Market Overview: E-commerce Packaging Scales to $231.5B by 2034 on Unboxing, Returns Mitigation, and Paper-First Sustainability (CAGR 11.6%)

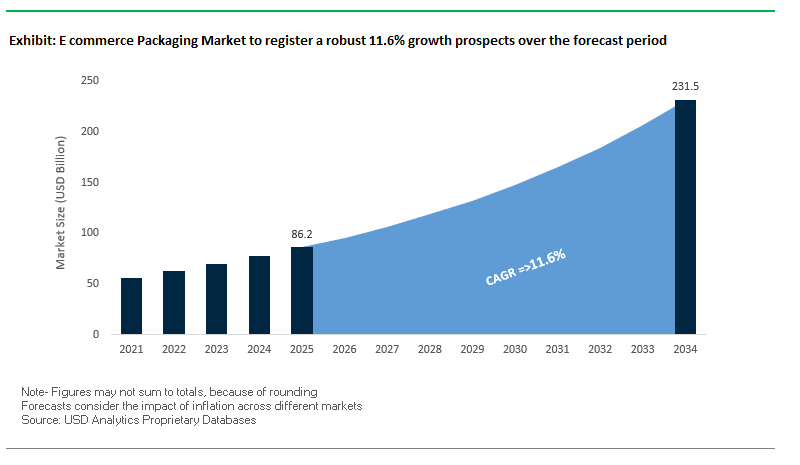

The global e-commerce packaging market is set to expand from $86.2 billion in 2025 to $231.5 billion by 2034, advancing at a robust 11.6% CAGR. As digital retail matures, packaging has shifted from a cost center to a growth lever shaping brand perception, reducing damage-driven returns, and enabling efficient, low-carbon fulfillment. For senior packaging, procurement, and CX leaders, core questions include: how to optimize damage rate vs. material spend, how to design a memorable unboxing without compromising curbside recyclability, and how to deploy automation and right-sizing to cut DIM weight and labor.

Executive insights for industry buyers

- Unboxing as marketing: 65% of consumers will share products on social media when packaging feels gift-like or premium, making structural design and print a top-line growth driver.

- Damage & returns pressure: 50%+ of consumers report receiving damaged items from inadequate packaging, inflating reverse-logistics costs and harming LTV prioritize fit-for-ship designs and certified test protocols.

- Paper preference: 80%+ of U.S. consumers favor cardboard/paper for environmental reasons lean into curbside-recyclable mailers, paper cushions, and mono-material designs.

- Automation for scale: Right-sizing and automated void-fill reduce labor and material, stabilize pack quality, and improve carrier fees via reduced DIM weight.

Market Analysis: Consolidation, Paper-Forward Innovation, and Risk-Adjusted Protection (2024–2025)

Sector consolidation reshapes paper supply and e-com capacity. In October 2024, shareholders approved International Paper’s acquisition of DS Smith, forming a new paper powerhouse that will influence linerboard availability and corrugated e-commerce formats across Europe and North America. In July 2025, Smurfit Kappa and WestRock completed their merger, creating Smurfit WestRock, one of the largest paper-based packaging players globally. These moves enhance access to recyclable, high-performance corrugated, accelerate design libraries for retail-ready unboxing, and strengthen box supply resilience for peak seasons.

Premium categories pull protective performance higher. In August 2025, Orora closed the Saverglass acquisition (≈€1.29B), signaling sustained growth in luxury spirits and beauty segments that demand crush, drop, and vibration-optimized shipper kits and custom molded components. Concurrently, a June 2025 industry report noted 576 containers lost at sea in 2024, exacerbated by Cape of Good Hope reroutes; the headline: risk-adjusted packaging (edge crush, corner protection, shock isolation) must step up for fragile SKUs and long ocean legs serving DTC.

Paper-based alternatives and molded fiber scale. Suppliers continue to launch curbside-recyclable protectives: in September 2024, Pregis introduced EasyPack GeoTerra (wrappable paper cushioning). In November 2024, Dart Container + PulPac brought dry-molded fiber production to North America an enabler for plastic displacement in mailers, inserts, and protective components. A April 2025 consulting report highlighted slower but rising interest in reusable FMCG packaging, nudging pilots for reverse-logistics-ready formats.

Materials breadth via M&A; automation lifts throughput. In February 2025, Berry Global announced a merger with Glatfelter, aligning films and specialty papers for hybrid mailers, coatings, and barrier papers. Automation remains the backbone of profitable e-commerce: on-demand paper, inflatable systems, foam-in-place, and right-size-to-fit machines minimize touches and ensure consistent pack quality at peak.

Trends and Opportunities Defining the Future of the E-Commerce Packaging Market

Rapid Implementation of “Right-Weighting” and Automated Packaging Systems

The e-commerce packaging market is undergoing a transformative shift through the adoption of AI-driven right-weighting and automated packaging systems, which are redefining cost efficiency and material optimization. Retail giants such as Amazon are leading this charge, using AI models and automated box-making systems that dynamically select the smallest viable package for each order. Amazon reported that its Package Decision Engine, launched in 2019, now prevents over 500,000 tons of packaging material from being used each year, a milestone that highlights the scale of this optimization. At the same time, automated machines capable of creating right-sized boxes and poly mailers on demand have reduced packaging weight per shipment by 43% across North America and Europe. Beyond material savings, these systems reduce shipping damage by 24% and cut overall costs by 5%, proving the dual benefit of sustainability and operational efficiency. For e-commerce players operating under thin margins and immense pressure during seasonal peaks, automation is no longer an option but a strategic imperative that ensures faster throughput, optimized dimensional weight charges, and a reduced carbon footprint across global operations.

Strategic Shift Towards Reusable and Returnable Packaging Systems for B2B and B2C

The growing consumer backlash against single-use plastics is accelerating the adoption of reusable and returnable packaging solutions, reshaping the market from a disposable model to a packaging-as-an-asset ecosystem. Pilot programs in the fashion industry, backed by Fashion for Good, demonstrated that reusable systems can reduce carbon emissions by 82% and plastic waste by 87%, offering a quantifiable advantage over single-use corrugated or plastic mailers. Companies like Repax are pioneering the “Packaging-as-a-Service” model, which covers the full lifecycle of containers including collection, cleaning, and redistribution, thereby easing adoption for retailers. Consumer sentiment strongly supports this trend, with a 2024 survey showing that 73% of consumers recognize the environmental benefits of reusable packaging, though adoption lags due to lack of convenience. To address this gap, market leaders are building reverse logistics networks, incentivized return schemes, and digital tracking systems that make reusables viable at scale for both B2B and B2C channels. This shift has the potential to revolutionize e-commerce packaging by reducing waste and creating service-based revenue streams around packaging management.

Development of Performance-Enhanced, Curbside-Recyclable Flexible Mailers

As the shift from corrugated boxes to lightweight flexible mailers becomes mainstream, the industry faces the challenge of creating solutions that are both high-performing and widely recyclable. The opportunity lies in the commercialization of curbside-recyclable mono-material plastic films and paper-based mailers that can withstand the rigors of automated fulfillment while aligning with sustainability mandates. Paper-based mailers designed for automated bagging systems are increasingly being adopted, with companies like PAC Machinery launching recyclable paper solutions suitable for direct substitution of traditional poly mailers. In plastics, mono-material polyolefin mailers from groups like Mondi have achieved recyclability ratings of up to 93% from cyclos-HTP, demonstrating that high durability and environmental responsibility can coexist. Success will depend on consumer-friendly recycling pathways such as How2Recycle®-labeled mailers that offer clear disposal instructions and integrate seamlessly into existing recycling systems. For brands, adopting such solutions not only improves environmental credentials but also strengthens consumer loyalty by aligning with buyer expectations for sustainable e-commerce packaging.

Integration of Embedded Digital Technology for Supply Chain and Marketing

E-commerce packaging is evolving beyond protection to become a digital engagement and supply chain intelligence platform, opening new frontiers in both operational efficiency and consumer interaction. The integration of digital watermarks, QR codes, and NFC chips provides multifaceted benefits. For consumers, connected packaging offers a direct gateway to brand ecosystems whether through loyalty rewards, ingredient transparency, or immersive AR experiences with studies showing 43% of consumers already use QR codes to access product information. For brands, NFC tags with unique IDs offer robust anti-counterfeiting solutions, especially for luxury goods where authenticity validation is critical. On the logistics side, digital identifiers allow real-time inventory tracking and predictive data analytics, empowering manufacturers and retailers to reduce shrinkage and streamline distribution. As digital-first retail continues to expand, packaging that doubles as a data carrier and marketing channel is set to become a defining competitive differentiator, turning every shipped box or mailer into a touchpoint for engagement, trust, and operational intelligence.

Competitive Landscape: Leaders in Paper Systems, Protective Automation, and Experience-Led Design

A mix of integrated paper majors and protective-pack innovators competes on sustainability, total cost of fulfillment, damage-rate reduction, and unboxing aesthetics. Winning programs blend corrugated engineering, automation, and consumer-ready branding.

Smurfit WestRock Paper-Based E-commerce Systems Optimized for DIM and CX

Smurfit WestRock (formed July 2025) delivers custom e-commerce boxes, inserts, dividers, and pads that manage shock and vibration while elevating the unboxing experience. With integration from sustainably managed forests to finished packaging, it offers quality control and speed to market. The company’s sustainable focus prioritizes void reduction and dimensional-weight savings; high-graphics options and its Design2Market methodology streamline concept-to-launch, reducing cycle time for seasonal and DTC programs.

Sealed Air Corporation Automation-Led Protective Packaging with Recyclable Options

Sealed Air’s portfolio spans Instapak® foam-in-place, Bubble Wrap® brand cushioning, and on-demand paper systems, enabling custom-conforming protection for fragile and high-value goods. Recent investments center on automated void-sensing and paper-insertion to standardize pack quality at scale. New paper bubble mailers and recycled inflatable bubbles (up to 80% recycled content) underscore its sustainability roadmap while preserving throughput and pack integrity in high-volume fulfillment centers.

Pregis LLC Curbside-Recyclable Cushioning and Total-Cost Optimization

Pregis offers AirSpeed® inflatable, Easypack® on-demand paper, and foam-in-place systems, tightly integrated with analytics and automation. Its EverTec™ cushioned mailer and EasyPack GeoTerra paper extend curbside-recyclable options with a clean, brandable aesthetic. Pregis differentiates with a Total Cost of Ownership mindset right-sizing SKUs, swapping carton-to-mailer where viable, and deploying EcoGauge assessments to map damage, labor, and material savings alongside carbon reductions.

DS Smith Circular Design, Transit Testing, and Collaborative Development

Now part of International Paper (Oct 2024), DS Smith brings a circular business model and deep supply-cycle analysis to e-commerce programs. With 700+ designers and its DISCS test methodology (Drop, Impact, Shock, Crush, Shake), DS Smith tailors boxes and inserts for verified protection. PackRight and Impact Centres let customers co-create and simulate solutions end-to-end from warehouse flow to doorstep cutting damage and speeding commercialization of unboxing-optimized designs.

Ranpak Holdings Corp. Paper-Only In-the-Box Automation for Speed and Sustainability

Ranpak focuses exclusively on paper-based protective systems, including FillPak® (void fill), PadPak® (cushioning), and Geami® (die-cut wrap) with proprietary converters placed at pack stations. Its Cut’it!™ EVO automates height reduction and box closing (up to ~15 boxes/min), trimming DIM weight and improving trailer density. Pad’it!™ automates paper-pad insertion, lowering labor and variability while maintaining a fully curbside-recyclable inside-the-box experience that consumers prefer.

E-commerce Packaging Market Share Insights

Boxes, Mailers, and Protective Solutions Shape E-Commerce Packaging Market Share by Format

By 2025, boxes and cartons dominate the e-commerce packaging market with 40% share, followed closely by mailers and envelopes at 30%, while protective packaging, labels and closures, and specialty formats account for the remainder. Boxes and cartons maintain leadership due to their structural strength, versatility, and ability to deliver a premium unboxing experience, with innovations such as right-sizing and lightweight fluting reducing shipping costs and material usage. Mailers and envelopes, meanwhile, are the fastest-growing segment, winning share through lightweight efficiency and sustainability, as recyclable paper-based and compostable alternatives replace conventional poly mailers. Protective packaging remains indispensable for damage prevention in electronics, homeware, and fragile goods, with the shift toward paper-based void fill strengthening sustainability credentials. Labels, tapes, and closures, though smaller in share, underpin logistics efficiency through secure sealing and automation compatibility, increasingly adopting recyclable water-activated tapes. Specialty packaging, while niche, is a powerful differentiator for premium brands in cosmetics, subscription boxes, and luxury goods, where unboxing drives loyalty and social media visibility. Collectively, this segmentation underscores a dual market dynamic: cost efficiency and logistics on one hand, and consumer experience and sustainability on the other.

Fashion, Electronics, and Beauty Lead Market Share by E-Commerce End-Use Industry

On the end-use side, fashion and apparel lead the e-commerce packaging market with 28% share in 2025, closely trailed by consumer electronics at 25%, with home & living, food & beverages, and personal care & cosmetics forming the balance. Fashion and apparel dominate due to the sheer frequency of online purchases and high return volumes, favoring flexible mailers and return-friendly packaging designs. Consumer electronics drive value share with sophisticated corrugated boxes and protective inserts designed for premium positioning and damage prevention. Home & living spans a diverse product mix from décor to furniture, demanding strength-optimized and right-sized cartons for bulky shipments. Food and beverages are rapidly scaling, with insulated liners, gel packs, and compliant formats addressing perishability and regulatory needs. Personal care and cosmetics elevate packaging into a brand identity tool, using custom boxes and premium mailers to enhance unboxing and justify higher price points. Together, these industries shape the innovation trajectory of e-commerce packaging, balancing operational functionality with consumer-facing differentiation.

United States: Personalized and Sustainable E-commerce Packaging Drives Market Leadership

The U.S. e-commerce packaging market is a global leader, propelled by the country’s expansive online retail sector. Brands are increasingly adopting digital printing on packaging to deliver personalized and memorable unboxing experiences, enhancing brand loyalty and differentiation. Sustainability is a key focus, with companies shifting toward lightweight, recyclable, paper-based, biodegradable, and compostable materials, including post-consumer resins (PCR) and polylactic acid (PLA), to meet environmental goals and consumer expectations.

The surge in fragile goods e-commerce, such as electronics and glass products, has driven demand for protective and smart packaging solutions. Integration of QR codes and RFID tags improves supply chain visibility, authenticity, and customer engagement. Strategic partnerships between packaging suppliers and e-commerce companies are streamlining logistics, while the adoption of AI-driven automated packaging processes enhances operational efficiency and reduces labor costs.

Germany: EU Regulations and Circular Economy Propel Sustainable Packaging Solutions

Germany’s e-commerce packaging market is shaped by stringent European Union regulations, including the Packaging and Packaging Waste Regulation (PPWR) effective February 2025. These rules limit empty space in parcels to 40%, encouraging the adoption of right-sized, efficient packaging solutions. The country’s focus on the circular economy drives the development of packaging with high recycled content and reusable systems, ensuring compliance and environmental responsibility.

Innovation in paper-based packaging solutions is a major trend, as German companies lead in reducing plastic usage. For example, Mondi has developed cost-effective, recyclable paper bags that enhance the unboxing experience while aligning with sustainability targets. German marketplaces also require sellers to register packaging and participate in dual recycling systems, creating opportunities for companies that prioritize eco-friendly and compliant solutions.

China: High-Volume E-commerce and Sustainability Initiatives Drive Packaging Evolution

China’s e-commerce packaging market is defined by massive domestic volume and export-oriented demand. Platforms like Alibaba and JD.com require a consistent supply of packaging materials for domestic and international shipping. The government’s push to ban single-use, non-degradable plastic packaging by 2025 has accelerated the adoption of sustainable alternatives, including reusable packaging solutions.

E-commerce giants are investing in shared and reusable packaging, such as JD.com’s 1.5 million reusable express boxes, reducing environmental impact and aligning with national sustainability goals. The market is also leveraging smart logistics and data analytics to optimize packaging sizes, reduce waste, and lower shipping costs, creating a more efficient and eco-friendly e-commerce supply chain.

India: Rapid E-commerce Growth and Government Policies Stimulate Packaging Innovation

India’s e-commerce packaging market is witnessing exponential growth, fueled by rising digital adoption, a growing middle class, and the expansion of online retail across sectors such as electronics, fashion, and food. Government bans on certain single-use plastics have catalyzed a shift toward sustainable materials and innovative packaging solutions.

The increasing sale of high-value and fragile products has amplified the demand for protective packaging, including air pillows, molded pulp, and cushioning materials. Domestic manufacturers are expanding production capacities, particularly for corrugated boxes, which remain the largest and fastest-growing segment. Investments in local manufacturing ensure that India meets the rising demand for cost-effective, durable, and eco-friendly e-commerce packaging solutions.

Japan: High-Quality Presentation and Sustainable Packaging Define Market Trends

Japan’s e-commerce packaging market emphasizes product presentation, quality, and the consumer unboxing experience. There is strong demand for packaging that is not only protective but also aesthetically pleasing and easy to open, reflecting Japan’s focus on consumer satisfaction and premium product handling.

Sustainability is a growing priority, with innovations in eco-friendly, paper-based packaging and reduced material thickness to lower the carbon footprint of shipped products. Compliance with strict customs and labeling regulations is critical for international shipments, prompting Japanese companies to focus on correct packing, labeling, and sustainable solutions that ensure smooth cross-border logistics.

E commerce Packaging Market Report Scope

E commerce Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$86.2 Billion

|

|

Market Size (2034)

|

$231.5 Billion

|

|

Market Growth Rate

|

11.6%

|

|

Segments

|

By Material Type (Corrugated Board, Plastic, Paper & Paperboard, Flexible Films & Mailers, Bioplastics, Other Materials), By Packaging Format (Boxes and Cartons, Mailers and Envelopes, Protective Packaging, Labels Tapes and Closures, Specialty Packaging), By End-Use Industry (Consumer Electronics, Fashion and Apparel, Food and Beverages, Personal Care & Cosmetics, Home & Living, Other End-Users)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Amcor plc, DS Smith Plc, Mondi Group, Sealed Air Corporation, Smurfit Kappa Group Plc, Sonoco Products Company, WestRock Company, Georgia-Pacific LLC, Huhtamaki Oyj, BillerudKorsnäs AB, Rengo Co., Ltd., Greif, Inc., Shurtape Technologies, LLC, Pregis LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

E-commerce Packaging Market Segmentation

By Material Type

- Corrugated Board

- Plastic

- Paper & Paperboard

- Flexible Films & Mailers

- Bioplastics

- Other Materials

By Packaging Format

- Boxes and Cartons

- Mailers and Envelopes

- Protective Packaging

- Labels Tapes and Closures

- Specialty Packaging

By End-Use Industry

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Personal Care & Cosmetics

- Home & Living

- Other End-Users

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in E commerce Packaging Market

- International Paper Company

- Amcor plc

- DS Smith Plc

- Mondi Group

- Sealed Air Corporation

- Smurfit Kappa Group Plc

- Sonoco Products Company

- WestRock Company

- Georgia-Pacific LLC

- Huhtamaki Oyj

- BillerudKorsnäs AB

- Rengo Co., Ltd.

- Greif, Inc.

- Shurtape Technologies, LLC

- Pregis LLC

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the evolving dynamics, growth drivers, and technological breakthroughs shaping the global e-commerce packaging market. The analysis reviews historical trends from 2021 to 2024 and provides forward-looking forecasts up to 2034, highlighting opportunities across automation, sustainable material adoption, and consumer-centric design. This report emphasizes performance-optimized and curbside-recyclable packaging solutions, digital integration for supply chain visibility, and innovations in reusable and returnable systems. It highlights strategic mergers, material diversification, and market consolidation trends that influence global supply chains, operational efficiency, and brand experience. By exploring protective performance, cost-optimization, automation adoption, and eco-conscious packaging, this report is an essential resource for packaging engineers, procurement leaders, CX strategists, and sustainability officers seeking actionable insights and competitive intelligence in a rapidly transforming e-commerce environment.

Scope Highlights:

- Segmentation: By Material Type (Corrugated Board, Plastic, Paper & Paperboard, Flexible Films & Mailers, Bioplastics, Other Materials); By Packaging Format (Boxes and Cartons, Mailers and Envelopes, Protective Packaging, Labels, Tapes and Closures, Specialty Packaging); By End-Use Industry (Consumer Electronics, Fashion and Apparel, Food & Beverages, Personal Care & Cosmetics, Home & Living, Other End-Users)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: Historic data from 2021–2024; forecast from 2025–2034.

- Companies Covered: Profiles and analysis of 15+ companies including International Paper Company, Amcor plc, DS Smith Plc, Mondi Group, Sealed Air Corporation, Smurfit Kappa Group Plc, Sonoco Products Company, WestRock Company, Georgia-Pacific LLC, Huhtamaki Oyj, BillerudKorsnäs AB, Rengo Co., Ltd., Greif, Inc., Shurtape Technologies, LLC, Pregis LLC.

Methodology

The study employs a multi-layered research methodology combining primary and secondary data to deliver a comprehensive market assessment. Primary research involved interviews with packaging engineers, supply chain managers, procurement officers, and senior executives from leading e-commerce and logistics companies to capture insights on automation, sustainability, and design preferences. Secondary research drew from annual reports, press releases, regulatory filings, company websites, trade journals, and specialized databases to validate historical trends and competitive positioning. Quantitative analysis included market sizing, CAGR calculations, and material- and format-specific adoption rates, while qualitative evaluation focused on consumer behavior, unboxing trends, return rates, and ESG compliance initiatives. USDAnalytics integrates triangulation, data normalization, and expert validation to ensure accuracy, while predictive modeling projects the market evolution up to 2034, enabling decision-makers to identify emerging opportunities and optimize resource allocation in a highly dynamic e-commerce packaging landscape.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.