaceuticals. This is creating opportunities for material innovation and compliance-driven solutions in life sciences.

Key Insights for Industry Professionals:

- Market to grow from USD 7B (2025) → USD 12.1B (2034), CAGR 6.3%.

- Laminated barrier films dominate due to superior oxygen, moisture, and light protection.

- Easy-peel seals are in high demand for convenience and consumer experience.

- Smart packaging adoption is expanding, especially in food traceability and pharma.

- Healthcare sector driving growth in sterile and tamper-evident lid stock solutions.

Market Analysis: Recent Developments in the Flexible Lid Stock Packaging Industry

The Flexible Lid Stock Packaging Industry is highly competitive and dynamic, with recent activities underscoring a strong push toward sustainability, smart packaging integration, and consolidation among global players.

In August 2025, ProAmpac announced plans to acquire PAC Worldwide, reinforcing its position in e-commerce fulfillment and protective packaging, areas that increasingly overlap with flexible lid stock applications. In the same month, reports highlighted a growing demand for smart packaging technologies, with lid stock manufacturers embedding QR codes, NFC tags, and RFID tracing systems to improve supply chain transparency and consumer interaction.

Also in August 2025, Sealed Air reported steady volumes in its food segment but revealed a strategic shift toward retail packaging solutions, addressing changes in consumer purchasing behavior. In July 2025, two major mergers reshaped the industry landscape: the Amcor–Berry Global combination, forming a global leader in flexibles and rigid containers, and the Smurfit Kappa–WestRock merger, strengthening the competitive position in paper-based packaging that could influence sustainable lid stock adoption.

Another major highlight came in July 2025, when Huhtamaki launched a compostable and recyclable lid solution for ice cream packaging, reinforcing its focus on circular packaging solutions. In June 2025, industry reports pointed to the pharmaceutical sector’s increasing adoption of lid stock for single-dose medicines, driven by dosage accuracy and contamination reduction requirements. Earlier in May 2025, DS Smith achieved its goal of replacing over 1 billion plastic components with fiber-based alternatives, an important milestone supporting the broader paperization trend in flexible packaging.

Emerging Trends and Strategic Opportunities Driving the Global Flexible Lid Stock Packaging Market

Accelerated Shift Towards Polypropylene-Based Mono-Material Solutions

The flexible lid stock packaging market is experiencing a decisive shift from complex multi-material laminates (such as PET/ALU/PE) to all-polypropylene (PP) mono-material lid stock. This transition is primarily driven by the need for full-package recyclability, as PP lids on PP containers create a single-material system compatible with existing polypropylene recycling streams. Flexible packaging, despite being the fastest-growing plastic packaging category, has one of the lowest recycling rates globally due to multi-material compositions. Companies like Toppan are innovating mono-material barrier packaging that protects contents while being recyclable. Mitsui Chemicals, a member of the Circular Economy for Flexible Packaging (CEFLEX) initiative, has developed PP-based lid stock exceeding 90% polypropylene content, adhering to CEFLEX guidelines. This mono-material adoption represents a significant growth avenue, especially for the food and beverage sector where sustainability compliance is critical. The shift is also reshaping the value chain, demanding closer collaboration between raw material suppliers, packaging converters, and CPG brands, alongside investment in new machinery and R&D for high-performance mono-material solutions.

Integration of Functional Additives for Active Food Preservation

The flexible lid stock market is increasingly integrating active functionalities, such as oxygen scavengers and antimicrobial agents, directly into the polymer or sealant layers. These enhancements actively extend the shelf life of perishable foods, reducing waste and enabling cleaner-label products. Active packaging systems interact with both the food and packaging, improving safety, shelf life, and sensory properties. Reports highlight that integrated slow-release antimicrobial layers using silver nanoparticles can extend the shelf life of high-risk foods from 7 days to up to 14 days. Industry leaders like Avient Corporation are introducing low-haze antimicrobial additives tailored for transparent food packaging, demonstrating the growing emphasis on functional, food-preserving lid stock. The development of these solutions provides a high-value growth avenue, offering products that not only seal but actively preserve food, meeting the increasing consumer demand for fresh, preservative-free options. The trend is also reshaping the supply chain, requiring enhanced collaboration among lid stock manufacturers, additive suppliers, and food scientists to ensure additive safety and compatibility.

Development of High-Barrier, Fiber-Based Lidding for Compostable Applications

A key innovation opportunity lies in creating fiber-based or paper-centric lid stock coated with bio-polymers, offering high barrier properties for fully compostable packaging. This addresses growing demand for sustainable ready-meal and fresh-produce packaging in regions with industrial composting infrastructure and strict plastic reduction mandates. Traditional multi-material films are difficult to recycle, prompting R&D into bio-based alternatives. BASF offers certified compostable biopolymers for extrusion coating on paper and board, ensuring excellent barriers against fats, liquids, and grease. Academic research highlights bacterial cellulose films that reduce water vapor permeability by 84% and biodegrade in soil within a month, proving bio-based materials can meet stringent functional requirements. The commercialization of these high-barrier compostable lid stocks presents a substantial growth avenue for manufacturers targeting environmentally conscious consumers and regions with strong composting mandates.

Adoption of Digital Printing for Short-Run, Personalized Promotional Lids

The adoption of digital printing for flexible lid stock is enabling cost-effective, short-run production tailored to limited-time offers, seasonal promotions, hyper-personalized campaigns, and regional variations. Digital presses eliminate the need for gravure cylinders, reducing setup costs and material waste. HP has deployed over 300 flexible packaging presses across 50 countries, highlighting the rapid uptake of this technology. Digital printing allows brands to test new designs economically, produce just-in-time packaging, and enhance engagement with consumers. This creates a high-growth opportunity for the flexible lid stock market, particularly for small and medium-sized direct-to-consumer (D2C) brands. It also fosters a more collaborative and agile value chain, with packaging suppliers acting as strategic partners, helping brands reduce inventory, minimize waste, and deliver personalized packaging experiences.

Competitive Landscape: Leading Companies Defining Flexible Lid Stock Packaging

The Global Flexible Lid Stock Packaging Market is led by a mix of diversified packaging giants and specialized players that are actively investing in sustainable solutions, technological advancements, and regional expansion.

Amcor plc strengthens portfolio with recyclable and smart lid stock solutions

Amcor is a global leader with a strong position in flexible lid stock packaging for food, beverage, and healthcare. Its portfolio includes die-cut lids and roll stock made from Tyvek® and foil laminations for medical and pharmaceutical applications. Amcor has been pioneering smart packaging innovations, embedding QR and NFC technology for traceability and consumer engagement. With its AmPrima® recyclable solutions, Amcor is moving toward its target of making all packaging recyclable or reusable by 2025, aligning with global sustainability trends.

Huhtamaki Oyj expands compostable lid solutions for circular packaging

Huhtamaki continues to lead in sustainable innovation. In July 2025, it launched a new recyclable and compostable lid stock for ice cream packaging, showcasing its commitment to eco-friendly alternatives. Its blueloop™ range offers flexible packaging designed for recyclability, targeting foodservice and consumer goods applications. Huhtamaki supplies lid stock for dairy, ready-meals, and fresh produce trays, emphasizing performance and sustainability. Its global reach makes it a key enabler of the circular economy.

Constantia Flexibles pioneers aluminum and eco-designed lid solutions

Constantia Flexibles is a major global producer with expertise in high-barrier films and foil-based lid stock. In August 2025, it launched ComforLid, a sustainable alternative to plastic lids, and EcoPeelCover, the world’s thinnest die-cut aluminum lid. These innovations strengthen its Ecolutions® portfolio, which emphasizes recyclability and resource efficiency. With over €100 million invested in upgrading global facilities, Constantia is focusing on mono-material sustainable solutions for food, pharma, and pet food markets.

Sealed Air Corporation focuses on protein and dairy lid stock innovation

Sealed Air, best known for its Cryovac® brand, is a key player in meat, poultry, and dairy lid films. Its products incorporate anti-fog technology and high-barrier protection, ensuring extended shelf life and food freshness. In August 2025, Sealed Air announced a turnaround strategy focused on retail channels, as demand shifts from foodservice to grocery. The company remains committed to reducing its environmental footprint by increasing the recycled content in its flexible packaging portfolio.

Flexible Lid Stock Packaging Market Share Insights

Peelable Lids Dominate Market Share by Packaging Type in Flexible Lid Stock Packaging

Peelable lids command 50% of the flexible lid stock packaging market, reflecting their indispensable role in ensuring both product integrity and consumer convenience. They are the default choice for dairy products, ready-to-eat meals, salads, and pharmaceutical diagnostic kits because they combine hermetic sealing with easy peel functionality, reducing consumer frustration while maintaining tamper evidence. The ability to integrate advanced barrier coatings and high-quality print finishes makes peelable lids not only functional but also a key branding surface for food and healthcare companies. This balance of safety, performance, and premium consumer experience ensures that peelable lids retain leadership over heat-sealed and pressure-sensitive formats.

Food & Dairy Products Lead Market Share by End-Use in Flexible Lid Stock Packaging

The food and dairy sectors collectively account for 65% of demand in the flexible lid stock packaging market, establishing them as the industry’s growth engine. From single-serve yogurt and desserts to multi-pack ready meals and condiment tubs, these industries rely heavily on lid stock for extended freshness, contamination prevention, and regulatory compliance. Beyond functionality, lid stock provides critical real estate for brand differentiation through high-resolution graphics and embossing, particularly in premium dairy and convenience foods. Increasing consumer preference for single-serve, on-the-go portions, combined with global growth in fresh and chilled foods, ensures that food and dairy remain the dominant end-use sectors for lid stock.

United States Flexible Lid Stock Packaging Market Driven by EPR Laws and Sustainable Innovations

The U.S. flexible lid stock packaging market is experiencing significant growth under a fragmented regulatory environment, with several states adopting Extended Producer Responsibility (EPR) laws that shift recycling and waste management costs from taxpayers to manufacturers. These regulations incentivize the development of mono-material films and other recyclable packaging solutions. Technological innovations, such as Drytac’s double-sided graphics adhesive film introduced in August 2025, are enhancing both product protection and consumer engagement across various lid stock applications.

Corporate investments are propelling market expansion, with Sonoco Products Co. announcing a $30 million facility expansion to produce 100 million additional units of sustainable adhesive packaging in flexible formats, including lid stocks. The market is particularly strong in the dairy, food, and pharmaceutical sectors, driven by the demand for tamper-evident seals, sterile packaging, and convenient single-serving portions. Sustainability remains a core focus, with bio-based films and recyclable paperboard gaining widespread adoption to meet consumer demand for environmentally responsible packaging solutions.

Germany Flexible Lid Stock Packaging Market Strengthened by Circular Economy Leadership and Regulatory Compliance

Germany’s flexible lid stock market operates under stringent regulatory frameworks, including the European Union’s Packaging and Packaging Waste Regulation (PPWR), aimed at reducing packaging waste through reuse and recycling, with restrictions on chemicals like PFAS. The country’s Packaging Act (VerpackG) and Extended Producer Responsibility (EPR) system drive innovation in recyclable packaging design, while encouraging reusable containers and trays for FMCG products.

Technological advancements include digital product passports and watermarks that improve transparency and recycling efficiency. Corporate developments, such as Amcor showcasing CleanStream technology at Fachpack Expo 2025 with mechanically recycled polypropylene (PP), highlight the focus on sustainable solutions. Key applications include the dairy, food, and beverage sectors, where premium lid stocks with high-barrier films ensure extended product shelf life while meeting consumer demand for sustainable, high-quality packaging.

China Flexible Lid Stock Packaging Market Accelerated by Green Policies and Advanced Manufacturing

China’s flexible lid stock market is driven by governmental initiatives, such as the “dual carbon” goal and the March 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement, promoting sustainable materials and recycling practices. Regulatory reforms effective September 2023, including limits on packaging layers and void ratios, have a direct impact on e-commerce and retail packaging.

Technological investments, including AI, 5G-enabled industrial internet, and automation, are optimizing production efficiency and flexible manufacturing capacities. The domestic push for technology substitution is expanding local production capabilities to meet the growing demand for high-quality, circular lid stocks. Key applications include ready-to-eat foods, e-commerce deliveries, and the food and beverage sector, with online grocery deliveries forecasted to drive substantial new volumes in flexible lid stock packaging.

India Flexible Lid Stock Packaging Market Growing Through Circular Economy Initiatives and Domestic Production

India’s flexible lid stock market is benefiting from government initiatives promoting a circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which mandate food-grade materials and restrict recycled plastics in food contact applications. Technological advancements, such as UFlex’s Electron Beam Coating Technology and Ascelpius™ BOPET films with up to 100% PCR content, are creating efficient and sustainable packaging solutions.

Corporate investments, including UFlex’s manufacturing capacity of over 100,000 TPA and four R&D laboratories, are driving production capabilities to meet domestic demand. The market’s growth is fueled by expanding food and beverage, and personal care sectors, the rise of e-commerce, and increasing consumer demand for sustainable packaging. The “Make in India” initiative further supports local manufacturing and technological innovation in flexible lid stock packaging.

Japan Flexible Lid Stock Packaging Market Pioneering High-Performance Films and Functional Packaging Innovations

Japan’s flexible lid stock market leverages advanced precision manufacturing, with innovations such as Toppan Inc.’s recycled BOPP film developed in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., suitable for mass production of sustainable lid stocks. Regulatory guidance under the Plastic Resource Circulation Act (April 2022) promotes environmental design and reduces single-use plastics, with a target to introduce 2 million tonnes per year of bio-based plastics by 2030.

High-performance films with superior barrier properties, IoT-enabled tracking, and functional enhancements like easy-open tear notches and resealable closures are driving product innovation. These solutions cater to aging populations and single-person households, supporting specialized food and beverage applications. The Japanese market emphasizes sustainability, functionality, and high-quality performance, positioning it as a global leader in advanced flexible lid stock packaging solutions.

Flexible Lid Stock Packaging Market Report Scope

Flexible Lid Stock Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7 Billion

|

|

Market Size (2034)

|

$12.1 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material Type (Plastics, Aluminum, Paper & Paperboard, Bioplastics), By Packaging Type (Peelable Lids, Heat-Sealed Lids, Pressure-Sensitive Lids), By End-Use Industry (Food & Beverages, Dairy Products, Pharmaceuticals, Cosmetics & Personal Care, Industrial, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Sonoco Products Company, UFlex Ltd., Constantia Flexibles Group, Sealed Air Corporation, Coveris Holdings SA, TC Transcontinental Packaging, Berry Global Group, Inc., ProAmpac, Printpack Inc., Rengo Co., Ltd., DS Smith plc, WestRock Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Lid Stock Packaging Market Segmentation

By Material Type

- Plastics

- Aluminum

- Paper & Paperboard

- Bioplastics

By Packaging Type

- Peelable Lids

- Heat-Sealed Lids

- Pressure-Sensitive Lids

By End-Use Industry

- Food & Beverages

- Dairy Products

- Pharmaceuticals

- Cosmetics & Personal Care

- Industrial

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Lid Stock Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- UFlex Ltd.

- Constantia Flexibles Group

- Sealed Air Corporation

- Coveris Holdings SA

- TC Transcontinental Packaging

- Berry Global Group, Inc.

- ProAmpac

- Printpack Inc.

- Rengo Co., Ltd.

- DS Smith plc

- WestRock Company

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive and integrated methodology to deliver an authoritative analysis of the Global Flexible Lid Stock Packaging Market. Our approach combined in-depth primary research, including interviews with packaging manufacturers, supply chain professionals, and sustainability experts, with extensive secondary research derived from corporate reports, regulatory filings, trade journals, and industry publications. Quantitative forecasting models were developed to evaluate market growth by material type, packaging type, and end-use industry, while qualitative insights analyzed emerging trends such as mono-material polypropylene lid stock, high-barrier fiber-based solutions, active food preservation additives, digital printing innovations, and smart packaging technologies like QR codes and NFC tags. Regional dynamics, including the impact of U.S. EPR laws, Germany’s circular economy mandates, China’s green policies, and Japan’s advanced manufacturing standards, were closely examined. Strategic corporate developments, including mergers, acquisitions, and product innovations by industry leaders such as Amcor, Huhtamaki, and Constantia Flexibles, were evaluated to provide actionable insights. USDAnalytics also assessed sustainability adoption, regulatory compliance, and technology integration, ensuring industry professionals gain a detailed, actionable, and forward-looking understanding of the flexible lid stock packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.