Market Overview: Growing Role of Flat Pouches in Global Packaging

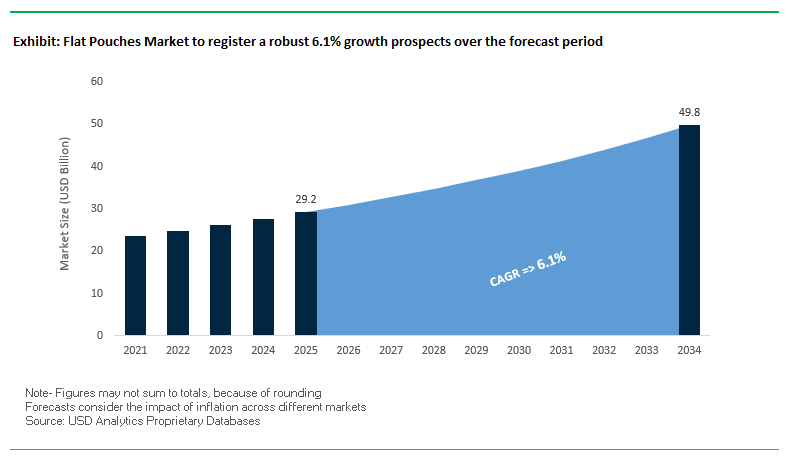

The Flat Pouches Market is projected to reach USD 29.2 billion in 2025 and expand to USD 49.8 billion by 2034, advancing at a steady CAGR of 6.1%. The market is thriving as industries seek lightweight, cost-efficient, and high-barrier packaging formats that deliver both convenience and sustainability. For professionals, the pressing questions revolve around how flat pouches can meet the demands of e-commerce, sustainability mandates, and sensitive product protection while offering scalability across industries.

Flat pouches stand out for their versatility, barrier properties, and branding potential, serving applications ranging from single-serve snacks to pharmaceutical unit doses and industrial chemicals. The rise of e-commerce logistics has further boosted demand, as their lightweight design reduces shipping costs and enhances product protection during transit. Moreover, multi-layer laminated pouches continue to dominate due to their superior protection against oxygen, moisture, and light—critical for extending product shelf life.

The pharmaceutical industry represents a key growth avenue, with flat pouches emerging as tamper-evident and contamination-resistant packaging formats that improve dosage safety. Meanwhile, the sustainability push is steering companies toward recyclable, compostable, and mono-material pouches, aligning with regulatory pressure to reduce plastic waste.

Key Insights for Industry Professionals:

- Market expected to grow from USD 29.2B (2025) to USD 49.8B (2034) at 6.1% CAGR.

- E-commerce shipments are driving demand for lightweight and durable flat pouches.

- Pharmaceutical packaging is expanding with unit-dose and tamper-evident pouch formats.

- Multi-layer laminated pouches dominate due to barrier performance and versatility.

- Sustainability focus is accelerating adoption of recyclable, biodegradable, and mono-material formats.

Market Analysis: Recent Developments Driving Flat Pouch Adoption

The global flat pouches industry is witnessing rapid transformation led by sustainability commitments, mergers of packaging giants, and adoption of smart technologies. In August 2025, a market report emphasized the growing integration of smart packaging technologies—including QR codes, NFC, and RFID tracking—into flat pouches. These features allow brands to deliver real-time verification, interactive consumer experiences, and robust supply chain traceability.

In July 2025, two major consolidations reshaped the packaging industry. The all-stock merger between Amcor and Berry Global established a new leader in flexible and rigid packaging innovation, with a strong focus on sustainability. During the same month, Smurfit Kappa and WestRock completed their merger, creating Smurfit WestRock, a dominant force in paper-based packaging that is expected to influence fiber alternatives within flat pouch applications.

Earlier in June 2025, a pharmaceutical sector report highlighted increasing adoption of flat pouches for single-dose medications, underlining their contamination resistance and patient safety benefits. In May 2025, a distributor launched 100% recyclable pouches designed for e-commerce logistics, showcasing how sustainability demands and online retail growth are converging.

Other key developments reflect industry diversification. In April 2025, the aerospace sector reported a rise in reusable ESD containers to safeguard high-value components, while in March 2025, a conductive polymer manufacturer partnered with an electronics firm to advance antistatic trays and carriers. Meanwhile, Sealed Air’s February 2025 partnership with a retail chain aimed at increasing recycled content in shipping pouches underscored the industry’s pivot toward circular economy models.

Transformative Trends and Strategic Opportunities Shaping the Global Flat Pouches Market

Accelerated Regulatory-Driven Shift to Mono-Material and Recyclable Structures

The flat pouches market is witnessing a rapid transformation as regulatory mandates, including Extended Producer Responsibility (EPR) regulations and plastic taxes, compel brands to transition from traditional multi-material laminates to mono-material polyolefin structures. These pouches, primarily made from polyethylene and polypropylene, are engineered to be fully recyclable while maintaining essential barrier properties for food and beverage protection. Multi-layer packaging has long posed recycling challenges due to the difficulty of separating different materials. With the EU Packaging and Packaging Waste Regulation (PPWR) enforcing recyclability and India’s Plastic Waste Management Rules, 2024 introducing mandatory EPR compliance, brands are incentivized to adopt recyclable pouches rapidly. Leading companies are taking action: Unilever aims for all plastic packaging to be reusable, recyclable, or compostable by 2035, emphasizing mono-material solutions, while Nestlé actively collaborates with the UK Flexible Plastic Fund to enhance flexible plastic recycling. This regulatory-driven trend opens a significant growth avenue for material suppliers and packaging manufacturers, particularly in the food and beverage sector, as compliance with sustainability standards becomes a key differentiator. The shift is also reshaping the flat pouches value chain, promoting collaboration between brands, material suppliers, and recyclers while driving investment in R&D and machinery for high-performance mono-material pouches.

Integration of Digital Printing for Mass Customization and Agile Supply Chains

The rise of direct-to-consumer (D2C) brands, limited-edition runs, and region-specific marketing is accelerating the adoption of digital printing on flat pouches. This technology eliminates the need for traditional printing plates, reduces setup times, and enables short-run, high-graphics customization for agile supply chains. Digital printing is particularly advantageous for product lines with multiple SKUs or seasonal variations, allowing brands to economically test new designs without incurring high fixed costs. Companies like Huhtamaki utilize the HP Indigo 20000 wide-web digital press to offer variable data printing, personalized QR codes, and unique design freedom, enabling rapid product launches and heightened customer engagement. The integration of digital printing provides a major growth avenue, particularly for smaller brands needing just-in-time production capabilities. It also reduces waste from obsolete pre-printed inventory and allows flat pouch manufacturers to act as strategic partners to brands, fostering a dynamic, collaborative, and data-driven packaging ecosystem.

Development of High-Barrier, Compostable Polymer Films

There is a critical growth opportunity for high-performance, compostable films capable of providing robust barrier properties for sensitive applications, including coffee, pet food, and packaged foods. These films must comply with ASTM/EN compostability standards while remaining cost-competitive with existing materials. Traditional multi-layer pouches, containing diverse polymers, are incompatible with recycling and composting, highlighting the need for alternative solutions. Companies such as TIPA are leading innovation, offering home- or industrially-compostable films that protect against oxygen, moisture, and UV light while biodegrading naturally within months. Academic research has further demonstrated bacterial cellulose films with modified surfaces achieving 84% reduced water vapor permeability and complete biodegradability in soil within a month. Commercializing these films represents a significant opportunity for the flat pouches market, aligning with consumer demand for sustainable, plastic-free packaging and enabling brands to meet ambitious environmental goals.

Implementation of Digital Watermarking for Accurate Post-Consumer Sorting

The incorporation of digital watermarking technologies, exemplified by the HolyGrail 2.0 initiative, is transforming the recyclability of flat pouches by enabling high-speed, accurate sorting at Material Recovery Facilities (MRFs). Flexible plastics are notoriously difficult to recycle due to tangling in sorting machinery and low weight, but digital watermarks provide a unique ID for each package, dramatically improving material purity and recycling rates. The initiative, involving over 130 global organizations, achieved 99% detection and 93% purity in industrial trials, highlighting its real-world efficacy. Deploying digital watermarking creates a high-value growth avenue, enabling manufacturers to support brands in achieving recycling targets, comply with evolving EU regulations, and reduce landfill waste. Additionally, it fosters a more interconnected, data-driven value chain, requiring collaboration among flat pouch manufacturers, technology providers, and waste management companies, ultimately creating scalable, sustainable solutions for flexible packaging.

Competitive Landscape: Leading Companies in Flat Pouches Market

The flat pouches industry is shaped by global packaging leaders and niche innovators that combine sustainable material science, flexible production, and brand-focused design. Companies are increasingly focusing on recyclable solutions, high-barrier laminates, and smart packaging technologies to remain competitive.

Amcor plc drives smart and sustainable pouch innovation

Amcor remains a global leader in responsible packaging, leveraging its vast network and R&D strength. Its portfolio includes recycle-ready flat pouches for consumer goods and healthcare, including tamper-evident pre-made medical pouches. Amcor is pioneering smart packaging integration with NFC tags and QR codes, boosting consumer engagement and supply chain visibility. With a clear 2025 sustainability goal of 100% recyclable or reusable packaging, Amcor is positioning itself as a frontrunner in circular economy-driven pouch solutions.

Huhtamaki Oyj invests in circular food packaging

Huhtamaki is a global specialist in food and foodservice packaging, with strong expertise in fiber and flexible materials. In July 2025, it introduced a recyclable and compostable packaging solution for the ice cream sector, strengthening its position in sustainable packaging. Through its blueloop™ brand, Huhtamaki is scaling flexible packaging innovations designed for circularity. Its global presence, combined with investments in efficiency programs, reinforces its influence in eco-conscious flat pouch solutions.

Sonoco Products Company enhances precision and flexibility

Sonoco offers a wide portfolio of packaging, including multi-layer film flat pouches enhanced with high-quality flexographic and rotogravure printing. The company is actively investing in laser scoring and precision die-cutting technologies to deliver advanced convenience features. Guided by its purpose, “Better Packaging. Better Life,” Sonoco continues to emphasize innovation and sustainability, providing durable, consumer-friendly pouch formats that balance performance and recyclability.

ProAmpac develops mono-material recyclable pouches

ProAmpac, recognized for its QUADFLEX® pouches and custom-engineered flexible packaging, is innovating with its ProActive Sustainability® platform. The company’s patented mono-material polyethylene pouch is pre-qualified for in-store drop-off recycling, combining durability with a recyclable structure. By offering drop-in replacements for conventional laminates, ProAmpac helps clients transition toward sustainability without compromising productivity or shelf appeal, reinforcing its role as a leading flexible packaging innovator.

Flat Pouches Market Share Insights

Stand-Up Pouches Lead Market Share by Packaging Type in the Flat Pouches Industry

Stand-up pouches command 40% of the flat pouches industry, representing the most premium and consumer-preferred packaging format. Their ability to stand upright provides superior shelf visibility and extensive branding real estate, which is critical in highly competitive FMCG categories. The integration of resealable zippers, spouts, and high-barrier laminates enhances functionality, ensuring product freshness and consumer convenience while replacing rigid packaging in multiple sectors. This shift reflects broader industry trends toward lightweighting and sustainability, as stand-up pouches require significantly less material and energy in production and transport. Their continued adoption across food, beverages, personal care, and household products ensures that they remain the anchor format in flat pouch packaging.

Food & Beverages Dominate Market Share by End-Use in the Flat Pouches Industry

The food and beverages sector holds 70% of demand in the flat pouches industry, underscoring its role as the primary driver of innovation and volume. Pouches deliver lightweighting, extended shelf life, and vibrant printing that align perfectly with modern consumer demands for convenience, on-the-go formats, and sustainability. From pet food and coffee to sauces and ready-to-drink beverages, the sector leverages pouches to achieve cost efficiencies while maintaining strong branding impact. Importantly, the rise of e-commerce grocery sales and demand for portion-controlled packaging continue to accelerate pouch adoption. The overwhelming dominance of this sector reflects both scale and innovation, making food and beverages the cornerstone of the flat pouches market.

United States Flat Pouches Market Accelerated by Sustainability Initiatives and E-Commerce Growth

The U.S. flat pouches market is being reshaped by a combination of federal and state-level regulations, particularly Extended Producer Responsibility (EPR) laws, with Maryland being the most recent adopter in 2025. These regulations shift the financial burden of recycling from taxpayers to producers, encouraging the development of recyclable and material-efficient pouches, including mono-material formats that reduce multi-layer complexity. Technological innovations, such as smart packaging with integrated QR codes and NFC chips, are enhancing supply chain traceability and consumer engagement through product information and augmented reality experiences.

Corporate investments are driving market expansion, exemplified by Sonoco Products Co.’s $30 million facility expansion in August 2025, targeting sustainable adhesive packaging with a focus on flexible formats. Key applications are concentrated in e-commerce, direct-to-consumer (DTC), and food & beverage sectors, where durable, lightweight pouches ensure product integrity during shipping. Sustainability remains a strategic imperative, with bio-based films and recyclable materials being prioritized to meet growing consumer demand for eco-friendly packaging options.

Germany Flat Pouches Market Driven by Regulatory Compliance and Circular Economy Leadership

Germany’s flat pouches market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) enforced in February 2025, which mandates full recyclability or reusability by 2030. The national Packaging Act (VerpackG) further enforces high material-specific recycling rates, prompting a transition from multi-layer laminates to mono-material pouches. Germany’s Extended Producer Responsibility (EPR) system encourages innovation in recycling and sorting, fostering the development of durable and reusable packaging solutions.

Technological innovations are advancing rapidly, with digital product passports and watermarks improving material transparency and recycling efficiency. The market’s key applications are in retail and food service, where consumer demand for high-quality, sustainable pouches with high-barrier films drives adoption. Strategic partnerships between film producers and brand owners are facilitating the creation of high-performance, eco-friendly converted flexible packaging solutions, while mandatory reuse rates under the PPWR are pushing the industry to develop durable and reusable transport containers.

China Flat Pouches Market Expanding Through Governmental Green Initiatives and Domestic Manufacturing

China’s flat pouches market is benefiting from governmental policies targeting sustainability, including the 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement,” which encourages the adoption of recyclable materials. Regulatory reforms effective September 2023 set limits on packaging layers and void ratios, influencing e-commerce and consumer goods packaging channels.

Technological advancements such as AI and 5G-enabled industrial internet platforms are optimizing production efficiency and enhancing flexible manufacturing capacities. A key trend is domestic substitution of imported technology, with local companies expanding production to meet growing demand for high-quality, circular packaging. The rapid expansion of e-commerce, food and beverage delivery, and quick-service restaurant industries is driving demand for flat pouches, positioning China as a rapidly growing market for sustainable packaging solutions.

Japan Flat Pouches Market Innovating Through High-Performance Films and Sustainable Technologies

Japan’s flat pouches industry is at the forefront of precision manufacturing and sustainable packaging, demonstrated by Nippon Molding’s installation of the PulPac Modula dry-molded fiber machine in September 2025, which significantly reduces water and energy usage. Regulatory guidance under the Plastic Resource Circulation Act, effective April 2022, is promoting environmentally conscious design and reducing single-use plastics.

The market is seeing a shift toward specialty and value-added films with superior barrier properties, IoT integration for real-time monitoring, and digital printing for enhanced functionality. Consumer-focused innovations, such as easy-open tear notches and resealable closures, are addressing the needs of an aging population and single-person households. Cross-industry collaborations, like LyondellBasell’s partial incorporation of bio-based PP into Shiseido’s cosmetic packaging, illustrate the market’s strong emphasis on sustainability and multifunctional packaging solutions.

Brazil Flat Pouches Market Accelerating with Regulatory Push and Sustainable Packaging Innovations

Brazil’s flat pouches industry is being influenced by the National Solid Waste Policy and recent regulations aimed at banning single-use disposable items, with a 2030 deadline for all packaging to be returnable, recyclable, or compostable. These regulations are driving significant innovation and adoption of sustainable packaging solutions.

Technological advancements, including robotics, AI, and biodegradable films developed from sugarcane bagasse (CMC), are enhancing production efficiency and product quality. Corporate investments, such as Wheaton’s new interactive design facility in São Paulo (May 2024), are focusing on sustainable packaging solutions for food, beverage, and cosmetics sectors. The industry is witnessing a growing shift toward paper-based pouches with bio-based coatings, aligning with Brazil’s sustainability goals, and the expanding food processing sector is boosting demand for technologically advanced and environmentally responsible flat pouch solutions.

Flat Pouches Market Report Scope

Flat Pouches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.2 Billion

|

|

Market Size (2034)

|

$49.8 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Packaging Type (Three-Side Seal Pouches, Four-Side Seal Pouches, Pillow Pouches, Other), By Material Type (Plastic, Paper, Aluminum, Bioplastic, Other Materials), By End-Use Industry (Food & Beverages, Pharmaceuticals, Consumer Goods, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, International Paper Company, DS Smith plc, WestRock Company, Sonoco Products Company, Sealed Air Corporation, Crown Holdings Inc., Ardagh Group, Ball Corporation, Billerud AB, Graphic Packaging Holding Company, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flat Pouches Market Segmentation

By Packaging Type

- Three-Side Seal Pouches

- Four-Side Seal Pouches

- Pillow Pouches

- Others

By Material Type

- Plastic

- Paper

- Aluminum

- Bioplastic

- Other Materials

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Consumer Goods

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flat Pouches Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- International Paper Company

- DS Smith plc

- WestRock Company

- Sonoco Products Company

- Sealed Air Corporation

- Crown Holdings Inc.

- Ardagh Group

- Ball Corporation

- Billerud AB

- Graphic Packaging Holding Company

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics adopted a comprehensive and data-driven methodology to provide an in-depth analysis of the Global Flat Pouches Market. Our approach combined extensive primary research, including interviews with packaging manufacturers, supply chain experts, and sustainability consultants, with secondary research from corporate reports, regulatory filings, trade publications, and industry journals. Quantitative modeling was applied to forecast market growth by packaging type, material, and end-use industry, while qualitative insights explored emerging trends such as mono-material recyclable structures, high-barrier compostable films, digital printing for mass customization, and digital watermarking for post-consumer sorting. Regional dynamics across the U.S., Germany, China, Japan, and Brazil were analyzed, taking into account regulatory frameworks like Extended Producer Responsibility (EPR), the EU Packaging and Packaging Waste Regulation, and national sustainability initiatives. USDAnalytics also assessed technological innovations, corporate mergers, and strategic partnerships shaping the market, ensuring that industry professionals gain actionable intelligence for strategic planning, product development, and operational optimization in the evolving flat pouches landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.