Market Overview: Growth Drivers in Converted Flexible Packaging

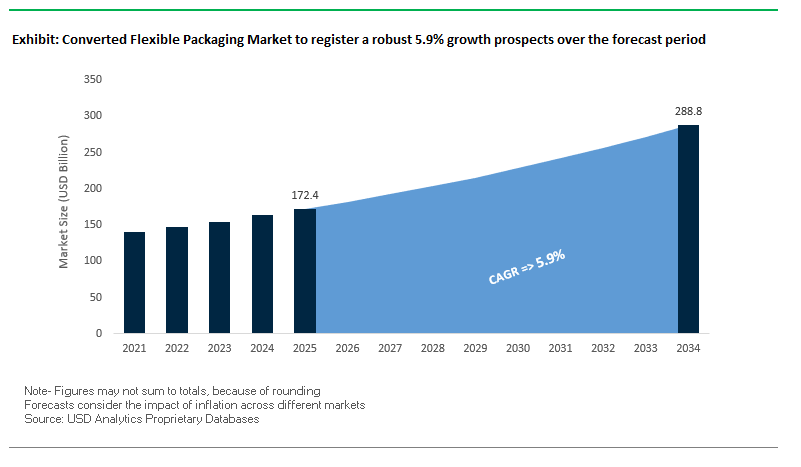

The Global Converted Flexible Packaging Market is valued at USD 172.4 billion in 2025 and is projected to reach USD 288.8 billion by 2034, expanding at a healthy CAGR of 5.9%. This market plays a critical role in the global consumer goods economy, offering lightweight, customizable, and cost-efficient packaging formats such as pouches, wraps, and bags. It serves as a key enabler of shelf-life extension, food safety, and supply chain efficiency, making it indispensable for the food, beverage, healthcare, and e-commerce industries.

A defining trend in the sector is the shift to mono-material packaging, with leading companies developing recyclable polyethylene (PE) and polypropylene (PP) films that align with circular economy goals. At the same time, high-barrier films for food and beverage remain essential, protecting products against oxygen, light, and moisture to reduce food waste. The rise of e-commerce has created strong demand for resealable pouches and stand-up bags designed for on-the-go consumption and improved product portability. Moreover, significant R&D investments are being directed into bio-based and compostable flexible packaging, aiming to deliver scalable, sustainable alternatives that balance performance and cost-effectiveness.

Key Insights for Industry Professionals:

- Mono-material structures gain momentum to enable recycling.

- High-barrier films dominate in food and beverage to reduce spoilage.

- E-commerce growth fuels demand for resealable, portable packaging.

- Bio-based and compostable packaging is a key R&D priority.

Market Analysis: Recent Developments in the Converted Flexible Packaging Industry

The converted flexible packaging industry is undergoing rapid consolidation, innovation, and sustainability-driven transformation. In August 2025, Constantia Flexibles expanded its Ecolutions portfolio at FACHPACK 2025, unveiling recyclable mono-material packaging and a mono-PP spouted pouch tailored for circular economy models. The same month, Mondi completed its acquisition of Schumacher Packaging’s Western Europe assets, strengthening its European footprint and delivering future synergy benefits.

In July 2025, Sealed Air reported Q2 performance updates, emphasizing a turnaround strategy for its protective packaging division and a pivot to becoming more substrate agnostic, moving away from plastics-only approaches. Also in July, ProAmpac published its Sustainability Impact Report 2025, showcasing its progress toward climate goals and reiterating its pledge that 100% of its product portfolio will have sustainable attributes.

In June 2025, Constantia announced a €100 million global production upgrade, focused on expanding aluminum foil capacity and adding new lacquering and digital printing lines. This follows May 2025, when Amcor posted strong Q4 results, building momentum after its April 2025 all-stock merger with Berry Global, a move that created a new leader in consumer packaging and dispensing solutions. Earlier in February 2025, ProAmpac presented new recyclable films at Packaging Innovations 2025, including its Fiberization of Packaging® technology and ProActive Recyclable R-2000 series.

Emerging Trends and Strategic Opportunities Driving the Converted Flexible Packaging Market

Strategic Integration of Post-Consumer Recycled (PCR) Content

A dominant trend in the converted flexible packaging market is the strategic incorporation of post-consumer recycled (PCR) content. Major brands such as Coca-Cola, Nestlé, and Unilever are setting ambitious sustainability targets, compelling converters to source and integrate high-quality PCR materials into flexible packaging. Regulatory frameworks, including the EU Plastics Strategy, mandate minimum recycled content, driving demand across the entire value chain. Partnerships between resin suppliers, converters, and recyclers are critical to secure a reliable PCR supply. For example, a leading petrochemical company successfully integrated 30% PCR into flexible film for household cleaning products without compromising performance. This trend is reshaping the supply chain by creating a need for advanced recycling technologies, new PCR sourcing strategies, and enhanced collaboration among stakeholders, reinforcing the circular economy model in flexible packaging.

Advanced Automation and Smart Packaging for Supply Chain Efficiency

Flexible packaging converters are increasingly deploying smart packaging technologies, including digital watermarking, RFID, and NFC tags, to enable end-to-end supply chain traceability, anti-counterfeiting, and advanced sorting at end-of-life. The complexity of modern supply chains, particularly in e-commerce, requires real-time product tracking to enhance inventory management and reduce counterfeit risks. Companies are investing in AI-driven automation, enabling precise cutting and forming of packaging to fit products perfectly, which reduces material waste and lowers shipping costs. Smart packaging also offers brands a direct channel to engage consumers by providing information on product origin, ingredients, and sustainability efforts through simple QR code or NFC scans. This trend is creating a high-value segment within the converted flexible packaging market, driving demand for integrated technology solutions and collaborative innovation with tech providers.

Development of Mono-Material Polyethylene (PE) Packaging Structures

There is a substantial growth opportunity in mono-material PE packaging for flexible packaging converters. Multi-layer laminates are challenging to recycle, creating demand for single-polymer solutions that align with existing drop-off recycling streams. Companies like Mondi have pioneered mono-material barrier pouches, certified by leading industry bodies, which maintain barrier performance while ensuring recyclability. Advanced coatings and thin-film technologies are being developed to enhance oxygen, moisture, and light protection in mono-material designs. As global regulatory requirements tighten and consumer demand for sustainable packaging grows, high-performance mono-material PE packaging represents a prime market opportunity for converters capable of delivering both eco-friendly and aesthetically appealing solutions.

Expansion of Packaging-Light, Performance-Engineered Formats

The push for lightweight, high-strength flexible packaging represents a significant opportunity to reduce material usage, shipping costs, and carbon emissions. Transportation costs and Scope 3 GHG reduction goals are motivating brands to adopt performance-engineered films and structures that minimize packaging weight while maintaining protection. Studies on supply chain efficiency show that even minor improvements in packaging design can yield substantial reductions in logistics costs and environmental impact. The rise of e-commerce further drives demand for packaging-light formats, where protective, lightweight materials reduce both shipping expenses and the environmental footprint. Flexible packaging converters are increasingly acting as strategic partners, collaborating with brands to optimize packaging design, enhance supply chain efficiency, and meet sustainability targets, thereby transforming their role from simple suppliers to value-added consultants in the global converted flexible packaging ecosystem.

Competitive Landscape: Key Players in Converted Flexible Packaging

The converted flexible packaging industry is led by global multinationals and innovative mid-sized players with strong commitments to recyclability, circularity, and performance innovation.

Amcor plc strengthens global leadership post-Berry Global acquisition

Amcor has emerged as a global leader following its 2025 merger with Berry Global. Its strategy centers on leveraging enhanced material science capabilities and scale to deliver sustainable mono-material films and high-barrier flexible solutions. Amcor’s portfolio spans food, healthcare, and personal care applications, including sterile and recyclable formats. Its Q4 2025 results showed 3% volume growth, underscoring successful integration and synergy realization.

Mondi plc expands European footprint with Schumacher acquisition

Mondi is driving its MAP2030 Action Plan, focused on making all packaging reusable, recyclable, or compostable by 2025. In 2025, it completed the acquisition of Schumacher Packaging’s assets, reinforcing its European market leadership. Mondi’s FunctionalBarrier Papers and stand-up pouches serve as fiber-based alternatives to plastics, targeting food and FMCG sectors. Its strength lies in its dual portfolio of paper and flexible plastics, enabling holistic sustainable design choices for customers.

Sealed Air Corporation pivots to substrate-agnostic strategies

Sealed Air, known for Cryovac® food packaging and Bubble Wrap® protective solutions, is undergoing a strategic pivot. Its 2025 updates emphasized becoming substrate agnostic, expanding beyond plastics into fiber-based solutions. Its protective packaging segment is being reshaped to serve e-commerce and fresh food markets with cost-optimized, sustainable alternatives. Ongoing optimization is stabilizing performance, ensuring its long-term competitive edge.

Constantia Flexibles enhances portfolio with Ecolutions innovation

Constantia Flexibles has positioned itself at the forefront of sustainable flexible packaging. Its Ecolutions portfolio, including recyclable mono-materials and mono-PP pouches, highlights its focus on future-ready packaging. The acquisition of Aluflexpack in 2025 expanded its reach in food and pharmaceutical segments. With over €100 million invested in digital printing and foil upgrades, Constantia is building a more agile and sustainable global network.

ProAmpac advances fiberization and recyclable packaging innovation

ProAmpac has distinguished itself with its ProActive Sustainability® framework, offering recyclable films, compostable pouches, and fiber-based alternatives. Its 2025 Sustainability Report formalized its SBTi net-zero commitment, highlighting accountability. At Packaging Innovations 2025, ProAmpac showcased Fiberization of Packaging® and the R-2000 film series, solutions that combine recyclability with strong barrier performance. Its customer base spans food, pet care, and personal care, emphasizing shelf appeal alongside sustainability.

Converted Flexible Packaging Market Share Insights

Pouches Dominate Market Share by Packaging Format in Converted Flexible Packaging

Pouches represent the largest share of the converted flexible packaging industry, capturing approximately 40% of the market by 2025. Their rise is anchored in versatility, premium shelf presence, and strong sustainability potential. Stand-up pouches (SUPs) lead the charge, combining resealability, spouts, and superior printability with lightweight material efficiency. Importantly, pouches are the front line of sustainability-driven innovation, with brand owners and converters investing heavily in mono-material polyethylene (PE) and polypropylene (PP) pouches that meet recyclability mandates under Extended Producer Responsibility (EPR) frameworks in Europe and similar plastic packaging reduction laws in North America and Asia-Pacific. Their widespread use across coffee, pet food, premium snacks, and even homecare detergents reflects how this format has become the nexus of functionality, branding, and circular packaging innovation.

Food & Beverages Anchor Market Share by End-Use Industry in Converted Flexible Packaging

Food & beverages account for nearly 60% of all converted flexible packaging consumption, underscoring their position as the undisputed anchor segment. This dominance is a function of both scale and necessity: converted flexible packaging delivers the advanced barrier properties required to extend shelf life, reduce food waste, and preserve flavor integrity across diverse categories such as dairy, meat, snacks, beverages, and ready meals. At the same time, the sector is the crucible for sustainability breakthroughs, as regulators and retailers impose aggressive recycled content and recyclability targets. Features such as zippers, laser scoring for easy opening, and microwavability illustrate how food applications also lead in convenience-driven innovation. As e-commerce grocery expands globally, food packaging’s demand for lightweight yet durable formats further cements its majority market position.

United States Converted Flexible Packaging Market Driven by EPR Regulations and Sustainable Mono-Materials

The United States converted flexible packaging market is being reshaped by a patchwork of state-level regulations, with Extended Producer Responsibility (EPR) bills accelerating the shift toward recyclable, compostable, and mono-material solutions. Flexible packaging producers are innovating with recyclable mono-materials compatible with real-world recovery systems while leveraging digital printing technologies to create short-run, high-quality graphics that embed QR codes for traceability and loyalty programs. Strategic investments in sustainable materials and advanced machinery are enabling the production of high-demand pouches and bags, which dominate market volume.

Demand is particularly strong in the food and beverage, personal care, and e-commerce sectors, driven by on-the-go consumption and omnichannel distribution. Sustainability initiatives focus on light-weighting strategies that reduce logistics costs and Scope 3 emissions. Value-added features such as resealability, high-quality graphics, and eco-friendly materials are commanding higher pricing, while new applications in household products, pet food, and consumer durables are expanding market opportunities. These factors position the U.S. as a leader in sustainable, high-performance converted flexible packaging solutions.

Germany Converted Flexible Packaging Market Accelerating Through Circular Economy Leadership and Innovation

Germany’s converted flexible packaging market is governed by stringent regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating full recyclability or reuse by 2030. The country’s well-established Extended Producer Responsibility (EPR) system drives recycling and sorting innovation, with new recyclability standards coming into effect in 2026. Companies like Amcor are leading with single-material, lightweight, tamper-evident closures, aligning with both regulatory demands and consumer expectations.

The market is particularly strong in food and beverage and retail sectors, driven by demand for high-performance, aesthetically appealing packaging. Collaborative R&D initiatives between brand owners and film producers are focusing on lighter, stronger, and more sustainable packaging solutions, including digital product passports and watermarks to improve transparency and recyclability. Amcor’s CleanStream technology demonstrates the integration of domestically recovered, mechanically recycled polypropylene (PP), alongside reusable cups and lids, highlighting Germany’s focus on circular, sustainable, and functional converted flexible packaging solutions.

China Converted Flexible Packaging Market Expanding Through Green Transformation and Domestic Innovation

China’s converted flexible packaging market is being propelled by governmental “dual carbon” goals and the 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement. Regulatory reforms targeting excessive packaging, including limits on layers, void ratios, and packaging costs, are driving compliance in food and cosmetics sectors. Express delivery companies are also required to prioritize eco-friendly, reusable, and reduced packaging solutions.

Technological advancements are significant, with automation, AI, and the integration of “5G plus industrial internet” optimizing production efficiency and flexible manufacturing. Domestic substitution of imported technology is a key trend, with local companies expanding capacity to meet rising demand for high-quality, circular packaging. Rapid growth in e-commerce, fresh food, and food delivery industries continues to fuel the market, while China’s high volume of patents and R&D initiatives position the country as a global hub for innovation in converted flexible packaging materials and production methods.

India Converted Flexible Packaging Market Strengthening Through Government Initiatives and Infrastructure Investments

India’s converted flexible packaging market is benefiting from government programs like Swachh Bharat Abhiyan and plastic waste management rules, which ban certain single-use plastics and implement EPR regulations requiring 30% recycled content in rigid plastics by 2025. Investments exceeding INR 10,000 crore are enhancing recycling infrastructure, providing contract packagers with steady access to recycled materials. In May 2025, JPFL Films expanded capacity with new BOPP, PET, and CPP lines in Nashik, Maharashtra, with a capital commitment exceeding INR 700 crore, highlighting strong growth in flexible packaging.

Technological adoption is accelerating with automated systems and affordable, efficient solutions, including plastic-free laminate films suitable for lamination with paper and foil. Rapid expansion of domestic e-commerce, food and beverage, and pharmaceutical sectors is a major driver, while strategic partnerships such as the CIRCLE Alliance, backed by Unilever, USAID, and EY with USD 21 million, promote circular packaging practices. The growing food processing sector, particularly ready-to-drink beverages and processed foods, continues to fuel demand for sustainable, functional, and high-performance converted flexible packaging in India.

Brazil Converted Flexible Packaging Market Growing on Regulatory Support and Strategic Investments

Brazil’s converted flexible packaging market is influenced by the National Solid Waste Policy and new legislation banning single-use disposable items, setting a 2030 target for fully compostable or recyclable packaging. Robotics and AI are enhancing efficiency and quality control, with biodegradable films such as carboxymethyl cellulose (CMC) from sugarcane bagasse emerging as sustainable solutions.

Corporate investments are shaping market growth, exemplified by Sonoco’s acquisition of Inapel Embalagens Ltd. to strengthen flexible packaging operations and meet rising food sector demand. Key applications include food and beverage and cosmetics sectors, with expanding food processing driving technology adoption. Government support, such as Klabin’s BRL 188 million (USD 35.7 million) investment in Ceará, expanding sustainable corrugated board capacity, reinforces the focus on environmentally friendly packaging. The Brazilian market is witnessing a marked shift toward recyclable and biodegradable flexible packaging solutions, driven by regulatory backing and growing consumer sustainability awareness.

Japan Converted Flexible Packaging Market Innovating Through Bio-PP and High-Performance Films

Japan’s converted flexible packaging industry is a leader in precision manufacturing and next-gen production, increasingly turning to bio-polypropylene (bio-PP) to achieve sustainability targets. The Plastic Resource Circulation Act (April 2022) encourages environmentally conscious design, aiming for 2 million tonnes per year of bio-PP products by 2030.

The market is shifting toward specialty and value-added films, with innovations in barrier properties and IoT-enabled tracking. Functional enhancements such as high dimensional stability and deformation resistance are driving premium applications. Corporate collaborations, such as LyondellBasell’s bio-based PP partnership with Shiseido, and acquisitions like TOPPAN Holdings’ purchase of Sonoco’s Thermoformed & Flexible Packaging business for USD 1.8 billion, are strengthening the industry’s position in food, healthcare, and retail packaging. Japan’s market exemplifies the integration of sustainability, technology, and high-performance functional packaging for advanced consumer applications.

Converted Flexible Packaging Market Report Scope

Converted Flexible Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$172.4 Billion

|

|

Market Size (2034)

|

$288.8 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Packaging Material (Plastic, Paper, Aluminum), By Packaging Format (Pouches, Bags, Films, Wraps, Lids & Labels), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Industrial, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Constantia Flexibles, Sonoco Products Company, ProAmpac, DS Smith plc, WestRock Company, Sealed Air Corporation, Berry Global Group, Inc., Coveris Holdings S.A., Uflex Ltd., TC Transcontinental Inc., Novolex, Ahlstrom-Munksjö

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Converted Flexible Packaging Market Segmentation

By Packaging Material

By Packaging Format

- Pouches

- Bags

- Films

- Wraps

- Lids & Labels

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Industrial

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Converted Flexible Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles

- Sonoco Products Company

- ProAmpac

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Berry Global Group, Inc.

- Coveris Holdings S.A.

- Uflex Ltd.

- TC Transcontinental Inc.

- Novolex

- Ahlstrom-Munksjö

* List Not Exhaustive

Methodology

The Converted Flexible Packaging Market analysis has been conducted by USDAnalytics using a comprehensive and structured methodology tailored for industry professionals. Our approach combines primary research, including in-depth interviews with key stakeholders such as converters, brand owners, sustainability experts, and regulatory authorities, with secondary research from corporate reports, press releases, patent databases, government regulations, and trade publications. Quantitative analysis was applied to forecast market size, growth, and segmentation by packaging material, packaging format, and end-use industry, while qualitative insights evaluated sustainability adoption, mono-material integration, smart packaging innovations, and automation trends. USDAnalytics also analyzed M&A activity, capital investments, technological advancements in high-barrier films, post-consumer recycled (PCR) content, and bio-based materials, ensuring a holistic understanding of global market dynamics, competitive strategies, and strategic opportunities for decision-making in the converted flexible packaging sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.