Market Overview: Cups and Lids Sector Expands to $30 Billion by 2034

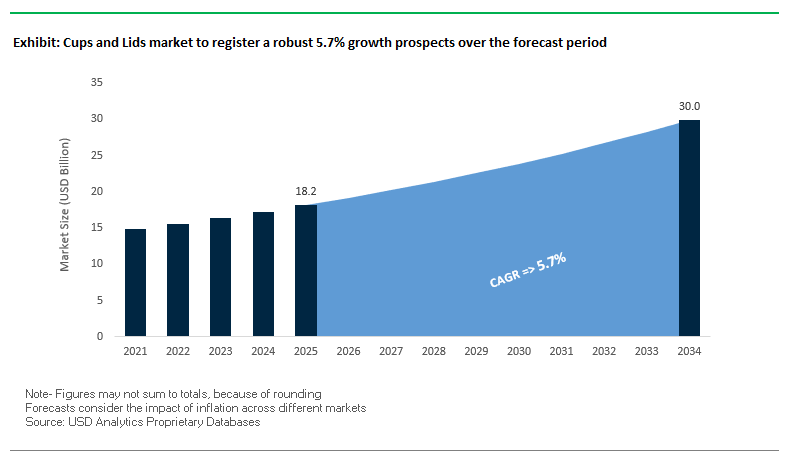

The global cups and lids market is projected to grow from $18.2 billion in 2025 to $30 billion by 2034, achieving a CAGR of 5.7%. This sector plays a pivotal role in the foodservice, on-the-go consumption, and consumer goods industries, evolving rapidly to meet sustainability goals, consumer convenience needs, and branding opportunities. For industry professionals, critical questions include: How fast will paper and bio-based materials replace traditional plastics? What innovations will dominate on-the-go and delivery packaging? And how will high-definition customization drive consumer engagement?

Key Insights shaping the cups and lids market:

- Sustainable Material Shift: Over 75% of new hot beverage cup launches now focus on paper or bio-plastics, accelerating the move away from traditional plastics.

- On-the-Go Packaging: Rising delivery and takeaway consumption fuels demand for leak-resistant and tamper-evident lids to ensure safety and product integrity.

- Recycled Content: New PET cups with up to 65% PCR material mark a milestone in circular economy progress.

- Branding and Customization: More than 70% of companies are adopting HD printing on cups and lids, transforming packaging into marketing assets that enhance brand visibility.

The growth trajectory reflects a market balancing eco-friendly mandates, consumer lifestyle shifts, and brand marketing needs, positioning cups and lids as a critical enabler of sustainable and convenient foodservice packaging.

Market Analysis: Sustainability, M&A, and Innovation Drive Growth

The global cups and lids market in 2025 is being reshaped by sustainability initiatives, mergers and acquisitions, and product innovation across regions.

In September 2025, Sabert Corporation Europe partnered with Flexeserve to launch its PulpUltra plant-based hot food packaging range, highlighting the trend toward fiber-based complementary cups and lids. Similarly, in August 2025, Verallia introduced its Vista bottle using 100% PCR glass, signaling the broader packaging shift to recycled content a practice increasingly mirrored in plastic cups and paper lids.

Also in August 2025, Orora Group acquired Saverglass for €1.29 billion, strengthening its position in premium beverage and cosmetic packaging. Though focused on glass, this reflects a wider consolidation trend across adjacent packaging categories, including cups and lids. In July 2025, Huhtamaki launched compostable fiber-based ice cream cups, emphasizing its leadership in fully compostable foodservice products. That same month, the Smurfit Kappa–WestRock merger created Smurfit WestRock, a powerhouse in paper-based packaging, reshaping the competitive dynamics for paper cups and lids.

Earlier in the year, in February 2025, The Good Cup introduced a breakthrough single-use paper cup design that eliminates the need for a separate plastic lid. Meanwhile, March 2025 developments highlighted WestRock and Liberty Coca-Cola’s installation of recyclable paperboard multipack carriers, further reinforcing the market shift away from plastics.

Trends and Opportunities Reshaping the Cups and Lids Market

Regulatory-Driven Material Transition from PFAS-Treated to Compliant Fiber-Based Solutions

The cups and lids market is undergoing a regulatory-driven transformation, as governments and regulators mandate the elimination of per- and polyfluoroalkyl substances (PFAS) from food-contact materials. Growing health concerns, alongside legal restrictions, are compelling manufacturers to accelerate innovation in barrier coatings that provide grease and moisture resistance without relying on “forever chemicals.” In the U.S., multiple states including Washington, Maine, and California implemented bans on intentionally added PFAS in packaging beginning in 2022, reshaping procurement policies for foodservice operators. This trend gained further momentum in February 2024, when the U.S. FDA confirmed the voluntary withdrawal of PFAS-containing grease-proofing agents from the American market.

Leading suppliers are responding with PFAS-free, recyclable alternatives. Companies like Solenis have introduced TopScreen™ water-based coatings, which are both compostable and repulpable, enabling cups and lids to enter conventional recycling streams without contamination. On the global stage, the EU-funded Zero F project exemplifies collaborative innovation, uniting 12 industry and research partners since 2023 to develop barrier coatings from renewable raw materials. Collectively, these regulatory and technological shifts mark a pivotal moment, positioning fiber-based, compliant cups as the new industry benchmark for safety, sustainability, and regulatory compliance.

Integration of Digital Printing for Hyper-Customization and Limited-Edition Campaigns

Another defining trend in the cups and lids market is the rapid adoption of digital printing technology to enable high-impact customization and agile marketing strategies. Beverage brands, quick-service restaurants, and event organizers increasingly demand short-run, personalized packaging that can reflect regional campaigns, limited-edition launches, or co-branded promotions. A case study by Canon Europe demonstrated that corrugated and cup packaging producers using digital platforms can offer highly tailored designs with significantly faster turnaround times compared to analog printing.

The shift toward on-demand digital printing also reduces inventory pressure and minimizes waste from obsolete stock. Seasonal campaigns such as summer beverage launches or sports-event tie-ins can be executed efficiently without committing to large, inflexible print runs. In parallel, advances in digital inkjet technology now allow cups to feature full-color, photographic-quality graphics, significantly elevating visual appeal and consumer engagement. This makes the cup itself a powerful, on-the-go marketing medium, turning functional packaging into a dynamic brand-building tool, especially in markets where unboxing and consumer experience are central to brand value.

Development of Truly Recyclable and Compostable Mono-Material Polypropylene Cups

While PLA-lined paper cups have gained traction in recent years, their industrial compostability remains limited by infrastructure availability. This has created a clear market opportunity for mono-material polypropylene (PP) cups and lids, which are highly recyclable in existing PP streams. According to sustainability publications, mono-material packaging eliminates the need for resin separation, simplifying the recycling process and increasing recovery rates.

The use of all-PP solutions also aligns with global recycling mandates and streamlines supply chains, as companies can rely on a single material family for compliance across multiple markets. Brands adopting this solution benefit from a reduced carbon footprint, simplified procurement, and alignment with consumer demand for genuinely recyclable packaging formats. In addition, PP-based cups and lids can be engineered to meet high-performance standards for heat resistance, durability, and product safety, positioning them as both a cost-effective and sustainable alternative to hybrid packaging models.

Smart Lid Integration for Enhanced Consumer Experience and Operational Efficiency

The lids segment represents a high-potential platform for innovation, with opportunities to integrate smart and connected features that enhance both consumer experience and operational efficiency. NFC-enabled lids, for example, can connect consumers directly to loyalty programs, digital games, or feedback surveys through a smartphone tap, providing brands with a powerful channel for first-party data collection and engagement.

From a functional perspective, temperature-sensitive smart lids are being explored to provide consumers with real-time safety indicators, such as color-changing features that signal when a hot beverage has cooled to a drinkable temperature. More advanced iterations may incorporate sensors capable of monitoring beverage freshness or alerting users to temperature fluctuations. On the operational side, RFID-enabled lids offer tangible value to quick-service restaurants and foodservice providers by improving inventory management, speeding up order fulfillment, and reducing service errors in high-volume environments.

Competitive Landscape: Leading Players Shaping the Cups and Lids Market

The cups and lids market is led by global packaging giants and specialized innovators, each leveraging sustainability, scale, or branding solutions to maintain competitive strength.

Dart Container Corporation leverages scale with its Solo® brand

Dart Container is a market leader with its Solo® brand, offering cups and lids made from foam, PET, paper, and bio-based materials. With over 40 facilities across six countries, Dart benefits from scale and vertical integration, producing raw materials and inks internally to reduce costs. Its distribution network and diversified portfolio make it a one-stop supplier for foodservice, healthcare, education, and retail clients.

Berry Global integrates high PCR content into PET cups

Berry Global manufactures clear PET and PP drinking cups with dome lids, emphasizing sustainability through 65% PCR integration. It recently launched reusable plastic cups for foodservice, positioning itself as a key enabler of the circular economy. Berry’s vertically integrated model ensures raw material sourcing, compliance management, and digital-printing compatibility, serving food, healthcare, and industrial clients worldwide.

Huhtamaki Oyj pioneers compostable fiber-based cup solutions

Huhtamaki is a global foodservice packaging giant, offering paper hot and cold cups and a variety of lids. Its blueloop platform drives next-generation sustainable innovation. In July 2025, it launched fiber-based compostable ice cream cups suitable for both home and industrial composting. Key offerings include Bioware compostable hot cups and Impresso double-wall insulated cups, underscoring Huhtamaki’s global leadership in paper-based packaging.

Sonoco Products Company specializes in niche and specialty lids

Sonoco, known for industrial and rigid paper packaging, also provides specialty cups and lids for food, lab, and industrial use. Its expertise lies in peelable membranes and easy-open ends, enhancing sealing and safety. Recent divestitures reflect Sonoco’s strategic refocus on high-growth specialty packaging, aligning with its “Better Packaging. Better Life.” initiative.

Sabert Corporation drives plant-based packaging innovation

Sabert specializes in foodservice packaging with its Hot & Tasty and PulpUltra ranges, offering plant-based, paperboard, and recyclable solutions. In September 2025, it launched PulpUltra recyclable hot food boxes in collaboration with Flexeserve. Sabert is also pioneering PFAS-free packaging to meet stricter regulatory demands. Its acquisition of Colpac in the UK bolstered its leadership in paper-based foodservice packaging, a high-growth segment aligned with global sustainability goals.

Cups and Lids market Share Insights

Paper & Fiber-Based Packaging Dominates Market Share by Material

Paper and fiber-based cups and lids are projected to hold 48% of the cups and lids market in 2025, overtaking plastic as the leading material category. This shift is directly tied to global sustainability regulations, including bans on single-use plastics and Extended Producer Responsibility (EPR) mandates in regions such as Europe and North America. Paper cups, typically lined with thin layers of polyethylene (PE) or polylactic acid (PLA) for liquid resistance, are widely adopted by quick-service restaurants (QSRs), coffee chains, and institutional buyers aiming to comply with these mandates. Plastic, with a 35% share, remains resilient, particularly polypropylene (PP) cups that excel in heat resistance and leak-proof performance for hot beverages. Cost competitiveness and robust supply chains ensure plastics continue to play a critical role despite regulatory headwinds. Bio-based and compostable alternatives, though still emerging, represent the fastest-growing material category, with PLA and other biopolymers offering the performance of plastic while addressing end-of-life concerns. Their uptake is strongly supported by corporate ESG commitments but constrained by cost premiums and inconsistent industrial composting infrastructure.

Cups Drive the Majority of Market Share by Product Type

Cups account for 70% of the cups and lids market in 2025, reflecting their role as the primary product purchased and the focal point of sustainability innovation. The ongoing transition from plastic to paper and compostable options is overwhelmingly cup-driven, as regulators and consumers place direct scrutiny on beverage containers. Design improvements such as double-walled fiber cups and PLA-lined variants are setting new industry standards for functionality and compliance. Lids, representing 30% of the market, remain a smaller but strategically critical segment. Their importance lies in compatibility and performance creating leak-proof seals, ensuring fit across multiple cup sizes, and providing user-friendly features such as sippable spouts or strawless openings. Lid development has lagged behind cup innovation, but with increasing emphasis on full-system recyclability and compostability, sustainable lid solutions are becoming a top priority for packaging producers.

Food & Beverage Services Continue to Anchor Market Share by End-Use

Food and beverage services dominate the cups and lids market with a 75% share in 2025, led by QSR chains, coffee shops, and fast-casual outlets. Their massive daily beverage volumes and strong brand reliance on packaging as a customer touchpoint make them the epicenter of both regulatory impact and material innovation. These businesses are leading the transition toward paper and compostable cups, supported by both consumer expectations and policy mandates. Institutional buyers, including schools, corporate offices, and healthcare facilities, hold 15% of the market, with large-volume purchasing that is highly cost-sensitive but increasingly driven by institutional sustainability commitments. They represent a crucial demand center for competitively priced fiber-based or compostable products. Households remain a smaller segment, where purchase decisions are influenced more by price and convenience than sustainability, allowing plastic cups and lids to retain strong shelf presence at retail. This end-use segmentation underscores the dominance of foodservice as the driver of change, while institutions and households act as secondary markets with varying degrees of sustainability adoption.

United States: Driving Innovation in Sustainable and E-Commerce Friendly Cups and Lids

The U.S. cups and lids market is being reshaped by a surge in demand for sustainable and compostable materials, particularly plant-based options like polylactic acid (PLA). Consumer preference for environmentally friendly alternatives, coupled with state-level restrictions on single-use plastics, is accelerating adoption of eco-friendly cups and lids. Lightweighting is another key trend, with manufacturers introducing thinner-wall injection molded designs that maintain structural integrity while reducing material usage and environmental impact.

The rapid growth of food delivery and e-commerce is driving demand for spill-proof, durable cups and lids that ensure product quality during transit. Brands are also increasingly integrating digital printing technologies, enabling rapid customization, enhanced branding, and alignment with evolving consumer trends. These innovations position the U.S. as a leader in sustainable, functional, and consumer-focused cups and lids solutions.

Germany: Leading the Way in Reusable and Circular Economy Cups and Lids

Germany’s cups and lids industry is at the forefront of the reusable packaging revolution, driven by the Packaging Act (VerpackG), which mandates reusable alternatives for takeaway items. Companies are innovating with reusable cup and lid systems and reverse vending infrastructures, reducing environmental impact. The German market is also pioneering biodegradable solutions, such as cups made from coffee grounds and waste oil, significantly cutting the carbon footprint compared to traditional disposable cups.

Strict EU regulations, including the Single-Use Plastics Directive, are further shaping the market, compelling manufacturers to adopt plastic-free alternatives. These developments make Germany a leader in circular economy-aligned cups and lids, combining sustainability with regulatory compliance and innovation in design.

China: Expanding Manufacturing Base and Sustainable Paper-Based Cups

China remains a global manufacturing and export hub for cups and lids, serving both its vast domestic market and international demand. The country is witnessing a notable shift toward paper-based solutions with biodegradable coatings, responding to growing consumer preference for eco-friendly and compostable cups and lids. Manufacturers are investing in advanced production machinery and automated lines to efficiently meet high-volume demand while expanding product offerings, from traditional plastics to innovative biodegradable alternatives.

This focus on scale, efficiency, and sustainability positions China as a key player in the global cups and lids market, driving both domestic consumption and international exports. The integration of technological innovation ensures that products are functional, durable, and environmentally responsible.

India: Accelerating Adoption of Sustainable Cups and Lids in Food Service

India’s cups and lids market is strongly influenced by government initiatives to reduce plastic waste, encouraging the adoption of sustainable materials like bagasse, a plant-based and compostable alternative. The country’s booming food service and delivery sector is a major end-user, fueling demand for hygienic, convenient, and eco-friendly cups and lids.

Domestic manufacturers are responding by expanding production facilities and adopting advanced technologies to meet rising demand and support exports. This growth reflects India’s dual focus on sustainability and market expansion, positioning the country as an emerging hub for eco-conscious cups and lids solutions.

Brazil: Transitioning to Bio-Based Plastics and Premium Packaging Designs

Brazil’s cups and lids market is shifting toward bio-based plastics, primarily derived from sugarcane, in response to both consumer demand and government sustainability initiatives. This move reduces environmental impact and aligns with global trends toward eco-friendly packaging materials.

The growth of e-commerce and food delivery services is driving demand for secure, tamper-evident lids, ensuring food safety and product integrity during transportation. Additionally, the market is witnessing premiumization trends, with a focus on enhanced functionality, unique designs, and branding opportunities for cups and lids. These innovations highlight Brazil’s commitment to sustainable, high-quality, and consumer-oriented packaging solutions.

Cups and Lids market Report Scope

Cups and Lids market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.2 Billion

|

|

Market Size (2034)

|

$30 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material (Paper, Plastic, Bio-based & Compostable Materials), By Product Type (Cups, Lids), By End-Use Industry (Food & Beverage Services, Institutional, Household, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Dart Container Corporation, Berry Global Inc., Genpak, LLC, Sonoco Products Company, Pactiv Evergreen Inc., Newell Brands Inc., International Paper Company, Fabri-Kal, Lollicup USA Inc., BillerudKorsnäs AB, Fuling Global Inc., Detpak, Paper Straws, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cups and Lids Market Segmentation

By Material

- Paper

- Plastic

- Bio-based & Compostable Materials

By Product Type

By End-Use Industry

- Food & Beverage Services

- Institutional

- Household

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cups and Lids Market

- Huhtamaki Oyj

- Dart Container Corporation

- Berry Global Inc.

- Genpak, LLC

- Sonoco Products Company

- Pactiv Evergreen Inc.

- Newell Brands Inc.

- International Paper Company

- Fabri-Kal

- Lollicup USA Inc.

- BillerudKorsnäs AB

- Fuling Global Inc.

- Detpak

- Paper Straws

- Greiner Packaging International GmbH

* List Not Exhaustive

Research Coverage

This report investigates the global Cups and Lids Market, offering comprehensive insights into material innovations, regulatory influences, and evolving consumer preferences. USDAnalytics presents an in-depth analysis of breakthroughs in sustainable paper, bio-based, and recyclable plastics, highlighting advances in PFAS-free coatings, mono-material polypropylene solutions, and digital printing customization. The report reviews market dynamics including on-the-go and delivery packaging trends, branding opportunities, and the integration of smart lid technologies that enhance consumer engagement. It also highlights the competitive landscape, covering strategic expansions, mergers, and product innovations among leading players, making this report an essential resource for investors, manufacturers, packaging designers, and industry professionals seeking actionable intelligence and forward-looking market forecasts. From sustainability-driven shifts to regional growth patterns, this analysis provides detailed guidance on opportunities, challenges, and strategies that will define market performance from 2025 to 2034. USDAnalytics ensures the report combines historical trends, cutting-edge innovations, and forecast projections to deliver unparalleled clarity for decision-making.

Scope Highlights:

- Segmentation: By Material (Paper, Plastic, Bio-based & Compostable Materials), By Product Type (Cups, Lids), By End-Use Industry (Food & Beverage Services, Institutional, Household, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ companies including Huhtamaki Oyj, Dart Container Corporation, Berry Global Inc., Genpak, Sonoco Products Company, Pactiv Evergreen, and others

Methodology

The Cups and Lids Market report employs a rigorous research methodology combining both primary and secondary sources to deliver reliable, actionable insights. Primary research included interviews with industry executives, packaging designers, sustainability specialists, and procurement managers to gather qualitative and quantitative data on emerging trends, material innovations, and regulatory compliance. Secondary research involved comprehensive review of industry reports, company filings, trade publications, regulatory frameworks, and market databases. Data triangulation was used to validate findings, while market modeling techniques projected growth rates, market shares, and material adoption patterns from 2025 to 2034. USDAnalytics also analyzed historical data from 2021 to 2024 to identify growth drivers, regional performance variations, and end-user dynamics, ensuring the research is both forward-looking and grounded in proven market behavior.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.