Packaging Paper Market Set to Reach $94.1 Billion by 2034, Driven by E-Commerce Growth and Sustainability

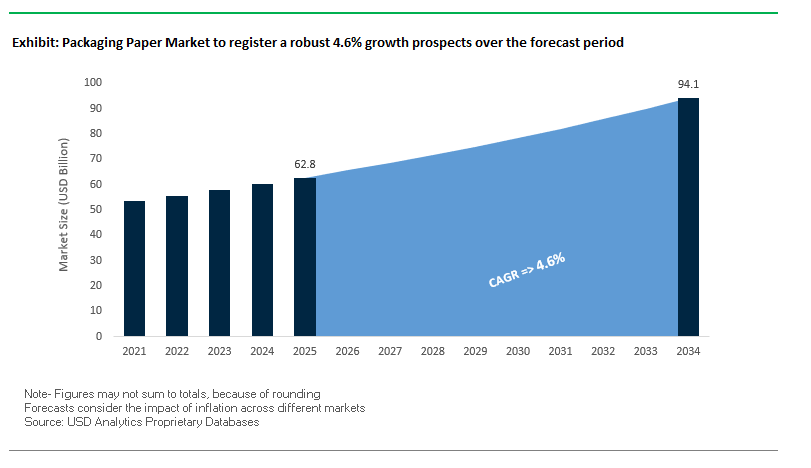

The Global Packaging Paper Market is projected to grow from $62.8 billion in 2025 to $94.1 billion by 2034, reflecting a CAGR of 4.6%. This growth is fueled by the increasing demand for eco-friendly, high-performance paper solutions that protect, preserve, and present goods across industries. Paper packaging, including corrugated boxes, folding cartons, and paper bags, is central to e-commerce, retail, and supply chain efficiency, offering superior printability, lightweighting, and recyclability.

Key Insights for Industry Professionals:

- E-commerce Driving Demand: Growth in online retail is creating a need for protective, right-sized, and easily shippable paper packaging, emphasizing material strength and durability.

- Sustainability at the Core: Brands are transitioning from plastic to renewable, recyclable, and biodegradable paper, responding to consumer demand and regulatory pressure.

- Enhanced Brand Appeal: Advanced paperboard with superior print surfaces and vibrant graphics allows companies to use packaging as a marketing tool.

- Lightweighting and Cost Reduction: Innovation in thinner, yet strong materials reduces raw material use, lowers shipping costs, and decreases carbon footprint.

- Compliance and Circularity: Paper solutions align with circular economy initiatives and meet evolving sustainability standards.

Market Developments Highlighting Strategic Expansion and Eco-Friendly Packaging Innovations

The Packaging Paper Industry has experienced dynamic strategic movements emphasizing sustainability, operational optimization, and product innovation. In August 2025, Mondi launched Ad/Vantage Smooth Brown Semi Extensible, a high-performance paper for demanding packaging applications, while International Paper announced the sale of its Global Cellulose Fibers business for $1.5 billion, focusing on sustainable packaging solutions.

In July 2025, Smurfit WestRock plc implemented significant capacity reductions and closed several U.S. and German facilities to optimize operational efficiency. Mondi also introduced the re/cycle PaperPlus Bag Advanced, a high-barrier paper bag for humidity-sensitive products. Earlier in June 2025, Mondi partnered with Saga Nutrition to launch a sustainable paper-based pet food pouch, while Stora Enso introduced Performa Nova, a fiber-based solution aiding brands in plastic reduction and sustainability compliance.

Other strategic moves include International Paper’s $9.9 billion acquisition of DS Smith in April 2025, expanding its European footprint, Smurfit Kappa’s acquisition of WestRock in November 2024, forming a global packaging giant, and ProAmpac’s September 2024 launch of ProActive RP-1000, a recyclable, high-barrier paper solution.

Trends and Opportunities Transforming the Packaging Paper Market

Unprecedented Demand Driven by Plastic Substitution Mandates

The packaging paper market is experiencing accelerated growth as plastic bans and substitution mandates reshape material choices across industries. Governments worldwide are implementing strict restrictions on single-use plastics, forcing brand owners and retailers to transition toward fiber-based packaging solutions. In India, the Plastic Waste Management (Amendment) Rules, 2022, banned several low-utility, high-littering plastic items, fueling demand for paper-based cutlery, straws, and food packaging. Similarly, the EU Single-Use Plastics Directive has banned multiple plastic formats, providing a powerful regulatory tailwind for paper.

Corporate ESG commitments are amplifying this shift. IKEA’s pledge to eliminate plastic from consumer packaging by 2028 and Amazon’s elimination of single-use plastic packaging in India highlight the global scale of corporate-driven demand for packaging paper. At the same time, Extended Producer Responsibility (EPR) fee modulation is giving brands a direct financial incentive to adopt recyclable, paper-based solutions, as recyclable formats reduce their compliance costs. Finally, consumer surveys reveal that buyers are increasingly willing to pay a premium for recyclable, renewable packaging, reinforcing the market’s long-term trajectory toward fiber-based formats.

Strategic Investment in Recycled Paperboard Capacity to Secure Supply

The structural shift toward paper has triggered multi-billion-dollar investments in recycled paperboard production. Companies like International Paper and DS Smith, following their merger, are actively scaling recycled fiber operations to strengthen vertical integration and secure raw material supply. This consolidation ensures consistent access to high-quality recycled paperboard, reducing dependency on external suppliers.

Capacity expansion is a critical focus. For example, DS Smith’s €13 million investment in its Romanian production site is increasing output capacity by more than 20% while directly supporting plastic replacement initiatives with customers. Across North America and Europe, paperboard mills are being upgraded or newly constructed to handle higher volumes of recycled content, ensuring that supply meets the surge in demand driven by regulatory mandates and retailer requirements. This wave of investment highlights the industry’s proactive response to the global paper packaging boom.

Development of High-Barrier, Functional Paper Coatings

A major opportunity lies in advancing functional coatings that give paper packaging the same barrier properties once exclusive to plastics. Innovations like Toppan’s GL-X-P barrier-coated paper demonstrate this potential, offering strong oxygen and water vapor resistance while achieving a 35% reduction in CO₂ emissions compared to plastic laminates.

Companies are actively developing repulpable, water-based, and bio-based coatings that ensure recyclability while maintaining performance. H.B. Fuller’s diversified coatings portfolio is an example of tailored solutions for application-specific needs, from moisture resistance to grease protection. Future innovations are targeting retortable paper packaging that can withstand sterilization processes. For instance, UPM Specialty Papers’ collaboration with Eastman to introduce compostable biopolymer coatings provides oxygen and grease barriers suitable for food packaging, addressing one of the toughest challenges—replacing multi-material retort pouches with fully paper-based alternatives.

Integration of Digital Watermarking for Intelligent Recycling

Another transformative opportunity lies in digital watermarking technology for recycling optimization. The HolyGrail 2.0 initiative validated its industrial-scale feasibility in 2025, proving that digital watermarks can enable high-speed, SKU-level sortation of paper packaging. By distinguishing food-grade from non-food-grade paperboard, this technology generates cleaner recycling streams, improving both quality and commercial value of recycled paper.

The integration of digital watermarks paves the way for a digital product passport system, enhancing traceability and compliance with circular economy mandates. Early pilots by Procter & Gamble and Nestlé in Europe show strong corporate interest, signaling that this innovation is approaching commercial adoption. For brands, the technology enhances EPR compliance, recycling efficiency, and consumer trust, while recyclers gain a stronger business case for upgrading sorting lines with watermark-reading modules.

Leading Packaging Paper Companies Driving Innovation, Sustainability, and Global Market Growth

The Packaging Paper Market is shaped by companies leveraging materials science, vertical integration, and sustainability to deliver high-performance, cost-effective, and eco-friendly solutions for diverse industries.

Smurfit WestRock: Combining Scale and Sustainability to Optimize Global Paper Packaging

Smurfit WestRock was formed by the merger of Smurfit Kappa and WestRock, creating a global leader in paper-based packaging. Its vertically integrated operations cover sustainable forestry, paper manufacturing, and converting, ensuring a consistent supply of high-quality materials. In July 2025, the company closed select mills in the U.S. and Germany to streamline operations and improve profitability. Its offerings include containerboard, corrugated board, and paper-based bags, designed for both industrial and consumer applications. The strategic focus is on circularity, recyclability, and global delivery of innovative paper solutions.

International Paper Company: Expanding Sustainable E-Commerce Packaging Capabilities

International Paper is a leader in fiber-based packaging and pulp, with vertically integrated operations ensuring consistent quality and supply. In August 2025, the company sold its Global Cellulose Fibers business to focus on sustainable packaging and invested $250 million in its Riverdale mill to produce containerboard for e-commerce demand. Key products include containerboard, corrugated boxes, and specialty paper packaging, supporting a wide range of consumer goods. Its strategy emphasizes innovation, operational excellence, and sustainability to meet evolving global market needs.

Mondi Group: Innovating High-Barrier and Sustainable Paper Solutions for Consumer Goods

Mondi provides a broad range of paper and plastic-based packaging, emphasizing sustainability and innovation. In June 2025, it partnered with Saga Nutrition to launch a paper-based pet food pouch and introduced the re/cycle PaperPlus Bag Advanced. Mondi’s portfolio includes flexible laminates, paper sacks and bags, and corrugated boards, with products like PerFORMing paper-based laminates highlighting eco-friendly performance. The company focuses on reusable, recyclable, and compostable solutions to align with global sustainability trends.

Billerud AB: Pioneering High-Performance Virgin Fiber Solutions to Reduce Plastic Dependence

Billerud specializes in virgin fiber-based paper and packaging materials, offering superior strength, printability, and eco-efficiency. Collaborations such as with Moelven Wood demonstrate innovation in replacing plastics with paper-based shrink wraps and caps. Billerud provides liquid packaging boards, sack paper, and containerboard, including FibreForm Caps as a recyclable alternative to traditional metal caps. The company’s strategy focuses on leading sustainable packaging transformation through high-performance materials.

Stora Enso Oyj: Leveraging Renewable Materials to Enable Circular Economy Packaging

Stora Enso provides renewable packaging, biomaterials, and paper solutions, with expertise in sustainable forestry and fiber-based innovation. In June 2025, it launched Performa Nova, a fiber-based board aiding brands in plastic reduction and compliance. Its product portfolio includes consumer board for liquid packaging, food service packaging, and luxury paperboard (Ensocoat™). The strategic focus is on renewable, sustainable solutions to help customers transition away from fossil-based packaging and advance the circular economy.

Packaging Paper Market Share Insights, 2025-2034

Corrugated Boxes Dominate Market Share by Product Type in the Packaging Paper Industry

Corrugated boxes account for 55% of the global packaging paper market, establishing themselves as the undisputed leader in terms of volume and value. Their dominance is directly tied to the rapid expansion of e-commerce and logistics, where corrugated boxes are indispensable for shipping, protection, and branding. Their strength-to-weight ratio, stackability, and customization flexibility make them critical for global supply chains, allowing businesses to optimize shipping costs while ensuring durability. Folding cartons, sacks, bags, and liquid cartons also play important roles, but none match the scalability and versatility of corrugated formats. Sustainability trends are accelerating corrugated adoption further, with recycled kraft liners, lightweight fluting, and digital printing for on-box branding becoming industry standards. While folding cartons continue to grow in premium F&B and pharmaceutical sectors, and paper sacks are rising in industrial bulk and retail shopping, corrugated packaging remains the central pillar of the packaging paper industry, driving both volume and technological investment.

E-commerce and Logistics Lead Market Share by Application in the Packaging Paper Industry

E-commerce & logistics represent 40% of global demand for packaging paper, positioning this segment as the largest end-use application. The explosive rise of online retail has made corrugated boxes, protective paper wraps, and mailers the backbone of distribution. Key drivers include right-sizing to reduce dimensional weight charges, lightweighting to cut emissions, and high-strength board grades to prevent product damage in transit. Beyond pure functionality, e-commerce packaging is increasingly used as a branding tool, with companies deploying printed boxes, branded tapes, and recyclable inserts to enhance unboxing experiences. Food & beverage remains a close second, using folding cartons, liquid cartons, and sacks for cereals, beverages, dairy, and frozen goods, but its share is gradually eroded by the surge in digital commerce. Industrial, pharmaceutical, and cosmetics applications provide value-driven niches—industrial relying on heavy-duty sacks, pharmaceuticals on high-quality compliant cartons, and cosmetics on specialty paper finishes for premium shelf appeal—yet none match the sheer scale of e-commerce-driven corrugated consumption.

United States Packaging Paper Market Strengthened by EPR Laws and AF&PA Recycling Initiatives

The United States packaging paper market is shaped by regulatory shifts and sustainability-driven policies. A major influence is the GS1 Sunrise 2027 Project, which will transition to 2D barcodes and expand the use of smart packaging, directly impacting packaging paper applications. At the state level, Extended Producer Responsibility (EPR) laws in Maine, Maryland, and Washington are driving producers to adopt recyclable and paper-based solutions, reducing reliance on plastics. On the government front, the American Forest & Paper Association (AF&PA) reported in July 2025 that packaging paper and specialty packaging shipments rose 5% year-on-year, while U.S. paper recycling rates reached 60–64% and cardboard recycling stood even higher at 69–74%, confirming strong momentum for circular paper packaging.

Corporate action is aligning with these trends. In August 2025, companies like General Mills, Mars, and PepsiCo launched the US Flexible Film Initiative (USFFI), aimed at boosting recycling infrastructure for flexible packaging. This complements the industry’s shift toward mono-material, recyclable paper-based packaging structures, which deliver the barrier properties of plastics but are fully recyclable. Demand is strongest in e-commerce, food and beverages, and consumer packaged goods (CPG), where durable, lightweight, and sustainable paper-based formats ensure both regulatory compliance and consumer appeal.

Germany Packaging Paper Market Boosted by PPWR and Circular Economy Leadership

Germany’s packaging paper market is heavily influenced by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This framework imposes ambitious recyclability and reuse targets, restricts single-use plastics, and mandates minimum recycled content levels by 2030 and 2040. In parallel, the German Packaging Act (VerpackG)—expanded in 2022—sets high recycling rate targets for paper, glass, and plastics, fueling demand for advanced recycling and sorting technologies.

The country’s focus on transparent labeling and recyclability disclosure, to be enforced from 2025, ensures packaging papers must clearly indicate material composition and end-of-life options. Demand is particularly strong in folding cartons, corrugated boxes, and paper bags for the food, beverage, and cosmetics sectors, where paper continues to replace plastics. Germany’s strong recycling infrastructure, combined with its innovation in circular economy packaging materials, positions it as a leader in developing sustainable paper packaging solutions across Europe.

China Packaging Paper Market Expands Under Dual-Carbon Goals and E-Commerce Growth

China’s packaging paper market is advancing rapidly under the government’s dual-carbon strategy, which aims for carbon peaking by 2030 and carbon neutrality by 2060. Regulations in the express delivery sector, effective from June 2025, are compelling logistics providers and e-commerce platforms to adopt environmentally friendly and reusable packaging papers. This is particularly critical in a country where parcel deliveries surged to 175 billion units in 2024, underscoring the need for durable, efficient, and sustainable paper-based solutions.

The regulatory landscape is also evolving, with the GB 7718-2025 national food labeling standard, effective March 2027, requiring allergen disclosure and stricter oversight of claims like “free of.” These policies are pushing demand for high-quality printed packaging paper with improved traceability. At the same time, manufacturers are investing in automation, AI-driven quality control, and smart regulatory platforms to meet safety and efficiency standards. Rising demand is concentrated in consumer goods, e-commerce, food processing, and electronics packaging, where paper offers both cost efficiency and regulatory compliance advantages over plastics.

India Packaging Paper Market Driven by PLI Schemes and Food Processing Expansion

The packaging paper market in India is being boosted by government initiatives such as Make in India and the Production Linked Incentive (PLI) scheme, which support domestic manufacturing capacity. The EPR mandate for 30% recycled content in rigid plastics by April 2025 is also accelerating substitution toward paper-based alternatives. These policies are creating fertile ground for investments in sustainable packaging papers, especially as the country seeks greater industrial self-reliance.

India is also witnessing rapid technological adoption. Robotics, AI, and smart packaging innovations are being integrated into production lines to reduce labor costs and improve efficiency. In May 2024, Andhra Paper Limited announced a $14.4 million agreement with Valmet AB for a new tissue paper line, building on its $31.1 million investment in Andhra Pradesh for paper production machinery. The food and beverage sector, especially the on-the-go and online retail categories, is the largest consumer of packaging paper, with demand increasing for convenient, recyclable, and lightweight formats. Together, industrial expansion and consumer demand are reinforcing India’s strong role in the global packaging paper market.

Japan Packaging Paper Market Advanced by Positive List Regulation and Innovation in Barrier Papers

Japan’s packaging paper market is evolving under the positive list system for food-contact materials, which came into effect on June 1, 2025. This regulation defines which synthetic substances can be used, pushing companies to adopt paper-based alternatives in food applications. Regulatory developments also include widespread e-labeling supported by QR codes, which enhance transparency and supply chain traceability.

Japanese manufacturers are global leaders in innovative and functional paper packaging. For instance, Nippon Paper Industries developed SHIELDPLUS, a barrier-coated paper offering plastic-like protection while maintaining recyclability. These innovations align with Japan’s broader sustainability agenda, which targets a 46% reduction in GHG emissions by 2030 and net zero by 2050. The government’s planned introduction of 2 million tonnes per year of bio-PP by 2030 will further favor paper-based formats over plastics. Strongest demand comes from ready-to-drink tea, coffee, and snack packaging, where Japanese consumers value lightweight, aesthetically pleasing, and environmentally responsible packaging paper.

Packaging Paper Market Report Scope

Packaging Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$62.8 Billion

|

|

Market Size (2034)

|

$94.1 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Folding Cartons, Corrugated Boxes, Sacks & Bags, Liquid Cartons, Others), By Grade (Containerboard, Boxboard, Kraft Paper, Specialty Paper), By Application (Food & Beverage, Healthcare & Pharmaceutical, Personal Care & Cosmetics, E-commerce & Logistics, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Mondi Group, DS Smith Plc, Nippon Paper Industries Co., Ltd., Oji Holdings Corporation, Smurfit Kappa Group Plc, WestRock Company, Graphic Packaging Holding Company, Stora Enso Oyj, Klabin S.A., UPM, Sonoco Products Company, Billerud AB, Rengo Co., Ltd., Asia Pulp & Paper Group (APP)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Paper Market Segmentation

By Product Type

Folding Cartons

Corrugated Boxes

Sacks & Bags

Liquid Cartons

Others

By Grade

Containerboard

Boxboard

Kraft Paper

Specialty Paper

By Application

Food & Beverage

Healthcare & Pharmaceutical

Personal Care & Cosmetics

E-commerce & Logistics

Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Paper Market

- International Paper Company

- Mondi Group

- DS Smith Plc

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Smurfit Kappa Group Plc

- WestRock Company

- Graphic Packaging Holding Company

- Stora Enso Oyj

- Klabin S.A.

- UPM

- Sonoco Products Company

- Billerud AB

- Rengo Co., Ltd.

- Asia Pulp & Paper Group (APP)

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-layered research methodology to provide an in-depth and actionable analysis of the Global Packaging Paper Market. Our approach combines primary research, including interviews with key stakeholders such as manufacturers, distributors, retailers, and industry experts, with secondary research sourced from corporate reports, regulatory publications, trade journals, and sustainability frameworks. Quantitative modeling is applied to forecast market growth from 2025 to 2034, considering product types (corrugated boxes, folding cartons, sacks & bags, liquid cartons, and others), grades (containerboard, boxboard, kraft paper, specialty paper), and applications (food & beverage, healthcare, personal care, e-commerce & logistics, and industrial sectors). The methodology also integrates analysis of technological innovations, such as high-barrier coatings, lightweighting, digital watermarks for recycling optimization, and sustainable paper alternatives replacing plastics. Regional insights cover critical markets including the U.S., Germany, China, India, and Japan, highlighting regulatory frameworks like EPR, PPWR, Single-Use Plastics Directive, GB 7718-2025, and Japan’s Positive List system. Additionally, competitive intelligence is drawn from strategic investments, mergers, capacity expansions, and sustainability initiatives by leading players including International Paper, Smurfit WestRock, Mondi Group, Billerud AB, and Stora Enso. By combining market dynamics, regulatory drivers, and technological advancements, USDAnalytics delivers precise insights tailored for industry professionals seeking eco-friendly, cost-efficient, and high-performance paper packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.