Rigid Paper Containers Market Size, Overview, and Growth Outlook (2025–2034)

Rigid Paper Containers Market to Surge to $730.6 Billion by 2034 Driven by Sustainability and Innovation

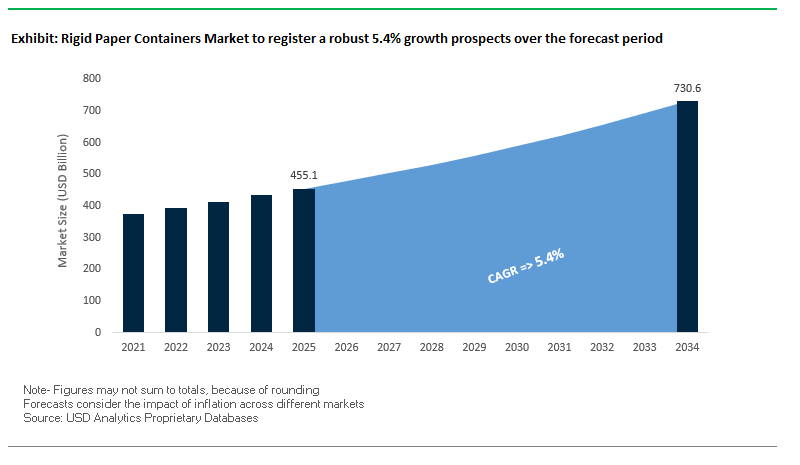

The global rigid paper containers market is projected to grow from $455.1 billion in 2025 to $730.6 billion by 2034, reflecting a CAGR of 5.4%. Growth is fueled by rising adoption of recycled fibers, high recyclability rates, and increasing demand in the chilled food packaging sector. These containers provide durability, temperature stability, and brand enhancement opportunities, making them a preferred alternative to single-use plastics.

Key Insights for industry professionals and buyers:

- Recycled Fiber Integration: Leading manufacturers use up to 100% recycled paperboard, with 90% sourced from post-consumer materials.

- High Recyclability: Independent studies, including those by Western Michigan University, show over 85% fiber recovery during recycling of all-paper containers.

- Chilled Food Dominance: Rigid paper containers are the preferred choice for chilled and perishable food packaging, offering both insulation and durability.

- Versatility and Printability: Boxes and cartons dominate the product segment due to their design flexibility, shelf appeal, and brand customization potential.

- Sustainability Pressure: Regulatory and consumer demand is pushing manufacturers toward circular economy packaging solutions.

- Premium Packaging Potential: Rigid paper containers allow innovative printing, labeling, and premium finishes to enhance product perception.

The rigid paper containers market balances sustainability, product protection, and branding, making it a high-priority segment for global packaging professionals.

Market Analysis: Strategic Investments and Mergers Accelerate Rigid Paper Container Market Growth

The rigid paper container market is witnessing robust growth through strategic investments, mergers, and sustainable innovation. In August 2025, Sonoco Products Company announced a $30 million investment in its Orlando, Florida facility to enhance paper and recycling capabilities. The same month, Nefab Denmark acquired FARUSA Emballage, expanding its portfolio in heavy-duty corrugated solutions. July 2025 marked the completion of the International Paper and DS Smith merger, creating a global leader in sustainable paper-based packaging.

In June 2025, Mondi launched a sustainable solution for pet food packaging, highlighting the use of functional, eco-friendly paper-based materials. By May 2025, Mondi’s €400 million Štětí paper machine became operational, reinforcing its leadership in high-quality, sustainable packaging production. Companies are increasingly divesting non-core businesses to focus on rigid paper containers and circular economy initiatives, as evidenced by Sonoco’s sale of its Thermoformed and Flexibles Packaging business in April 2025.

The market also sees innovations targeting lightweight and protective e-commerce packaging. In March 2025, Smurfit Kappa launched a paper-based packaging series for European e-commerce, emphasizing ease of assembly and high protection. February 2025 saw Mondi and Proquimia introduce paper-based stand-up pouches for dishwashing tabs, marking a significant step toward plastic replacement in household products.

Rigid Paper Containers Market: Key Trends and Emerging Opportunities

Accelerated Phase-Out of PFAS in Food-Contact Paper Packaging

One of the most significant trends influencing the rigid paper containers market is the rapid elimination of per- and polyfluoroalkyl substances (PFAS) in food-contact packaging. In the United States, state-level regulations are at the forefront of this shift. By late 2024, California, New York, Washington, and Connecticut had all enacted bans on intentionally added PFAS in food-contact materials, creating non-negotiable compliance requirements for manufacturers. This regulatory momentum is pushing packaging producers to innovate barrier technologies that maintain food safety without PFAS reliance. At the corporate level, leading brands and retailers are responding with aggressive phase-out commitments. For instance, in 2024, Archroma introduced PFAS-free water-based coatings designed for food packaging applications, offering manufacturers a compliant, scalable, and recyclable alternative. Together, these regulatory and corporate initiatives are making PFAS elimination a top priority in rigid paper container production, fundamentally reshaping material sourcing and coating technologies across the industry.

Corporate Investment in Molded Fiber Production for E-Commerce

Another defining trend is the growing investment in molded fiber solutions, particularly for e-commerce and high-value retail sectors. As e-commerce expands, companies are looking for sustainable replacements for plastics and Styrofoam in protective packaging. A 2025 case study highlighted an electronics manufacturer that replaced plastic inserts with custom-molded fiber components, offering superior cushioning, full recyclability, and enhanced unboxing aesthetics. This aligns with consumer demand for eco-friendly and premium packaging experiences. In response, packaging producers are scaling up production capacity. For example, in 2025, Omni-Pac partnered with HP to digitize molded fiber production, enhancing design flexibility while enabling mass production for premium segments like cosmetics and electronics. These advancements underscore molded fiber’s role in addressing both environmental regulations and evolving consumer expectations, cementing it as a critical growth driver for rigid paper containers in the digital economy.

Development and Scaling of High-Performance Bio-Based Barrier Coatings

The regulatory ban on PFAS opens a significant opportunity for the development of bio-based barrier coatings tailored for rigid paper packaging. Recent academic studies highlight chitosan and cellulose derivatives as promising candidates for creating moisture-, oxygen-, and grease-resistant coatings that preserve food integrity while maintaining recyclability and compostability. Building on this, companies such as Solenis have launched advanced product lines like TopScreen™ coatings, which are water-based, PFAS-free, and suitable for direct food-contact applications. These coatings not only provide high-performance oil and grease resistance but also align with brand sustainability targets by being recyclable and compostable. This innovation space offers manufacturers a way to combine functionality with compliance, positioning bio-based coatings as the next frontier in food-safe, environmentally responsible rigid paper packaging.

Integration of Digital Watermarking for Enhanced Recycling Streams

Another major opportunity lies in digital watermarking technologies for recycling efficiency and traceability. The HolyGrail 2.0 initiative, backed by over 130 industry players, has already proven the industrial-scale feasibility of digital watermarks. In 2025 trials, watermarked rigid packaging achieved sorting accuracy of over 95% purity, enabling recyclers to separate coated and uncoated paperboard with unmatched precision. Beyond sorting, digital watermarks serve as a “digital passport”, embedding critical data on material type, food versus non-food usage, and recyclability parameters. This granular level of detail enhances material recovery rates and creates new high-value recycling streams for rigid paper containers. By providing transparency throughout the lifecycle, digital watermarking not only optimizes circularity but also supports compliance with upcoming EU Digital Product Passport regulations, which will require traceability in packaging and consumer goods.

Competitive Landscape: Leading Companies Are Driving the Global Rigid Paper Containers Market with Sustainable Innovations

The global rigid paper containers industry is highly competitive, with leading players focusing on recycled fiber utilization, product innovation, and integrated supply chains to maintain a sustainable edge. Companies offer a range of solutions across food, beverage, and personal care segments, emphasizing both product protection and premium presentation.

Sonoco Products Company: Strengthening Global Presence Through Strategic Investments and Core Focus

Sonoco provides a wide variety of rigid paper containers, including paper cans, composite cans, and paperboard tubes. In August 2025, the company invested $30 million to enhance its Orlando facility, complementing its Performance Hub in Hyderabad, India. Sonoco strategically divested its Thermoformed and Flexibles Packaging business in April 2025 for $1.8 billion, allowing a sharper focus on rigid paper containers. Its strength lies in advanced barrier solutions, recycled paperboard usage, and sustainable packaging expertise.

Smurfit Kappa Group Plc: Leveraging Integrated Supply Chains to Drive Sustainable Paper-Based Packaging

Smurfit Kappa offers an extensive portfolio of rigid paper containers, including corrugated boxes, folding cartons, and solidboard packaging. The July 2025 merger with WestRock expanded its global footprint and product diversity. In March 2025, the company launched a new paper-based e-commerce packaging series. Smurfit Kappa’s fully integrated supply chain, including forestry, paper mills, and converting plants, ensures sustainable material sourcing and secure supply.

International Paper Company: Creating a Circular Economy with Fiber-Based Packaging and Strategic Investments

International Paper provides corrugated packaging, consumer packaging, and pulp-based rigid containers. Its July 2025 merger with DS Smith strengthened its presence in North America and Europe. Strategic initiatives under the “Building a Better IP” plan include a $100 million corrugated facility in Pennsylvania. International Paper’s recycling operations, processing over 7 million tons of paper annually, are integral to its circular business model.

Graphic Packaging International: Innovating Chilled Food Packaging Through Design and Sustainability

Graphic Packaging International specializes in rigid paperboard boxes, cartons, and trays for food, beverage, and personal care. In July 2023, it partnered with ABP Food Group to develop vacuum skin packaging (VSP) trays for Aldi, enhancing chilled meat preservation. Graphic Packaging’s strength lies in design innovation, product preservation technologies, and strong chilled food market presence.

Mondi Group: Driving Sustainable Paper Manufacturing Through Advanced Facilities and Circular Packaging

Mondi offers a wide range of rigid paper containers, including paper-based sacks and boxes, with strong operations in corrugated packaging. In May 2025, Mondi started up a €400 million paper machine at its Štětí plant. Strategic acquisitions, such as Schumacher Packaging’s Western Europe assets, strengthen its footprint. Mondi’s MAP2030 sustainability commitments target fully reusable, recyclable, or compostable products, supported by an integrated value chain from forestry to converting.

Rigid Paper Containers Market Share Insights, 2025-2034

Boxes & Cartons dominate Market Share by Product Type in the Rigid Paper Containers Industry

Boxes and cartons hold the dominant share of the rigid paper containers industry at 55%, reflecting their unmatched versatility and alignment with global sustainability agendas. Folding cartons for dry foods, beverage cartons for dairy and juices, and rigid set-up boxes for luxury goods such as electronics and cosmetics highlight the sector’s breadth. Their strength lies in excellent printability, branding potential, and recyclability, which resonate strongly in both retail and e-commerce environments. Recent innovations in moisture- and grease-resistant barrier coatings are extending paperboard applications into traditionally plastic-heavy categories like frozen food and takeaway meals. This positions cartons as the cornerstone of the industry’s substitution strategy against single-use plastics, ensuring that they remain the most strategic product type in both volume and growth relevance.

Food & Beverages drive Market Share by End-Use Industry in the Rigid Paper Containers Industry

The food and beverages sector accounts for 40% of rigid paper container demand, making it the primary growth engine for this market. From bakery and frozen foods to dairy and beverages, brands are increasingly shifting to rigid paper formats to meet consumer demand for recyclable and compostable packaging. The sector’s scale ensures that material innovations—such as compostable barrier coatings and molded fiber trays—find their first and widest adoption here, reinforcing paper as a functional and sustainable substitute for plastic. This alignment between consumer preference, regulatory pressure, and operational suitability secures the food and beverage segment’s leading position, while also setting the direction for the industry’s innovation pipeline.

European Union: PPWR and ESPR Regulations Accelerating Rigid Paper Container Innovation

The European Union rigid paper containers market is undergoing significant transformation due to the Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025. This regulation sets strict reuse targets, mandates reductions in per capita packaging waste, and requires that all plastic components in packaging contain minimum percentages of post-consumer recycled content by January 2030. These mandates are driving the development of advanced paper-based coatings and barrier solutions as substitutes for plastics in rigid containers.

The EU is also scaling Deposit Return Systems (DRS) to secure high-quality recycled material, ensuring a robust feedstock supply for rigid paper packaging production. The Ecodesign for Sustainable Products Regulation (ESPR), effective from mid-2024, introduces the Digital Product Passport, improving transparency and compliance across the packaging value chain. Restrictions on PFAS in food contact packaging (effective August 2026) are accelerating R&D into non-toxic barrier layers. Leading companies such as Stora Enso are responding with large-scale investments, including a $1 billion board line in Finland, expected to deliver 750,000 tons of annual capacity, reinforcing Europe’s role as a global leader in sustainable rigid paper packaging.

United States: Recycling Goals and Corporate Innovation Boosting Rigid Paper Containers

The U.S. rigid paper containers market is driven by the EPA’s national recycling target to raise recycling rates to 50% by 2030, alongside Extended Producer Responsibility (EPR) laws in seven states. Maryland’s mandate that Producer Responsibility Organizations (PROs) cover at least 90% of waste management costs by 2030 is reshaping supply chains toward circularity.

Investments in recycling and manufacturing infrastructure are strengthening local production. For example, Saica Group is investing $110 million in a new corrugated manufacturing facility in Anderson, Indiana, boosting domestic capacity. Innovation is accelerating, with Sonoco’s Paper Can with Paper Bottom representing a breakthrough: it is over 90% paper-based and made with 100% recycled paperboard, including 85–90% post-consumer recycled content. These advancements align with consumer preferences for sustainable, lightweight, and fully recyclable rigid paper packaging.

China: E-Commerce Growth and Green Policies Driving Rigid Paper Containers

The China rigid paper containers market is heavily shaped by regulatory reforms under the “14th Five-Year Plan”. The NDRC and MEE are tightening controls on plastic pollution, boosting demand for eco-friendly rigid paper formats. Effective June 1, 2025, express delivery companies are required to adopt eco-friendly and reusable packaging, providing a major boost to corrugated paper boxes and rigid paper containers.

China’s Dual Circulation strategy is fueling domestic demand growth, particularly in the booming e-commerce sector, where rigid paper packaging is critical for durability and sustainability. Major logistics firms such as JDL Express and SF Express are already adopting reusable circulation boxes to replace single-use formats. Additionally, government tax incentives for remanufacturing and green technologies are pushing companies to invest in sustainable materials, reinforcing the role of rigid paper packaging in China’s transition toward circular economy practices.

India: EPR Expansion and Cold Chain Growth Stimulating Rigid Paper Containers

The India rigid paper containers market is growing rapidly under the Plastic Waste Management (Amendment) Rules, 2024, which extend EPR obligations to paper, glass, and metal packaging. These rules are pushing the adoption of paper-based rigid formats as alternatives to plastics. At the same time, the Food Safety and Standards Authority of India (FSSAI) is drafting new guidelines for rPET in food packaging, indirectly accelerating demand for hybrid paper-based solutions.

From April 1, 2025, PIBOs must include minimum recycled plastic content in rigid packaging, incentivizing paper-based solutions with minimal plastic barriers. The Indian Institute of Packaging (IIP) is actively promoting sustainable rigid paper packaging standards, aligning with government goals for eco-friendly manufacturing. Additionally, India’s rising demand for processed foods and beverages is driving growth in rigid paperboard containers and corrugated formats, making the country a key emerging hub for innovation in paper-based packaging.

Japan: Circular Economy Mandates Driving Advanced Paper-Based Rigid Packaging

The Japan rigid paper containers market is driven by the Plastic Resource Circulation Strategy, which mandates that all plastic packaging be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law (2025) requires redesign or reduction of 12 categories of single-use plastic products, directly boosting the demand for rigid paper alternatives.

Japanese companies are leading global innovation in barrier-coated and performance-enhanced paper solutions. Nippon Paper Industries’ SHIELDPLUS is a notable development, offering oxygen- and odor-impermeable paper packaging as a substitute for plastic laminates. Meanwhile, partnerships between companies like LyondellBasell and Shiseido to integrate bio-based PP with paper packaging formats reflect a growing hybrid-material trend. With a government goal to double renewable material use by 2030, Japan is establishing itself as a front-runner in rigid paper container technology.

Brazil: Reverse Logistics and Waste Import Ban Strengthening Rigid Paper Packaging

The Brazil rigid paper containers market is guided by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and waste reduction. The January 2025 enforcement of Law No. 15,088, banning the import of solid waste including paper and plastics, has incentivized the development of domestic recycling infrastructure to support rigid packaging.

The government is also promoting reverse logistics systems, placing responsibility on producers for post-consumer packaging collection and recycling. This has encouraged greater corporate accountability and investment in recyclable rigid formats such as corrugated paperboard containers. Additionally, Anvisa’s revised technical regulations for food-contact packaging are creating opportunities for rigid paper packaging that meets stricter health and safety standards. Combined with the growing demand for sustainable packaging in the food and retail sectors, Brazil is reinforcing its role as a regional leader in paper-based rigid packaging innovation.

Rigid Paper Containers Market Report Scope

Rigid Paper Containers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$455.1 Billion

|

|

Market Size (2034)

|

$730.6 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Corrugated Fibreboard, Paperboard, Molded Fiber, Kraft Paper), By Product Type (Boxes & Cartons, Tubes & Cylinders, Trays & Clamshells, Drums & Barrels, Sleeves & Dividers), By End-Use Industry (Food & Beverages, Consumer Goods, Electronics, Healthcare & Pharmaceuticals, E-commerce & Retail, Industrial Goods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Co., WestRock Company, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, DS Smith Plc, Mondi Group, Stora Enso Oyj, Rengo Co., Ltd., Huhtamaki Oyj, Greif, Inc., Oji Holdings Corporation, Billerud AB, Pactiv Evergreen Inc., Mayr-Melnhof Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Paper Containers Market Segmentation

By Material

- Corrugated Fibreboard

- Paperboard

- Molded Fiber

- Kraft Paper

By Product Type

- Boxes & Cartons

- Tubes & Cylinders

- Trays & Clamshells

- Drums & Barrels

- Sleeves & Dividers

By End-Use Industry

- Food & Beverages

- Consumer Goods

- Electronics

- Healthcare & Pharmaceuticals

- E-commerce & Retail

- Industrial Goods

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Paper Containers Market

- International Paper Co.

- WestRock Company

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- DS Smith Plc

- Mondi Group

- Stora Enso Oyj

- Rengo Co., Ltd.

- Huhtamaki Oyj

- Greif, Inc.

- Oji Holdings Corporation

- Billerud AB

- Pactiv Evergreen Inc.

- Mayr-Melnhof Group

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, data-driven methodology to deliver precise insights into the global rigid paper containers market. Our research integrates extensive secondary sources—including corporate sustainability reports, regulatory filings, academic studies, and industry publications—with primary interviews of key stakeholders, including manufacturers, brand owners, distributors, and end-users across food & beverages, consumer goods, healthcare, electronics, and e-commerce sectors. Market sizing and forecasting are derived from detailed analyses of material trends (corrugated fiberboard, paperboard, molded fiber, kraft paper), product innovations, regulatory frameworks (EU PPWR, ESPR, U.S. EPR laws, China’s 14th Five-Year Plan, India’s Plastic Waste Management rules, and Japan’s Circular Economy mandates), and sustainability-driven adoption of recycled and bio-based materials. USDAnalytics also examines corporate investments, mergers and acquisitions, barrier coating technologies, molded fiber solutions, digital watermarking, and lightweighting strategies to provide actionable intelligence on market growth, competitive positioning, and end-use segmentation. This methodology ensures that industry professionals receive a holistic, accurate, and actionable perspective on trends, innovations, and opportunities shaping the rigid paper containers market globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.