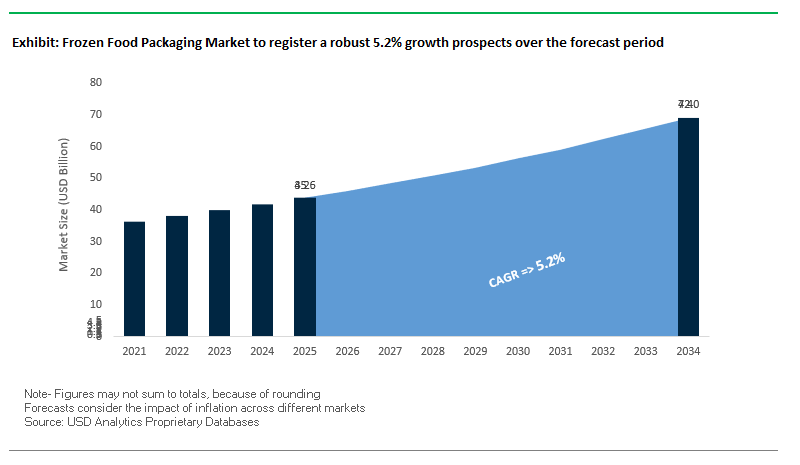

Market Overview: Frozen Food Packaging Market to Reach $72 Billion by 2034

The global frozen food packaging market is valued at $45.6 billion in 2025 and is projected to reach $72 billion by 2034, registering a CAGR of 5.2%. This sector plays a critical role in protecting product integrity, reducing food waste, and meeting consumer demand for convenience and sustainability. For industry professionals and buyers, frozen food packaging is not just a necessity it is a strategic driver of supply chain efficiency, shelf-life management, and eco-friendly product innovation.

Packaging innovations are centered around barrier films, recyclable materials, and lightweighting. The integration of consumer convenience features, such as microwaveable trays and resealable zippers, reflects the growing popularity of ready-to-eat and on-the-go frozen meals. At the same time, sustainability remains a top priority, with manufacturers shifting toward mono-material films, recyclable PE structures, and compostable trays that align with circular economy goals.

Key Insights for Industry Professionals:

- Advanced Barrier Films: Prevent freezer burn, extend shelf life, and maintain freshness.

- Recyclable and Compostable Materials: Rapid adoption of mono-material PE films and paperboard trays.

- Convenience Packaging: Easy-open, resealable, and microwave-ready formats drive consumer appeal.

- Lightweighting Practices: Reduced material use lowers costs and cuts transportation emissions.

Market Analysis: Recent Developments Driving Frozen Food Packaging Growth

The frozen food packaging industry has seen significant developments in 2024–2025, marked by mergers, material innovation, and sustainability-driven collaborations.

In August 2025, Amcor posted strong Q4 earnings, reflecting the success of its expanded portfolio of sustainable frozen food packaging solutions following its merger with Berry Global. Also in July 2025, the merger of Smurfit Kappa and WestRock created Smurfit WestRock, a major player in paperboard trays and liners for frozen foods. In the same month, Huhtamaki launched recyclable and compostable ice cream packaging, expanding its role in sustainable frozen desserts.

Earlier in April 2025, WestRock partnered with Recipe Unlimited to develop recyclable paperboard packaging, expected to reduce millions of plastic containers from Canadian landfills. In March 2025, MULTIVAC partnered with Watttron on “Smart Heating” technology to improve efficiency in producing recyclable thermoformed packs used widely in frozen ready meals.

On the innovation side, Mondi collaborated with Proquimia in February 2025 to launch paper-based stand-up pouches with high-barrier protection, while in January 2025, ITC Ltd. acquired Prasuma to strengthen its frozen food footprint in India. Earlier, Amcor launched Eco-Tite® R in November 2024, a recyclable PVDC-free shrink bag, underlining the shift toward packaging designed for existing recycling streams. Together, these developments underscore the sector’s dual focus on sustainability and consumer convenience.

Trends and Opportunities Shaping the Frozen Food Packaging Market

E-commerce Logistics Demanding Performance-Engineered Durability

The rapid rise of direct-to-consumer (DTC) frozen food delivery and third-party platforms such as Instacart, DoorDash, and Amazon Fresh is forcing a fundamental redesign of frozen food packaging. Unlike traditional retail distribution, where frozen products remain within a controlled supply chain, DTC models expose shipments to automated sortation systems, multiple transit handoffs, and variable thermal environments. This environment demands packaging with enhanced puncture resistance, high-integrity seals, and robust thermal insulation to preserve product quality throughout the journey.

A 2025 analysis of e-commerce cold chain logistics emphasized that a single temperature breach can render entire shipments unsafe, triggering recalls and reputational damage. Moreover, academic studies on Time-Temperature Indicators (TTIs) reveal that cumulative moderate thermal abuse (e.g., two hours at 15°F) can be more damaging than a brief exposure to higher temperatures. This underscores the need for packaging engineered for long-term temperature stability, shock absorption, and freezer-burn prevention.

For high-value frozen goods such as seafood or premium prepared meals, leak-proofing is now considered mandatory. Brands are deploying multi-layered solutions primary vacuum-sealed pouches paired with secondary rigid or molded containers to avoid spillage during transit. Negative consumer experiences tied to leaking frozen packages have been directly linked to poor reviews and churn in subscription meal-kit businesses, making seal integrity and structural performance central to brand competitiveness in the frozen food packaging market.

Regulatory Scrutiny on Plastic Waste Driving Material Substitution

Governments worldwide are implementing stringent bans, taxes, and EPR (Extended Producer Responsibility) frameworks targeting single-use plastics and EPS (expanded polystyrene), historically dominant in frozen food insulation. The EU’s Packaging and Packaging Waste Regulation (PPWR) mandates recyclability of all food packaging by 2030, while the Single-Use Plastics Directive (SUPD) has already phased out EPS items in Europe. In the U.S., states including Delaware and Maryland have passed EPS bans effective from 2025, adding to an increasingly fragmented compliance landscape.

India’s nationwide single-use plastic ban, effective since July 2022, eliminated polystyrene trays, cups, and containers, creating a significant demand surge for fiber-based, compostable, and recyclable alternatives. Globally, major FMCG and frozen food brands are proactively committing to phase out EPS in alignment with consumer expectations and regulatory mandates. Public commitments from multinational food producers to adopt recyclable, plastic-free insulated solutions have accelerated R&D pipelines for bio-based insulation and recyclable molded fiber containers.

This convergence of regulatory compliance, financial penalties under EPR schemes, and consumer sustainability preferences is creating an unprecedented demand shift, positioning recyclable and compostable frozen packaging solutions as the industry’s next growth frontier.

Development of High-Performance Molded Fiber with Integrated Insulation

The regulatory phase-out of EPS is creating a white-space opportunity for molded fiber insulated containers engineered for cold chain logistics. Success depends on balancing thermal retention, structural durability, and recyclability within a single, scalable packaging format.

Companies such as PulPac are pioneering dry molded fiber technologies with lower carbon footprints and engineered air-pocket designs for natural insulation. Parallel corporate-academic collaborations are producing fiber-based self-insulating containers using bio-coatings for moisture and grease resistance, providing direct competition to EPS. Unlike foam, molded fiber can be produced from 100% recycled paper and is both biodegradable and compostable, addressing both environmental and compliance concerns.

With frozen foods representing one of the most logistically demanding packaging segments, the ability to offer a monomaterial, curbside-recyclable insulated container could disrupt the market. This would give brands a future-proof solution to meet EU recyclability mandates while addressing consumer preference for plastic-free frozen packaging.

Integration of Time-Temperature Indicators (TTIs) for Quality Assurance

As frozen food delivery grows, the challenge of temperature abuse during last-mile logistics becomes more pronounced. Time-Temperature Indicators (TTIs) present a transformative opportunity by offering visual, irreversible cues that signal whether a frozen product has been exposed to unsafe thermal conditions.

Recent advances in Maillard reaction-based TTIs have demonstrated strong correlation between indicator color change and quality degradation in frozen foods like shrimp and chicken. These TTIs not only enhance consumer confidence but also provide brands with liability protection in the event of a cold chain failure.

The integration of TTIs also supports food waste reduction. Instead of relying solely on static “best-by” dates, retailers and consumers can make real-time decisions based on actual freshness, preventing premature disposal of safe products. Leading TTI manufacturers now offer low-cost, frozen-food-specific labels that trigger a color change at 0°C, directly addressing consumer concerns about freezer burn and product safety.

Competitive Landscape: Key Players Driving Frozen Food Packaging Innovation

The frozen food packaging market is highly consolidated, with multinational leaders dominating through strategic acquisitions, material science innovation, and eco-friendly product launches.

Amcor: Expanding Frozen Food Packaging with Sustainable Innovation

Amcor remains a frontrunner with a diverse portfolio of frozen food pouches, films, and trays. Following its 2025 merger with Berry Global, the company strengthened its consumer packaging leadership. Amcor’s AmPrima™ recycle-ready solutions and AmFiber™ paper-based formats highlight its sustainability agenda. Its global R&D network enables innovations like Eco-Tite® R shrink bags, designed for recycling while maintaining food safety.

Berry Global: Strengthening Circular Packaging in Frozen Foods

Berry Global maintains a strong position in frozen packaging, offering tubs, trays, and rigid plastics. After spinning off its health and hygiene division in 2025, Berry sharpened focus on consumer packaging. It is investing heavily in post-consumer recycled (PCR) content, ensuring recyclability and circularity in frozen food solutions. Its emphasis on rigid trays and flexible formats makes it a key supplier to global brands.

Mondi: Driving Growth with FunctionalBarrier Paper for Frozen Foods

Mondi has introduced FunctionalBarrier Paper, a recyclable paper-based packaging solution for frozen food, providing strong protection against moisture and grease. Under its MAP2030 sustainability plan, Mondi focuses on creating packaging “sustainable by design.” Its vertically integrated supply chain, from forestry to finished product, allows it to deliver consistent quality and expand eco-friendly frozen food packaging globally.

Sealed Air: Innovating with Cryovac® High-Performance Solutions

Sealed Air is best known for its Cryovac® brand shrink bags and films, widely used in frozen packaging for their ability to ensure shelf life and product protection. With its integrated systems of materials, machinery, and technical support, Sealed Air provides processors with complete solutions. Its strategic focus on waste reduction and sustainability positions it as a trusted partner for frozen food companies.

Huhtamaki: Expanding Compostable and Fiber-Based Frozen Packaging

Huhtamaki is broadening its frozen food packaging portfolio with recyclable and compostable products. In July 2025, it launched an innovative ice cream pack and expanded its fiber-based egg carton lines made from 100% recycled materials. With investments in Asia, particularly in Thailand and Vietnam, Huhtamaki is scaling capacity while advancing its goal of protecting food, people, and the planet.

Coveris: Building Circularity with Recyclable Mono-Material Films

Coveris is a European leader in frozen packaging, known for high-barrier films and recyclable trays. It recently launched films with higher recycled content to meet eco-label demands. Its mono-material solutions are designed for full recyclability, while its advanced printing capabilities deliver strong shelf impact for frozen food brands. Coveris combines material innovation with circular economy principles, strengthening its competitive edge.

Frozen Food Packaging Market Share Insights

Flexible Packaging Dominates Market Share by Packaging Type in Frozen Food Packaging

In 2025, flexible packaging secures 60% of the frozen food packaging market, cementing its position as the most efficient and dominant format. Bags, pouches, and barrier films perfectly align with the economics of frozen food by reducing material costs, optimizing storage space, and providing moisture and oxygen protection to prevent freezer burn. This dominance is evident across fruits, vegetables, seafood, and frozen entrées, where free-flow packaging and resealable options are increasingly standard. Rigid packaging maintains a vital 40% share, anchored by ready meals, frozen desserts, and bakery products that require structure, crush resistance, and consumer-friendly features such as microwave- and oven-compatibility. Rigid trays and tubs, often made from PP, PET, or coated paperboard, are especially critical in premium categories where convenience and presentation directly influence purchasing decisions. The segmentation illustrates how flexible packaging drives high-volume, cost-sensitive frozen food, while rigid packaging preserves premium positioning, structural integrity, and heating convenience.

Fruits and Vegetables Lead Market Share by Application in Frozen Food Packaging

By application, fruits and vegetables command 30% of the frozen food packaging market in 2025, reflecting their sheer global volume and reliance on flexible packaging formats. Individually Quick Frozen (IQF) peas, berries, and mixed vegetables are packaged in large-format bags that prioritize seal strength and moisture control to prevent clumping and ice crystallization. Ready-to-eat (RTE) meals follow with 25%, serving as the fastest-growing segment as consumers increasingly favor microwave-ready trays and dual-ovenable containers for convenience. Meat, poultry, and seafood packaging relies heavily on vacuum-sealed flexible bags and rigid trays to protect high-value proteins from oxidation and freezer burn, while frozen desserts demand rigid tubs, cartons, and protective formats to safeguard structure and brand identity. Bakery and confectionery products use hybrid packaging systems that combine trays with overwraps or cartons to maintain product integrity and freshness. Collectively, this breakdown shows how fruits and vegetables anchor frozen packaging volumes, RTE meals fuel innovation in convenience formats, and proteins, desserts, and bakery sustain demand for high-barrier, structure-protective solutions.

United States: Sustainability and Innovation Shaping the Frozen Food Packaging Industry

The U.S. frozen food packaging market is being transformed by a strong focus on sustainability and innovation. Companies are increasingly adopting recyclable and eco-friendly films to reduce reliance on fossil-based plastics, with Stora Enso introducing new board-grade packaging solutions for chilled and frozen foods. Barrier coating innovations, such as water-based dispersion coatings, are reducing the use of fluorochemicals while protecting products against water vapor and grease. The booming e-commerce and food delivery sectors are driving demand for durable, lightweight packaging capable of withstanding shipping, ensuring product integrity and a positive consumer experience. Technological advancements in modified atmosphere packaging (MAP) are extending the shelf life of frozen products, preserving freshness, and reducing food waste. Rising consumer demand for mono-material, recyclable packaging is pushing brands to move away from multi-material laminates, aligning with sustainability trends and circular economy principles.

Germany: Circular Economy Leadership and Paper-Based Packaging Innovation

Germany's frozen food packaging market is at the forefront of Europe’s circular economy, driven by the German Packaging Act (VerpackG) and the EU’s Single-Use Plastics Directive. The market is seeing significant innovation in recyclable materials, including partnerships to develop sustainable packaging pouches from circular-certified polymers. A key trend is the shift toward fully fiber-based, paper packaging solutions for frozen foods, compatible with existing packaging equipment. Collaboration between manufacturers and retailers, such as the Parkside and Iceland partnership, has resulted in recyclable paper packaging for frozen foods, marking a significant step toward plastic-free alternatives. These initiatives are reinforcing Germany’s leadership in sustainable frozen food packaging, focusing on reducing environmental impact while maintaining product performance.

China: Government Regulations and Intelligent Packaging Driving Market Expansion

China’s frozen food packaging market is being shaped by strict government policies promoting sustainability and food safety. Plastic bans and waste management regulations are compelling manufacturers to adopt eco-friendly and reusable packaging solutions. The industry is rapidly integrating intelligent packaging technologies, leveraging IoT, AI quality inspection, and 5G remote monitoring to enhance production efficiency and equipment stability. Rapid urbanization and changing lifestyles, coupled with growth in convenience foods and ready-to-eat products, are driving domestic demand for safe, convenient, and attractively packaged frozen food. Smart packaging solutions, such as temperature monitoring and freshness indicators, are increasingly used to maintain product quality throughout the supply chain, addressing both consumer expectations and regulatory requirements.

India: Government Incentives and E-Commerce Fuel Sustainable Packaging Growth

India’s frozen food packaging market is expanding due to strong government support, including the Production Linked Incentive (PLI) Scheme, which encourages investment in automated food and packaging lines. Sustainability is gaining momentum, with the FSSAI approving recycled PET as a food-contact material, driving demand for eco-friendly packaging solutions. The rapid growth of modern retail and e-commerce platforms is increasing the need for lightweight, durable packaging that protects products during shipping and handling. Regulatory focus on food safety and hygiene is influencing packaging innovation, ensuring that all materials in direct contact with frozen foods meet strict safety standards. These trends position India as a growing market for sustainable, technologically advanced frozen food packaging solutions.

Brazil: Bioplastics and Circular Economy Initiatives Leading Market Trends

Brazil’s frozen food packaging industry is a global leader in bioplastics, with green polyethylene derived from sugarcane ethanol reducing reliance on fossil fuels. Regulatory frameworks set by Anvisa ensure strict compliance for food contact materials, establishing uniform guidelines for packaging registration and product safety. The market is increasingly embracing circular economy initiatives, such as the “eureciclo” program, which provides Packaging Recycling Certificates to companies committing to environmental waste compensation. These measures encourage the adoption of sustainable packaging materials and practices, positioning Brazil as a key player in eco-friendly frozen food packaging innovation.

Japan: Automation and Compact Packaging Solutions Address Labor and Consumer Needs

Japan’s frozen food packaging market is adapting to an aging and shrinking workforce, with automation and advanced machinery becoming essential. Labor shortages are driving demand for packaging that can be efficiently handled by automated systems. The market is also responding to demographic trends, including the rise of single-person households, by developing compact, small-format packaging solutions that meet consumer convenience needs. Strict hygiene regulations under the Japanese Sanitation Act ensure that packaging is highly safe and minimizes contamination, making food safety a top priority. These trends highlight Japan’s focus on innovation, operational efficiency, and safety in frozen food packaging.

Frozen Food Packaging Market Report Scope

Frozen Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$45.6 Billion

|

|

Market Size (2034)

|

$72 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Aluminum, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Bakery & Confectionery, Ready-to-Eat Meals, Frozen Desserts, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, DS Smith Plc, Sealed Air Corporation, Sonoco Products Company, Graphic Packaging Holding Company, WestRock Company, Constantia Flexibles Group GmbH, Berry Global Group, Inc., Pactiv Evergreen Inc., TC Transcontinental Inc., DuPont de Nemours, Inc., Novamont S.p.A., Coveris Holdings S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Frozen Food Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Aluminum

- Bioplastics

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Application

- Fruits & Vegetables

- Meat

- Poultry & Seafood

- Bakery & Confectionery

- Ready-to-Eat Meals

- Frozen Desserts

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Frozen Food Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- DS Smith Plc

- Sealed Air Corporation

- Sonoco Products Company

- Graphic Packaging Holding Company

- WestRock Company

- Constantia Flexibles Group GmbH

- Berry Global Group, Inc.

- Pactiv Evergreen Inc.

- TC Transcontinental Inc.

- DuPont de Nemours, Inc.

- Novamont S.p.A.

- Coveris Holdings S.A.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global frozen food packaging market, providing an in-depth analysis of breakthroughs, emerging innovations, and strategic developments that are transforming the sector. The analysis reviews historical data from 2021 to 2024 and delivers comprehensive forecasts from 2025 to 2034, highlighting advancements in flexible packaging, rigid trays, high-barrier films, and sustainable alternatives such as mono-material PE, fiber-based trays, and bioplastics. This report emphasizes the growing importance of convenience-focused packaging with microwaveable, resealable, and easy-open features, alongside the integration of smart technologies like Time-Temperature Indicators (TTIs) to enhance quality assurance across cold-chain logistics. Key developments covered include material substitution driven by regulatory pressures, e-commerce-ready durability, and innovations in molded fiber insulation to replace EPS, reducing environmental impact while maintaining product integrity. Analysis reviews major mergers, collaborations, and sustainability initiatives across 15+ leading companies, including Amcor, Berry Global, Mondi, Huhtamaki, and Sealed Air, while highlighting global market trends and regional growth drivers. For industry professionals, this report is an essential resource for understanding market dynamics, competitive positioning, regulatory compliance, and opportunities to optimize frozen food packaging for efficiency, sustainability, and consumer satisfaction.

Scope Highlights:

- Segmentation: By Material Type (Plastics, Paper & Paperboard, Aluminum, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Bakery & Confectionery, Ready-to-Eat Meals, Frozen Desserts, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historical insights from 2021–2024 and projections from 2025–2034

- Companies: Analysis and profiles of 15+ key players, including Amcor, Mondi, Huhtamaki, Berry Global, Sealed Air, WestRock, Coveris, and others

Methodology

The study employs a rigorous research methodology combining primary and secondary data sources to ensure actionable insights for industry professionals. Primary research involved detailed interviews with executives, R&D specialists, supply chain managers, and packaging engineers to capture perspectives on material innovations, smart packaging adoption, and sustainability initiatives. Secondary research encompassed company reports, press releases, regulatory publications, industry journals, and academic studies to evaluate market trends, competitive strategies, and regional growth dynamics. Data triangulation was applied to reconcile discrepancies across sources, ensuring accuracy in historical data from 2021 to 2024 and reliable forecasting through 2034. Quantitative modeling incorporated CAGR analysis, material adoption rates, and packaging format penetration, while qualitative insights were used to assess market drivers, regulatory impacts, and consumer behavior. Competitive benchmarking, SWOT analysis, and strategic profiling of 15+ global players provided a detailed understanding of market positioning and innovation pipelines, enabling industry professionals to make informed decisions on frozen food packaging investments, sustainability strategies, and product development.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.