Oxygen Barrier Materials Market Driven by EVOH Capacity Expansion and Recyclable Mono-Material Innovation

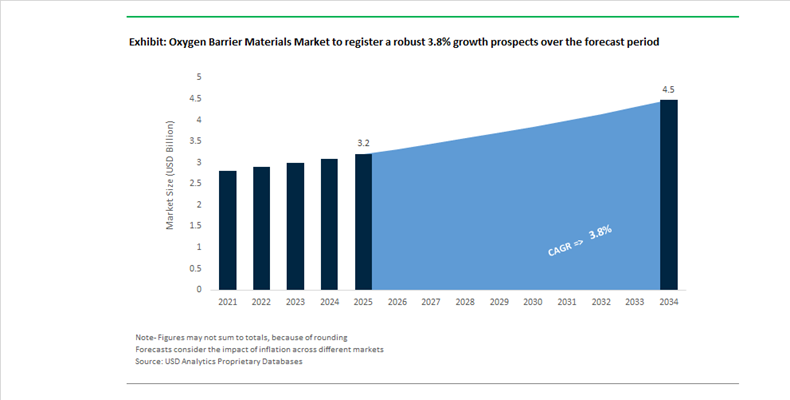

The Oxygen Barrier Materials Market is projected to increase from $3.2 billion in 2025 to $4.5 billion by 2034, registering a CAGR of 3.8%. Growth is being shaped by regulatory pressure on multilayer plastics, rising demand for extended shelf life in food and pharmaceutical packaging, and the automotive sector’s continued reliance on high-barrier resins for fuel system components. Ethylene Vinyl Alcohol (EVOH), polyvinyl alcohol (PVOH), barrier-coated polyolefins, and emerging aluminum-free technologies are central to this transition. The competitive landscape is increasingly defined by capacity localization, recyclability mandates, and mono-material engineering.

In October 2024, Honeywell announced the spin-off of its Advanced Materials business into Solstice Advanced Materials Inc., expected to complete in 2025. The portfolio includes high-performance barrier films and specialty additives serving packaging and industrial markets. This restructuring reflects the strategic separation of specialty barrier technologies from diversified conglomerate structures, allowing sharper capital allocation toward high-margin materials science. In March 2024, Greif completed the acquisition of Ipackchem Group SAS, strengthening its position in recyclable high-barrier plastic containers capable of incorporating up to 50% post-consumer recycled content. This transaction underscores the shift toward circular industrial packaging solutions where oxygen barrier performance must coexist with recyclability compliance.

Capacity expansion in EVOH remains a structural growth lever. In July 2025, Mitsubishi Chemical Group is scheduled to commence production at its expanded SoarnoL™ EVOH facility in the United Kingdom, adding 21,000 tonnes annually to address European food packaging and automotive fuel tank demand. Similarly, Kuraray confirmed that its new EVAL™ EVOH plant in Singapore will begin operations in 2026, following a 2024 expansion in Belgium. These investments secure regional supply chains and mitigate logistics volatility, particularly as pharmaceutical blister packs and retort food pouches require consistent oxygen transmission rates below critical thresholds.

Sustainable packaging design is accelerating material innovation. In October 2024, Klöckner Pentaplast introduced kp FlexiFlow EH 155 R and PH 255 R recyclable barrier flow wraps, reducing packaging weight by up to 75% while maintaining high oxygen barrier performance for fresh food. In March 2024, TOPPAN launched GL-SP, a BOPP-based transparent barrier film designed for mono-material food packaging. In North America, Amcor expanded its AmFiber™ curbside-recyclable paper laminate portfolio in 2024, achieving widely recyclable certification while delivering oxygen protection comparable to plastic laminates.

Technological breakthroughs are targeting aluminum replacement and coating innovation. In October 2025, Jiangnan University researchers demonstrated an aluminum-free high-barrier dairy packaging material using natural extracts and 2D layered structures, achieving foil-equivalent oxygen protection in a 100,000-unit pilot. In January 2026, Swansea University researchers introduced a modified PVOH (m-PVOH) coating on PET with oxygen permeance below 0.05 cm³/m²/day/atm, stable in ambient moisture but removable in hot water to enable high-purity PET recycling. Concurrently, Solenis partnered with Heidelberger Druckmaschinen in September 2024 to integrate oxygen-resistant barrier coatings directly into flexographic printing processes, enabling fiber-based packaging to compete with multilayer plastic laminates.

Commercial Trends and Revenue-Generating Opportunities in the Oxygen Barrier Materials Market

Lithium-Ion Battery Logistics Drive Mandatory Adoption of High-Barrier Packaging Materials

The global acceleration of lithium-ion battery production for electric vehicles, energy storage systems, and consumer electronics is fundamentally reshaping packaging requirements across battery logistics and transportation. Safety has moved from a compliance checkbox to a cost-critical operational risk, particularly during long-duration air and sea freight where exposure to oxygen ingress, mechanical damage, and temperature variation can amplify thermal runaway risks. As a result, oxygen barrier materials are increasingly specified as a mandatory component of battery secondary and tertiary packaging.

The enforcement of the 66th Edition of the International Air Transport Association Dangerous Goods Regulations in 2025 marks one of the most consequential regulatory shifts for battery transport in the past decade. Packaging solutions are now required to minimize internal gas accumulation, reduce external short-circuit risks, and maintain structural integrity across complex logistics chains. This has accelerated demand for barrier-coated fiberboard, high-purity polyamide liners, and metallized polymer films that combine puncture resistance with gas-tight sealing performance.

In parallel, the UN 38.3 8th Edition certification has become a non-negotiable prerequisite for global lithium battery trade in 2025. Packaging manufacturers are responding by qualifying multi-layer structures such as metallized PET and oxidized polyethylene films that can withstand extreme temperature cycling from minus 40 degrees Celsius to plus 72 degrees Celsius without degradation of oxygen barrier performance. Regulatory tightening has further intensified following the February 2025 amendments to battery waste management rules in major markets including the EU and India. These rules are pushing battery producers toward flame-retardant, high-barrier packaging designs, accelerating the shift away from aluminum foils toward silicon oxide coated films that deliver inert gas protection without electrical conductivity risks. Collectively, these developments are transforming oxygen barrier materials from a cost line item into a strategic enabler of compliant, insurable battery logistics.

Recyclable Mono-Material High-Barrier Packaging Becomes a Strategic Imperative

Sustainability regulation is rapidly reshaping the economics of flexible packaging, with oxygen barrier materials at the center of this transition. The EU Packaging and Packaging Waste Regulation, which entered into force in February 2025, is forcing converters and brand owners to rethink traditional multi-layer laminate structures that are incompatible with mechanical recycling. The market is now moving decisively toward mono-material packaging formats that maintain high oxygen barrier performance while meeting recyclability thresholds.

Under the PPWR Design for Recycling mandates, packaging placed on the EU market must achieve Grade A recyclability by 2038, effectively requiring 95% material recovery. This has catalyzed the development of mono-polypropylene and mono-polyethylene films that incorporate oxygen barrier technologies such as EVOH at concentrations below 5% by weight. This threshold-based integration allows converters to preserve low oxygen transmission rates suitable for snacks, coffee, and dry foods while remaining compatible with existing recycling streams.

Commercial innovation is accelerating. In early 2025, Mondi and Henkel finalized the rollout of a fully recyclable mono-material refill pouch using high-density polyethylene with an internal barrier coating. The design delivers up to 70% plastic reduction versus rigid containers while preserving shelf-life performance for liquid detergents and personal care products. Similarly, Jindal Films has committed to launching multiple high-barrier BOPP films annually, achieving oxygen transmission rates below 0.1 cubic centimeters per square meter per day in metal-free, recyclable formats. These shifts indicate that oxygen barrier materials are becoming a strategic differentiator in sustainable packaging portfolios rather than a passive functional layer.

Ultra-High Barrier Materials Unlock Scale-Up in Flexible Electronics and Solar Applications

The commercialization of foldable displays and next-generation photovoltaic technologies is opening a premium growth corridor for ultra-high-performance oxygen barrier materials. Unlike food packaging, these applications demand near-zero oxygen and moisture ingress to protect sensitive electronic layers over long operational lifetimes. As flexible OLED displays and perovskite solar cells move from pilot lines to commercial-scale manufacturing, barrier reliability is becoming a yield and warranty determinant.

Advanced thin-film encapsulation technologies are now a focal point of investment. Barrier performance targets in the range required for organic electronics have driven increased adoption of multilayer coatings that combine inorganic gas-blocking layers with organic defect-smoothing interlayers. Recent breakthroughs reported in late 2025 demonstrate that solution-processed silicon nitride barriers can be produced at industrial speeds, materially reducing the cost and complexity of ultra-high barrier film production. This cost inflection is critical for scaling foldable smartphones and flexible solar modules beyond niche markets.

For perovskite solar cells, which are increasingly targeting operational lifespans comparable to silicon photovoltaics, demand for robust encapsulation is accelerating. Manufacturers are trialing advanced stop-layer films that maintain barrier integrity even under extreme humidity and thermal stress. As device makers prioritize long-term stability to secure bankability and insurance coverage, oxygen barrier materials are emerging as a decisive factor in the commercialization trajectory of flexible electronics and next-generation solar technologies.

Modified Atmosphere Packaging Expands in Plant-Based and Fresh Produce Segments

The rapid growth of plant-based proteins and fresh-cut produce is driving a shift from passive to active oxygen barrier materials in food packaging. These products are highly sensitive to oxidation, discoloration, and microbial spoilage, making oxygen management a critical determinant of shelf life, waste reduction, and retail acceptance. Modified Atmosphere Packaging is increasingly adopted to fine-tune internal oxygen and carbon dioxide levels, extending freshness while preserving visual appeal.

Plant-based meat alternatives are a key driver. As of late 2025, major retailers have expanded the use of MAP solutions to maintain the color stability and oxidative integrity of plant-based red meat analogs. By combining controlled oxygen atmospheres with polyethylene and polyamide co-extruded films, producers have extended refrigerated shelf life by up to 21 days while reducing returns and markdowns.

Innovation is also accelerating in fresh-cut produce. Advanced oxygen barrier films integrated with anti-fog and UV-blocking functionality are reducing enzymatic browning and moisture condensation in pre-cut salads and vegetables. Commercial deployment of UV-blocking barrier solutions has been shown to reduce retail food waste by 15% to 20%. At the same time, compostable high-barrier films are entering the market, offering oxygen and moisture protection suitable for snacks and produce while supporting organic waste disposal routes. These developments position oxygen barrier materials as a central enabler of value creation across premium, sustainability-driven food categories.

Oxygen Barrier Materials Market Share and Segmentation Insights

Ethylene Vinyl Alcohol Leads Oxygen Barrier Materials Market with Ultra-Low Oxygen Transmission Performance

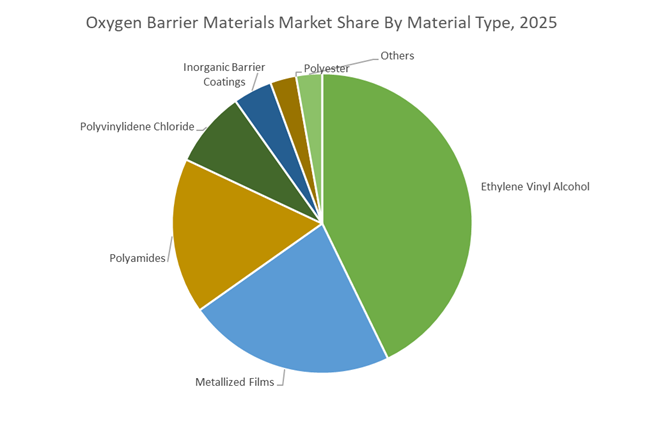

Ethylene vinyl alcohol accounted for 42.80% of the Oxygen Barrier Materials Market by material type in 2025, establishing it as the leading barrier polymer used in high-performance packaging structures. EVOH is widely adopted because it delivers extremely low oxygen transmission rates, often reaching 0.01 cc/m²/day, which makes it highly effective for preserving oxygen sensitive food products. This polymer is commonly incorporated into multilayer packaging structures where it is protected from moisture while providing superior oxygen barrier protection. In 2025, manufacturers are focusing on EVOH barrier layer optimization, developing grades with improved barrier efficiency at reduced thickness, enabling downgauging of packaging structures while maintaining oxygen protection and improving compatibility with polyolefin tie layers in multilayer coextrusion systems.

Food and Beverage Packaging Drives Oxygen Barrier Material Consumption for Shelf Life Extension

The food and beverage sector accounted for 68.40% of the Oxygen Barrier Materials Market by end-use industry in 2025, reflecting the critical role oxygen barrier packaging plays in protecting oxygen sensitive food products. Processed meats, dairy products, coffee, snacks, ready meals, and beverage products require advanced barrier packaging to maintain freshness, flavor stability, and nutritional quality during storage and transportation. Flexible and rigid packaging structures incorporating EVOH, metallized films, and high barrier polymers are widely used across food processing supply chains. In 2025, the growing emphasis on food waste reduction across global supply chains is increasing demand for advanced oxygen barrier packaging solutions that extend shelf life, reduce spoilage, and support sustainability initiatives in retail and packaged food distribution networks.

Oxygen Barrier Materials Market Competitive Landscape

The Oxygen Barrier Materials Market is rapidly evolving toward mono-material recyclable films, bio-based EVOH resins, and high-performance oxygen transmission rate (OTR) solutions. Market leaders are investing in circular packaging technologies, AI-driven manufacturing, and lightweight barrier structures to meet EPR regulations and food-grade sustainability requirements.

Kuraray expands EVOH capacity to secure global high-barrier packaging demand

Kuraray Co., Ltd. continues to dominate the oxygen barrier materials market through its EVAL™ EVOH resin, delivering up to 10,000 times higher oxygen barrier performance than conventional polyethylene. The planned expansion of its Singapore production facility, following earlier capacity additions in Belgium, strengthens supply chain resilience for Asia-Pacific food packaging markets. A global price revision in 2026 reflects rising raw material and logistics costs while maintaining premium positioning. With 79.2% of sales generated outside Japan, Kuraray’s localized manufacturing model minimizes lead times for global FMCG packaging clients. The company is also scaling VECTRAN™ liquid crystal polymer production to support advanced industrial and aerospace barrier applications. This combination of capacity expansion, pricing strategy, and global reach reinforces its market leadership.

Mitsubishi Chemical advances recyclable EVOH coatings with AI-driven low-carbon production

Mitsubishi Chemical Group (MCG) is strengthening its position through SoarnoL™ EVOH innovations aligned with circular economy packaging trends. Its breakthrough PFAS-free coating technology enables paper-based substrates to achieve high gas barrier and oil resistance, targeting commercial rollout by 2026. The doubling of production capacity at its Hull facility to 18,000 tonnes annually establishes Europe’s largest EVOH manufacturing hub. Under its KAITEKI Vision 35, MCG is deploying AI-driven manufacturing to reduce carbon emissions by 20–30% in high-barrier film production. SoarnoL™ resins are increasingly used in mono-material recyclable packaging structures compatible with polyolefin recycling streams. This integration of sustainability, scale, and advanced materials positions MCG strongly in next-generation packaging solutions.

Amcor accelerates mono-material high-barrier packaging with recyclable OTR solutions

Amcor plc is leading the transition to recyclable oxygen barrier materials through its Responsible Packaging strategy and advanced mono-material film technologies. The launch of high-barrier polyolefin packaging for premium pet food demonstrates its ability to replace aluminum laminates while maintaining comparable oxygen protection. Its AmLite Ultra Recyclable range delivers up to 64% carbon footprint reduction by eliminating PET and aluminum layers. Through its Lift-Off innovation program, Amcor is fostering development of compostable and bio-based OTR barrier solutions. Strategic investments via Amcor Ventures further support dispersion-coated barrier technologies for paper packaging. This focus on recyclability, innovation ecosystems, and carbon reduction strengthens Amcor’s leadership in sustainable flexible packaging.

Berry Global scales lightweight high-barrier packaging with recycled content integration

Berry Global Group, Inc. is enhancing its competitive position through lightweight, high-barrier packaging solutions that reduce material usage without compromising performance. Its newly introduced packaging line achieves approximately 15% material reduction while maintaining oxygen barrier integrity for food preservation. The acquisition of a specialized flexible films business strengthens its capacity in high-barrier pet food packaging across North America and Europe. BerryBarrier™ PCR solutions integrate post-consumer recycled content into barrier structures, balancing sustainability with OTR performance. The company’s global manufacturing footprint supports localized production of mono-material containers for nutraceutical and food applications. This combination of material efficiency, recycling integration, and scale drives Berry’s market competitiveness.

Toppan leads transparent barrier films with vapor deposition and smart packaging integration

Toppan Holdings Inc. is a global leader in transparent oxygen barrier films, leveraging its GL BARRIER technology to replace aluminum-based laminates in flexible packaging. Its GL-SP innovations enable high-performance, eco-friendly barrier films tailored for premium nutrition and retort packaging applications. Collaboration with Toppan Speciality Films in India is accelerating production of BOPP-based barrier films for rapidly growing Asian markets. These solutions provide microwaveability, product visibility, and strong oxygen barrier performance for shelf-stable foods. Toppan is also integrating digital traceability features into its films, enabling real-time monitoring of OTR performance across supply chains. This convergence of material science and smart packaging positions Toppan at the forefront of advanced barrier technologies.

Japan – Bio-Circular Barriers and Hydrogen-Grade Performance Materials

Japan is setting the technical and sustainability benchmark for oxygen barrier materials through rapid commercialization of bio-circular polymers and expansion into hydrogen infrastructure. At the K 2025 trade fair, Kuraray introduced ISCC PLUS certified EVAL™ EVOH resins, enabling food and medical packaging converters to lower lifecycle carbon footprints without compromising ultra-high oxygen barrier performance. This development aligns with the February 2025 “Plan for Global Warming Countermeasures,” which provides targeted subsidies for advanced barrier production lines that support national decarbonization goals. Beyond packaging, Japan is extending oxygen barrier science into energy systems, with specialized EVAL™ multilayer liners now deployed in next-generation hydrogen tanks to prevent gas permeation under extreme pressure conditions.

Material innovation is also being driven by downstream application shifts. Sumitomo Chemical and Mitsubishi Chemical Group have intensified R&D around high-heat and UV-resistant acrylics for EV lighting and sensor housings, where oxygen ingress can accelerate material degradation. In pharmaceuticals, transparent high-barrier blister films are replacing aluminum foils to allow visual inspection while maintaining protection against oxygen-sensitive formulations. Parallelly, Polyplastics is scaling TOPAS® COC to reinforce PE mono-material pouches, ensuring compatibility with Japan’s advanced recycling streams while delivering improved stiffness and oxygen barrier integrity.

Germany – Mono-Material Transition and PFAS-Free Barrier Systems

Germany’s oxygen barrier materials market is being reshaped by circular economy mandates and chemical regulation leadership. By October 2025, over 40% of new food packaging specifications had shifted toward recyclable mono-material PE or PP structures enhanced with thin-film oxygen barriers, reflecting compliance with EU circular packaging targets. BASF SE has reinforced this transition through implementation of mass balance production at its specialty dispersion facilities, enabling lower-carbon barrier coatings for construction, automotive, and industrial applications. Investments in Controlled Free Radical Polymerization technology further enhance coating stability in demanding environments.

Regulatory anticipation is a defining factor. Evonik Industries launched PFAS-free TEGO® PPA grades in late 2025, positioning converters ahead of forthcoming EU chemical restrictions. Paper-based packaging has also seen a breakthrough, with Kuraray’s Poval™ and EXCEVAL™ polymers enabling fluorine-free aqueous oxygen barriers that allow paper laminates to compete with plastic structures. Collectively, these developments position Germany as a premium hub for compliant, recyclable, and low-toxicity oxygen barrier solutions.

United States – Transparent High-Barrier Films and Semiconductor Protection

The United States oxygen barrier materials landscape is characterized by transparency-driven innovation and cross-sector demand from food, pharma, and semiconductors. In September 2025, Avery Dennison launched UV Barrier clear film labels that combine oxygen protection with UV shielding for light-sensitive biologics, addressing regulatory and stability requirements without sacrificing visibility. The company also introduced PET labels with chemically recycled content for EV battery applications, where long-term oxygen resistance and flame retardancy are critical.

Advanced inorganic barrier technologies are gaining traction. U.S. manufacturers scaled Aluminum Oxide coated films by late 2024 to support windowed snack packaging trends that demand both transparency and high oxygen resistance. Policy influence is also evident, as the CHIPS Act is accelerating adoption of ultra-purity oxygen barrier materials for semiconductor wafer transport and storage. Food waste reduction initiatives targeting a 50% cut by 2030 are further driving integration of active oxygen scavengers into barrier films for meat and dairy packaging.

China – Capacity Localization and Green Building Alignment

China is rapidly localizing oxygen barrier material production to support domestic food, construction, and automotive demand. The 2025–2026 green building materials plan, issued by multiple ministries including Ministry of Industry and Information Technology of China, prioritizes high-barrier insulation materials as part of a targeted 300 billion yuan revenue objective. In parallel, BASF SE launched a high-performance dispersant production line in Nanjing in November 2025, enabling local supply of advanced barrier additives for Asian coatings markets.

China has also expanded domestic EVOH capacity in 2025 to reduce reliance on Japanese imports for shelf-stable convenience foods. However, April 2025 export controls on select rare-earth-related items are indirectly increasing costs for specialized inorganic barrier coatings that rely on doped materials. On the innovation front, Chinese research institutes are advancing chitosan and cellulose-based oxygen barrier coatings, targeting commercialization in agricultural films by 2027 and reinforcing the country’s push toward biodegradable barrier technologies.

Türkiye – Regional Hub for Low-Carbon Barrier Additives

Türkiye is emerging as a strategic regional production base for oxygen barrier additives serving Europe, the Middle East, and North Africa. In October 2025, BASF SE commissioned a new production line in Dilovası to manufacture low-VOC and low-CO2 dispersions for architectural coatings. This facility strengthens local-for-local supply while reducing logistics-related emissions for neighboring markets.

A distinguishing feature of the Turkish expansion is its sustainability profile. The Dilovası site operates on 100% green electricity, positioning it among the first oxygen barrier additive plants in the region with a net-zero power footprint. This combination of geographic proximity, regulatory alignment, and low-carbon manufacturing enhances Türkiye’s role as an emerging hub in the global oxygen barrier materials value chain.

Comparative Snapshot – Oxygen Barrier Materials by Country

Oxygen Barrier Materials Market County Level Snapshot

|

Country

|

Primary Focus Area

|

Policy or Industry Lever

|

Strategic Role

|

|

Japan

|

Bio-circular EVOH and hydrogen liners

|

Decarbonization subsidies

|

Technology and performance benchmark

|

|

Germany

|

Recyclable mono-material barriers

|

EU circular economy and PFAS regulation

|

Premium compliant solutions

|

|

United States

|

Transparent high-barrier films

|

CHIPS Act and food waste targets

|

Cross-sector innovation hub

|

|

China

|

EVOH localization and green buildings

|

MIIT green materials plan

|

Scale-driven domestic supply

|

|

Türkiye

|

Low-CO2 dispersions

|

Green electricity transition

|

Regional production gateway

|

Oxygen Barrier Materials Market Report Scope

Oxygen Barrier Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Material Type (Ethylene Vinyl Alcohol, Polyvinylidene Chloride, Polyacrylonitrile, Polyamides, Cyclic Olefin Copolymers, Polyester, Inorganic Barrier Coatings, Metallized Films, Bio-Based Polymers), By Product Format (Films and Sheets, Coatings, Resins and Concentrates, Active Scavengers), By Packaging Type (Flexible Packaging, Rigid Packaging, Lidding Films, Shrink and Stretch Wraps), By End-Use Industry (Food and Beverage, Pharmaceutical and Healthcare, Automotive, Electronics, Industrial)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kuraray, Mitsubishi Chemical Group, Amcor, BASF, Berry Global, Sealed Air, Toppan Holdings, Dai Nippon Printing, Arkema, Honeywell International, Evonik Industries, Solvay, Polyplastics, Avery Dennison, Huhtamaki

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oxygen Barrier Materials Market Segmentation

By Material Type

- Ethylene Vinyl Alcohol

- Polyvinylidene Chloride

- Polyacrylonitrile

- Polyamides

- Cyclic Olefin Copolymers

- Polyester

- Inorganic Barrier Coatings

- Metallized Films

- Bio-Based Polymers

By Product Format

- Films and Sheets

- Coatings

- Resins and Concentrates

- Active Scavengers

By Packaging Type

- Flexible Packaging

- Rigid Packaging

- Lidding Films

- Shrink and Stretch Wraps

By End-Use Industry

- Food and Beverage

- Pharmaceutical and Healthcare

- Automotive

- Electronics

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oxygen Barrier Materials Industry

- Kuraray

- Mitsubishi Chemical Group

- Amcor

- BASF

- Berry Global

- Sealed Air

- Toppan Holdings

- Dai Nippon Printing

- Arkema

- Honeywell International

- Evonik Industries

- Solvay

- Polyplastics

- Avery Dennison

- Huhtamaki

*- List not Exhaustive