Market Overview: Singapore EVOH Capacity, PFAS-Free Paper Coatings, and Circular Polyolefin Resins Reshape Barrier Resins Market

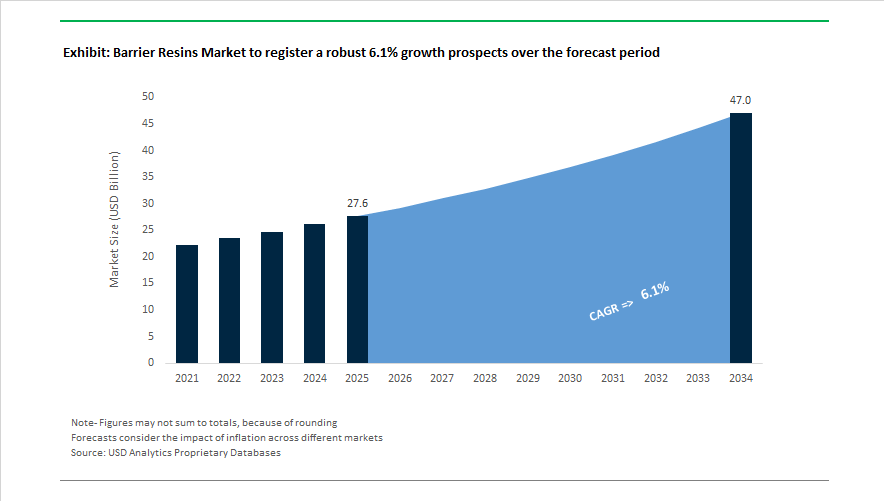

The Barrier Resins Market is valued at $27.6 billion in 2025 and is forecast to reach $47 billion by 2034, expanding at a 6.1% CAGR. Growth is supported by rising adoption of EVOH barrier resins, oxygen barrier polymers, recyclable mono-material packaging resins, circular polyolefins, PFAS-free barrier coatings, and sustainable high-barrier materials across food packaging, industrial containers, and infrastructure applications. Capacity expansion momentum began in August 2024 when Kuraray broke ground on a $410 million EVAL EVOH plant in Singapore with 36,000 tons annual capacity, scheduled to start operations by the end of 2026 to supply Asian food preservation markets. Circular material development strengthened in 2025 when Kuraray introduced 100% bio-based Circular EVAL, enabling oxygen barrier packaging with a reduced carbon footprint for premium sustainable brands.

Paper substitution and European supply growth accelerated through 2024–2025. Mitsubishi Chemical Corporation received RecyClass approval in 2024 confirming that multilayer films with up to 10% SoarnoL EVOH remain compatible with PE recycling streams. Mitsubishi expanded its UK SoarnoL capacity in July 2025, increasing Saltend output by 21,000 tons to meet food preservation demand. In December 2025, Mitsubishi Chemical commercialized PFAS-free SoarnoL paper coating technology, enabling paper food packaging to achieve gas and oil resistance beyond conventional fluorinated systems, targeting adoption in food service formats by fiscal 2026. Regional technical service expansion continued in July 2025 when Kuraray opened its Mumbai laboratory to support local converter design of EVAL structures.

Recyclable polyolefin barrier structures and circular feedstock integration define the latest industry shift. Dow launched INNATE TF 220 Precision Packaging Resin in June 2025, enabling recyclable BOPE films that replace multi-layer laminates. Commercial adoption was demonstrated during 2024–2025 when Dow partnered with Liby in China to launch fully recyclable laundry detergent packs using BOPE resins. LyondellBasell advanced circularity in November 2025 through a closed-loop collaboration with Nippon Paint China utilizing CirculenRecover resins to convert used industrial barrels into new packaging. At PLASTINDIA in January 2026, LyondellBasell showcased Hyperzone PE technology for high-performance barrier HDPE. Recycling infrastructure support progressed as Dow partnered with Xycle from 2024 to 2026 to construct a Netherlands advanced recycling plant producing virgin-quality circular resins. Mitsubishi Chemical reinforced sustainable material positioning at the Tokyo Functional Materials Expo in January 2026, presenting EVOH integration with fiber substrates aimed at eliminating aluminum foil from aseptic packaging.

Trends and Opportunities Transforming the Barrier Resins Market

Market Trend: Capacity Expansion of Recyclable High-Barrier Copolymers to Meet Circularity Compliance

Circular packaging policies are redefining supply-demand dynamics, and high-barrier resins such as EVOH and metallocene-based copolymers are becoming essential to enable recyclability in mono-material packaging systems. These materials allow food, beverage, cosmetic, and pharma producers to achieve moisture and oxygen protection without compromising downstream recyclability.

Kuraray is leading the global capacity race. To serve rising global demand, the company has expanded its EVAL™ EVOH resin output by 5,000 tons across the United States and Europe in 2024 and began constructing a USD 410 million, 18,000-ton facility in Singapore scheduled to begin operations by late 2026. This single investment represents one of the most significant supply additions in the history of barrier resins and is designed specifically to support the conversion of legacy multilayer packaging into recyclable mono-material formats.

The Regulation (EU) 2025/40 (PPWR), which took effect on February 11, 2025, is now accelerating the transition. Under its framework, all packaging marketed in the EU must be recyclable by 2030 and meet Class A–C recyclability standards. To comply, high-barrier resins such as EVOH must now remain below 5% by weight in total package structure to avoid contaminating PE or PP recycling streams. This requirement is shifting procurement and formulation strategies across converters, FMCG brands, and global packaging contract manufacturers.

Market Trend: High-Clarity and High-Barrier Resin Systems Unlock Sustainable Bottle Design

The market is moving beyond opaque, multi-layer packaging toward transparent, lightweight bottles that deliver both premium aesthetics and reduced carbon footprint. New high-clarity Polyamide (PA) grades and advanced PET copolymers are enabling brands to offer “glass-like transparency” and long shelf life without sacrificing recyclability.

In December 2025, ALPLA announced continued progress on its fully recyclable barrier PET wine and spirits bottles. By using integrated barrier copolymers instead of multilayer structures, these bottles achieve a 50% lower carbon footprint compared with glass and offer 12-month oxygen protection for sensitive beverages. This marks a significant inflection point for sectors that historically relied exclusively on glass for quality retention.

Bio-based barrier technologies are also progressing rapidly. At K 2025, material innovators demonstrated ethanol-derived PE processed with Machine Direction Orientation (MDO). The result: mono-material high-barrier film pouches and flow packs with enhanced optical clarity and a life-cycle footprint as low as –2.27 kg CO₂e per kg. These developments align tightly with ESG commitments across multinational food and personal care companies, making them commercially attractive and highly investable.

Market Opportunity: Inner Sealing Barrier Resins for Lithium-Ion Pouch Cell Manufacturing

Battery technology is becoming a dominant pull-factor for barrier resin demand. Soft-pack lithium-ion pouch batteries require a specialized inner sealing resin layer that resists moisture transmission, electrolyte corrosion, and thermal cycling throughout the service life of an electric vehicle.

Technical disclosures from 2024–2025 by suppliers including NAGASE and Mitsui Chemicals confirm that automotive-grade pouch films must deliver WVTR below 0.05 g/m²/day and maintain seal strength above 150 N/15 mm. As EV architectures move toward 800V systems and ultra-fast charging environments, inner sealing layers must tolerate exposure to corrosive electrolyte solvents such as EC/DMC without delamination.

Despite cyclical EV market conditions, this application remains a high-value segment because pouch cells are up to 20% lighter than metal-can cylindrical cells. Lower pack weight enables superior watt-hours per kilogram, making pouch resins strategically relevant for premium-range EVs, e-mobility OEMs, and energy-dense grid storage solutions.

Market Opportunity: Barrier-Grade Resins for Hydrogen Transport, Storage, and Zero-Emission Mobility

Hydrogen’s commercialization requires high-barrier polymer liners that prevent permeation and maintain structural reliability under extreme pressure and temperature differentials. Type IV hydrogen storage tanks (700 bar) rely on HDPE or Polyamide 6 (PA6) liners to preserve hydrogen integrity.

Arkema’s Rilsan® PA11 gained industry attention in early 2025 as a candidate resin for hydrogen tank liners, particularly due to its bio-based feedstock profile and demonstrated resistance to blistering and crack formation under rapid decompression. This solves a critical failure mode known as explosive decompression, which historically limited polymer use in hydrogen systems.

In June 2025, peer-reviewed research in the International Journal of Hydrogen Energy showed that lamellar inorganic components (LIC) added into PA6 reduced hydrogen permeation by three to five times. By lowering resin permeability, manufacturers can reduce tank liner thickness, improving payload capacity and driving fuel-cell trucking economics. The commercial pull for these solutions is strongest in heavy-duty transport, aerospace hydrogen propulsion concepts, and fleet-based decarbonization programs across Europe, Japan, and North America.

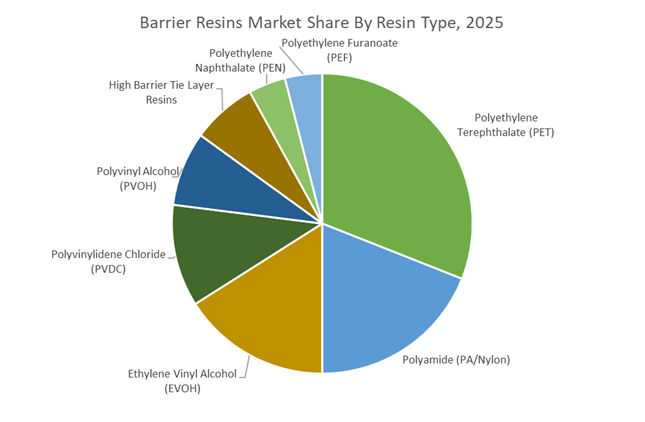

Resin Type Market Share: PET Leads at 31% While EVOH and Next-Gen PEF Reshape High-Barrier Packaging

In 2025, polyethylene terephthalate (PET) accounts for 31% of the global barrier resins market, retaining volume leadership due to its recyclability advantage and compatibility with oxygen scavengers, PVOH coatings, EVOH blends, and MXD6 reinforcements. Beverage giants are accelerating 100% rPET and PET-PET monomaterial strategies, structurally favoring PET over PVDC-containing multilayers. Polyamide, particularly MXD6, serves as the mechanical barrier specialist, offering oxygen barrier approaching EVOH with superior humidity resistance and thermoformability in vacuum meat and retort applications. EVOH remains the premium oxygen barrier resin, critical in juice, ketchup, and MAP meat packaging, with emerging ReEVOH recycling streams in Europe. PVDC continues terminal decline in Western markets, though it persists in Asia-Pacific pharma blisters. PVOH grows as a coating resin, especially in water-soluble pods. PEN remains niche, while PEF emerges as the long-term disruptor, offering bio-based, high-barrier performance as commercialization scales post-2025.

End-Use Industry Market Share: Food and Beverage Dominates at 58% as Pharma and Automotive Drive Technical Upgrades

By end use, food and beverage represents 58% of barrier resin consumption in 2025, making it the defining sector for oxygen and moisture barrier innovation. Applications span carbonated soft drinks using PET/EVOH, beer bottles leveraging PEN and emerging PEF, juice and dairy containers requiring EVOH layers, and PA/EVOH structures in meat packaging. Sustainability mandates are accelerating the shift away from PVDC and non-recyclable multimaterials toward monomaterial PET and polyolefin solutions with advanced barrier coatings. Pharmaceutical and medical applications deliver the highest margins, historically dependent on PVDC laminates but now transitioning toward PCTFE and COP/COC materials for high-value drugs. Industrial and chemical packaging prioritizes aggressive chemical resistance, while automotive fuel tanks rely on HDPE/EVOH co-extrusions to meet emission standards. Agriculture sees rapid uptake of water-soluble PVOH sachets, reflecting tightening operator safety regulations across Brazil and the EU.

Barrier Resins Market Competitive Landscape

The Barrier Resins Market in 2026 is being reshaped by circular packaging mandates, EV-driven lightweighting, PFAS-free coatings, and mono-material architecture. Competition centers on EVOH oxygen barriers, advanced tie-layer resins, compatibilizers for mechanical recycling, and bio-based polyolefins that preserve barrier integrity at high recycled content. Leading producers are expanding capacity across Europe and Asia, deploying AI-driven shelf-life modeling, and accelerating mass-balance and PCR integration. Strategic priorities now include retort-stable transparency, drop-in sustainability for converters, and closed-loop compatibility for food, healthcare, personal care, and automotive packaging.

Global EVOH leadership and circular-grade innovation by Kuraray Co., Ltd.

Kuraray remains the global benchmark for EVOH barrier resins, anchoring its 2026 strategy around PASSION 2026 and sustainable, high-functionality materials. Its EVAL™ EVOH portfolio now includes EVAL™ SC, engineered for circular multi-layer structures compatible with existing polyolefin recycling streams. Capacity expansions in Belgium and Singapore are underway to support surging demand for lightweight, high-barrier EV packaging. Recent innovation EVAL™ E105B delivers retort-stable transparency and gas protection, accelerating glass-to-plastic conversion in food packaging. Strategically, Kuraray is integrating PVOH and EVOH production to ensure seamless supply for healthcare, detergent, and specialty packaging markets worldwide.

PFAS-free green barrier architecture from Mitsubishi Chemical Group

Mitsubishi Chemical Group is defining the premium “Green Barrier” segment through precision EVOH chemistry and environmental compliance. Its SoarnoL™ platform now emphasizes bio-based grades using plant-derived ethylene, cutting barrier-layer carbon footprints by up to 30%. Under its 2025 Three Disciplined Approaches, the group prioritized food quality preservation while divesting legacy petrochemicals to fund barrier R&D. A late-2025 SoarnoL™ paper coating delivers oil and gas resistance without PFAS, directly addressing 2026 regulatory bans. Mitsubishi’s One Global Leadership model provides converters integrated support, optimizing tie-layer compatibility with recycled PE and diverse substrates.

Mono-material enablement and recycling compatibilization by Dow Inc.

Dow operates as the primary enabler of mono-material barrier packaging through advanced polyethylenes and specialty adhesives. Its 2026 “Transform the Waste” strategy targets 3 million metric tons of circular and renewable solutions annually by 2030, led by the REVOLOOP™ PCR line. INNATE™ Precision Resins and RETAIN™ Polymer Modifiers chemically compatibilize EVOH and PA layers during mechanical recycling, unlocking circularity for multilayer films. Dow showcased a 100% all-PE stand-up pouch with ultra-high barrier via vacuum metallization in 2025. Through Pack Studios, AI-driven modeling now cuts physical prototyping time by nearly 50%.

High-performance tie-layer resins and circular scale from LyondellBasell

LyondellBasell leads functionalized polyolefins and tie-layer innovation, critical for bonding EVOH and PA to polyethylene. Its Plexar® resins are now optimized for high-speed co-extrusion in thin-walled medical packaging. Backed by a $1.3 billion Cash Improvement Plan through 2026, LYB is rapidly expanding its Circulen recycled and renewable resin family. A 2026 partnership with Polynt introduced +LC marine resins using mass-balance bio-circular feedstocks. Through MoReTec technology, LyondellBasell uniquely converts hard-to-recycle plastics into virgin-quality barrier resins at industrial scale, strengthening its integrated mechanical and molecular recycling leadership.

Lightweight polypropylene barrier solutions by Borealis AG

Borealis dominates advanced PP barrier resins in Europe, specializing in lightweight rigid and flexible packaging. A €100 million investment in a High Melt Strength PP line in Germany, launching in H2 2026, will triple capacity for recyclable foam barrier solutions. Its Daploy™ HMS PP enables containers up to 60–90% lighter than conventional alternatives, driving material efficiency in automotive and food packaging. Borealis also supplies high-temperature barrier resins for oil and gas transport and vehicle electrification. Through its We4Customers strategy, the company delivers bespoke compounding that blends virgin polymers with PCR to accelerate brand sustainability targets.

Hybrid recycled polymers and drop-in sustainability from INEOS

INEOS is accelerating adoption of hybrid barrier resins that combine high recycled content with premium aesthetics. Its Recycl-IN portfolio integrates mechanically recycled plastics with booster polymers to preserve mechanical strength and barrier performance. In January 2026, INEOS launched rPP1025C, a polypropylene containing 70% recycled material tailored for luxury cosmetics packaging. The company’s drop-in sustainability approach requires zero converter re-tooling, enabling up to 35% carbon footprint reduction without capital investment. FDA No Objection Letters secured in early 2026 now allow INEOS recycled barrier resins to be deployed in food-contact and medical applications across North America.

Japan: EVOH Scale-Up, PFAS-Free Paper Barriers, and R&D Consolidation

Japan remains the global technology anchor for high-performance barrier resins, with a strong focus on EVOH capacity expansion, PFAS-free innovation, and R&D efficiency. Kuraray Co., Ltd. is executing its PASSION 2026 medium-term plan, which centers on a substantial global expansion of EVAL™ EVOH resin capacity. A pivotal element of this strategy is a new production site in Singapore scheduled to commence operations by late 2026, designed to stabilize the Asian supply chain and ensure consistent availability of high-barrier materials for food and pharmaceutical packaging across the region.

Innovation in PFAS-free barrier solutions is also accelerating. In December 2025, Mitsubishi Chemical Corporation announced a breakthrough approach enabling paper packaging to be coated with SoarnoL™ EVOH solutions. This technology positions EVOH as a viable oil- and grease-resistant alternative to PFAS-based coatings for food-contact applications. Recyclability has moved from pilot validation to formal approval. In October 2025, Mitsubishi Chemical’s SoarnoL™ resins received RecyClass Technology Approval for use in multilayer films at up to 10 weight percent, confirming compatibility with standard polyethylene recycling streams. Structurally, Japan’s barrier resin R&D ecosystem has become more centralized. Following the merger of Nippon Gohsei into Mitsubishi Chemical, the group consolidated its research programs to prioritize high-value coating and adhesion derivatives for the 2026 fiscal year, reinforcing Japan’s leadership in advanced barrier resin chemistry.

India: Localization of Technical Capabilities and Export-Oriented Resin Strategy

India’s barrier resins industry is transitioning from import dependence toward localized technical development and export-oriented manufacturing. A critical step in this shift was the inauguration of Kuraray India’s dedicated technical laboratory in Mumbai in July 2025. This facility enables localized testing of multilayer barrier structures and significantly shortens development cycles for Indian brand owners seeking to replace aluminum foil with EVOH-based films in food and pharmaceutical packaging.

Policy frameworks are reinforcing domestic capacity expansion. Under the government’s Production Linked Incentive scheme for specialty chemicals, with an outlay of ₹1.97 lakh crore, Indian manufacturers are scaling production of high-performance polyolefins and barrier tie-layers to reduce reliance on imported resins. Strategic alignment is further supported by NITI Aayog’s Chemical Industry Vision 2030, published in July 2025, which identifies specialty chemicals as a core growth pillar and explicitly incentivizes R&D in green chemistry and high-barrier resin systems. As technical infrastructure and production scale improve, India is being repositioned as a strategic export hub for barrier-packaged pharmaceuticals and processed foods, particularly serving Middle Eastern and Southeast Asian markets that require consistent barrier performance and regulatory compliance.

United States: Consolidation-Led R&D Scale and Recycling System Integration

The United States barrier resins industry is being reshaped by consolidation-driven R&D scale, capacity expansion, and progress in recyclability pre-qualification. The mid-2025 merger between Amcor plc and Berry Global Group, Inc. created a materials science platform with extensive production reach. The combined entity is leveraging its integrated research capabilities to accelerate adoption of recyclable barrier resins in North American healthcare and regulated food packaging applications.

Capacity scaling has followed demand shifts toward lightweight and unbreakable packaging formats. A new plant in the Charlotte, North Carolina region reached full operational status in 2025, nearly doubling output of SoarnoL™ EVOH pellets to support growing use in baby food and meat packaging. Regulatory alignment has improved recyclability outcomes. In 2025, the Association of Plastic Recyclers and How2Recycle pre-qualified several EVOH resin grades as Store Drop-off Recyclable. This clearance removed a major barrier to broader use of EVOH-containing flexible stand-up pouches and reinforced EVOH’s role as a compliant barrier resin within existing recycling systems.

European Union (Belgium and Germany): PFAS Thresholds and Circular Chemistry Mandates

Belgium and Germany are at the center of the European Union’s regulatory-driven transformation of the barrier resins industry. Effective August 12, 2026, EU Regulation 2025/40 under the Packaging and Packaging Waste Regulation framework mandates that food-contact packaging cannot exceed 25 parts per billion for any single PFAS substance. This requirement is forcing a rapid shift toward barrier resins that deliver grease resistance through intrinsic polymer properties rather than chemical additives.

Circular economy targets are reinforcing this transition. The EU’s 65% recycling rate objective for 2025 is driving chemical clusters in Germany and Belgium to prioritize chemically recycled barrier polyamides over virgin fossil-based materials. At the same time, regulatory scrutiny is intensifying. By December 2026, the European Commission, supported by European Chemicals Agency, is required to complete an assessment of substances of concern in barrier layers. This process is expected to influence the future viability of certain PVDC-based formulations and further accelerate substitution with EVOH, polyamide, and next-generation recyclable barrier resins.

China: High-Density Barrier Grades and Import Substitution Momentum

China’s barrier resins industry is entering a new capacity expansion cycle between 2026 and 2029, with a pronounced emphasis on high-density barrier-grade polymers. Polyethylene production capacity is projected to expand significantly in 2026, with a notable share allocated to grades optimized for moisture and oxygen barrier performance in food and industrial packaging.

This expansion aligns with China’s broader import substitution strategy. Primary-form plastic imports are expected to remain constrained as domestic producers successfully localize the manufacture of high-purity EVOH and polyamide barrier resins that were previously sourced from Japan and the United States. As a result, China is strengthening self-sufficiency in advanced barrier materials while improving cost competitiveness for domestic converters serving food, pharmaceutical, and consumer goods markets.

Country-Level Strategic Snapshot: Barrier Resins Industry

Barrier Resins Market County Level Snapshot

|

Country / Region

|

Strategic Emphasis

|

Key Developments

|

|

Japan

|

EVOH capacity and PFAS-free innovation

|

New Singapore plant, SoarnoL™ paper coatings, RecyClass approval, R&D consolidation

|

|

India

|

Localization and export positioning

|

Mumbai technical lab, PLI-backed capacity, green chemistry incentives

|

|

United States

|

Consolidation-led scale and recyclability

|

Amcor–Berry integration, North Carolina capacity expansion, APR pre-qualification

|

|

EU (Belgium/Germany)

|

PFAS thresholds and circular chemistry

|

PPWR enforcement, Ccycled polyamides, substance assessments

|

|

China

|

Capacity expansion and import substitution

|

Barrier-grade PE growth, localized EVOH and PA production

|

Barrier Resins Market Report Scope

Barrier Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.6 Billion

|

|

Market Size (2034)

|

$47 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Resin Type (Ethylene Vinyl Alcohol, Polyvinylidene Chloride, Polyethylene Furanoate, Polyamide, Polyethylene Naphthalate, Polyvinyl Alcohol, Polyethylene Terephthalate, High Barrier Tie Layer Resins), By Application (Flexible Packaging, Rigid Packaging, Blister Packs, Bag in Box Systems, Agricultural Films, Tubes), By End Use Industry (Food and Beverage, Pharmaceutical and Medical, Cosmetics and Personal Care, Agriculture and Agrochemicals, Industrial and Chemical, Automotive)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kuraray, Mitsubishi Chemical Group, Dow, BASF, Amcor, Arkema, Solvay, Asahi Kasei, Eastman Chemical Company, LyondellBasell Industries, Exxon Mobil Corporation, Honeywell International, Nippon Shokubai, INVISTA, INEOS Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Barrier Resins Market Segmentation

By Resin Type

- Ethylene Vinyl Alcohol

- Polyvinylidene Chloride

- Polyethylene Furanoate

- Polyamide

- Polyethylene Naphthalate

- Polyvinyl Alcohol

- Polyethylene Terephthalate

- High Barrier Tie Layer Resins

By Application

- Flexible Packaging

- Rigid Packaging

- Blister Packs

- Bag in Box Systems

- Agricultural Films

- Tubes

By End Use Industry

- Food and Beverage

- Pharmaceutical and Medical

- Cosmetics and Personal Care

- Agriculture and Agrochemicals

- Industrial and Chemical

- Automotive

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Barrier Resins Industry

- Kuraray

- Mitsubishi Chemical Group

- Dow

- BASF

- Amcor

- Arkema

- Solvay

- Asahi Kasei

- Eastman Chemical Company

- LyondellBasell Industries

- Exxon Mobil Corporation

- Honeywell International

- Nippon Shokubai

- INVISTA

- INEOS Group

*- List not Exhaustive