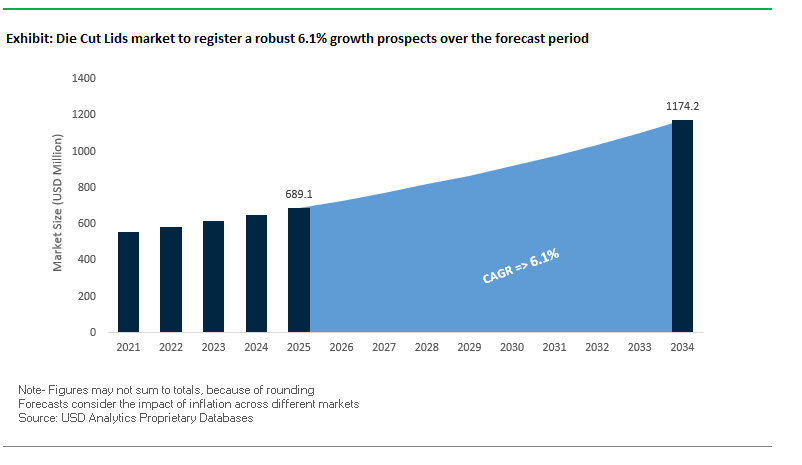

Die-Cut Lids Market Overview: Scaling to $1,174.1 Million by 2034 on Barrier Performance, Sustainability, and Smart Print (CAGR 6.1%)

The global die-cut lids market is projected to grow from $689.1 million in 2025 to $1,174.1 million by 2034, at a 6.1% CAGR. As the primary hygienic seal for dairy, beverages, ready-to-eat meals, and medical consumables, die-cut lids combine high oxygen/moisture/light barriers, tamper evidence, and on-the-go convenience with increasingly sustainable materials and high-definition printing. For procurement leaders and packaging engineers, the core questions are: how to meet shelf-life and seal-integrity KPIs with thinner, lower-carbon structures; how to upgrade user experience (easy-peel, drink-through, reseal) without sacrificing line speeds; and how to turn lids into branded, data-rich touchpoints via QR and digital decoration.

Executive insights:

- Product Protection First: ~60% of global die-cut lids serve applications demanding tamper-evident, hygienic seals with strong barrier to moisture, oxygen, and light directly extending freshness and shelf life.

- Material Innovation: Thinner aluminum gauges and solvent-free coatings are cutting material use by up to 25%, lowering greenhouse emissions while preserving seal performance.

- Consumer Convenience: Formats with easy-peel tabs, integrated drink openings, and reseal features are rising in response to on-the-go consumption.

- Smart, HD Decoration: >70% of new food & beverage SKUs deploy high-definition digital printing (graphics + QR codes), elevating brand differentiation and traceability.

Market Analysis: Low-Carbon Aluminum, Digital Workflows, and Paper-First Designs Redefine 2025

The 2025 landscape showcases sustainability-led launches, equipment upgrades, and paper-first substitutions that expand use-cases for die-cut lidding while improving total cost of ownership for converters and brand owners. In September 2025, Constantia Flexibles announced ComforLid, an aluminum lid with an integrated drinking function produced from low-carbon aluminum to reduce GHG emissions by up to 43% a clear step toward climate-aligned closures. The same month, BERHALTER spotlighted its Swiss Die-Cutter™, engineered to reduce web waste and downtime, improving yield in lid and label converting lines particularly valuable as substrates lightweight and graphics complexity rises.

In August 2025, Constantia previewed an expanded Ecolutions lidding portfolio for FACHPACK 2025, underscoring the shift to recyclable, lower-impact materials; simultaneously, Orora’s acquisition of Saverglass signaled continued premiumization across luxury beverages and cosmetics adjacent segments that often leverage premium die-cut lids for portion packs and gifting SKUs. In July 2025, the Smurfit Kappa–WestRock merger formed Smurfit WestRock, consolidating paper-based expertise that will likely accelerate paper-lidding and fiber-forward alternatives where sealing and barrier allow.

Earlier milestones reinforce the same direction. In May 2025, DS Smith launched DryPack in North America to replace EPS in cold-chain seafood, echoing the industry’s move away from fossil-based foams. In March 2025, WestRock with Liberty Coca-Cola scaled paperboard carriers to replace plastic rings, and in February 2025, The Good Cup introduced a fully paper cup eliminating a separate plastic lid a design pivot that directly pressures traditional lid SKUs and pushes lidding suppliers to innovate paper/foil-paper hybrids and seal-through lacquers.

Die Cut Lids Market: Trends and Opportunities Driving Sustainable and Smart Packaging Growth

Adoption of Mono-Material and Polymer-Based Recyclable Structures

The die cut lids market is witnessing a decisive pivot from multi-material laminates long criticized for their poor recyclability towards mono-material, polymer-based recyclable structures. This transition is being accelerated by regulatory pressure and corporate circular economy commitments. Packaging leaders like Mondi and Toppan are rolling out PE- and PP-based barrier films that not only ensure protection against oxygen and moisture but are also validated for recyclability. A supplier announcement in 2025 confirmed that a mono-material lidding film achieved 93% recyclability, a major milestone in replacing traditional, non-recyclable laminates. Independent certifications are further boosting market confidence: the German cyclos-HTP Institute certified a PP-based tray and lid combination as recyclable in a single stream, eliminating the separation challenges of mixed-material packaging. Meanwhile, the EU Packaging and Packaging Waste Regulation (PPWR) has intensified the financial burden on non-recyclable formats through higher Extended Producer Responsibility (EPR) fees, creating a strong financial and compliance incentive for brands to transition. Together, these developments position mono-material die cut lids as the new standard in recyclable flexible packaging.

Integration of Smart Features for Freshness Communication and Traceability

The second defining trend is the evolution of die cut lids into intelligent packaging platforms. By embedding sensors and indicators, manufacturers are turning static lids into dynamic communication tools that enhance safety, traceability, and consumer trust. For instance, pH-sensitive indicators developed from natural food colorants can detect volatile compounds released during spoilage, changing color to provide a clear freshness signal. Similarly, time-temperature indicators (TTIs) are being integrated into lids for chilled and frozen foods, offering irreversible visual cues that confirm cold chain integrity. These smart features directly tackle global challenges such as food waste reduction by providing more reliable freshness information than static “best before” labels. For retailers and consumers alike, smart lids create a value proposition beyond containment, offering a blend of safety assurance, waste reduction, and consumer engagement.

Development of High-Barrier Compostable and Bio-Based Lidding Films

As sustainability becomes non-negotiable, the development of compostable die cut lids with high-barrier properties presents a clear market opportunity. Packaging producers are now launching compostable lidding films designed for use with pulp or paperboard trays, creating a fully compostable packaging system suitable for chilled and dairy products. One major packaging company recently introduced a compostable lidding line targeting the yogurt and soft cheese markets, where oxygen and moisture barriers are critical to shelf life. The biggest growth driver lies in home-compostable materials, which align with decentralized, consumer-driven composting initiatives. Unlike industrial composting, home-compostable lids can be disposed of in backyard compost bins, addressing infrastructure limitations and making adoption easier for eco-conscious households. This segment is poised to capture strong demand from food manufacturers seeking end-to-end sustainable solutions in regulated markets such as the EU and North America.

Precision Application of Functional Coatings for Enhanced Performance

The second opportunity lies in the precision application of ultra-thin coatings that improve performance while maintaining recyclability. For chilled products, anti-fog coatings ensure product visibility by preventing condensation inside the lid an increasingly important feature in consumer purchase decisions. A leading adhesives and coatings company has already launched a dual-function heat-seal and anti-fog solution, combining visibility with strong sealing performance. Precision coatings are also being deployed to enhance peelability, delivering controlled opening force that improves consumer convenience without compromising hermetic sealing. Furthermore, these coatings enable material reduction strategies by replacing thick aluminum or PET layers with micro-thin coatings that achieve the same barrier performance at a fraction of the material use. This approach not only lowers costs but also reduces environmental impact, positioning precision-coated die cut lids as a high-performance, low-footprint alternative in the flexible packaging industry.

Competitive Landscape: Leaders Advancing Barrier Science, Circularity, and User-Centric Features

A mix of global packaging majors and specialty innovators is competing on barrier performance, sustainability credentials, converting efficiency, and consumer-friendly design. Buyers should benchmark vendors on peel force stability, heat-seal window breadth, retort/yogurt/CFB line speeds, recyclability claims, and HD-print fidelity.

Amcor Plc High-barrier, custom-engineered lidding at global scale

Amcor’s die-cut lidding spans food, beverage, and medical, marrying high oxygen/moisture barriers with reliable tamper evidence. The company prioritizes sustainable, recyclable structures, including metal-free high-barrier options and PCR content pathways where applicable.

Custom lids with peel-and-reseal, anti-counterfeit graphics, and print-ready surfaces help brands differentiate without compromising sealing windows. Amcor’s global design-to-scale network shortens qualification cycles and supports multi-region rollouts with consistent CQV performance.

Constantia Flexibles Group GmbH Low-carbon aluminum and drink-through innovation

A specialist in aluminum die-cut lids for dairy, food, and pharma, Constantia is pushing circular, low-carbon materials across its Ecolutions range.

ComforLid (Sep 2025) integrates a drinking opening to replace plastic lids, pairing user convenience with GHG reduction (up to 43%). Its water-based, full-surface digital print service for aluminum/PET dairy lids removes plate costs and speeds artwork changes ideal for seasonal SKUs and late-stage customization.

Huhtamaki Oyj Fiber-forward lids aligned to compostable cup systems

A global foodservice leader, Huhtamaki supplies paper and plastic lids tuned to hot/cold performance and blueloop sustainability principles.

Fiber-based, compostable platforms (e.g., July 2025 ice-cream cups) demonstrate barrier know-how transferable to paper lidding for specific sealing setups. Portfolio highlights include Impresso insulation cups and BioWare compostable hot cups, with lids engineered for leak resistance and fit integrity across fast-moving QSR lines.

Sonoco Products Company Specialty membranes and easy-open ends for secure seals

Sonoco focuses on peelable membranes and easy-open ends for rigid paper/metal containers, delivering high-performance sealing in niche and industrial applications.

Strategy centers on “Better Packaging. Better Life.” and a monomaterial push in can/closure systems, translating into lidding solutions that improve recyclability while meeting retort/sterilization demands. Portfolio streamlining strengthens focus on higher-growth specialty lids and precision-engineered openings.

Berry Global Group, Inc. PCR-rich PET/PP lids with print-ready surfaces

Berry supplies PET and PP lids emphasizing circularity and process efficiency. Recent rollouts feature reusable cup systems and PET lids with up to 65% PCR without sacrificing clarity or snap-fit performance.

Die Cut Lids Market Share Insights

Aluminum Foil Dominates Market Share by Material Type

Aluminum foil holds 55% of the die cut lids market in 2025, making it the unrivaled leader in material selection. Its dominance is rooted in its unmatched barrier protection against oxygen, moisture, and light, which is vital for maintaining freshness, flavor, and product stability across both food and pharmaceutical applications. Beyond protection, aluminum foil is highly adaptable it can be laminated with other substrates, printed with branding elements, and engineered for clean-peel functionality that enhances user convenience. Its widespread compatibility with high-speed automated filling lines further cements its market leadership. Plastic films, accounting for 30%, remain the second pillar of the market, particularly polyethylene terephthalate (PET) and polypropylene (PP) used where visibility and branding play a role such as in dairy cups, fresh salads, and chilled ready-to-eat meals. While plastics cannot match foil’s absolute barrier, they offer excellent versatility and cost-effectiveness, making them indispensable for short to medium shelf-life products. Paper-based lids, although a smaller niche, are gaining traction, particularly in fresh food applications driven by sustainability mandates. However, their limited natural barrier properties mean they are often paired with coatings, complicating recyclability. Other multilayer laminates serve specialized roles, combining foil, plastics, and paper for high-performance sealing in medical or industrial applications where no single substrate suffices.

Food & Beverage Continues to Anchor Market Share by Application

The food and beverage sector dominates the die cut lids market with a commanding 70% share in 2025, making it the single largest end-use industry. Die cut lids are indispensable in this segment for sealing dairy products such as yogurt and cream, ready-to-eat meals, smoothies, and snack packs, where freshness, tamper evidence, and shelf appeal are non-negotiable. This segment drives continuous innovation, particularly in developing resealable lids, easy-peel films, and sustainable alternatives that align with both consumer demand and food safety regulations. Pharmaceuticals and healthcare hold 20% of the market, representing a high-value segment where lid performance is mission-critical. Applications include blister packs, sterile medical devices, and protective liners, all of which require uncompromising barrier integrity and strict compliance with global pharmacopeia standards. The cost sensitivity here is far outweighed by the stakes of product safety and regulatory adherence. Cosmetics and personal care represent a growing niche, leveraging die cut lids for creams, masks, and lotions. Here, the balance shifts toward aesthetics and consumer experience, with demand for premium finishes such as metallic gloss, soft-touch coatings, and custom printing. Other applications, though smaller, include industrial and electronic packaging, where die cut lids protect reagents, chemicals, or components from contamination and moisture, proving the versatility of this packaging format across industries.

United States: Healthcare and Sustainable Innovation Driving Die Cut Lids Market

The U.S. die cut lids market is heavily influenced by the healthcare and pharmaceutical sectors, with companies like Oliver Healthcare Packaging producing die cut lids for medical packaging applications, including syringes, implants, and on-body wearables. The focus on sterility and superior barrier properties ensures the protection of sensitive medical products. In response to rising demand, major players are expanding thermoforming capacity, allowing integrated production of both thermoforms and companion die cut lids from a single location.

Sustainability is another key driver, with manufacturers like Winpak Ltd. introducing eco-friendly die cut lids made from biodegradable, recyclable, and renewable-content materials, catering to the growing preference for green packaging solutions. Strategic partnerships are also shaping the market, enabling end-users to streamline procurement by sourcing both filling machinery and compatible die cut lids from a single provider. These trends position the U.S. as a leader in innovative, sustainable, and functional die cut lids for healthcare and beyond.

Germany: Circular Economy and High-Barrier Die Cut Lids for Food and Pharma

Germany’s die cut lids industry is strongly guided by EU environmental regulations, particularly the Single-Use Plastics Directive, as well as national policies discouraging disposable packaging. This has spurred the development of plastic-free and recyclable die cut lids, aligning with eco-design and circular economy principles. Manufacturers are increasingly using high-recycled-content materials and exploring compostable and paper-based alternatives to meet regulatory and consumer demands.

The food and pharmaceutical sectors in Germany require die cut lids with excellent barrier properties to ensure product safety, long shelf life, and compliance with stringent hygiene standards. Multi-layer foil and plastic lids are in high demand, providing protection against oxygen, moisture, and light, making Germany a leader in high-performance, sustainable die cut lid solutions for regulated industries.

China: High-Volume Production and Technological Advancements Fuel Market Growth

China’s die cut lids market is primarily driven by the rapid expansion of the food and beverage industry, with applications spanning dairy, ready-to-eat meals, and packaged goods. Urbanization and rising disposable incomes have further accelerated the demand for convenient and secure packaging solutions.

As a global manufacturing hub, China boasts immense production capacity, catering to both domestic consumption and export requirements. Manufacturers are investing in advanced printing and cutting technologies, enabling the production of functional, visually appealing, and brand-differentiated die cut lids. Additionally, government regulations emphasizing food safety and hygiene are promoting the adoption of tamper-evident lids and robust barrier solutions, enhancing the overall reliability and appeal of Chinese die cut lid products.

India: Packaged Food Growth and Sustainability Drive Demand for Die Cut Lids

India’s die cut lids market is experiencing rapid growth, fueled by the expansion of the packaged food and beverage sector, particularly on-the-go and ready-to-eat products like dairy items and snacks. The increasing demand for convenient, hygienic, and functional packaging is pushing manufacturers to innovate with die cut lids that combine strong sealing properties and cost-effectiveness.

Government initiatives aimed at reducing plastic waste and promoting a circular economy are encouraging the development of sustainable and alternative materials. Indian manufacturers are focusing on economical yet functional die cut lids, catering to large-scale production while maintaining tamper-evident features. This positions India as a growing hub for innovative, sustainable, and affordable die cut lid solutions.

Japan: Precision, Sustainability, and High-Barrier Die Cut Lids

The Japanese die cut lids market emphasizes sustainability and high-quality standards, with companies developing lids that use reduced material thickness and solvent-free processes to minimize the carbon footprint. Precision in production ensures excellent peelability, sealing, and barrier properties, essential for sensitive products such as dairy and prepared foods.

High consumer expectations for reliability and convenience have pushed the market toward superior barrier solutions that extend shelf life without refrigeration. Japan’s combination of advanced manufacturing, sustainability initiatives, and quality-driven innovation ensures that die cut lids meet both functional and environmental demands.

Die Cut Lids Market Report Scope

Die Cut Lids market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$689.1 Million

|

|

Market Size (2034)

|

$1174.1 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Material Type (Aluminum Foil, Plastic, Paper, Other Materials), By Sealing Type (Heat Seal, Pressure Sensitive Seal), By Application (Food & Beverage, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Huhtamaki Oyj, Berry Global Inc., Constantia Flexibles, Sonoco Products Company, Tekni-Plex, Inc., Sealed Air Corporation, Winpak Ltd., Watershed Packaging, Oliver Healthcare Packaging, Pactiv Evergreen Inc., FFP Packaging Solutions, R-Pharm Germany GmbH, Uflex Ltd., ProMach Inc. (Modern Packaging)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Die Cut Lids Market Segmentation

By Material Type

- Aluminum Foil

- Plastic

- Paper

- Other Materials

By Sealing Type

- Heat Seal

- Pressure Sensitive Seal

By Application

- Food & Beverage

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Die Cut Lids market

- Amcor plc

- Huhtamaki Oyj

- Berry Global Inc.

- Constantia Flexibles

- Sonoco Products Company

- Tekni-Plex, Inc.

- Sealed Air Corporation

- Winpak Ltd.

- Watershed Packaging

- Oliver Healthcare Packaging

- Pactiv Evergreen Inc.

- FFP Packaging Solutions

- R-Pharm Germany GmbH

- Uflex Ltd.

- ProMach Inc. (Modern Packaging)

* List Not Exhaustive

Research Coverage

This report investigates the global Die Cut Lids Market, presenting a detailed analysis of material innovations, sustainability breakthroughs, and emerging smart-print technologies that are reshaping packaging solutions. USDAnalytics highlights the evolution of die-cut lids from traditional multi-material laminates to mono-material, polymer-based recyclable structures, alongside advances in high-barrier compostable films and precision coatings that improve performance while reducing environmental impact. The analysis reviews market dynamics including consumer convenience features, tamper-evident and hygienic seal requirements, digital decoration integration, and low-carbon aluminum adoption. The report also highlights competitive strategies, mergers, and acquisitions that define market leadership, providing insights into product innovation, recyclability, and barrier performance. This report is an essential resource for packaging engineers, brand owners, procurement professionals, and sustainability managers seeking forward-looking intelligence, historical trends, and forecasts from 2025 to 2034, enabling informed decision-making and strategic planning.

Scope Highlights:

- Segmentation: By Material Type (Aluminum Foil, Plastic, Paper, Other Materials), By Sealing Type (Heat Seal, Pressure Sensitive Seal), By Application (Food & Beverage, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ companies including Amcor plc, Huhtamaki Oyj, Berry Global Inc., Constantia Flexibles, Sonoco Products Company, Tekni-Plex, Winpak Ltd., Oliver Healthcare Packaging, and others

Methodology

The Die Cut Lids Market report leverages a robust methodology combining primary and secondary research to deliver accurate, actionable insights. Primary research involved interviews with industry executives, packaging engineers, R&D specialists, and procurement managers to assess emerging trends, barrier performance requirements, and sustainability adoption. Secondary research included review of company reports, trade journals, regulatory frameworks, and market databases. Data triangulation validated findings, while market modeling techniques projected growth, material adoption, and product innovation from 2025 to 2034. Historical data from 2021 to 2024 was analyzed to identify growth patterns, regional dynamics, and end-use demand, ensuring a research output that is both data-driven and forward-looking. USDAnalytics integrates these insights into a structured, reader-friendly analysis tailored to industry professionals.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.