Market Overview: Convenience and Sustainability Transforming Disposable Drinkware

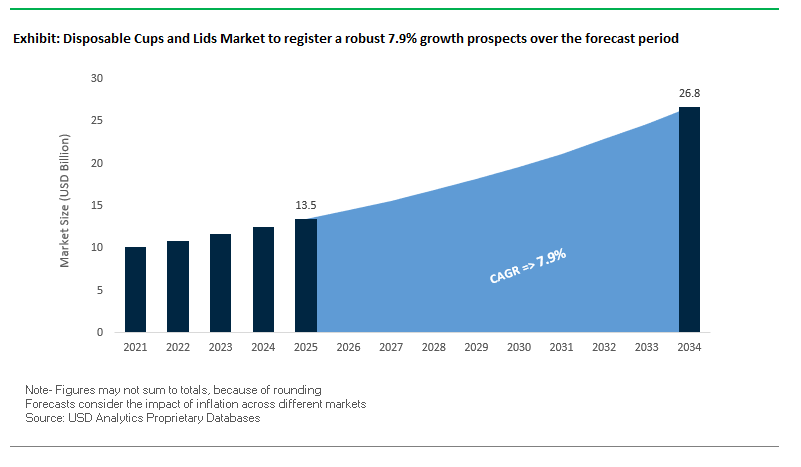

The Global Disposable Cups and Lids Market is projected to grow from USD 13.5 billion in 2025 to USD 26.8 billion by 2034, expanding at a CAGR of 7.9%. This market represents a critical intersection between consumer convenience, quick-service demand, and sustainability imperatives, making it a central focus for foodservice providers, beverage brands, and packaging manufacturers.

Disposable cups and lids remain indispensable for quick-service restaurants (QSRs), cafés, and the booming online food delivery sector, where hot and cold beverages account for a significant portion of consumption. The shift toward eco-friendly materials—such as compostable PLA, molded fiber, and recyclable mono-material plastics—is redefining growth strategies as governments tighten regulations on single-use plastics.

Technological advancements are also reshaping the industry. Digital printing on paper cups is increasingly used to deliver high-quality graphics and variable data personalization, offering brand owners new avenues for consumer engagement and promotional campaigns. Meanwhile, the adoption of mono-material lids (PET/PP) is simplifying recycling processes and helping brands align with circular economy goals.

Key Insights for professionals and Buyers:

- Online food delivery and QSRs drive massive global consumption of cups and lids.

- Regulatory pressure accelerates shift from plastic/foam to fiber-based and compostable materials.

- Mono-material PET/PP lids are emerging as a scalable recycling solution.

- Digital printing adoption supports personalization and brand marketing on cups.

- Consolidation through mergers and acquisitions is reshaping competitive strategies.

Market Analysis: Recent Developments in the Disposable Cups and Lids Industry

The Disposable Cups and Lids Market has been witnessing major strategic shifts in 2025, with companies investing in sustainability, acquisitions, and technological upgrades to remain competitive.

In August 2025, Dart Container Corporation launched recyclable paperboard lids to replace traditional plastic, gaining strong adoption from leading quick-service chains. During the same month, Huhtamaki Oyj priced EUR 300 million in notes to refinance debt and channel funds toward sustainable packaging growth.

Earlier in May 2025, Dart Container introduced Solo® recycled-content paper hot cups featuring scannable QR codes, enabling consumer interaction and reinforcing its circular economy commitment. In April 2025, Pactiv Evergreen secured regulatory approvals for its acquisition by Novolex, a consolidation expected to strengthen its North American leadership. Also in April, the Smurfit Kappa–WestRock merger reshaped the paper-based packaging landscape, with potential implications for corrugated cup and container segments.

Technology-driven sustainability is also in focus. In March 2025, Dart Container partnered with Sweden’s PulPac to bring dry molded fiber technology to North America, aiming to revolutionize cup and lid production with fiber-based alternatives. In February 2025, the merger of International Paper and DS Smith created a new global leader in sustainable packaging solutions, while Berry Global reaffirmed its commitment to FMCG packaging by prioritizing mono-material innovations and recycled-content designs.

Disruptive Trends and High-Value Opportunities Reshaping the Disposable Cups and Lids Market

Accelerated Regulatory-Driven Material Transition from PFAS-Treated Paper to Safer Alternatives

The disposable cups and lids market is undergoing a rapid transformation due to regulatory bans on per- and polyfluoroalkyl substances (PFAS) in food packaging. Several U.S. states, including New York and Colorado, have already implemented bans, while the European Union is progressing toward restricting nearly 10,000 PFAS compounds. This regulatory wave, combined with rising consumer health awareness, is compelling brands and packaging converters to pivot from PFAS-coated paperboard to safer alternatives such as polyethylene (PE)-coated paper, polylactic acid (PLA)-coated paper, and polymer-based substrates. Global leaders are making decisive moves—Starbucks announced complete PFAS elimination from U.S. packaging by 2022 and globally by 2023, creating a ripple effect across the supply chain. At the same time, R&D initiatives like the EU-funded Zero F project are accelerating innovation in renewable raw material coatings. Emerging solutions, such as water-based dispersion coatings that are food-safe and home-compostable, showcase the industry’s shift toward sustainability. This material transition not only ensures compliance but also opens avenues for premium eco-friendly packaging solutions, reinforcing brand value while future-proofing supply chains.

Strategic Expansion of Reusable Cup-as-a-Service (RaaS) Infrastructure by Global QSRs

Another disruptive trend in the disposable cups and lids market is the rise of Reusable Cup-as-a-Service (RaaS) models, particularly among quick-service restaurants (QSRs) and global coffee chains. With single-use plastic taxes looming and consumer awareness of waste reduction increasing, brands are piloting scalable, trackable reusable cup systems. For example, Zero Waste Scotland reported that over 388.7 million single-use beverage cups are used annually in the country, sparking proposals for consumer charges to encourage reuse. Companies are responding with deposit-return schemes, where customers borrow a durable cup and return it at any participating location for cleaning and redistribution, often supported by third-party logistics providers. Some operators employ digital tracking via unique IDs or mobile apps, enabling seamless cup circulation and minimizing loss. This evolution shifts the market from a one-time transactional model to a long-term, asset-based value chain, creating demand for durable cup designs, washing logistics infrastructure, and digital tracking solutions. For packaging manufacturers and logistics providers, RaaS represents a high-growth segment, with the potential to redefine brand-consumer relationships while aligning with global sustainability goals.

Development of High-Performance, Home-Compostable Polymer Blends for Hot Applications

One of the most compelling opportunities in the disposable cups and lids industry lies in the development of high-performance, compostable polymer blends that can rival traditional plastics in functionality while offering full home and industrial compostability. Current solutions like PLA excel in cold applications but fail under high temperatures, making them unsuitable for hot beverages and carbonated drinks. This performance gap is driving R&D investment into novel resins and cellulose-based materials. For instance, a leading bioplastics innovator has created a cellulose molding compound with mechanical properties comparable to polypropylene, while also being marine biodegradable. Such breakthroughs highlight the technical feasibility of replacing petroleum-based plastics without compromising performance. For brands, adopting these materials provides a dual benefit: meeting consumer demand for eco-friendly solutions and ensuring compliance with tightening sustainability regulations. The commercialization of compostable, heat-resistant polymers represents a massive growth avenue, enabling companies to capture a premium eco-conscious consumer segment while accelerating progress toward a circular packaging economy.

Integration of Digital Watermarking for Advanced Waste Stream Sorting

The integration of digital watermarking technologies represents a game-changing opportunity to solve one of the industry’s biggest challenges—accurate sorting and recycling of disposable cups. Current Material Recovery Facilities (MRFs) struggle to distinguish between polymers, resulting in contamination and reduced recycling efficiency. The HolyGrail 2.0 initiative, backed by over 120 companies across the value chain, has proven the feasibility of embedding invisible digital codes directly into packaging. These codes, detected by high-resolution cameras, allow precise sorting by polymer type, brand, or compostability, dramatically improving recycling purity rates. Semi-industrial trials have already shown strong results, suggesting scalability across global systems. For manufacturers, incorporating digital watermarking into cup designs creates a high-value differentiation strategy, positioning their products as not only recyclable but also recycling-enabled. Beyond compliance, this technology fosters a data-driven packaging ecosystem, requiring collaboration among converters, technology providers, and waste management operators. By enabling closed-loop recovery systems, digital watermarking could unlock the full circular potential of disposable cups, transforming waste into a resource.

Competitive Landscape: Key Players Reshaping Disposable Cups and Lids

The global market is dominated by established leaders and fast-moving innovators, each leveraging sustainability, technology, and M&A activity to strengthen their positions.

Dart Container Corporation focuses on recyclable and fiber-based innovation

Dart Container leads through its Solo® and Dart® brands, offering an extensive range of plastic, foam, and paper cups and lids. In August 2025, it launched recyclable paperboard lids, while in March 2025, it partnered with PulPac to introduce dry molded fiber production in North America. Dart also unveiled QR-enabled Solo® cups in May 2025, integrating sustainability with consumer engagement. Its focus is on next-generation fiber-based packaging to replace legacy foam and plastics.

Huhtamaki Oyj strengthens global footprint with sustainability-driven investments

Huhtamaki is a global packaging specialist with deep expertise in foodservice packaging. In 2025, it priced EUR 300 million in notes to fund growth initiatives and completed the acquisition of Zellwin Farms to expand its U.S. packaging operations. Huhtamaki emphasizes compostable and recyclable cup and lid solutions, aligned with its three-year efficiency program and a strategy to lead in fiber-based and circular economy packaging.

Berry Global Group advances mono-material cups and lids for recycling

Berry Global is at the forefront of plastic packaging innovation, with strong expertise in mono-material lid development and the integration of Post-Consumer Resin (PCR). Its February 2025 Q1 results showed growth driven by FMCG demand. Berry’s strategy focuses on designing cups and lids optimized for recyclability, reducing virgin plastic use, and expanding its role in circular packaging systems.

Graphic Packaging International drives fiber-based cup innovation

Graphic Packaging specializes in sustainable paperboard packaging, providing high-quality cups and cartons. In 2025, it won PAC Global’s Best in Class Innovation Award for its EnviroClip™ solution, which eliminates shrink film. Its investments in the Waco, Texas recycled paperboard facility will significantly expand capacity for sustainable cup and container production. Graphic Packaging’s strength lies in graphically rich, recyclable, and renewable paperboard packaging for beverages and foodservice.

Pactiv Evergreen consolidates with Novolex to expand foodservice leadership

Pactiv Evergreen is a major supplier of disposable cups, lids, and food containers in North America. In April 2025, it received final approvals for its acquisition by Novolex, a move that will create a stronger integrated leader in foodservice packaging. Pactiv’s portfolio spans plastic and fiber-based cups, lids, trays, and containers, with a strategic focus on scaling recyclable and renewable materials. The merger enhances its capacity to address both QSR and e-commerce-driven food delivery markets.

Disposable Cups and Lids Market Share Insights

Cups Maintain Overwhelming Market Share by Product Type in Disposable Cups and Lids

Cups dominate the disposable cups and lids industry, holding 75% of the market share by 2025. This dominance stems from their inherent role as the consumable core of the category, while lids function only as complementary accessories. High demand from quick-service restaurants (QSRs), coffee shops, and beverage chains ensures daily, global-scale consumption volumes, particularly for cold drinks and water where lids are optional. Meanwhile, regulatory scrutiny on single-use plastics is pushing rapid adoption of compostable and fiber-based cups, making this segment central to the industry’s sustainability transition. Innovations in biopolymer linings, recyclable barrier coatings, and reusable cup models are primarily concentrated in this category, underscoring why cups not only dominate by volume but also serve as the focal point of technological development and environmental compliance.

Food Services Dominate Market Share by End-Use in Disposable Cups and Lids

Food services account for 70% of industry demand, making them the undisputed growth engine of the disposable cups and lids market. This segment includes QSRs, fast-casual dining, coffee chains, and delivery platforms, where convenience, hygiene, and branding are non-negotiable. The entrenched culture of takeaway consumption, coupled with the rise of food delivery apps, sustains massive daily demand. Food service operators also act as early adopters of compostable and recyclable cup-lid systems, responding both to regulatory mandates and consumer expectations for eco-friendly options. Their dominance also reflects the operational scale of this channel, where bulk procurement, rapid turnover, and global standardization of packaging drive continuous innovation and investment.

United States Disposable Cups and Lids Market Driven by Eco-Friendly Innovations and On-the-Go Demand

The United States disposable cups and lids market is shaped by a fragmented regulatory environment, with state and city-level bans on single-use plastic foam products driving a shift toward paper, compostable, and reusable alternatives. FDA regulations on food contact materials are also influencing the selection of materials and coatings, ensuring safety and compliance. Technological advancements in water-based or aqueous coatings are making paper cups fully recyclable, overcoming the limitations of traditional polyethylene linings.

Corporate investments are focused on expanding sustainable production capabilities. In 2024, a leading packaging firm invested millions in a new facility to produce high-performance, recyclable paper cups and lids, catering to the surging demand from quick-service restaurants (QSRs) and food delivery sectors. Key applications include coffee shops, convenience stores, and e-commerce-driven delivery services, where durability, insulation, and spill-resistance are crucial. Sustainability initiatives are further supported by the adoption of Post-Consumer Recycled (PCR) content and compostable bioplastics like Polylactic Acid (PLA), reflecting strong consumer and brand-driven pressure for eco-friendly packaging solutions.

Germany Disposable Cups and Lids Market Advancing Through Reusables and Circular Economy Leadership

Germany’s disposable cups and lids market operates under strict EU regulations, including the Packaging and Packaging Waste Regulation (PPWR) effective February 2025, which mandates fully recyclable or reusable packaging by 2030. Germany’s well-established Extended Producer Responsibility (EPR) system encourages innovation in recycling and sustainable packaging design. A 2023 law requiring food service businesses to offer reusable alternatives alongside single-use cups is accelerating the adoption of reusable solutions.

Technological innovation is key, with machinery development to handle sustainable materials and the introduction of digital product passports and watermarks improving material transparency. The retail and food service sectors drive demand for premium paper cups with unique aesthetics and eco-friendly features. Germany’s “Plattform Industrie 4.0” initiative enhances manufacturing efficiency via cyber-physical systems and IoT integration. The market also serves as a testing ground for reusable and deposit-based beverage cup systems, which are increasingly adopted by cafes and businesses nationwide to reduce single-use waste.

China Disposable Cups and Lids Market Expands Through Green Policies and Smart Manufacturing

China’s disposable cups and lids market is propelled by governmental sustainability initiatives, including the 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement, which encourages recycling and the use of eco-friendly materials. Regulations targeting excessive packaging, including limits on packaging layers and void ratios, are particularly impactful in the e-commerce and food delivery sectors.

Technological investments in automation, AI, and “5G plus industrial internet” are optimizing production processes and enhancing flexible manufacturing capabilities. Domestic substitution of imported technologies is a key trend, with local companies scaling up production to meet growing demand for high-quality, circular packaging. Rapid expansion of e-commerce, food and beverage delivery, and quick-service restaurants are driving market growth, with ongoing R&D and patent activity enabling innovation in sustainable materials and advanced coatings.

Brazil Disposable Cups and Lids Market Accelerates Through Regulatory Mandates and Eco-Friendly Investments

Brazil’s disposable cups and lids market is strongly influenced by the National Solid Waste Policy and 2024 legislation banning single-use disposable items, requiring all packaging to be returnable, recyclable, or fully compostable by 2030. Sustainability-focused technological innovations, including AI, robotics, and biodegradable films with low water vapor permeability using sugarcane-derived carboxymethyl cellulose (CMC), are enhancing production efficiency and product performance.

Corporate investments focus on sustainable packaging solutions, exemplified by Wheaton’s interactive design facility in São Paulo. Key applications include food, beverage, and cosmetics sectors, where eco-friendly materials and bio-based coatings are increasingly in demand. Government support through FINEP-backed projects, such as a R$40 million sustainable cellulose fiber packaging plant, further reinforces the market’s focus on green manufacturing. Digital printing and high-performance paper solutions are emerging as preferred eco-friendly alternatives, aligning with Brazil’s ambitious sustainability targets.

Japan Disposable Cups and Lids Market Transforms Through Bio-Based Materials and High-Performance Films

Japan’s disposable cups and lids market leverages advanced precision manufacturing to integrate bio-polypropylene (bio-PP) and other sustainable materials. The Plastic Resource Circulation Act, effective April 2022, promotes environmental design and reduction of single-use plastics, complementing the adoption of bio-based materials in disposable cups and lids.

Focus on high-performance films with superior barrier properties, IoT-enabled tracking, and dimensional stability is driving innovation in functionality, catering to high-performance applications. Cross-industry collaborations, such as LyondellBasell supplying bio-based PP to Shiseido, exemplify strategies that can be extended to disposable cup manufacturing. The Japanese market continues to innovate with sustainable solutions while maintaining product performance, functionality, and compliance with stringent regulatory policies.

Disposable Cups and Lids Market Report Scope

Disposable Cups and Lids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2034)

|

$26.8 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastic, PLA & Bioplastics, Foam), By Product Type (Cups, Lids), By End-Use (Food Services, Commercial, Institutional, Household), By Application (Hot Beverages, Cold Beverages, Food)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Dart Container Corporation, Berry Global Group, Inc., Pactiv Evergreen Inc., Smurfit Kappa Group plc, Amcor plc, Sonoco Products Company, Graphic Packaging Holding Company, DS Smith plc, WestRock Company, Billerud AB, Uflex Ltd., Genpak LLC, ConverPack Inc., Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Disposable Cups and Lids Market Segmentation

By Material Type

- Paper & Paperboard

- Plastic

- PLA & Bioplastics

- Foam

By Product Type

By End-Use

- Food Services

- Commercial

- Institutional

- Household

By Application

- Hot Beverages

- Cold Beverages

- Food

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Disposable Cups and Lids Market

- Huhtamaki Oyj

- Dart Container Corporation

- Berry Global Group, Inc.

- Pactiv Evergreen Inc.

- Smurfit Kappa Group plc

- Amcor plc

- Sonoco Products Company

- Graphic Packaging Holding Company

- DS Smith plc

- WestRock Company

- Billerud AB

- Uflex Ltd.

- Genpak LLC

- ConverPack Inc.

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to develop a detailed outlook for the Global Disposable Cups and Lids Market, integrating both primary and secondary data to deliver actionable insights for industry professionals. Primary research involved structured interviews with key stakeholders, including packaging manufacturers, quick-service restaurant operators, beverage brands, and sustainability experts, to assess adoption trends, regulatory impact, and technological innovation. Secondary research leveraged company reports, press releases, industry journals, regulatory frameworks, patent filings, and market news to validate market size projections, competitive landscape, and regional dynamics. Quantitative analysis projected market valuation, CAGR, and segmentation by material type, product type, end-use, and application, while qualitative insights focused on sustainability transitions, digital printing adoption, Reusable Cup-as-a-Service (RaaS) models, and compostable polymer innovations. USDAnalytics also evaluated regional policies and government initiatives in the U.S., EU, China, Japan, Brazil, and the U.K., alongside recent M&A activity and technological advancements such as digital watermarking and AI-driven production. This methodology ensures a robust, data-driven perspective for strategic, operational, and investment decisions in disposable cups and lids.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.