Packaging Equipment Market Value, Growth Trajectory, and Industry Transformation

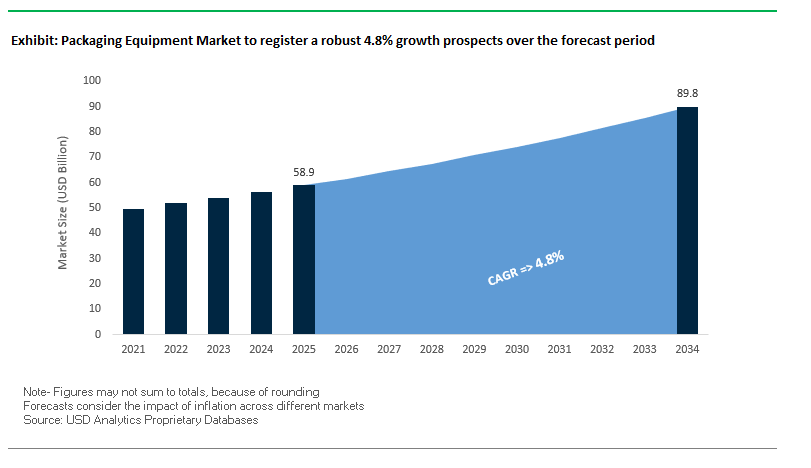

The Global Packaging Equipment Market is projected to expand from $58.9 billion in 2025 to $89.8 billion by 2034, reflecting a CAGR of 4.8%. This growth is underpinned by a worldwide shift towards automation, sustainability, and digital integration across production lines. Increasing operational efficiency, cost reduction imperatives, and rising consumer demand are compelling industries to adopt advanced packaging machinery at an accelerated pace.

Key Insights for Industry Stakeholders

- Automation and Robotics Driving Operational Excellence: AI-powered equipment and robotic systems enhance speed, precision, and reduce dependency on manual labor, directly lowering production costs.

- Sustainability Integration: Growing adoption of bioplastics, recycled paper, and mono-material packaging is influencing equipment design to minimize waste and energy consumption.

- Flexible and Customizable Solutions: E-commerce growth and shorter production runs demand machines capable of rapid format switching across diverse product sizes and packaging types.

- IoT and Smart Packaging Adoption: Real-time sensors, AI diagnostics, and predictive maintenance improve uptime, optimize machine performance, and enable data-driven decision-making.

- Strategic Consolidation Impact: Mergers and acquisitions are reshaping market dynamics, creating new equipment demands and fostering innovation.

Strategic Consolidation and Technological Innovation Driving Global Packaging Equipment Market Evolution

The Global Packaging Equipment Industry is undergoing significant transformation fueled by strategic acquisitions, technological innovations, and sustainability mandates. In August 2025, industry reports highlighted increasing adoption of intelligent packaging solutions with embedded sensors, enabling better monitoring of product conditions during storage and transit, thereby reshaping machinery specifications and operational standards.

In July 2025, the merger of Amcor and Berry Global Group created a dominant consumer packaging player, boosting demand for flexible and rigid container equipment. In May 2025, Mondi commissioned a €400 million paper machine at its Štětí mill, driving the need for machinery capable of handling sustainable paper-based packaging. Similarly, the April 2025 acquisition of DS Smith by International Paper reinforced corrugated packaging production, expanding the requirement for high-throughput, versatile packaging machinery.

Innovation continues to shape the market. Syntegon’s launch of the MLD® Advanced filling machine in April 2025, capable of processing 400 syringes per minute, reflects the pharmaceutical sector’s push toward automation, precision, and high-speed operations. Strategic consolidation in late 2024, such as Smurfit Kappa’s acquisition of WestRock in November and Mespack’s demonstration of advanced case packaging machinery in October, underscores the market’s evolution toward end-of-line automation and sustainable practices. Additionally, September 2024 reports highlighted the growing adoption of mono-material packaging, driving investment in equipment for fully recyclable materials.

Trends and Opportunities Driving Growth in the Packaging Equipment Market

Strategic Reshoring and Nearshoring Driving Demand for Automated Packaging Lines in North America

The packaging equipment market is being reshaped by a surge in reshoring and nearshoring strategies as companies realign global supply chains to mitigate geopolitical risks and labor shortages. In September 2025, GE Appliances announced a $3 billion, five-year modernization plan across 11 U.S. facilities, including its advanced Louisville, Kentucky site. The investment is focused on automation and high-tech packaging systems to offset rising labor costs and improve production resilience. Government policy is also amplifying demand: the Inflation Reduction Act (IRA) provides incentives and tax credits for domestic manufacturing, particularly in clean energy and EV supply chains, sending a long-term signal to invest in advanced packaging lines. Labor shortages remain a pressing challenge, with over 415,000 unfilled U.S. manufacturing jobs in June 2025, pushing companies like John Deere to announce $20 billion in U.S. investments over the next decade, integrating AI-enabled packaging and inspection systems. Supplier localization is another critical aspect—Apple expanded its American Manufacturing Program in September 2025, funding packaging and semiconductor suppliers in Texas, Arizona, and New York to strengthen the domestic packaging ecosystem. Together, these developments underscore how reshoring strategies are catalyzing sustained investment in automated packaging infrastructure.

Integration of AI-Powered Machine Vision for Defect Detection and Quality Control

The deployment of AI-powered machine vision is revolutionizing quality control in packaging lines, particularly in high-precision industries such as pharmaceuticals, electronics, and food processing. Unlike traditional systems that rely on pre-defined defect rules, deep learning-based vision systems can detect microscopic flaws, discolorations, or structural deviations with accuracy beyond human capabilities. Real-time anomaly detection reduces both false positives and false negatives, improving yield and reducing waste. For example, packaging lines equipped with advanced AI systems now offer end-to-end traceability, enabling real-time product monitoring and streamlining recall management. These systems also enhance efficiency by supporting automated sorting and classification based on product size, shape, or color, boosting throughput in high-volume operations. The convergence of machine learning, computer vision, and robotics is transforming packaging equipment into intelligent, self-correcting systems, aligning with Industry 4.0 manufacturing models that prioritize data-driven operations, operational resilience, and sustainability.

Development of Modular and Retrofittable Automation Solutions for SMEs

Small and medium-sized enterprises (SMEs) face significant barriers to automation adoption due to high upfront capital costs and integration complexity. This creates a compelling opportunity for modular and retrofittable automation systems that enable phased investment. Instead of a full packaging line overhaul, SMEs can adopt collaborative robots (cobots) for specific repetitive tasks such as carton erecting, labeling, or pick-and-place operations. Cobots, designed for safe human-machine collaboration without extensive safety cages, are particularly appealing for SMEs with limited floor space and workforce expertise. To further reduce integration barriers, equipment providers are rolling out pre-engineered, plug-and-play modules that allow rapid deployment and customization. These modular systems also feature quick-changeover designs, enabling SMEs to adapt to short production runs and diverse product portfolios with minimal downtime. For equipment manufacturers, offering scalable, cost-efficient automation tailored to SMEs unlocks a large and underserved segment of the packaging equipment market.

Equipment Designed for the Circular Economy: Reusable Packaging Handling Systems

The global shift toward circular economy packaging models is creating new demand for packaging equipment that can process reusable, returnable containers in sectors like e-commerce, grocery delivery, and consumer goods. Unlike single-use formats, durable containers require specialized handling systems that include automated washing, sanitization, inspection, sorting, and refilling lines. To support closed-loop logistics, companies are investing in reverse logistics infrastructure with AI-driven inspection and machine vision systems capable of identifying damage or contamination before reuse. These systems are complemented by robotics and smart sorting technologies that can differentiate reusable packaging from recycling or waste streams, ensuring containers are reintegrated into circulation. Real-world adoption is already underway: global case studies show automated filling and capping lines being redesigned for non-standardized, durable packaging formats, requiring more advanced robotic adaptability than traditional equipment. With leading FMCG companies and consortia like Loop piloting reusable models, purpose-built equipment for returnable container ecosystems is set to become a core growth area in the packaging equipment market.

Competitive Leadership and Technological Differentiation in the Global Packaging Equipment Market

The Packaging Equipment Industry is dominated by key players leveraging engineering expertise, automation, and sustainability innovations to provide high-performance solutions. These companies are defining industry standards through smart, flexible, and highly efficient machinery across multiple sectors.

Krones AG: Delivering High-Speed and Sustainable Beverage and Liquid Packaging Solutions

Krones AG is a leader in integrated production lines for beverage and liquid food industries, providing modular, flexible systems from filling and labeling to palletizing. Recent innovations include high-speed filling machines and smart diagnostics, enabling predictive maintenance and reduced downtime. Krones emphasizes energy efficiency and sustainability, integrating digital platforms for real-time monitoring, enhancing overall operational performance.

Syntegon Technology GmbH: Advancing Precision Automation in Food and Pharmaceutical Packaging

Syntegon Technology GmbH, formerly Bosch Packaging Technology, specializes in high-precision, sterile packaging equipment for pharmaceutical and food industries. Innovations like the April 2025 MLD® Advanced filling machine and the July 2023 high-speed capsule filler highlight its focus on automation, throughput, and regulatory compliance. IoT and AI integration provides predictive maintenance, remote support, and enhanced quality control, making Syntegon a market leader in smart packaging solutions.

Coesia S.p.A.: Expanding Global Reach with Hybrid and End-to-End Packaging Solutions

Coesia S.p.A. offers diversified end-to-end packaging solutions across food, luxury, and electronics sectors. Strategic acquisitions and hybrid machines combining mechanical and digital technologies ensure high efficiency and flexibility. Coesia’s portfolio includes labeling, flexible packaging, and end-of-line systems, designed to handle complex, high-speed production requirements.

Tetra Pak: Leading Aseptic and Sustainable Packaging Innovation

Tetra Pak is globally recognized for aseptic packaging solutions, enabling long-term storage without refrigeration. The company is advancing sustainable materials, including paper-based and plant-based packaging, with specialized machinery for high-speed, hygienic production. Tetra Pak invests in low-carbon circular economy initiatives and develops equipment capable of processing a wide range of eco-friendly materials.

Marchesini Group S.p.A.: Compact, High-Precision Solutions for Pharmaceuticals and Cosmetics

Marchesini Group S.p.A. specializes in compact, automated machinery for pharmaceutical and cosmetics industries. Key developments include AI-enabled inspection systems and machinery for personalized medicine production. Its portfolio, covering blister packaging, cartoning, and liquid filling systems, provides high precision, reliability, and operational efficiency, meeting stringent sector regulations.

Packaging Equipment Market Share Insights

Fully Automatic and Robotics-Integrated Systems Dominate Market Share by Automation Level in the Packaging Equipment Industry

Fully automatic and robotics-integrated systems hold 58% of the packaging equipment market, underlining the industry’s decisive shift toward automation. The dominance of this segment is tied to the growing demand for operational efficiency, labor reduction, and enhanced quality control in packaging processes. Robotics-enabled solutions provide unmatched flexibility for high-mix, low-volume production environments, enabling personalization, small-batch runs, and seamless adaptation to evolving consumer preferences. Integration with Industry 4.0 frameworks and smart factory ecosystems positions this segment at the core of future-ready packaging operations. While semi-automatic and manual equipment retain relevance in SMEs, prototyping, and niche artisan production, the global packaging industry is firmly oriented toward fully automated lines that deliver throughput, consistency, and compliance with strict hygiene and traceability requirements.

Food & Beverage Companies Hold the Largest Market Share by End-Use in the Packaging Equipment Industry

Food and beverage companies represent 42% of the end-use demand for packaging equipment, making them the undisputed industry leader. Their dominance is driven by the sheer scale of global food production, the critical importance of extended shelf-life, and the rapid pace of packaging innovation needed to align with evolving consumer preferences. Equipment in this sector supports advanced processes such as modified atmosphere packaging, aseptic filling, high-speed bottling, and recyclable material handling, ensuring both product safety and sustainability compliance. The influence of retail-ready packaging and e-commerce grocery growth further reinforces investment in high-performance systems. While pharmaceuticals and healthcare drive high-value, precision equipment demand, and cosmetics prioritize customization and premium finishes, the volume intensity and innovation-driven requirements of food and beverage packaging secure its position as the most influential end-use industry in the global packaging equipment market.

United States Packaging Equipment Market Driven by Stringent Regulations and Automation Investments

The United States packaging equipment market is heavily influenced by a stringent regulatory environment focused on food safety, pharmaceutical compliance, and sustainable packaging practices. The FDA enforces high standards for equipment used in food and drug packaging, while state-level policies such as California’s SB-54 are pushing manufacturers to adopt machinery capable of handling recyclable and post-consumer recycled (PCR) materials. These legal frameworks are creating new growth opportunities for suppliers of sustainable and automation-ready packaging systems. At the same time, the U.S. government is actively supporting sustainability through grants from agencies like the Department of Energy (DOE) and the USDA, which are funding pilot plants for biopolymer production, further stimulating equipment innovation.

A key driver in the U.S. market is the rapid adoption of robotics, automation, and AI-enabled vision systems across packaging lines. These technologies improve predictive maintenance, minimize downtime, and optimize quality control. A notable example came in August 2025 when Mary Kay invested $2 million to upgrade its packaging line, cutting line labor by 85% with new automation solutions. Growth is especially strong in food and beverages, pharmaceuticals, and e-commerce packaging. With e-commerce parcel volumes soaring, demand for secondary packaging equipment such as case packers and palletizers continues to rise, positioning the U.S. as one of the most innovation-driven packaging equipment markets globally.

Germany Packaging Equipment Market Boosted by EU Sustainability Rules and Beverage Demand

Germany’s packaging equipment market is shaped by the European Union’s Packaging and Packaging Waste Regulation (PPWR) and the German Packaging Act (VerpackG), both of which emphasize recyclability, recycled content, and circular economy principles. The 2025 amendments to VerpackG have intensified obligations on businesses, driving demand for packaging machinery that can meet higher sustainability benchmarks. German mechanical engineering firms are also pioneering intelligent, modular packaging lines that offer flexibility and energy efficiency, aligning with EU climate goals.

Technological innovation remains Germany’s strongest advantage. The country is a hub for advanced films, extrusion lines, and next-generation automation systems. Corporate sentiment is optimistic, with incoming packaging machinery orders rising 16% in real terms during the first four months of 2024. Strong demand is concentrated in food, beverage, and pharmaceutical applications, with beverage packaging machinery showing significant growth due to high production volumes. German companies are increasingly developing modular solutions tailored for rapid format changes, enabling manufacturers to handle diverse product lines without compromising sustainability.

China Packaging Equipment Market Accelerated by Dual-Carbon Targets and Smart Manufacturing

China’s packaging equipment industry is experiencing rapid transformation under the government’s dual-carbon targets—carbon peaking by 2030 and neutrality by 2060. These initiatives are encouraging the adoption of eco-friendly coatings, water-based materials, and energy-efficient machinery. To support compliance and food safety, the government is also investing in smart regulatory platforms for traceability and information sharing, which is pushing local manufacturers to integrate AI-driven automation and intelligent manufacturing into their packaging systems.

Corporate investments are reinforcing this momentum. Amcor’s state-of-the-art facility in Huizhou, equipped with intelligent production systems, highlights the shift toward sustainable and high-quality packaging for the growing food processing and e-commerce markets. China’s e-commerce ecosystem alone generated over 175 billion parcel deliveries in 2024, creating unprecedented demand for durable, automation-ready secondary packaging equipment. Alongside e-commerce, the electronics and consumer goods industries are expanding at a rapid pace, cementing China’s role as one of the fastest-growing packaging equipment markets worldwide.

India Packaging Equipment Market Strengthened by EPR Policies and E-Commerce Growth

India’s packaging equipment market is being propelled by the government’s Make in India initiative and the Production Linked Incentive (PLI) scheme, which encourage local manufacturing and innovation. The implementation of Extended Producer Responsibility (EPR) guidelines for plastic packaging is accelerating the transition to a circular economy, forcing companies to invest in equipment capable of handling recyclable and sustainable materials. These regulatory changes are significantly reshaping investment priorities in the sector.

The rise of e-commerce and modern retail formats is driving demand for advanced packaging solutions that ensure product safety, presentation, and efficiency. The food and beverage sector, being central to India’s food processing industry, is a major consumer of packaging machinery. Corporate investments are supporting this shift, such as the Huhtamaki Foundation’s CloseTheLoop initiative, which allocated Rs. 10 crore (US$ 1.18 million) to establish recycling plants for post-consumer plastics. This investment will create demand for specialized recycling and packaging equipment. With supermarkets and online grocery platforms expanding rapidly, packaging machinery has become indispensable for ensuring shelf appeal, quality, and protection.

Japan Packaging Equipment Market Driven by Food-Contact Rules and High-Precision Technologies

Japan’s packaging equipment market is evolving under new regulatory policies, including the positive list system for food-contact packaging that came into effect in June 2025. This system specifies permitted substances for food-contact applications, creating a strong push for machinery that can handle approved, safe, and eco-friendly materials. The regulation supports Japan’s wider sustainability targets of reducing GHG emissions by 46% by 2030 and achieving carbon neutrality by 2050, which in turn fuels investment in bio-based and recyclable packaging technologies.

Japanese manufacturers are at the forefront of technological precision and advanced design. For example, Shin-Etsu Chemical introduced machinery for producing semiconductor package substrates using the twin damascene process in 2024, highlighting Japan’s expertise in high-end applications. The market is particularly robust in ready-to-drink beverages, snacks, and premium packaging segments, where lightweight, durable, and aesthetically appealing designs are in high demand. With consumers prioritizing quality and sustainability, Japan is focusing on packaging equipment that balances environmental compliance with innovation-driven design.

Brazil Packaging Equipment Market Shaped by Anvisa Regulations and Circular Economy Push

Brazil’s packaging equipment market is strongly influenced by regulatory frameworks, particularly those set by the National Health Surveillance Agency (Anvisa) and the National Solid Waste Policy (PNRS). In April 2024, Anvisa revised its regulation on metallic coatings for food-contact applications, introducing a positive list of authorized materials and strict limits on heavy metals. This regulatory shift has created demand for advanced machinery capable of processing safer coatings and packaging components. Furthermore, upcoming decrees mandating companies to recycle up to 50% of their products are accelerating investment in recycling-compatible equipment.

The market is also benefiting from technological innovation and sustainability initiatives. Manufacturers are increasingly utilizing bio-based materials such as corn starch and sugarcane bagasse in packaging applications. Ambev’s launch of canned water in aluminum cans, supported by Brazil’s high recycling rates, demonstrates the growing emphasis on circular economy practices. Food and beverage packaging remains the largest application segment, with strong demand for equipment that ensures barrier protection, product safety, and reduced waste. As a global leader in canned goods production, Brazil continues to prioritize machinery that supports safe, sustainable, and efficient packaging processes.

Packaging Equipment Market Report Scope

Packaging Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$58.9 Billion

|

|

Market Size (2034)

|

$89.8 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Machine Type (Filling & Dosing, Labeling/Decorating/Coding, Form-Fill-Seal, Cartoning, Wrapping & Bundling, Palletizing & Depalletizing, Capping & Sealing, Others), By Automation Level (Manual, Semi-Automatic, Fully Automatic & Robotics-Integrated), By End-Use Industry (Food & Beverage, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Consumer Goods, Industrial), By Technology Platform (General Packaging, MAP, Aseptic Packaging, Intelligent & Connected Packaging Lines)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Krones AG, Syntegon Technology, Tetra Pak International S.A., Coesia S.p.A., IMA Group, Sidel, MULTIVAC Sepp Haggenmüller SE & Co. KG, Fuji Machinery Co., Ltd., Marchesini Group S.p.A., Barry-Wehmiller Companies, Inc., Aetna Group S.p.A., ARPAC LLC (A Duravant Company), Duravant LLC, Nichrome India Ltd., Ishida Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Equipment Market Segmentation

By Machine Type

- Filling & Dosing

- Labeling/Decorating/Coding

- Form-Fill-Seal

- Cartoning

- Wrapping & Bundling

- Palletizing & Depalletizing

- Capping & Sealing

- Others

By Automation Level

- Manual

- Semi-Automatic

- Fully Automatic & Robotics-Integrated

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Consumer Goods

- Industrial

By Technology Platform

- General Packaging

- MAP

- Aseptic Packaging

- Intelligent & Connected Packaging Lines

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Equipment Market

- Krones AG

- Syntegon Technology

- Tetra Pak International S.A.

- Coesia S.p.A.

- IMA Group

- Sidel

- MULTIVAC Sepp Haggenmüller SE & Co. KG

- Fuji Machinery Co., Ltd.

- Marchesini Group S.p.A.

- Barry-Wehmiller Companies, Inc.

- Aetna Group S.p.A.

- ARPAC LLC (A Duravant Company)

- Duravant LLC

- Nichrome India Ltd.

- Ishida Co., Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver precise insights into the global packaging equipment market. This approach combines primary research, secondary data analysis, and predictive modeling to ensure accuracy and relevance for industry professionals. Primary research includes interviews and consultations with packaging engineers, operations managers, automation specialists, and sustainability experts from leading companies such as Krones AG, Syntegon Technology, and Tetra Pak. Secondary research draws upon regulatory frameworks including FDA guidelines, EU Packaging and Packaging Waste Regulation (PPWR), Japan’s positive list for food-contact materials, and Brazil’s PNRS policies, as well as corporate filings, press releases, and market reports. USDAnalytics evaluates trends in automation, robotics, AI-driven machine vision, modular solutions for SMEs, and circular economy-driven equipment innovations. The methodology incorporates historical market performance, technological adoption rates, and production line transformations to forecast growth trajectories. Competitive landscape analysis highlights strategic mergers, technological differentiation, and sustainability-driven equipment development, providing actionable insights for manufacturers, investors, and supply chain decision-makers seeking to navigate the rapidly evolving packaging equipment ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.