Collation Shrink Films Market Overview: Growth to $7 Billion by 2034

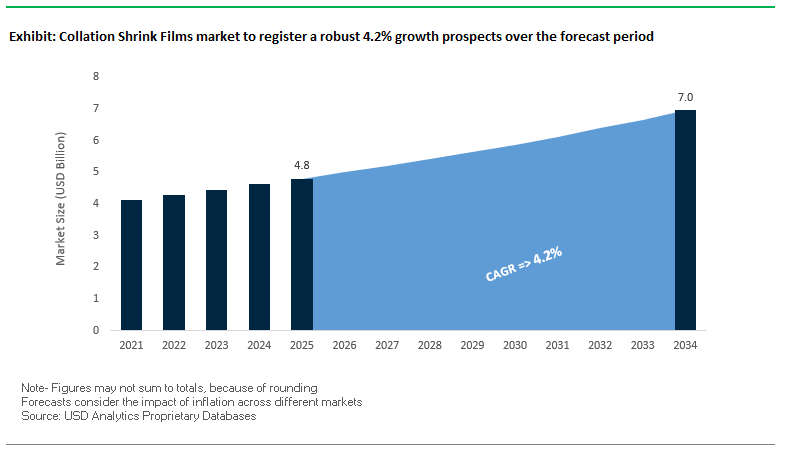

The global collation shrink films market is projected to reach $4.8 billion in 2025 and expand to $7.0 billion by 2034, growing at a CAGR of 4.2%. This market plays a vital role in modern packaging, offering efficient bundling, secure transportation, and enhanced branding for multipack goods. Industry professionals increasingly view collation shrink films as both a functional packaging medium and a brand communication tool, particularly in sectors such as food, beverages, healthcare, and e-commerce. The central questions driving the industry are: How will downgauging and PCR integration transform production economics? How will regulatory and consumer shifts toward sustainability influence demand? And how will digital printing reshape retail visibility?

Key Insights include:

- Downgauging and Lightweighting: Collation shrink films as thin as 10 microns are now commercially available, cutting material use without compromising performance.

- Recycled Content Integration: Leading players are achieving up to 100% PCR content in non-food shrink films, advancing circular economy goals.

- E-commerce Applications: Shrink films are increasingly used for tamper-evident protection in online retail shipments, ensuring product security in transit.

- Printing and Branding: Over 70% of brand owners leverage high-definition printed films to enhance shelf visibility and consumer engagement.

As consumer goods brands demand cost efficiency, sustainability, and premium branding, collation shrink films are evolving from utility packaging into a strategic growth driver in global packaging systems.

Market Analysis: Sustainability, Tariffs, and AI Driving Strategic Shifts

The collation shrink films market is being reshaped by sustainability imperatives, geopolitical trade measures, and digital transformation. Industry stakeholders are navigating new pressures while innovating to meet customer and regulatory expectations.

In August 2025, an industry publication highlighted the impact of U.S. tariffs on PET shrink films, forcing packaging companies to recalibrate sourcing strategies and expand domestic capacity. Also in August, RKW Group partnered with Dow to launch collation shrink films made from household waste-derived PCR plastics, a significant milestone in recycling contaminated waste streams for high-performance applications.

In July 2025, a global logistics summit spotlighted the growing use of AI and predictive analytics for demand forecasting and inventory optimization in shrink film supply chains. That same month, reports confirmed growing demand for recyclable, lightweight shrink films for multipack beverages, supported by advances in downgauging technologies.

Earlier, in May 2025, Sonoco divested its thermoformed and flexible packaging business to TOPPAN Holdings, sharpening its focus on higher-value packaging sectors. In April 2025, a shift toward paper- and cartonboard-based alternatives was noted, reflecting consumer preference for eco-friendly multipacks, a competitive challenge to plastic-based shrink films.

Back in March 2025, a leading manufacturer announced thinner, co-extruded shrink films offering both strength and material savings, reducing carbon emissions across supply chains. In January 2025, Dow and Plastigaur launched a resin with 70% recycled plastic, enabling downgauging while cutting carbon emissions by 25%.

Emerging Trends and Opportunities Reshaping the Collation Shrink Films Market

Accelerated Adoption of High-Performance PE Films to Replace PVC and POF

The collation shrink films market is undergoing a structural material transformation, as polyethylene (PE) and polyolefin (POF)-based films replace traditional PVC films. This transition is being driven by mounting regulatory pressure, brand-owner sustainability goals, and superior technical performance of PE. Unlike PVC, which releases toxic substances during incineration or recycling, PE is widely recyclable and aligns with circular economy objectives.

Corporate sustainability initiatives are accelerating this shift. For example, Dow has launched advanced resins that enable collation shrink films with up to 70% post-consumer recycled polyethylene while retaining excellent optical and mechanical strength. This not only meets corporate ESG commitments but also helps global brands comply with new Extended Producer Responsibility (EPR) regulations. The European Union’s Packaging and Packaging Waste Regulation (PPWR) is central to this change, effectively phasing out hard-to-recycle materials like PVC by 2030, while national legislations in markets like India and the U.S. further reinforce the move toward recyclable plastics.

Beyond compliance, performance advantages are strengthening PE’s dominance. Unlike PVC, which becomes brittle in cold conditions, polyolefin films retain flexibility at temperatures as low as -50°C (-58°F), making them indispensable in frozen food packaging and cold chain applications. This performance edge ensures that brand owners benefit not only from regulatory compliance but also from improved product protection and consumer satisfaction.

Integration of Digital Watermarks for Advanced Sorting and Circularity

The recyclability of shrink films has long been challenged by sorting inefficiencies at material recovery facilities. To address this, the industry is embracing digital watermarking technologies that enhance recycling accuracy and generate higher-quality PCR (post-consumer recycled) streams. The HolyGrail 2.0 Initiative, led by the European Brands Association (AIM), has demonstrated that invisible digital watermarks embedded into packaging artwork can carry detailed compositional data. High-resolution cameras on sorting lines decode these watermarks, allowing near-perfect identification of material types. Recent trials showed a 99% detection rate and 95% ejection rate for flexible packaging, including collation shrink films, proving the technology’s ability to drive circularity. By enabling more granular sorting, this innovation ensures that shrink films can be efficiently recycled alongside compatible materials, reducing contamination rates and creating a more robust supply of high-quality recycled resins. As consumer brands and retailers commit to ambitious recycling targets, watermark-enabled films are emerging as a cornerstone technology for advancing the circular plastics economy.

Development of High-Recycled Content (PCR) Films Without Compromising Performance

The next growth frontier lies in scaling high-PCR-content shrink films that deliver the same performance as virgin-material counterparts. While incorporating recycled content typically reduces mechanical strength, recent breakthroughs in polymer blending and resin engineering have created new possibilities. For example, a collaboration between ExxonMobil and Windmöller & Hölscher produced a 40µm collation shrink film with 50% PCR content that maintained critical properties like puncture resistance and dart impact strength. Similarly, Trioworld’s Loop Collation shrink film, with 30–95% recycled content, allows brand owners to meet sustainability commitments without compromising shelf appeal or stability. This opportunity is being amplified by corporate sustainability targets and regulatory mandates requiring packaging to contain a minimum percentage of recycled material. By developing films that balance mechanical integrity, print quality, and recyclability, manufacturers can directly address the dual challenge of performance and circularity, positioning themselves as preferred suppliers to global consumer brands.

Innovation in E-commerce-Optimized, Protective-Durable Shrink Films

With the exponential growth of e-commerce, collation shrink films are being re-engineered to meet the unique demands of online retail. Unlike traditional retail distribution, e-commerce involves multiple handling stages, making durability, load stability, and aesthetics equally critical. New formulations of shrink films provide dual functionality, serving both as product bundling solutions and as protective layers during transit. This reduces reliance on corrugated boxes or foam inserts, cutting packaging costs and lowering shipping weights. Additionally, enhanced puncture and tear resistance ensures fewer product damages, directly reducing return rates and improving customer satisfaction. Brands are also using shrink films as a marketing canvas, with innovations in high-gloss finishes and full-color printability elevating the “unboxing experience”—a critical differentiator for direct-to-consumer (DTC) brands. At the same time, improved holding force and load stability minimize product shifting in transit, addressing one of the biggest challenges in e-commerce logistics. By integrating protective durability with branding potential, e-commerce-optimized shrink films present one of the most commercially promising growth opportunities in the next decade.

Competitive Landscape: Key Players Driving the Collation Shrink Films Market

The global collation shrink films market features multinational leaders and specialized innovators. Each company is advancing sustainable solutions, downgauging technologies, and branding-focused printing to strengthen their competitive edge.

Amcor Plc pioneers recycled-content shrink films

Amcor leverages its global footprint to deliver eco-friendly collation shrink films with verifiable recycled content. Its strategic focus on RPETG shrink films supports brand owners’ sustainability goals while ensuring high clarity and durability. Amcor collaborates with FMCG companies to design customized solutions, transforming shrink films into a retail branding tool. Its recent expansion in Costa Rica’s healthcare packaging sector highlights its strategy of targeting high-growth regions.

Berry Global Group, Inc. develops high-performance RPETG shrink films

Berry Global’s strength lies in high-performance flexible packaging with a strong emphasis on process efficiency and print compatibility. Its vertically integrated approach ensures quality from resin sourcing to finished films. Berry is actively innovating with RPETG shrink films, designed for food, healthcare, and industrial goods. Its investments in digital printing compatibility allow brands to integrate dynamic visuals and QR-enabled consumer engagement directly into shrink packaging.

Sealed Air Corporation integrates smart packaging features

Sealed Air, through its Cryovac brand, offers shrink films engineered for aesthetics, durability, and sustainability. Its products are widely used in food and beverage multipacks, offering tamper-evidence and protection during logistics. The company is driving innovation in smart packaging features, including QR codes and NFC-enabled shrink films for enhanced consumer interaction and supply chain traceability. Sealed Air remains a leader in premium, high-clarity shrink solutions.

Dow Inc. enables circular solutions with advanced resins

Dow plays a critical role as a materials science leader, supplying advanced resins to converters worldwide. Its REVOLOOP recycled resins—with up to 100% PCR content—are shaping the future of collation shrink films. In partnership with RKW Group, Dow is advancing circular packaging solutions derived from household waste streams. With a target to commercialize 3 million metric tons of circular and renewable solutions by 2030, Dow is a key enabler of the industry’s sustainability transition.

Collation Shrink Films Market Share Insights

LLDPE Leads Market Share by Material in Collation Shrink Films

Linear Low-Density Polyethylene (LLDPE) dominates the collation shrink films market with a 55% share in 2025, establishing itself as the industry’s go-to material for high-volume bundling applications. Its superiority lies in its tensile strength, puncture resistance, and downgauging capability, which allows thinner films to deliver equivalent performance while reducing material usage and waste—key benefits in cost-sensitive industries like food and beverage. These properties make LLDPE indispensable in automated high-speed palletizing lines and consumer multipack packaging. Polyolefin (POF), holding 25% of the market, is the premium choice where visual appeal and high gloss presentation are critical, particularly in consumer electronics, retail goods, and branded promotions. Its higher sealing strength and superior clarity justify its cost premium in markets where shelf appeal drives sales. LDPE and polypropylene (PP) retain niche roles, with LDPE sustained mainly by legacy machinery and PP serving applications requiring higher rigidity or moisture resistance, though both lack the performance advantages of LLDPE. Other polymers such as MDPE and HDPE are used sparingly, filling specific requirements for stiffness, balance, or sealing ease. This material segmentation reflects a clear hierarchy where LLDPE leads on efficiency and performance, while POF grows in value-driven, brand-sensitive applications.

Food & Beverage Remains the Volume Titan in End-Use Market Share

The food and beverage sector drives 40% of the global collation shrink films market in 2025, making it the largest end-use industry by volume. The need to unitize multipacks of soda cans, bottled water, snack packs, and yogurt containers ensures a constant demand for high-strength, low-cost LLDPE films. Promotional bundling further reinforces its dominance, as brands seek efficient and durable packaging for mass-market distribution. Consumer goods account for 25% of market demand, leveraging shrink films for everything from toys and stationery to hardware. This segment relies heavily on POF films due to their superior clarity, seal strength, and ability to enhance retail presentation while protecting products from tampering and pilferage. Beverages as a sub-segment are particularly influential, as the bundling of water bottles and carbonated soft drinks creates some of the highest, most consistent demand for LLDPE, with performance requirements focused on load stability and preventing unit separation. Personal care and home care industries depend on shrink films for heavy, unstable products such as shampoo bottles and detergent packs, where the emphasis is on durability and secure load stabilization during transportation. Pharmaceutical and healthcare applications form a smaller but critical niche, where shrink films are used to bundle bottles, hospital kits, or medical supplies under strict GMP compliance, prioritizing material consistency and reliability. Collectively, these end-use patterns demonstrate how collation shrink films balance performance, cost-efficiency, and presentation across industries, with food, beverage, and FMCG segments continuing to anchor global demand.

United States: Sustainability and Technological Innovation Driving Collation Shrink Films

The United States collation shrink film market is being shaped by a strong emphasis on sustainability and circular economy practices. Companies such as NOVA Chemicals are pioneering resins made from 100% post-consumer recycled (PCR) polyethylene, enabling the production of eco-friendly shrink films. This shift addresses growing consumer and brand demand for sustainable packaging while reducing the environmental footprint of multi-pack and retail-ready packaging.

Strategic expansions and mergers and acquisitions are also influencing market dynamics, as leading manufacturers aim to enhance production capabilities, diversify product portfolios, and strengthen market presence. Innovations in multi-layer shrink film technology are reducing material usage while maintaining durability, clarity, and protection for bundled goods. The growth of e-commerce and retail sectors further fuels demand, as collation shrink films provide cost-effective, lightweight, and protective solutions for transporting consumer products through complex supply chains.

Germany: Circular Economy Leadership and Collaborative Innovations in Shrink Films

Germany stands out as a pioneer in circular economy solutions for collation shrink films, largely influenced by the European Green Deal and national sustainability initiatives. The country is driving innovation with high-recycled-content films that are designed for recyclability, reflecting growing regulatory pressure under the EU Packaging and Packaging Waste Regulation (PPWR).

Collaborations between companies like Borealis, Freiberger, and alesco have resulted in award-winning shrink films with 65% PCR content and a 45% reduction in CO₂ footprint, demonstrating Germany’s commitment to eco-efficient manufacturing. The focus remains on developing B2B-grade films that are compliant with regulatory frameworks while supporting sustainability goals, making Germany a benchmark market for environmentally conscious collation shrink film solutions.

China: Industrial Scale and Branding Innovations Fuel Market Expansion

China’s collation shrink film market is driven by the country’s massive industrial and consumer goods sectors, particularly in the food and beverage industry. The need for efficient bundling and transport of products at scale has made shrink films a critical solution for logistics, distribution, and retail-ready packaging.

To meet high-volume demand, manufacturers are investing heavily in automation and advanced extrusion machinery, improving efficiency and reducing production costs. Beyond functional use, collation shrink films are increasingly leveraged as a branding and marketing tool, with high-quality printed films featuring vibrant graphics for enhanced product visibility. This dual focus on efficiency and brand promotion is positioning China as a dominant player in both domestic and global collation shrink film markets.

India: Food & Beverage Growth and Sustainability Driving Domestic Demand

India’s collation shrink film market is expanding rapidly alongside the country’s food and beverage sector, fueled by rising disposable incomes and evolving consumer habits. These films are essential for bundling water bottles, packaged goods, and other retail items efficiently, while maintaining product protection.

Government initiatives promoting a circular economy and regulations on plastic waste are encouraging the development of recyclable and durable shrink films. Domestic manufacturers like Tilak Polypack and Amcor Flexibles India are expanding production capacities to meet both local and international demand, supported by the "Make in India" initiative. Advanced production technologies are being adopted to produce films with varying specifications, thicknesses, and print options, allowing manufacturers to cater to a broad spectrum of industrial and retail requirements.

France: Regulatory Compliance and Material Efficiency Enhancing Market Growth

France’s collation shrink film market is strongly influenced by EU regulations on plastic packaging and anti-waste laws, which promote circular economy practices. Manufacturers are focusing on creating films that comply with stringent legal requirements while maintaining performance and durability for bundling and packaging applications.

Material innovation is a key trend, with companies developing thinner, high-performance films that reduce material usage without compromising strength or product protection. These advancements allow French manufacturers to meet sustainability goals, minimize waste, and provide reliable packaging solutions for industrial, retail, and e-commerce applications, reinforcing the country’s position as a progressive market in collation shrink films.

Collation Shrink Films Market Report Scope

Collation Shrink Films market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Material Type (Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE), Medium-Density Polyethylene (MDPE), High-Density Polyethylene (HDPE), Polypropylene (PP), Polyolefin (POF), Other Polymers), By End-Use Industry (Food & Beverage, Consumer Goods, Personal Care & Home Care, Pharmaceuticals & Healthcare, Transport & Logistics, Printing & Publications, Other Applications), By Thickness (Below 25 microns, 25–50 microns, 50–100 microns, Above 100 microns), By Application (Bottles, Cans, Cartons & Boxes, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Dow Inc., ExxonMobil Corporation, Sealed Air Corporation, Nova Chemicals Corporation, Mondi plc, AEP Industries Inc., DuPont de Nemours, Inc., WestRock Company, RKW Group, Coveris Holdings SA, Bolloré, Tilak Polypack, Plastigaur

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Collation Shrink Films Market Segmentation

By Material Type

- Low-Density Polyethylene

- Linear Low-Density Polyethylene

- Medium-Density Polyethylene

- High-Density Polyethylene

- Polypropylene

- Polyolefin

- Other Polymers

By End-Use Industry

- Food & Beverage

- Consumer Goods

- Personal Care & Home Care

- Pharmaceuticals & Healthcare

- Transport & Logistics

- Printing & Publications

- Other Applications

By Thickness

- Below 25 microns

- 25–50 microns

- 50–100 microns

- Above 100 microns

By Application

- Bottles

- Cans

- Cartons & Boxes

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Collation Shrink Films market

- Amcor plc

- Berry Global Inc.

- Dow Inc.

- ExxonMobil Corporation

- Sealed Air Corporation

- Nova Chemicals Corporation

- Mondi plc

- AEP Industries Inc.

- DuPont de Nemours, Inc.

- WestRock Company

- RKW Group

- Coveris Holdings SA

- Bolloré

- Tilak Polypack

- Plastigaur

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global collation shrink films market, highlighting recent breakthroughs in material innovation, recycled content integration, and e-commerce-ready protective solutions. The analysis reviews market trends from 2021 to 2024 and provides detailed forecasts from 2025 to 2034, emphasizing sustainability-driven product development, downgauging technologies, and digital printing adoption. The report highlights strategic investments, emerging applications, and regulatory influences shaping market growth while offering insights into operational efficiency, production optimization, and high-value branding opportunities. By profiling 15+ leading companies and examining their innovations in PE, POF, and recycled polymer films, this report is an essential resource for industry professionals, brand owners, packaging converters, and investors seeking to understand competitive dynamics, market segmentation, and long-term opportunities in collation shrink films. USDAnalytics ensures this comprehensive study equips decision-makers with actionable intelligence to navigate evolving regulations, circular economy trends, and technological transformation in packaging systems.

Scope Highlights:

- Segmentation: By Material Type (LDPE, LLDPE, MDPE, HDPE, PP, POF, Other Polymers); By End-Use Industry (Food & Beverage, Consumer Goods, Personal Care & Home Care, Pharmaceuticals & Healthcare, Transport & Logistics, Printing & Publications, Other Applications); By Thickness (Below 25 microns, 25–50 microns, 50–100 microns, Above 100 microns); By Application (Bottles, Cans, Cartons & Boxes, Others).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Analysis: Detailed insights on 15+ companies, including Amcor plc, Berry Global Inc., Dow Inc., ExxonMobil Corporation, Sealed Air Corporation, Nova Chemicals Corporation, Mondi plc, AEP Industries Inc., DuPont de Nemours, Inc., WestRock Company, RKW Group, Coveris Holdings SA, Bolloré, Tilak Polypack, and Plastigaur.

Methodology

The study employs a multi-step research methodology combining primary and secondary data sources to provide accurate market insights. USDAnalytics conducted extensive interviews with key industry stakeholders, including manufacturers, suppliers, distributors, and end-users, to validate market trends and adoption patterns. Secondary research incorporated regulatory reports, company filings, trade journals, and market literature to capture historical trends and growth drivers. Quantitative analysis included market sizing, CAGR calculations, and segmentation breakdowns by material, end-use industry, thickness, and application. Forecasting leverages scenario-based modeling and trend extrapolation, accounting for technological innovation, sustainability adoption, and regional regulatory shifts. Competitive intelligence was obtained through company profiles, strategic initiatives, and product launches, enabling a granular understanding of the global collation shrink films market landscape.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.