Market Overview: Premiumization and Sustainability Drive Cosmetic Packaging Growth

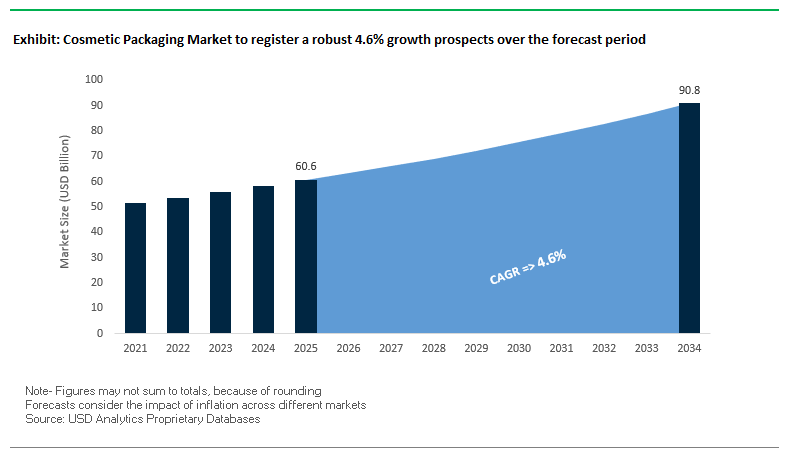

The Global Cosmetic Packaging Market is projected to grow from USD 60.6 billion in 2025 to USD 90.8 billion by 2034, expanding at a CAGR of 4.6%. Unlike traditional packaging markets, cosmetic packaging serves as both a functional necessity and a brand differentiator, with its role extending beyond protection to creating identity, enhancing luxury perception, and engaging consumers directly. This dual function has made cosmetic packaging one of the most dynamic segments in the global packaging industry.

The industry is rapidly evolving, fueled by premiumization, where brands employ glass, metal, and high-end decorative techniques such as embossing, lacquering, and soft-touch finishes to elevate brand appeal. At the same time, refillable and reusable systems are disrupting the single-use model, with luxury brands increasingly offering glass jars, aluminum compacts, and metal lipstick tubes designed for long-term reuse. Circular economy principles are also reshaping the industry, as companies invest in PCR plastics, bioplastics, and recyclable materials such as glass and aluminum. Additionally, the integration of smart packaging features like QR codes and NFC tags is bridging physical products with digital engagement, offering tutorials, authenticity verification, and loyalty programs.

Key Insights for Industry Professionals:

- Market Value: USD 60.6B (2025) → USD 90.8B (2034), CAGR 4.6%.

- Premiumization is driving luxury packaging demand, especially in skincare and fragrance.

- Refillable systems are reshaping sustainability in cosmetics.

- Circular economy focus with PCR plastics, bioplastics, glass, and aluminum.

- Smart packaging adoption supports authentication and digital brand engagement.

Market Analysis: Recent Developments in the Global Cosmetic Packaging Industry

The cosmetic packaging sector has witnessed significant consolidation, sustainability milestones, and product innovations in 2025, reflecting a highly competitive and fast-moving environment.

In August 2025, Albéa Group strengthened its global footprint by acquiring Amfora Packaging, a move aimed at boosting sourcing capabilities and growth in Latin America, a high-potential market for beauty and personal care. In the same year, AptarGroup collaborated with Clarins to launch the ninth generation of Double Serum featuring an eco-designed double-chamber pump system that is fully recyclable, setting a benchmark in premium and sustainable dispensing technology.

In July 2025, Berlin Packaging expanded its European design capabilities by acquiring Cosmei, adding design-forward cosmetic packaging expertise to its portfolio. Meanwhile, in May 2025, the Amcor–Berry Global merger officially closed, creating a global powerhouse in packaging with enhanced closures, flexibles, and rigid container solutions for the cosmetic sector. Also in May, a major cosmetic brand introduced compostable paperboard tubes for lip balms, highlighting innovation in small-format sustainable packaging.

Earlier in April 2025, L’Oréal re-entered dermatology by acquiring a 10% stake in Galderma, signaling growing demand for specialized and premium medical-aesthetic packaging. In March 2025, CSI rebranded to Canopy Beauty Packaging, focusing on PCR-based closures and jars made in the U.S. At the same time, Verescence, a leader in glass fragrance bottles, attracted new investment from Movendo Capital and Draycott, aimed at scaling decarbonization and recycled glass integration.

In February 2025, Chanel launched biodegradable paper pulp containers for select products, showcasing the fusion of luxury and eco-consciousness. These developments highlight how the industry is simultaneously pursuing premium aesthetics, eco-innovation, and digital transformation.

Key Trends and Emerging Opportunities Transforming the Cosmetic Packaging Market

Accelerated Integration of Post-Consumer Recycled (PCR) Materials

One of the most prominent trends reshaping the cosmetic packaging market is the accelerated integration of post-consumer recycled (PCR) materials into primary and secondary packaging formats. Unlike generic “green” marketing claims, this shift is quantifiable and driven by a mix of regulatory mandates and corporate sustainability targets. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective in 2026, sets binding requirements for recycled content in plastic packaging by 2030, making compliance non-negotiable for global beauty brands. Data from industry reports indicates that demand for beauty-grade recycled resins exceeds supply by nearly 60%, creating intense competition among brands for reliable PCR sourcing. Leading players such as Estée Lauder have expanded their refillable portfolio fivefold since 2019, while L’Oréal’s Elvive line now incorporates refill pouches using up to 60% less plastic. However, the adoption of PCR presents challenges around aesthetics and product safety, as issues such as color inconsistencies and black specks are unacceptable in luxury cosmetics. This has triggered major R&D investment in advanced decontamination and sorting technologies, aimed at producing high-quality PCR that maintains brand equity while meeting environmental standards. The result is a powerful structural shift where recyclers, resin suppliers, and beauty brands are forming direct partnerships to secure future-ready material streams.

Adoption of Refillable and Reusable Systems at Scale

Another transformative trend in the cosmetic packaging industry is the mainstream adoption of refillable and reusable systems across skincare, makeup, and fragrance categories. What began as niche, limited-edition packaging is evolving into a core business model for global beauty conglomerates. Consumer demand is a key catalyst, with refillable makeup sales rising sharply in 2022, signaling broad acceptance of durable packaging formats. Brands are responding at scale: L’Oréal’s #JoinTheRefillMovement campaign actively promotes refill pouches and durable outer shells, while beauty retailers in markets such as India are installing in-store refill stations to meet the needs of eco-conscious consumers. For packaging suppliers, this marks a business model shift—from single-use transactions to long-term partnerships where converters supply both durable outer casings and lightweight refill packs. The growth potential is immense, as refillable systems not only reduce material use and plastic waste but also enhance consumer engagement at retail. By creating new touchpoints for interaction, refill stations and reusable formats strengthen brand-consumer loyalty, while simultaneously reshaping value chain dynamics to foster closer collaboration among brands, retailers, and packaging innovators.

Development of Advanced Barrier Coatings for PCR and Monomaterial Plastics

A critical opportunity in the cosmetic packaging sector lies in the development of advanced barrier coatings that enable the use of monomaterial plastics or high-PCR content while maintaining product integrity for sensitive formulations like serums, vitamins, and creams. Historically, these products required multi-material laminates that offered superior oxygen, light, and moisture protection but compromised recyclability. Today, material scientists and chemical companies are creating new barrier solutions that deliver the same level of protection while being compatible with recycling systems. For example, specialized sustainable ionomer grades derived from circular and renewable feedstocks have been launched specifically for cosmetics, allowing brands to transition to sustainable yet high-performance designs. Research is also exploring coatings that can be separated from the base plastic during recycling, improving recovery rates without compromising quality. This is a high-margin growth segment for packaging converters and material innovators, as brands will increasingly demand solutions that resolve the long-standing conflict between functionality and recyclability. Successful adoption requires cross-disciplinary collaboration among scientists, designers, and brand owners, positioning this innovation at the center of a circular cosmetic packaging value chain.

Integration of Digital (QR/NFC) Technology for Authentication and Consumer Engagement

The integration of digital technologies such as NFC tags and unique QR codes represents a game-changing opportunity for the cosmetic packaging market, transforming packaging from a static container into a dynamic platform for authentication, transparency, and consumer engagement. Counterfeit cosmetics cost the global industry billions annually, making secure packaging a priority for premium brands. By embedding QR or NFC features, companies can provide proof of origin, anti-counterfeiting measures, and real-time product tracking. Leading brands are already experimenting with interactive applications: one beauty company used NFC tags to deliver makeup tutorials, while another deployed unique QR codes to disclose ingredient sourcing and sustainability stories, building deeper consumer trust. This also helps combat gray market diversion, as digital identities allow brands to monitor distribution channels and pinpoint unauthorized activity. Beyond security, digital packaging creates an interactive gateway for consumer engagement, offering personalized content, promotions, and tutorials directly via smartphones. This opportunity is redefining the value chain, requiring collaboration between packaging suppliers, technology providers, and brands to create seamless, connected packaging ecosystems. As consumer expectations evolve, digital integration is poised to become a premium differentiator in the cosmetic packaging industry.

Competitive Landscape: Global Leaders in Cosmetic Packaging

The cosmetic packaging market is defined by a balance of large-scale multinationals and specialized innovators, each using sustainability, design, and global reach as competitive levers.

AptarGroup pioneers recyclable dispensing technology

AptarGroup is a global leader in dispensing and active packaging systems, with expertise in high-performance pumps, sprayers, and closures. Its recent innovation, the all-plastic Advance pump, demonstrates its push toward fully recyclable dispensing systems. In partnership with Clarins in July 2025, Aptar introduced an eco-designed double-chamber pump that reinforced its leadership in premium, sustainable solutions. Aptar’s strategy focuses on controlled dosing, material innovation, and consumer experience enhancement, positioning it as a trusted partner for skincare and fragrance brands.

Albéa strengthens Latin American footprint with Amfora acquisition

Albéa Group is among the largest global cosmetic packaging manufacturers, offering tubes, jars, bottles, and dispensing systems. With its 2025 acquisition of Amfora Packaging, Albéa deepened its Latin American presence, strengthening supply networks in a rapidly growing region. The company is committed to making all products recyclable, reusable, or compostable by 2025, with strong emphasis on mono-material, refillable, and low-carbon packaging systems. Its wide portfolio and circular economy focus make Albéa a sustainability-driven market leader.

Amcor expands cosmetic reach through Berry Global merger

Amcor, following its May 2025 merger with Berry Global, has become a dominant force in global consumer packaging, offering an expanded portfolio across flexibles, rigids, closures, and dispensing solutions. Amcor’s integration of Berry brings greater material science expertise and economies of scale, enhancing its ability to deliver sustainable cosmetic packaging solutions. The company reported 3% volume growth in fiscal 2025, reflecting early success in capturing synergies. Its strategy is to leverage its global footprint and expanded product range to support cosmetic brands transitioning to recyclable and reusable formats.

HCP Packaging focuses on luxury aesthetics and sustainability

HCP Packaging specializes in color cosmetics and skincare packaging, producing compacts, palettes, and mascara packs with high-quality finishes such as metallization, lacquering, and stamping. Its focus on PCR plastics and bio-based materials positions it as a sustainability-conscious luxury packaging supplier. Following its acquisition by Carlyle, HCP is scaling globally while maintaining a strong focus on premium design and eco-friendly innovation, making it a preferred partner for high-end beauty brands.

Berlin Packaging expands with Cosmei acquisition

Berlin Packaging operates as a “Hybrid Packaging Supplier,” combining distribution, design expertise, and supply chain services. Its 2025 acquisition of Cosmei expanded its European design-forward packaging portfolio, reinforcing its presence in the cosmetics sector. Berlin offers glass, plastic, and metal containers, catering to both small-batch and large-scale production. Its strategy emphasizes seamless customer experience through design services, engineering, and global sourcing, enabling it to serve a diverse client base from indie startups to multinational cosmetic giants.

Cosmetic Packaging Market Share Insights

Skincare Commands the Largest Market Share by Application in Cosmetic Packaging

Skincare applications account for 40% of the cosmetic packaging market, underscoring how packaging innovation is intrinsically tied to the booming global skincare segment. The rise of premium serums, moisturizers, and wellness-driven formulations has created strong demand for airless bottles, droppers, jars, and high-barrier tubes that preserve sensitive actives like retinol, vitamin C, and peptides. Luxury-focused packaging aesthetics, such as frosted glass jars or metallic finishes, enhance brand perception and consumer experience, justifying higher price points. Regulatory pressures around recyclability and consumer expectations for sustainable beauty also shape this segment, with brands increasingly adopting PCR plastics, refill pods, and lightweight glass designs. Skincare’s commanding share is anchored by both volume and value, making it the dominant force in cosmetic packaging innovation.

Bottles & Jars Maintain Core Market Share by Packaging Type in Cosmetic Packaging

Bottles and jars account for 35% of cosmetic packaging demand, securing their role as the industry’s versatile backbone. These formats are ubiquitous across skincare, haircare, and body care, valued for their ability to accommodate liquid, cream, and gel formulations while offering strong brand customization. Their enduring share reflects a balance of premium aesthetics and functional performance, with brands shifting from PET and PP to high-end glass, PCR-based resins, and hybrid designs that integrate airless dispensing systems to protect sensitive formulations. Bottles and jars are also at the forefront of refillable systems, where durable outer shells are paired with lightweight refill inserts. Their adaptability across mass-market and luxury tiers ensures they remain the cornerstone of cosmetic packaging innovation and sustainability adoption.

United States Cosmetic Packaging Market Transforms Through MoCRA Regulations and Digital Printing Innovations

The United States cosmetic packaging market is undergoing a regulatory transformation driven by the Modernization of Cosmetics Regulation Act of 2022 (MoCRA), effective in late 2023. Stricter requirements for product registration, ingredient safety assessments, and expanded labeling are compelling packaging manufacturers to innovate with traceable codes and adaptable containers. FDA proposals to standardize asbestos testing in talc-based cosmetics further influence packaging compliance.

Technological advancements are reshaping the sector, with digital printing enabling short-run, customizable designs for direct-to-consumer (DTC) brands, reducing waste and supporting personalized product offerings. Corporate investments reflect strong momentum in sustainable and premium packaging, such as Alder Packaging’s partnership with Axilone Group and KKR’s USD 528 million acquisition of a Korean cosmetics packaging company. Key applications span skincare, makeup, and personal care segments, where e-commerce growth drives demand for durable, aesthetically pleasing, and right-sized packaging. Sustainability initiatives include increasing Post-Consumer Recycled (PCR) plastics, exploring glass and aluminum alternatives, and implementing refillable systems to enhance eco-friendly appeal and customer loyalty. Functional innovations, including airless pumps, dropper bottles, and twist-up tubes, enhance user experience while reducing product waste.

Germany Cosmetic Packaging Market Strengthened by PPWR Regulations and Circular Economy Leadership

Germany’s cosmetic packaging industry is navigating a stringent regulatory environment, notably the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. This legislation mandates fully recyclable or reusable packaging by 2030 and sets standards for recycled content while phasing out chemicals like PFAS. Germany’s well-established Extended Producer Responsibility (EPR) system incentivizes brands to design easily recyclable packaging, driving innovations in sorting, materials, and product transparency.

Corporate investments and strategic acquisitions, such as Berlin Packaging’s acquisition of Rixius AG, support expansion in the rigid cosmetic packaging segment. Technological innovation includes machinery capable of handling sustainable materials and digital product passports to enhance traceability. Key applications are strongest in skincare, fragrance, and color cosmetics, where German consumers value high-quality, aesthetically distinctive packaging. Digitalization and automation under “Plattform Industrie 4.0” integrate cyber-physical systems and IoT into manufacturing, improving productivity and operational efficiency.

China Cosmetic Packaging Market Expands Amid Green Transformation and Domestic Manufacturing Drive

China’s cosmetic packaging market is benefiting from governmental initiatives aligned with the “dual carbon” goal, promoting sustainable practices and recycling across the industrial sector. The 2024 Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement encourages the use of sustainable materials in packaging. Regulatory reforms effective September 2023 set limits on packaging layers, void ratios, and costs, directly impacting cosmetic packaging producers.

Technological advancements, including automation, AI, and “5G plus industrial internet” integration, are optimizing production efficiency and flexible manufacturing capacity. Local companies are scaling domestic production to substitute imports, meeting rising demand for high-quality, circular packaging. Rapid growth in e-commerce, skincare, and color cosmetics industries is driving demand, with Chinese manufacturers contributing significantly to innovation through extensive R&D in new materials and production methods.

India Cosmetic Packaging Market Rises with Sustainable Initiatives and Consumer-Centric Innovations

India’s cosmetic packaging industry is being reshaped by government initiatives such as the “Swachh Bharat Abhiyan” and plastic waste management rules, encouraging biodegradable and compostable alternatives. Extended Producer Responsibility (EPR) rules requiring 30% recycled content in rigid plastics by 2025 further support sustainable packaging adoption.

Corporate investments reflect a strong sustainability focus, exemplified by ITC’s use of 70% recyclable plastic for Savlon soap packaging. Technological advancements include automated systems and plastic-free laminate films for wide-ranging applications. Domestic demand is being fueled by the growth of e-commerce and personal care sectors, with brands like The Body Shop Asia South leveraging bold, vibrant packaging to attract Gen Z consumers. Strategic partnerships, such as The CIRCLE Alliance by Unilever, USAID, and EY with a USD 21 million commitment, further promote packaging circularity and reduce plastic waste. Key applications span ready-to-drink beverages, processed foods, and personal care, driving demand for sustainable, high-performance packaging solutions.

Brazil Cosmetic Packaging Market Driven by Regulatory Push and Technological Modernization

Brazil’s cosmetic packaging market is influenced by the National Solid Waste Policy and recent regulations banning single-use disposable items, with a 2030 target for returnable or fully compostable packaging. Technological integration of robotics and AI enhances efficiency, while innovations like biodegradable films using sugarcane-derived carboxymethyl cellulose (CMC) support eco-friendly solutions.

Corporate investments are growing, including Wheaton’s interactive design facility in São Paulo and FINEP-supported projects like Melhoramentos’ R$40 million sustainable cellulose fiber packaging plant. The food, beverage, and cosmetics sectors are major drivers, with packaging solutions designed for both protection and visual appeal. Sustainability remains a central focus, with Brazil’s market rapidly adopting eco-friendly materials and green manufacturing processes, positioning corrugated plastic and glass packaging as preferred alternatives to conventional single-use options.

Japan Cosmetic Packaging Market Innovates Through Bio-Based Materials and High-Performance Designs

Japan’s cosmetic packaging sector is leveraging advanced technologies, particularly bio-polypropylene (bio-PP), to meet sustainability goals. The Plastic Resource Circulation Act, effective April 2022, guides the industry toward reducing single-use plastics and promoting environmentally conscious design, with a target of 2 million tonnes per year of bio-PP by 2030.

The market emphasizes high-performance films with superior barrier properties, IoT integration for real-time tracking, and packaging innovation that enhances functionality, dimensional stability, and product protection. Corporate collaborations, such as LyondellBasell’s incorporation of bio-based PP into Shiseido packaging, and academic research on biopolymers, are driving sustainable and innovative packaging solutions. Japan’s market is distinguished by precision manufacturing and constant innovation, enabling the production of premium cosmetic packaging that meets stringent sustainability and functionality standards.

Cosmetic Packaging Market Report Scope

Cosmetic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$60.6 Billion

|

|

Market Size (2034)

|

$90.8 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Packaging Material (Glass, Plastic, Paper & Paperboard, Metal, Other Materials), By Application (Skincare, Haircare, Makeup, Fragrances, Other Cosmetics), By Packaging Type (Tubes, Bottles & Jars, Cans, Pouches, Sticks, Other Formats)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Smurfit Kappa Group plc, Huhtamaki Oyj, Constantia Flexibles, Sonoco Products Company, DS Smith plc, WestRock Company, Sealed Air Corporation, Silgan Holdings Inc., Berry Global Group, Inc., Ball Corporation, Crown Holdings, Inc., Uflex Ltd., Graphic Packaging Holding Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cosmetic Packaging Market Segmentation

By Packaging Material

- Glass

- Plastic

- Paper & Paperboard

- Metal

- Other Materials

By Application

- Skincare

- Haircare

- Makeup

- Fragrances

- Other Cosmetics

By Packaging Type

- Tubes

- Bottles & Jars

- Cans

- Pouches

- Sticks

- Other Formats

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cosmetic Packaging Market

- Amcor plc

- Mondi Group

- Smurfit Kappa Group plc

- Huhtamaki Oyj

- Constantia Flexibles

- Sonoco Products Company

- DS Smith plc

- WestRock Company

- Sealed Air Corporation

- Silgan Holdings Inc.

- Berry Global Group, Inc.

- Ball Corporation

- Crown Holdings, Inc.

- Uflex Ltd.

- Graphic Packaging Holding Company

* List Not Exhaustive

Methodology

USDAnalytics conducted the Cosmetic Packaging Market study using a robust methodology that integrates both primary and secondary research to provide actionable insights for industry professionals. Primary research included interviews and surveys with key stakeholders such as cosmetic packaging manufacturers, brand owners, design houses, sustainability experts, and supply chain managers to capture market dynamics, emerging trends, and technological adoption. Secondary research analyzed company reports, press releases, regulatory filings, patent databases, industry journals, and trade publications to validate market size, growth projections, and competitive developments. Quantitative analysis was applied to forecast market valuation, CAGR, and segmentation by material, packaging type, and application, while qualitative assessment focused on premiumization, refillable and reusable systems, PCR material adoption, advanced barrier coatings, and smart packaging integration such as QR/NFC technologies. USDAnalytics also evaluated mergers, acquisitions, regulatory frameworks like PPWR and MoCRA, and global sustainability initiatives to deliver a comprehensive, professional-grade market outlook, highlighting both growth opportunities and strategic challenges across regions including the U.S., Germany, China, India, Brazil, and Japan.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.