Market Overview: Digital Packaging Consolidation, Recycled Shrink Films, and Protein Shelf-Life Technologies Reshape Barrier Shrink Films Market

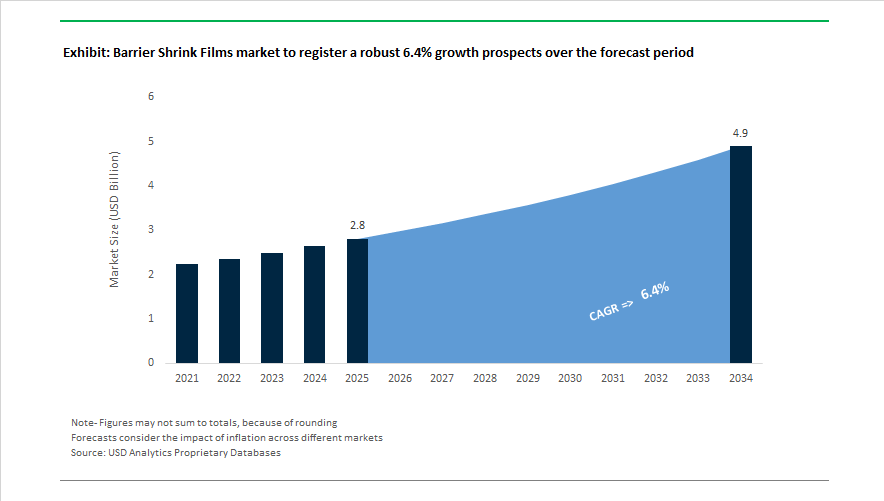

The Barrier Shrink Films Market is valued at $2.8 billion in 2025 and is projected to reach $4.9 billion by 2034, registering a 6.4% CAGR. Expansion is driven by demand for high-barrier shrink films, vacuum shrink bags, oxygen barrier packaging, MAP-compatible shrink films, recyclable polyolefin shrink films, and lightweight protein packaging. Structural industry transformation intensified in November 2025 when Clayton Dubilier & Rice agreed to acquire Sealed Air for $10.3 billion, a deal expected to close in mid-2026. The transaction is intended to accelerate Sealed Air’s shift toward digitalized, automated packaging platforms built around high-performance Cryovac barrier shrink technologies. Sustainability-linked innovation was also reinforced in November 2025 when Amcor launched its Lift-Off 2025/26 challenge, allocating up to $500,000 for compostable oxygen barrier solutions capable of replacing fossil-based resin structures.

Lightweighting and recycled-content integration define the technology pathway. In September 2024, Amcor introduced Clear-Tite 40 shrink film for fresh and processed proteins, reducing film thickness to 40µm and lowering plastic usage by 19% while maintaining oxygen barrier performance. Earlier in February 2024, Intertape Polymer Group released ExlfilmPlus PCR containing 35% recycled content and enabling a 9% reduction in overall material consumption through downgauging. Mondi expanded mono-PE recyclable offerings with FlexiBag Reinforced in August 2024, targeting high-puncture resistance applications that require shrink-ready durability. Circular material adoption extended into industrial uses when Cortec Corporation and Jakob Schober introduced PCR-based UV-resistant VpCI shrink film in February 2025 for corrosion protection of outdoor-stored metal components. Japan’s Gunze Limited followed with GEOPLAS HCT3 in 2024, incorporating 30% recycled resin via mass-balance to support premium labeling shrink applications.

Protein packaging automation and emission-reduction commitments complete the market trajectory. At IPPE in January 2026, Sealed Air’s Cryovac brand highlighted next-generation vacuum shrink rollstock systems optimized for high-speed automation and export shelf-life extension. Winpak strengthened climate-aligned product strategy after SBTi validated its emission targets in September 2025, with development of recycle-ready barrier thermoforming films and shrink-wraps. Coveris advanced hybrid fiber-film packaging between 2024 and 2025 through BarrierFresh MAP trays combining board with EVOH shrink films, reducing plastic by up to 90% while maintaining 21-day protein shelf life. ACTEGA addressed high-speed graphics performance in November 2024 with ShrinkFlex UV inks engineered to prevent distortion during heat-shrink processes. Amcor demonstrated AI-enabled Moda vacuum systems at IPPE January 2025 and January 2026, using machine vision to tailor barrier shrink bags on demand and cut film waste by up to 30 percent, underscoring the convergence of digital manufacturing, material efficiency, and high-barrier food packaging.

Trends and Opportunities Reshaping the Barrier Shrink Films Market

Market Trend: Mono-Polyolefin Barrier Shrink Films Become the Default for Compliance and Circularity

Barrier shrink films are undergoing a structural shift toward mono-PE and mono-PP formats as global policy and brand sustainability targets tighten. Under the EU Packaging and Packaging Waste Regulation (PPWR), now active as of February 2025, all packaging on the EU market must be recyclable at scale by 2030. Mono-material shrink formats are emerging as the most commercially viable way to meet recyclability grading requirements without disrupting existing recovery streams.

India’s April 2025 mandate further accelerated adoption. The Central Pollution Control Board (CPCB) is enforcing Extended Producer Responsibility (EPR) requirements that penalize brands failing to meet a 20% recycled plastic threshold. As a result, multinational beverage companies have begun re-specifying shrink films to mono-PE structures that are compatible with automated sortation systems and bale-ready recycling.

From a supply-side lens, resin producers are scaling PCR-enabled material platforms. Dow’s REVOLOOP™ portfolio added 100% post-consumer recycled (PCR) grades designed specifically for collation shrink films during 2024–2025. This ensures brand owners can satisfy Scope 3 carbon-reduction programs linked to retailer mandates. Walmart’s Project Gigaton has already reached its 1-billion-metric-ton reduction milestone, and 82% of private-brand packaging is now designed for recycling, creating a downstream expectation that secondary shrink film must also meet circularity specifications.

Market Trend: High-Clarity Barrier Films Enable “Sleeve-Free” Premiumization

Brand strategy is increasingly favoring minimal packaging that communicates sustainability and premium quality at shelf. Spirits, cosmetics, and gourmet food categories are accelerating the replacement of full-body non-recyclable shrink sleeves with ultra-clear, low-haze polyolefin shrink bands and selective spot labels.

In 2025, clarity and barrier became performance differentiators. High-barrier shrink films with haze values below 3% and oxygen transmission rates (OTR) under 50 cc/m²/day are enabling “naked bottle” designs that eliminate the need for external paperboard cartons. The outcome is both aesthetic and environmental: materials savings can reduce total packaging weight by as much as 15% while also maintaining shelf-life stability for oxygen-sensitive beverages.

Technology providers such as Tosaf, with UV9389PE modifier solutions, are helping premium brands prevent UV-induced product degradation. This has been especially impactful for craft spirits where natural botanicals and colorants are prone to oxidation. For marketing and operations teams, the move toward sleeve-free formats also reduces SKU complexity and freight weight, improving logistics efficiency and sustainability metrics simultaneously.

Market Opportunity: High-Barrier Shrink Bands for Regulated Pharmaceutical Cannabis Packaging

The medical and adult-use cannabis sector is emerging as a structurally high-margin niche within the Barrier Shrink Films Market. Packaging requirements in markets such as Germany and U.S. regulated states demand compliance with USP <671> moisture and light-protection standards. Film formulations must preserve volatile terpenes, prevent cannabinoid oxidation, and provide tamper-evidence suitable for controlled substances.

Multi-layer polyolefin shrink bands incorporating barrier layers that are Aclar®-free and PVDC-free are gaining traction, particularly for oral oils, tinctures, and vaporizer cartridges. Regulatory innovation is also enabling packaging differentiation. In June 2025, specialty converters reported rising adoption of Child-Resistant (CR) shrink sleeves engineered with micro-perforations and high-shrink-force geometry. These systems require a distinct peel or dual-action opening motion, improving patient safety compliance while remaining compatible with sustainable packaging frameworks.

Market Opportunity: Industrial-Grade Shrink Films for In-Transit Asset Protection

Outside of FMCG, demand is expanding rapidly for barrier shrink films that can secure high-value industrial assets during overseas freight and open-air storage. Aerospace turbines, automotive engine blocks, modular construction units, and wind turbine blades are increasingly wrapped using multi-layer heavy-gauge barrier shrink films to prevent water ingress, particulate contamination, and salt-air corrosion.

In 2025, Vapor Corrosion Inhibitor (VCI) chemistry became a commercial differentiator, with industrial shrink films now creating a micro-environment capable of neutralizing corrosive ions. Industry modeling suggests that VCI-integrated shrink wrapping can prevent corrosion-related losses that cost aerospace supply chains an estimated USD 2.5 billion annually.

Manufacturers such as RKW Group are producing heavy-duty films exceeding 150 microns in thickness, engineered for 24-month UV and environmental exposure. These solutions are emerging as the standard for large-format industrial logistics in infrastructure growth markets, positioning industrial shrink film suppliers to capture recurring contract-based revenue across long-term asset maintenance cycles.

Barrier Shrink Films Market Share and Segmentation Insights

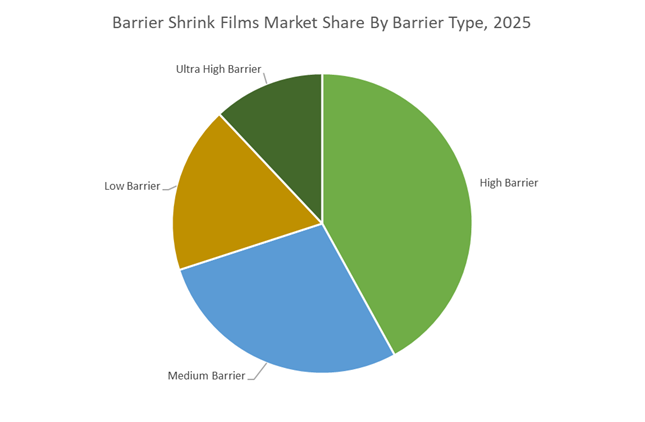

Barrier Type Market Share: High Barrier Leads at 42% While Ultra-High Barrier Accelerates in Export-Grade Packaging

In 2025, high barrier shrink films account for 42% of global barrier shrink film demand, serving as the industry standard for vacuum-packaged red meat, poultry, cheese, and processed meats requiring refrigerated shelf life of 21 to 45 days. These structures typically use 5 to 7 layer co-extrusions incorporating EVOH or PA, delivering OTR of 1 to 10 cc/m²/day and MVTR below 5 g/m²/day, with stable growth of 4 to 5% CAGR. Medium barrier films, used for short-cycle poultry and pork applications, are steadily losing share as retailers push for longer code dates to reduce markdowns and food waste. Low barrier films continue gradual decline, confined to frozen foods and industrial goods. Ultra-high barrier films are the fastest-growing segment, achieving OTR below 1 cc/m²/day through optimized EVOH, PVOH coatings, and SiOx/AlOx vapor deposits, enabling 90+ day shelf life for export meats and premium cheeses, commanding strong pricing.

End-Use Market Share: Food Commands 64% as Sustainability and Protein Packaging Drive Specification Intensity

By end use, food represents 64% of barrier shrink film consumption in 2025, making protein packaging the core demand driver. Fresh red meat remains the single largest application, followed by poultry, pork, processed meats, and cheese, with specifications tightly governed by oxygen control, moisture barrier, optical clarity, puncture resistance, and seal integrity. Sustainability pressure is reshaping material choices, accelerating migration toward recyclable monomaterial PE shrink films from traditional PA/EVOH structures. Beverage applications focus on secondary collation shrink, protecting multipacks and pallets in cold-chain logistics, while consumer goods leverage low to medium barrier films for tamper evidence and e-commerce presentation. Healthcare is a high-margin niche, requiring controlled permeability for sterilization rather than absolute barrier. Industrial and logistics remain cost-driven, though VCI shrink films for metal exports represent a small but profitable sub-segment.

Competitive Landscape Analysis of the Barrier Shrink Films Market

The competitive landscape of the barrier shrink films market is defined by strong technological differentiation, high entry barriers, and continuous innovation in sustainability, automation compatibility, and shelf-life extension. Leading manufacturers are competing on advanced multilayer structures, oxygen and moisture barrier performance, recyclability, downgauging capabilities, and integration with high-speed packaging machinery. Strategic investments in mono-material solutions, post-consumer recycled content, and smart barrier resins are reshaping procurement decisions across meat, poultry, dairy, seafood, and multipack applications. Market leaders are also leveraging vertical integration, proprietary resin technologies, and automation-driven packaging ecosystems to secure long-term contracts with global food processors and distributors.

Sealed Air leads the barrier shrink films market with Cryovac innovations

Sealed Air continues to dominate the global barrier shrink films market through its Cryovac brand, widely regarded as the industry benchmark for meat and poultry packaging. In 2025, the company expanded its patented microlayer technology, delivering ultra-thin polyolefin shrink films with over 30 functional layers that remain fully check-locally recyclable. Its Cryovac BDF barrier overwrap films introduced in 2026 feature enhanced anti-fog and oxygen-scavenging properties for irregular fresh protein cuts requiring a second-skin appearance. Sealed Air’s automation integration strategy bundles films with Cryovac 8600 series machinery, achieving throughput above 120 packs per minute. Its 2026 formulations demonstrate up to 53% spoilage reduction, reinforcing its leadership in shelf-life extension solutions.

Amcor strengthens high-barrier shrink film leadership through scale and sustainability

Amcor has emerged as a dominant force in high-barrier flexible and shrink film packaging following its large-scale integration of Berry Global during 2025 and 2026. The company announced major protein packaging capacity expansions across North America, installing advanced lamination and converting assets scheduled for full operation by early 2026. Amcor’s Lift-Off Challenge initiative actively funds startups focused on compostable oxygen barriers and nature-based additives. Its AmPrima PE-based shrink pouches and bags target replacement of non-recyclable multilayer laminates, particularly in dairy and cheese packaging. AI-driven waste analytics and digital twin modeling support seamless transitions to mono-material shrink films while maintaining long-duration gas and weather resistance.

Winpak differentiates through cast extrusion precision and cold-chain performance

Winpak holds a strong position in the North American barrier shrink films market through deep vertical integration and high-clarity cast extrusion expertise. Its DuraShrink and MAPfresh product lines introduced in 2026 deliver high shrink rates with low shrink force, preventing warping of irregular products such as whole poultry and hams. The company scaled 11 to 13 layer cast extrusion technology, enabling precise gauge control and downgauging while achieving puncture resistance around 20% above industry norms. Winpak emphasizes EVOH-based eco-friendly shrink bags for red meat and cheese, free from chlorine-based materials. Its films maintain flexibility down to minus forty degrees Celsius, supporting frozen seafood logistics.

Huhtamaki expands sustainable mono-material barrier shrink film solutions

Huhtamaki is a leading European supplier of sustainable flexible and shrink packaging, with a strong focus on reducing fossil-based plastic usage. Under its 2030 Strategy, the company targets fully recyclable, compostable, or reusable product portfolios by 2026, prioritizing mono-material PP and PE barrier shrink films. In early 2026, Huhtamaki scaled production of Blueloop barrier films that use advanced coatings to deliver moisture resistance on paper and mono-plastic substrates. The company is a key supplier to the global multipack segment, offering high-definition printed shrink films for beverages and personal care products. Its late 2025 expansion in Thailand strengthens APAC supply for e-commerce-driven demand.

Kureha Corporation pioneers high-barrier PVDC-based shrink film technologies

Kureha Corporation plays a critical role in the barrier shrink films ecosystem as a global innovator in PVDC and high-barrier resin technologies. In late 2025, the company introduced chlorine-reduced barrier shrink films to address sustainability requirements without compromising gas barrier performance. Its Krehalon brand leads the freshness preservation segment, offering shrink ratios up to 45% for tight-fit processed meat packaging. Kureha’s films are optimized for cook-in applications, enabling shrink-wrapped meats to be steam-cooked or water-bathed in the same package. Deep integration between resin production and film extrusion ensures uniform barrier performance even at thickness levels below forty microns.

Intertape Polymer Group repositions as a sustainability-focused shrink film supplier

Intertape Polymer Group has re-emerged as a sustainability-driven player in the polyolefin barrier shrink films market following its acquisition by Clearlake Capital. The launch of ExlfilmPlus PCR introduced polyolefin shrink films containing 35% post-consumer recycled content while preserving retail-grade clarity. IPG specializes in cross-linked polyolefin films with high seal strength and is focused on compatibility with high-speed automated packaging lines exceeding 125 packs per minute. Its 2026 roadmap emphasizes downgauged film formats between five and fifteen microns to reduce overall plastic usage by nearly 9%. Expansion of specialty additives includes antimicrobial coatings that significantly reduce microbial growth on packaged surfaces.

United States Barrier Shrink Films Market: MDO-PE Scale-Up, Recyclability Validation, and Protein Supply Chain Focus

The United States barrier shrink films industry is being reshaped by consolidation-led scale, accelerated adoption of machine direction orientation technology, and tighter recyclability governance across food and industrial applications. In April 2025, Amcor plc finalized its landmark combination with Berry Global Group, Inc., creating a materials science platform engineered to scale MDO-PE barrier shrink films across North American protein supply chains. The strategic rationale centers on replacing legacy multilayer, non-recyclable structures with mono-material MDO-PE films that deliver stiffness, clarity, and seal integrity required for high-speed meat and poultry operations.

Technology expansion is translating into tangible capacity. Charter Next Generation announced the installation of new nine-layer extrusion lines in late 2025, specifically designed to produce recycle-ready barrier shrink films using MDO processes. These lines replicate the optical performance of traditional multi-material laminates while maintaining compatibility with polyethylene recycling streams. Validation from recycling authorities has further de-risked adoption. Klöckner Pentaplast received Association of Plastic Recyclers design validation in May 2025 for its kp Infinity® range, supporting standardized use of recyclable barrier shrink films in foodservice and institutional channels. Industrial demand is also expanding. Polyzent Trading invested USD 1.1 million in December 2025 to launch a new manufacturing site in Virginia focused on high-integrity industrial shrink wraps for heavy and high-value shipments. Across the market, compliance with updated How2Recycle® guidelines is accelerating reformulation, particularly to tightly control EVOH concentrations while preserving widely recyclable status.

India Barrier Shrink Films Market: Localization Incentives, Smart Recycling, and Traceability Adoption

India’s barrier shrink films industry is advancing through policy-backed localization of resins, digital recycling innovation, and pharmaceutical-grade traceability. Under the Production Linked Incentive Scheme 2.0, specialized chemical hubs in Gujarat and Maharashtra have received targeted allocations to localize high-barrier nylon and EVOH resin production. This initiative is reducing import dependency and improving supply reliability for domestic shrink film converters serving food, beverage, and pharma sectors.

E-commerce optimization is a major growth vector. In 2025, leading Indian retailers partnered with Uflex Limited to deploy digital-watermarked shrink films. These films enable smart sorting and have demonstrated recycling efficiency improvements exceeding 40% in pilot programs. Sustainability-oriented R&D is scaling. Polyplex Corporation announced a USD 15 million investment in early 2026 to establish a new R&D center in Noida focused on biodegradable barrier resins engineered to maintain oxygen transmission stability in tropical climates. Regulatory traceability is also reshaping design. Implementation of the India Digital Traceability Act 2025 has driven adoption of laser-etched QR codes on barrier shrink bags for pharmaceuticals, strengthening anti-counterfeiting and tamper prevention across domestic distribution.

China Barrier Shrink Films Market: Mandatory Safety Standards, Thin-Gauge Localization, and PCR Incentives

China’s barrier shrink films industry is entering a compliance-driven and scale-optimized phase defined by mandatory safety standards, thin-gauge innovation, and incentives for post-consumer recycled content. Effective June 1, 2026, the Ministry of Industry and Information Technology will enforce GB 30981.2-2025, limiting harmful substances in industrial coatings and auxiliary film materials. This mandate is triggering a market-wide exit of heavy-metal-based stabilizers and accelerating adoption of cleaner additive systems in barrier shrink films.

Self-sufficiency has reached a new milestone. As of January 2026, China successfully localized production of ultra-thin eleven-layer barrier shrink films below 30 microns, significantly reducing reliance on imports for the domestic fresh-meat sector. Sustainability incentives are reinforcing this shift. The State Administration for Market Regulation established eco-packaging zones in Jiangsu in late 2025, offering tax rebates to manufacturers that incorporate more than 30% PCR content in industrial shrink wraps. These measures are accelerating domestic adoption of recycled-content barrier films without compromising mechanical strength or shrink performance.

United Kingdom and Switzerland Barrier Shrink Films Market: Circular Polymers, Shelf-Life Gains, and Alternative Proteins

The United Kingdom and Switzerland are emerging as innovation testbeds for circular polymers and shelf-life-extending barrier shrink films. In 2025, a collaboration between Dow and Bolloré delivered a food-contact barrier shrink film utilizing certified circular polymers derived from chemically recycled plastic waste. The solution is distributed exclusively by Yorkshire Packaging Systems, signaling growing retailer acceptance of chemically recycled inputs in regulated food packaging.

Performance-led innovation is delivering measurable outcomes. The OXBTEC_RCB shrink film introduced in late 2025 demonstrated the ability to extend poultry shelf life from seven to fourteen days, materially reducing food waste across European retail chains. Investment is also flowing into future protein formats. In 2025, MULTIVAC and Handtmann convened a global forum to develop FormShrink™ films tailored for alternative proteins. These applications require distinct gas permeability profiles compared with conventional meat, positioning barrier shrink films as a critical enabler for next-generation protein packaging.

Germany Barrier Shrink Films Market: Financial Reset, Circular Recognition, and Lightweight MAP Systems

Germany continues to set benchmarks for circularity and lightweight design in the barrier shrink films industry. In December 2025, Klöckner Pentaplast received court approval for a major financial restructuring, strengthening its balance sheet and enabling increased investment in 100% Tray2Tray® barrier shrink technology throughout 2026. This system supports closed-loop recycling of PET trays without cross-material contamination.

Innovation recognition is reinforcing Germany’s leadership. The Plastics Recycling Awards Europe 2025 highlighted German-developed barrier films that enable mono-material PET tray recycling without interference from barrier adhesives. Product innovation continues to reduce material intensity. The launch of kp Elite® Nova in July 2025 introduced a lightest-in-class modified atmosphere packaging tray that uses ultra-thin barrier shrink lids, cutting total plastic use by 12% while preserving shelf-life performance for fresh foods.

Country-Level Strategic Snapshot: Barrier Shrink Films Industry

Barrier Shrink Films market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

United States

|

MDO-PE scale and recyclability governance

|

Amcor–Berry integration, nine-layer MDO lines, APR validation, How2Recycle compliance

|

|

India

|

Localization, smart recycling, traceability

|

PLI-backed resin hubs, digital watermarking, biodegradable R&D, QR-based anti-counterfeiting

|

|

China

|

Compliance-led reformulation and thin-gauge scale

|

MIIT safety standards, sub-30 micron localization, PCR incentive zones

|

|

UK / Switzerland

|

Circular polymers and shelf-life extension

|

Chemically recycled films, doubled poultry shelf life, alternative protein FormShrink™

|

|

Germany

|

Circular reset and lightweight MAP

|

Financial restructuring, Tray2Tray® expansion, ultra-light barrier shrink lids

|

Barrier Shrink Films Market Report Scope

Barrier Shrink Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$4.9 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Ethylene Vinyl Alcohol, Polyamide, Polyvinylidene Chloride), By Barrier Type (Low Barrier, Medium Barrier, High Barrier, Ultra High Barrier), By Film Thickness (Below 15 Microns, 15 to 30 Microns, 30 to 50 Microns, Above 50 Microns), By Packaging Application (Shrink Wraps, Shrink Bags, Shrink Labels and Sleeves, Vacuum Skin Packaging), By End Use Industry (Food, Beverage, Healthcare, Consumer Goods, Industrial and Logistics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor, Sealed Air, Winpak, Bollore Group, Klockner Pentaplast, Multivac Group, Kureha, Flexopack, Coveris, Premiumpack, Uflex, Jindal Poly Films, Mitsubishi Chemical Group, Atlantis Pak, Schur Flexibles Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Barrier Shrink Films Market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Ethylene Vinyl Alcohol

- Polyamide

- Polyvinylidene Chloride

By Barrier Type

- Low Barrier

- Medium Barrier

- High Barrier

- Ultra High Barrier

By Film Thickness

- Below 15 Microns

- 15 to 30 Microns

- 30 to 50 Microns

- Above 50 Microns

By Packaging Application

- Shrink Wraps

- Shrink Bags

- Shrink Labels and Sleeves

- Vacuum Skin Packaging

By End Use Industry

- Food

- Beverage

- Healthcare

- Consumer Goods

- Industrial and Logistics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Barrier Shrink Films Industry

- Amcor

- Sealed Air

- Winpak

- Bollore Group

- Klockner Pentaplast

- Multivac Group

- Kureha

- Flexopack

- Coveris

- Premiumpack

- Uflex

- Jindal Poly Films

- Mitsubishi Chemical Group

- Atlantis Pak

- Schur Flexibles Group

*- List not Exhaustive