Pouches Market Overview: Growth Driven by Food, Beverage, and Sustainability Trends

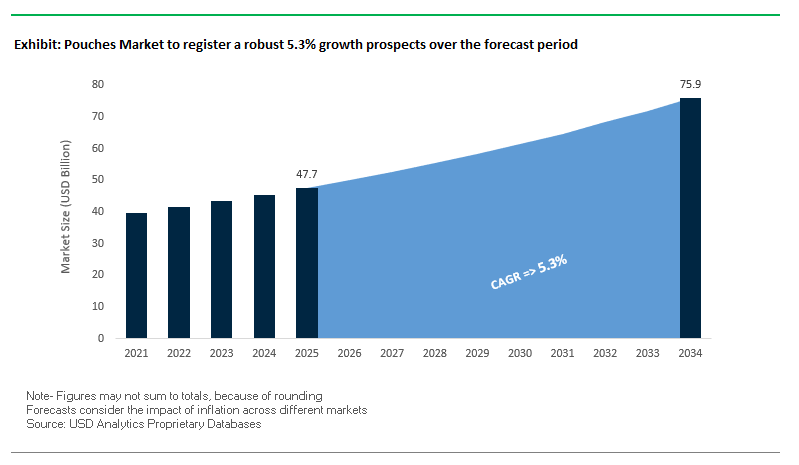

The Global Pouches Market is valued at $47.7 billion in 2025 and is projected to reach $75.9 billion by 2034, expanding at a CAGR of 5.3%. Pouches have emerged as one of the most versatile flexible packaging solutions, combining lightweight design, convenience, and cost efficiency. The food and beverage sector remains the largest consumer of pouches, driven by strong demand for ready-to-eat meals, baby food, snacks, and beverages. Their portability, resealability, and barrier properties make them the preferred choice for brands targeting both on-the-go consumption and extended shelf life.

Sustainability is reshaping the pouch packaging industry. Leading FMCG, pharmaceutical, and personal care companies are increasingly shifting toward monomaterial pouches and PCR (post-consumer recycled) content. Monomaterials simplify the recycling process and are considered a critical step in advancing circular economy models. Meanwhile, lightweight design provides transportation efficiencies by lowering freight costs and reducing carbon emissions, making pouches an essential component of modern supply chains.

Beyond sustainability, the industry is also witnessing innovation in digital printing, barrier performance, and smart packaging. Pouches now serve as branding platforms that enhance the consumer unboxing experience, particularly in e-commerce, where shelf appeal and product safety must coexist. The demand is further fueled by healthcare and nutraceutical industries, where child-resistant and high-barrier pouches are becoming integral to compliance and patient safety.

Key Insights for Industry Professionals

- Food and beverage sector dominates global pouch consumption, particularly in baby food, snacks, and ready-to-eat products.

- Monomaterial pouches are gaining traction for their recyclability and ease of integration into circular economy systems.

- Lightweight and portable advantages reduce logistics costs and carbon footprint compared to rigid packaging.

- E-commerce adoption is accelerating the need for durable, visually appealing pouch designs.

Market Analysis: Recent Industry Developments Shaping the Pouch Sector

The pouch packaging market is undergoing consolidation and technological advancement, marked by acquisitions, investments, and product innovations. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, reinforcing its ability to serve Latin American pharmaceutical markets, a key growth segment for sterile pouches. That same month, Duravant acquired Pattyn, a packaging automation systems provider, highlighting the integration of automation with flexible packaging growth.

Also in August 2025, ProAmpac acquired PAC Worldwide, strengthening its foothold in e-commerce and logistics pouch packaging, particularly for secure shipping and protective solutions. Mondi reported strong half-year results in August 2025, showcasing the impact of its sustainable product lines, while Constantia Flexibles announced a €100 million investment in July 2025 to expand its production of sustainable pouches.

Similarly, Sonoco announced a $30 million expansion in July 2025 to increase its adhesives and sealants capacity, which directly supports pouch sealing and laminating operations. Earlier, in January 2025, Smurfit WestRock introduced an all-paper stretch wrap for pallets, signaling the broader trend toward paper-based alternatives, while Nefab Group in November 2024 showcased its EdgePak Collar, a recyclable lightweight solution complementing circular economy packaging.

Finally, M&A activity is reshaping leadership. Amcor’s $8.4 billion acquisition of Berry Global in November 2024 created a new global giant in plastics and healthcare packaging, consolidating capabilities in flexible pouch formats.

Transformative Trends and Growth Opportunities in the Pouches Market

Accelerated Adoption of Recyclable Mono-Material Structures

A fundamental transition is underway from multi-layer laminates toward recyclable mono-material pouch designs, predominantly polyethylene (PE) and polypropylene (PP). This shift is driven by Extended Producer Responsibility (EPR) regulations, such as those emerging in multiple U.S. states, and the EU’s Circular Economy Action Plan. At the brand level, Nestlé has already achieved recyclability readiness for 89.5% of its total packaging and 86.4% of its plastic packaging by the end of 2024, demonstrating the market-wide push to meet 2025 circularity targets.

Technological advances have made mono-material structures more commercially viable, especially for applications requiring strong barrier properties. For example, new all-PE pouch structures for cheese deliver the same product protection as laminates while cutting non-renewable energy use by 25% and carbon emissions by 41%. Collaborations are central to this shift, with companies like Siegwerk and Borouge co-developing ink and coating systems tailored for mono-material packaging. These innovations make it possible to achieve durability, seal integrity, and aesthetics while maintaining recyclability.

Proliferation of High-Pressure Processing (HPP) Compatible Pouches for Fresh Food

The clean-label and fresh food movement is fueling strong demand for pouches designed to withstand High-Pressure Processing (HPP). This non-thermal pasteurization method preserves nutrients and extends shelf life, which is vital for categories such as cold-pressed juices, plant-based meals, and baby food. The FDA’s recognition of HPP as a safe pasteurization method has further accelerated adoption. Studies show that HPP can extend milk’s refrigerated shelf life to 60 days while retaining more than 90% of vitamins and minerals.

To meet these requirements, pouch designs must offer high flex-crack resistance and robust seals capable of withstanding pressures of 50,000–87,000 psi. Innovations in polymer blends and advanced sealant technologies are ensuring that leakage and structural failures are avoided. For brands, adopting HPP-compatible pouches allows differentiation by offering premium, preservative-free products while supporting consumer demand for fresh-tasting, nutrient-rich food experiences.

Development of Advanced Bio-Based and Marine-Degradable Films

A major opportunity lies in commercializing bio-based and marine-degradable pouch films that address end-of-life challenges for flexible packaging, particularly in regions lacking waste collection infrastructure. Research into polysaccharides, lipids, and seaweed-derived materials shows strong potential for creating biodegradable pouches with water barrier and tensile properties comparable to petroleum-based plastics.

Marine-degradable plastics are gaining urgency in light of mounting ocean pollution concerns. Companies like Mitsui & Co. are investing in biomass-derived plastics that meet new international standards for marine degradability. Furthermore, innovative “pouch-in-pouch” composite systems are being trialed, combining a moisture-resistant outer layer with an inner oxygen-barrier biodegradable film made from starch or PVA. This dual-layer approach balances performance with environmental responsibility, opening new avenues for sustainable packaging solutions in premium food categories.

Integration of Digital Watermarking for Intelligent Recycling

Digital watermarking, pioneered under the HolyGrail 2.0 initiative, represents a breakthrough for solving the recyclability challenge of flexible pouches. Invisible codes embedded on packaging can be scanned by high-speed cameras at material recovery facilities (MRFs), enabling sorting by polymer type and food vs. non-food use. Industrial trials in Germany demonstrated detection accuracy of up to 93.8% and throughput of 56,000 detections per day, proving large-scale feasibility.

The impact of this innovation is significant: it enables high-purity separation of flexible plastics, which is essential for producing food-grade recycled content. This aligns closely with regulatory targets for recycled material usage while supporting corporate sustainability strategies. Industry bodies such as AIM and the Alliance to End Plastic Waste are pushing commercialization to meet EU and global recycling mandates. By adopting digital watermarking, brands can not only future-proof their packaging compliance but also secure access to high-quality recycled resins critical for the next generation of circular pouch packaging.

Competitive Landscape: Key Companies in the Global Pouches Market

The pouches industry is characterized by a mix of global leaders and innovative mid-tier companies, with strong emphasis on sustainability, barrier technologies, and customization.

Amcor plc: Innovating with High-Barrier and Sustainable Pouches

Amcor is a leading global provider of flexible and rigid packaging with a strong pouch portfolio spanning retort, stand-up, and spout formats. Its AmLite line offers recyclable, metal-free, high-barrier pouches, while Vento integrates one-way venting systems for applications like coffee. With operations in over 40 countries, Amcor leverages its global scale to meet both local and multinational client demands.

Constantia Flexibles Group GmbH: Advancing Eco-Friendly High-Barrier Pouches

Constantia Flexibles specializes in high-barrier pouches for food and pharmaceutical applications. Awarded two WorldStar Global Packaging Awards in 2025, the company leads in sustainable innovation with products such as EcoPeelCover and EcoLamHighPlus. In August 2025, it committed €100 million to expand global production, reflecting its focus on scaling eco-friendly pouch solutions.

Mondi Group: Expanding Paper-Based and Mono-Material Pouch Solutions

Mondi delivers a broad range of paper- and plastic-based pouches, including retortable, spouted, and stand-up designs. Its FunctionalBarrier Papers and mono-material barrier pouches are designed for recyclability while maintaining durability and shelf life. The company’s commitment to circular packaging systems makes it a leader in developing sustainable pouch alternatives.

Sonoco Products Company: Providing Versatile Pouch and Cold Chain Solutions

Sonoco manufactures pouches for food, healthcare, and industrial markets, combining its expertise in flexible packaging with temperature-assured cold chain solutions. In July 2025, Sonoco invested $30 million to expand adhesives and sealants capacity, reinforcing its pouch production infrastructure. Its ISC Labs® testing services provide regulatory compliance and tailored pouch validation for customers.

ProAmpac: Strengthening E-Commerce and High-Performance Pouch Portfolio

ProAmpac offers a wide range of stand-up, retort, and spouted pouches, with strong capabilities in printing and material science. In August 2025, it acquired PAC Worldwide, enhancing its role in e-commerce packaging. Its ProActive Recyclable and Compostable lines deliver sustainable alternatives, while its CRREO child-resistant pouches serve regulated sectors such as pharmaceuticals and cannabis.

Pouches Market Share Insights

Stand-Up Pouches Dominate Market Share by Product Type in the Global Pouches Industry

Stand-up pouches (SUPs) account for half of the pouch packaging market, making them the most widely adopted format across consumer and industrial applications. Their dominance is rooted in their dual functionality: acting as both a protective barrier and a self-standing retail display unit, effectively replacing rigid formats like jars or tubs. SUPs are widely favored in food, beverage, and personal care sectors because they combine strong visual impact with consumer convenience features such as resealable zippers, tear notches, and spouts. Beyond aesthetics, they provide superior logistics efficiency by reducing packaging weight and transportation costs. With sustainability pressure intensifying, innovation is centered on recyclable and mono-material SUPs, ensuring they maintain leadership even as regulatory landscapes tighten around multi-material flexible packaging.

Food and Beverages Hold the Largest Market Share by End-Use in the Pouch Packaging Market

The food and beverages sector is the overwhelming driver of pouch packaging, representing nearly 70% of total demand in 2025. This dominance reflects the segment’s unique need for convenience-driven formats, portion control, and extended shelf life for products ranging from snacks and frozen foods to dairy alternatives and ready-to-drink beverages. Stand-up and retort pouches in particular provide lightweight protection while maximizing branding real estate on crowded retail shelves, making them indispensable in a highly competitive category. The sector’s scale also makes it the proving ground for sustainable pouch innovations, such as recyclable mono-material laminates and compostable films. With consumer demand for on-the-go formats and e-commerce-ready packaging rising sharply, the F&B industry will continue to set the pace for pouch market expansion and technological development.

United States: Rising Demand for Convenient and Sustainable Pouches in Food, Beverage, and Personal Care

The U.S. pouches market is experiencing strong growth due to a surge in demand for convenient, on-the-go products, particularly in the food and beverage and personal care sectors. Consumers increasingly prefer single-serve and portable formats, driving innovation in flexible packaging solutions. Companies are investing in high-speed, multi-lane packaging machinery, especially for stick packs and stand-up pouches, enabling faster production and cost efficiencies for high-volume consumer goods.

Sustainability is a core focus, with manufacturers adopting recyclable, mono-material, and paper-based pouch solutions to meet growing brand commitments toward eco-friendly packaging. Corporations like SC Johnson are introducing refillable pouches for concentrated household cleaners, reflecting the shift toward sustainable and reusable packaging formats. The proliferation of e-commerce further boosts demand for lightweight, durable pouches that minimize shipping costs and product damage. Regulatory developments, including state-level Extended Producer Responsibility (EPR) statutes, compel brands to rethink packaging design and end-of-life strategies, reinforcing the adoption of eco-conscious pouch solutions.

Germany: Circular Economy and Advanced Pouch Technologies Driving Market Innovation

The German pouches market is shaped by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which promotes eco-friendly and fully recyclable packaging solutions. Germany’s leadership in the circular economy emphasizes packaging designed for recyclability and the use of high recycled-content materials to meet national and EU sustainability targets.

Technological innovation is a key driver. For instance, SIG’s alu-layer-free full barrier aseptic carton, adopted by Berglandmilch, demonstrates advanced barrier technology that can be extended to pouch applications, improving shelf life and product safety. Investments in high-speed, high-precision filling and sealing equipment specifically designed for pouches enhance production efficiency and product quality. Government mandates under the PPWR, which require all packaging to be fully recyclable by 2030, are pushing companies to integrate reuse and refill targets, creating strong momentum for sustainable and technologically advanced pouch solutions.

China: Policy-Driven Sustainability and Flexible Pouch Manufacturing Fuel Growth

China’s pouches market is evolving rapidly, driven by government policies promoting eco-friendly and reusable materials as part of the country’s dual carbon goal for carbon peak and neutrality. This is reshaping pouch design and production, especially for food, beverage, and personal care products.

Manufacturers are investing in automation, AI, and 5G-enabled industrial internet technologies, improving production efficiency and flexible manufacturing capabilities. Sustainability-focused regulations restricting non-degradable plastics in express delivery are fueling demand for paper-based and recyclable pouches. The rise of domestic e-commerce platforms is increasing demand for secure, lightweight, and tamper-proof packaging. Market innovations include collaborations between Mespack and Fuji Seal to replace plastic bottles with pre-made spouted pouches, reflecting a shift toward flexible, high-performance packaging solutions. China’s “Made in China 2025” initiative further accelerates adoption of high-tech packaging solutions, aiming for 70% domestic content in core materials by 2025.

India: Eco-Friendly and High-Barrier Pouches Driving Growth in Food and Beverages

India’s pouches market is supported by government initiatives like Make in India and Zero Effect Zero Defect, fostering high-quality domestic production and strengthening infrastructure for flexible packaging. The Production Linked Incentive (PLI) Scheme for the food processing sector, with an outlay of INR 10,900 crore, enhances manufacturing capabilities, driving demand for standardized, high-quality pouch solutions.

Regulatory measures, including the Plastic Waste Management (Amendment) Rules, are encouraging a shift toward laminated and paper-based pouches, aligning with sustainability goals. Rising disposable incomes and urbanization are fueling demand for convenient, single-serve, and on-the-go products like instant coffee, snacks, and spices. Additionally, there is a notable increase in the use of high-barrier films to maintain product freshness and extend shelf life, particularly in the food and beverage industry, making India a rapidly expanding market for eco-friendly and technologically advanced pouches.

Pouches Market Report Scope

Pouches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$47.7 Billion

|

|

Market Size (2034)

|

$75.9 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material Type (Plastics, Paper, Aluminum, Bioplastics), By Product Type (Stand-up Pouches, Flat Pouches, Retort Pouches, Aseptic Pouches, Other Pouches), By Closure Type (Spout, Zipper, Tear Notch, Other Closures), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Homecare & Household, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Berry Global Inc., Sonoco Products Company, Huhtamaki Oyj, Constantia Flexibles, Sealed Air Corporation, AptarGroup, Inc., Goglio S.p.A., ProAmpac LLC, Gualapack S.p.A., Coveris Holdings S.A., Glenroy, Inc., Uflex Ltd., Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pouches Market Segmentation

By Material Type

- Plastics

- Paper

- Aluminum

- Bioplastics

By Product Type

- Stand-up Pouches

- Flat Pouches

- Retort Pouches

- Aseptic Pouches

- Other Pouches

By Closure Type

- Spout

- Zipper

- Tear Notch

- Other Closures

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Homecare & Household

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pouches Market

- Amcor plc

- Mondi Group

- Berry Global Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- Constantia Flexibles

- Sealed Air Corporation

- AptarGroup, Inc.

- Goglio S.p.A.

- ProAmpac LLC

- Gualapack S.p.A.

- Coveris Holdings S.A.

- Glenroy, Inc.

- Uflex Ltd.

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics has conducted a comprehensive, multi-layered analysis of the global Pouches Market, integrating both primary and secondary research to deliver actionable insights for industry professionals. Our methodology combines interviews with packaging manufacturers, FMCG and pharmaceutical stakeholders, and sustainability experts, alongside an in-depth review of corporate reports, mergers and acquisitions, government regulations, and technological advancements. Market sizing and growth forecasts are derived from historical trends, innovations in recyclable mono-material structures, high-barrier films, HPP-compatible pouches, and the rising adoption of bio-based and marine-degradable materials. Segmentation spans material type, product format, closure type, and end-use industry, with regional insights covering key markets including the U.S., Germany, China, and India. Competitive intelligence evaluates leading players such as Amcor, Constantia Flexibles, Mondi, and Sonoco, highlighting strategic investments, sustainability commitments, and product innovations. By synthesizing regulatory frameworks, consumer trends, and technological drivers, USDAnalytics provides a precise and actionable overview of the evolving pouches market for professional decision-makers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.