Market Overview: Private Equity Consolidation, Mono-Material Innovation, and Paper-Based Oxygen Barriers Reshape the Barrier Films Market

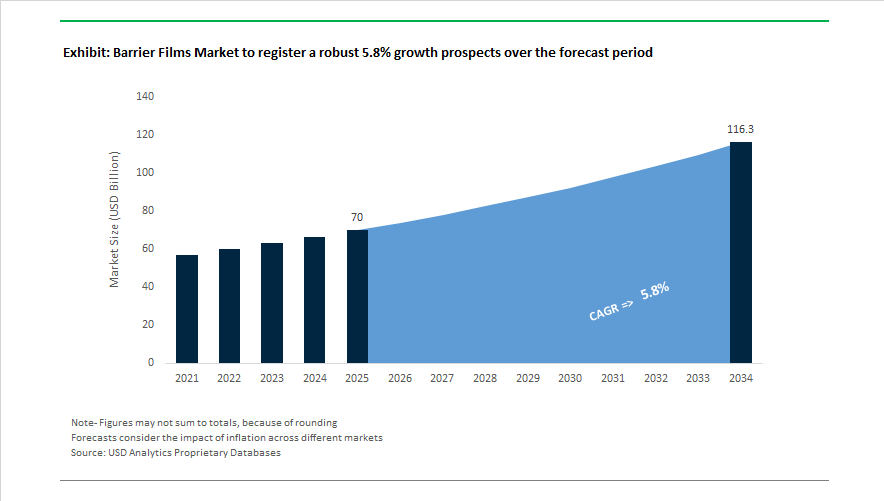

The Barrier Films Market stands at $70 billion in 2025 and is forecast to reach $116.3 billion by 2034, progressing at a 5.8% CAGR. Expansion is tied to rising demand for high-barrier packaging films, oxygen barrier materials, moisture barrier laminates, EVOH coextruded films, recyclable mono-material structures, compostable barrier coatings, and modified atmosphere packaging. Structural change accelerated in November 2025 when Clayton, Dubilier & Rice entered a definitive agreement to acquire Sealed Air Corporation for $10.3 billion. The transaction, expected to close in mid-2026, allows Sealed Air to intensify automation, digital packaging systems, and high-performance barrier film innovation under private ownership. In parallel, Amcor launched its 2025/26 Lift Off innovation challenge in November 2025, targeting nature-based barrier additives capable of delivering strong oxygen transmission rate performance on paper substrates via dispersion coatings.

Paper-based barrier solutions and mono-polyolefin structures gained industrial scale through 2025. Mondi began large-scale production of FunctionalBarrier Paper Ultimate in August 2025 following a €16 million Polish investment, achieving oxygen transmission rates below 0.5 cm³/m²/day and positioning the product as a recyclable alternative to aluminum-laminated flexible packaging. Mondi extended industrial barrier packaging in June 2025 with PaperPlus Bag Advanced, reducing plastic content by 60% while protecting humidity-sensitive construction powders. Toppan Holdings strengthened its European barrier film capabilities in March 2025 through acquisition of Irplast S.p.A., integrating S-BOPP technology for thin, high-stiffness films. Capacity growth continued in November 2025 as Toppan Speciality Films commissioned a hybrid BOPP and BOPE line in India, enabling rapid switching between polypropylene and polyethylene substrates to support circular mono-PE food packaging demand. Jindal Films invested in its Brindisi facility in October 2025 to expand Ethy-Lyte BOPE and Metallyte BOPP output for recyclable barrier laminates.

High-barrier polymers, retort recyclability breakthroughs, and intelligent film technologies expanded performance boundaries. Pregis increased EVOH coextruded film capacity in South Carolina in April 2025, targeting food sterility and medical packaging oxygen control. Cosmo Films introduced TR-BOPP in December 2025 for heat-resistant, recyclable pet food pouches. At the IPPE Expo in January 2026, Sealed Air highlighted Cryovac® vacuum skin packaging films emphasizing clarity and shelf-life extension. Bobst Group, Brückner Group, and Mitsui Chemicals collaborated during 2025 to commercialize a mono-material recyclable retort film, replacing aluminum-based multilayers in high-temperature food processing. Taghleef Industries introduced smart metallized barrier films with embedded leak-detection capability in 2025, adding real-time integrity monitoring for pharmaceutical and perishable food packs.

Trends and Opportunities Driving Growth in the Barrier Films Market

Market Trend: Recyclable Mono-Material Barrier Films Move to Industrial Scale

The transition from complex multi-material laminates to recyclable mono-PE and mono-PP structures is now the dominant direction in barrier films. The EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, requires that packaging achieve scalable recyclability by 2030, steering brand owners toward fully circular designs.

To meet these mandates, major converters such as Amcor and Berry Global have commercialized high-barrier mono-material solutions reinforced with AlOx and SiOx coatings that replicate the gas-barrier performance of traditional mixed laminates. At the infrastructure level, equipment spending on MDO (Machine Direction Orientation) lines has surged, with processing upgrades costing USD 15 million to USD 25 million per installation. These systems improve tensile strength and oxygen barrier properties, enabling mono-material pouches to replace aluminum-based or PET-based structures that will face higher plastic taxes across Europe.

The commercial narrative is shifting from “recyclable intent” to verifiable recyclability classification, positioning high-barrier mono-materials as the future foundation of food and personal care flexible packaging.

Market Trend: Ultra-High Barrier Films Gain Strategic Relevance in Lithium-ion Battery Supply Chains

The rapid spread of EV production is reshaping demand for Aluminum Laminate Pouch (ALP) films. These films must maintain extremely low Water Vapor Transmission Rates (WVTR < 0.02 g/m²/day) while providing corrosion resistance for 15-year design lifetimes in high-voltage EV architectures.

Next-generation 800V platforms require thinner 88 µm to 113 µm pouch materials to maximize volumetric energy density. At the same time, seal integrity must remain above 158 N/15 mm even after Warm Isostatic Pressing at 120°C and 4,000 bar.

Under India’s PLI manufacturing policy, battery-grade ALP demand is forecast to expand from USD 78 million in 2024 to USD 134 million by 2032. As OEMs pursue regionalized sourcing strategies, suppliers who can produce certified battery films domestically are securing long-term agreements with cell and module manufacturers.

Market Opportunity: Barrier-Engineered Films for Plant-Based Protein Packaging

Plant-based proteins degrade faster than animal-based products due to lipid oxidation and unstable color chemistry. This performance gap is creating demand for barrier films with tailored Oxygen Transmission Rates and moisture control.

Industrial trials in 2025 demonstrated that films incorporating natural antioxidants such as alpha-tocopherol or clove-oil reservoirs can extend refrigerated shelf life of plant-based meat by 30% to 42%. Growth is reinforced by changing consumer preferences: nearly 70% of plant-protein buyers now expect environmentally responsible packaging, pushing conversion toward bio-based gels and flexible structures that meet both sustainability and high-barrier requirements.

The commercial advantage rests with suppliers capable of linking food safety performance, shelf-life assurance, and recyclability into a consolidated value proposition for alternative-protein manufacturers.

Market Opportunity: Flexible Encapsulation Films for Perovskite Solar Commercialization

Perovskite photovoltaics are approaching commercial readiness but remain highly sensitive to moisture and oxygen exposure. Their bankability relies on Ultra-High Barrier encapsulation films that maintain WVTR below 10⁻⁴ g/m²/day while preserving visible-light transmission.

Recent breakthroughs are accelerating adoption. In December 2025, researchers in Singapore achieved 2,000 hours of survival in damp-heat testing (85°C, 85% RH) through a two-stage encapsulation method used in perovskite-silicon tandem cells. Taiwan Perovskite Solar Corp reported 25.37% power conversion efficiency at USD 0.20 per watt, demonstrating competitive economics relative to crystalline silicon.

Barrier film manufacturers positioned to scale flexible encapsulants, hot-melt adhesive integration, and thin-film lamination technologies stand to benefit from one of the fastest-growing niches in the global renewable energy packaging market.

Barrier Films Market Share and Segmentation Insights

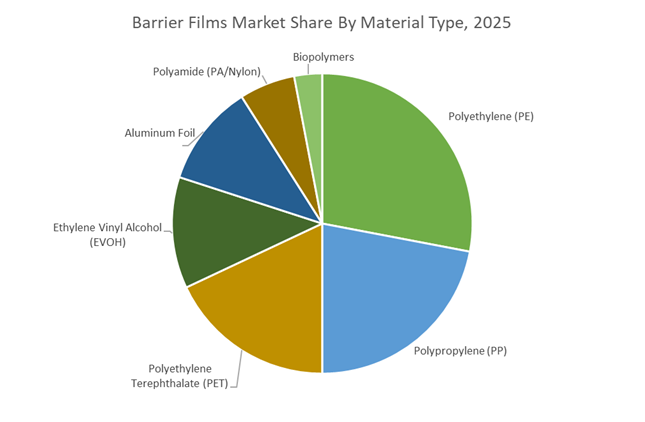

Material Type Market Share: Polyethylene Leads Volume While EVOH and PET Anchor High-Barrier Performance

In 2025, polyethylene (PE) accounts for 28% of global barrier films market share, maintaining volume leadership due to its superior moisture barrier, sealability, and cost efficiency in multilayer flexible packaging. LLDPE and metallocene-catalyzed PE grades are gaining traction through downgauging and enhanced mechanical performance. Polypropylene (PP) dominates rigid and retort packaging, with BOPP films widely used in snack and confectionery applications, increasingly substituting PET in non-retort formats on cost grounds. PET remains the preferred substrate for metallization and transparent high-barrier coatings such as AlOx and SiOx, particularly in coffee packs, vacuum bags, and pharmaceutical lidding. EVOH continues as the gold standard for oxygen barrier, essential in meat and dairy packaging, though humidity sensitivity requires encapsulation. Aluminum foil faces structural substitution pressure from transparent coatings, while polyamide supports puncture resistance in vacuum packs. Biopolymers remain small but policy-driven growth candidates.

End-Use Industry Market Share: Food and Beverage Commands 58% as Pharma and Electronics Drive Premium Demand

By end use, food and beverage represents 58% of global barrier film consumption in 2025, reinforcing its dominance in shelf-life extension, food waste reduction, and lightweight flexible packaging solutions. Fresh produce, meat, dairy, and ready meals remain primary volume drivers, with a visible shift from metallized laminates toward transparent high-barrier coatings to enhance recyclability and consumer visibility. Pharmaceutical and medical applications form the most technically demanding and recession-resilient segment, requiring USP Class VI and ISO 10993 compliance, particularly in solid-dose blister packaging and sterilizable medical pouches. Personal care and cosmetics leverage barrier films for aesthetic differentiation and pouch conversion, influenced by PCR mandates. Electronics applications demand near-hermetic moisture protection (WVTR < 10⁻³ g/m²/day) for OLED and photovoltaic systems. Agriculture and chemicals remain cost-sensitive, emphasizing chemical resistance and emerging biodegradable film mandates in Western Europe.

Barrier Films Market Competitive Landscape

The global Barrier Films Market in 2026 is shaped by mono-material innovation, recycle-ready high-barrier structures, vapor-deposited coatings, and digitally optimized packaging systems. Leading manufacturers are moving rapidly toward aluminum-free oxygen barriers, transparent high-performance films, and AI-driven material lightweighting. Competitive differentiation now centers on recyclability compliance (95/5 standards), healthcare-grade thermoformed packaging, automated food systems, and localized production resilience. Strategic M&A, capacity expansions in North America and Europe, and next-generation BOPE/BOPP platforms are redefining shelf-life extension for fresh proteins, pharmaceuticals, pet food, and e-commerce packaging, positioning barrier films as a core enabler of circular flexible packaging.

Recycle-ready mono-material leadership and M&A-driven scale by Amcor plc

Amcor maintains global dominance by aggressively expanding its recycle-ready barrier film portfolio and consolidating specialty assets. In late 2025 and early 2026, Amcor finalized the acquisition of Berry Global Inc., significantly strengthening its high-barrier lidding and healthcare packaging footprint. Flagship AmLite® Ultra Recyclable and AmPrima® mono-polyolefin films deliver foil-like oxygen protection without aluminum. In Q1 2026, Amcor unveiled APET-based AmSecure thermoformed trays for clarity-retaining medical packaging while investing heavily in North American protein packaging capacity. Strategically, Amcor’s “Lift-Off Challenge” funds startups developing home-compostable oxygen barriers and nature-based additives, reinforcing its leadership in sustainable flexible packaging.

Transparent vapor-deposited barrier innovation from Toppan Inc.

Toppan leads the visibility-first barrier segment through its proprietary GL BARRIER technology, using vacuum-deposited alumina and silica to achieve near-foil protection in transparent films. Following acquisitions of an Italian BOPP specialist and Sonoco’s TFP business in 2025, Toppan expanded its European footprint and thermoformed packaging capabilities. Its GL-RD retortable films and GL-RP all-PP mono-material grades are gaining traction in pharmaceutical blister packs as foil replacements. Vertical integration from film production to laser scoring enables premium graphics on high-barrier substrates. Recent “metal-detector friendly” films further support food processors requiring full foreign-matter inspection with maximum moisture protection.

Paper-based high-barrier solutions driven by circular design at Mondi Group

Mondi differentiates through its “paper where possible, plastic when useful” strategy, scaling FunctionalBarrier Paper Ultimate in 2025/2026 to replace plastic-aluminum laminates in dry food and coffee packaging. The company earned nine WorldStar Awards for converting non-recyclable multilayer structures into high-strength kraft paper alternatives. Mondi is a leader in pet food and personal care with re/cycle mono-material PE films meeting 95/5 recyclability criteria, while transitioning to PE-free wrappers across European mills by mid-2026. Its in-house Product Impact Assessment tool provides cradle-to-gate carbon footprint validation, making Mondi a preferred partner for brands prioritizing paper-based barrier packaging and ESG transparency.

High-volume performance films and AI lightweighting by Berry Global Inc.

Now integrating into Amcor, Berry Global remains influential in industrial and consumer barrier films. In 2025, Berry scaled Silotite Film&Film agricultural wrap to improve fermentation while enabling full recyclability. Its printed shrink films and high-barrier lidding are complemented by AI-driven “right-sized” packaging tools that reduce material usage by up to 20% without sacrificing barrier integrity. Berry also expanded flexible tube production for personal care, incorporating sleeves with up to 50% recycled content. Strategically, Berry is strengthening domestic North American sourcing of EVOH and specialty resins, ensuring supply resilience amid ongoing trade and tariff volatility.

Automated high-barrier systems and digital twins at Sealed Air Corporation

Rebranded as SEE, Sealed Air leads at the intersection of barrier films and automation. Its Cryovac® Darfresh® skin packaging has become the 2026 benchmark for extending fresh protein shelf life without MAP. SEE now offers fully recyclable or reusable packaging across its portfolio, integrating high-barrier films with automated vacuum and cartoning systems for food and e-commerce fulfillment. A major differentiator is AI-simulated barrier performance, where digital twins predict oxygen and humidity behavior before physical prototyping. SEE also excels in temperature-assured packaging, embedding thermal liners into barrier films for biopharmaceutical distribution.

Cost-efficient BOPP and mono-material growth from Jindal Poly Films

Jindal Films dominates BOPP-based barrier solutions for snacks and labels, supported by late-2025 investments in BOPE production in Brindisi, Italy. Its BICOR™ and METALLYTE™ metallized films deliver near-foil oxygen and moisture barriers, optimized for India and Southeast Asia’s fast-growing e-commerce sector. In 2024/2025, Jindal launched PP mono-material barriers for high-speed HFFS confectionery lines, ensuring compatibility with legacy machinery. Under its “Growing Together” strategy, Jindal partners directly with packaging equipment OEMs to match mono-material performance with traditional multilayer speeds, accelerating global adoption of recyclable flexible packaging.

United States Barrier Films Market: Consolidation-Led Scale, Regulatory Scrutiny, and Circular Material Acceleration

The United States barrier films industry is undergoing a decisive structural realignment driven by large-scale consolidation, intensified food safety oversight, and accelerated investment in circular and compostable materials. A defining inflection point occurred in April 2025 with the all-stock acquisition of Berry Global Group, Inc. by Amcor plc. The combined entity now operates a diversified USD 20 billion portfolio, with a clear strategic emphasis on scaling high-value circular barrier films for healthcare, nutrition, and regulated food packaging applications across North America. This consolidation has strengthened R&D depth in multilayer barrier structures while improving customer access to recyclable and downgauged solutions.

Regulatory pressure is further reshaping material choices. In 2025, the U.S. Food and Drug Administration enhanced its Post-Market Review Framework, increasing scrutiny on PFAS-based barrier coatings in food-contact applications. This regulatory shift is accelerating industry-wide movement toward aqueous-based functional barriers and PFAS-free coatings. Sustainability investments are also expanding upstream capacity. Klöckner Pentaplast announced significant capital expenditure in 2025 to expand post-consumer recycled content availability for thermoformable barrier films used in protein and fresh food packaging. Product innovation remains strong, with Glenroy, Inc. expanding its TruRela™ portfolio in late 2025 to introduce recyclable stand-up pouches with ultra-high barrier performance capable of replacing traditional foil structures in coffee and snack packaging. At the same time, home-compostable solutions are moving from niche to pilot-scale commercialization. U.S.-based innovators Loliware and TIPA launched advanced metallized barrier films derived from seaweed and biodegradable polymers in early 2025. Interstate regulation is reinforcing material reduction strategies. Following the California Plastic Pollution Prevention Act, manufacturers have accelerated adoption of downgauged barrier shrink films that cut plastic weight by up to 75% while preserving puncture resistance and seal integrity.

India Barrier Films Market: EPR-Driven Design Shifts and Rapid Specialty Film Localization

India’s barrier films industry is evolving through regulatory-driven traceability, elevated recycling mandates, and increasing localization of specialty film production. Effective July 1, 2025, the Ministry of Environment, Forest and Climate Change mandated QR code or barcode integration on all plastic packaging, including barrier films, to enable full supply-chain traceability and verify Extended Producer Responsibility compliance. This requirement is driving investments in digital printing, smart packaging layers, and track-and-trace compatible barrier film designs.

On the supply side, domestic capacity is shifting toward higher-value segments. Cosmo Films launched its Cosmo Plastech division in 2025, focusing on specialty barrier sheets and injection-molded products for electronics and pharmaceutical export markets. Sustainability-oriented collaboration is also gaining traction. In March 2024, TOPPAN Inc. and Toppan Speciality Films introduced GL-SP, a transparent vapor-deposited barrier film using a BOPP substrate designed for global sustainability benchmarks. Regulatory escalation is intensifying material redesign. For fiscal year 2025–26, India’s Plastic Waste Management Rules increased recycling targets to 60% for key plastic categories, accelerating brand migration from complex multi-material laminates toward mono-material PE and PP barrier formats. In parallel, bio-based innovation is expanding. Leveraging agricultural feedstocks, Uflex Limited and peers are investing in starch- and cellulose-derived high-barrier coatings to support compostable packaging solutions for India’s fast-growing e-commerce sector.

China Barrier Films Market: Policy-Endorsed Localization and Digitalized Barrier Performance Control

China’s barrier films industry is advancing through strong policy endorsement, rapid material substitution, and industrial digitalization. The government’s 2025 Edition of the Encouraged Catalogue for Foreign Investment explicitly prioritizes high-performance, environmentally friendly barrier films, offering tax incentives for localized production of advanced SiOx-coated structures. This policy stance is accelerating foreign and domestic investments in high-barrier flexible packaging for food, healthcare, and export-oriented applications.

Large-scale chemical integration is reinforcing closed-loop material strategies. BASF’s Zhanjiang Verbund site, coming online during 2025–2026, is producing Ultramid® Ccycled® polyamides that are already being deployed in China and Germany for closed-loop high-barrier meat packaging. Regulatory standards are simultaneously reshaping material selection. Implementation of GB 2760-2024 and related 2025 environmental codes has driven a rapid phase-out of traditional PVDC-coated barrier films, accelerating adoption of EVOH-free and AlOx-coated alternatives, particularly for fresh-cut produce and refrigerated foods. Operational efficiency is also improving through digitalization. Under the Ministry of Industry and Information Technology’s Industrial Digital Transformation Blueprint 2026, major Chinese film extruders have deployed AI-enabled real-time barrier monitoring systems to optimize multilayer co-extrusion, reduce material waste, and stabilize barrier performance at scale.

Germany Barrier Films Market: Circular Economy Mandates and Advanced Polyolefin Barrier Leadership

Germany represents a high-regulation, high-innovation market for barrier films, where circular economy mandates and advanced polyolefin technologies are redefining competitive advantage. Under Regulation (EU) 2025/40, Germany has implemented a stringent framework requiring all barrier packaging to be designed for recycling by 2030, unlocking a multi-billion-dollar opportunity for bio-based and recyclable alternatives. This regulation is accelerating substitution of non-recyclable multilayer structures with mono-material and chemically recyclable barrier formats.

German converters are leading this transition. In 2025, Werz, in collaboration with BASF, successfully launched a closed-loop barrier film system for the Horeca sector using chemically recycled materials. Product-level innovation continues to advance. Klöckner Pentaplast introduced FlexiFlow EH 155 R, a recyclable high-barrier flow-wrap that significantly lowers carbon intensity for dairy and meat producers. Germany’s leadership in machine-direction-oriented polyethylene films and recyclable barrier engineering positions it as a reference market for sustainable barrier film design across Europe.

Country-Level Strategic Snapshot: Barrier Films Industry

Barrier Films Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Key Developments (2024–2026)

|

|

United States

|

Consolidation and PFAS-free transition

|

Major merger, FDA scrutiny, PCR investment, compostable and downgauged barrier adoption

|

|

India

|

EPR compliance and specialty film localization

|

QR mandates, higher recycling targets, BOPP vapor-deposited films, bio-based coatings

|

|

China

|

Policy-backed localization and digitalization

|

Encouraged investment status, PVDC phase-out, AI-enabled barrier monitoring

|

|

Germany

|

Circular economy leadership and MDO-PE innovation

|

EU recycling mandates, closed-loop systems, recyclable high-barrier flow-wraps

|

Barrier Films Market Report Scope

Barrier Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$70 Billion

|

|

Market Size (2034)

|

$116.3 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (Polyethylene, Polyethylene Terephthalate, Polypropylene, Polyamide, Ethylene Vinyl Alcohol, Aluminum Foil, Biopolymers), By Type (Metallized Barrier Films, Transparent Barrier Films, Opaque Barrier Films, Multilayer Co Extruded Films), By Packaging Format (Bags and Pouches, Tray Lidding Films, Thermoforming Films, Shrink and Stretch Films, Blister Films, Vacuum Skin Packaging), By End Use Industry (Food and Beverage, Pharmaceutical and Medical, Personal Care and Cosmetics, Electronics, Agriculture and Chemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Group, Mondi Group, Huhtamaki Oyj, Sealed Air Corporation, Constantia Flexibles, Toppan Inc, Winpak Ltd, Jindal Films, Cosmo First, Toray Industries, Uflex Limited, ProAmpac, Klockner Pentaplast, Schur Flexibles Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Barrier Films Market Segmentation

By Material Type

- Polyethylene

- Polyethylene Terephthalate

- Polypropylene

- Polyamide

- Ethylene Vinyl Alcohol

- Aluminum Foil

- Biopolymers

By Type

- Metallized Barrier Films

- Transparent Barrier Films

- Opaque Barrier Films

- Multilayer Co Extruded Films

By Packaging Format

- Bags and Pouches

- Tray Lidding Films

- Thermoforming Films

- Shrink and Stretch Films

- Blister Films

- Vacuum Skin Packaging

By End Use Industry

- Food and Beverage

- Pharmaceutical and Medical

- Personal Care and Cosmetics

- Electronics

- Agriculture and Chemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Barrier Films Industry

- Amcor plc

- Berry Global Group

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Constantia Flexibles

- Toppan Inc

- Winpak Ltd

- Jindal Films

- Cosmo First

- Toray Industries

- Uflex Limited

- ProAmpac

- Klockner Pentaplast

- Schur Flexibles Group

*- List not Exhaustive